Electronic Adhesives Market Outlook:

Electronic Adhesives Market size was valued at USD 6.7 billion in 2025 and is predicted to cross USD 16.6 billion by the end of 2035, expanding at more than 9.5% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of electronic adhesives is assessed at USD 7.3 billion.

The electronic adhesives market is set for upward momentum propelled by the expansion of semiconductor fabrication, advanced packaging, and electronics assembly capacity. These electronic adhesives are utilized in chip packaging, thermal management, component attachment, and printed circuit board assembly, which makes demand very closely tied to semiconductor output and electronics manufacturing activity. In February 2025, the Semiconductor Industry Association revealed that global semiconductor sales reached a substantial USD 630.5 billion in 2024, which is a 19.1% increase from USD 526.8 billion in 2023, driven by strong demand across computing, artificial intelligence, communications, automotive, and industrial applications. Growth was led by the Americas, in which sales increased 44.8%, whereas memory products represented the strongest product-level expansion. This sustained rise in semiconductor production also supports upstream demand for electronic materials, including specialty adhesives used in chip packaging, assembly, and thermal management.

Global Semiconductor Market Overview 2024: Growth and Regional Performance Trends

|

Indicator (USD Billion) |

2023 |

2024 |

Growth (%) |

|

Global Semiconductor Sales |

526.8 |

630.5 |

19.1% |

|

Q4 Semiconductor Sales |

145.9 |

170.9 |

17.1% |

|

December Monthly Sales |

- |

57.0 |

- |

|

Logic Product Sales |

- |

212.6 |

Largest segment |

|

Memory Product Sales |

92.3 |

165.1 |

78.9% |

Source: SIA

Key Electronic Adhesives Market Insights Summary:

Regional Highlights:

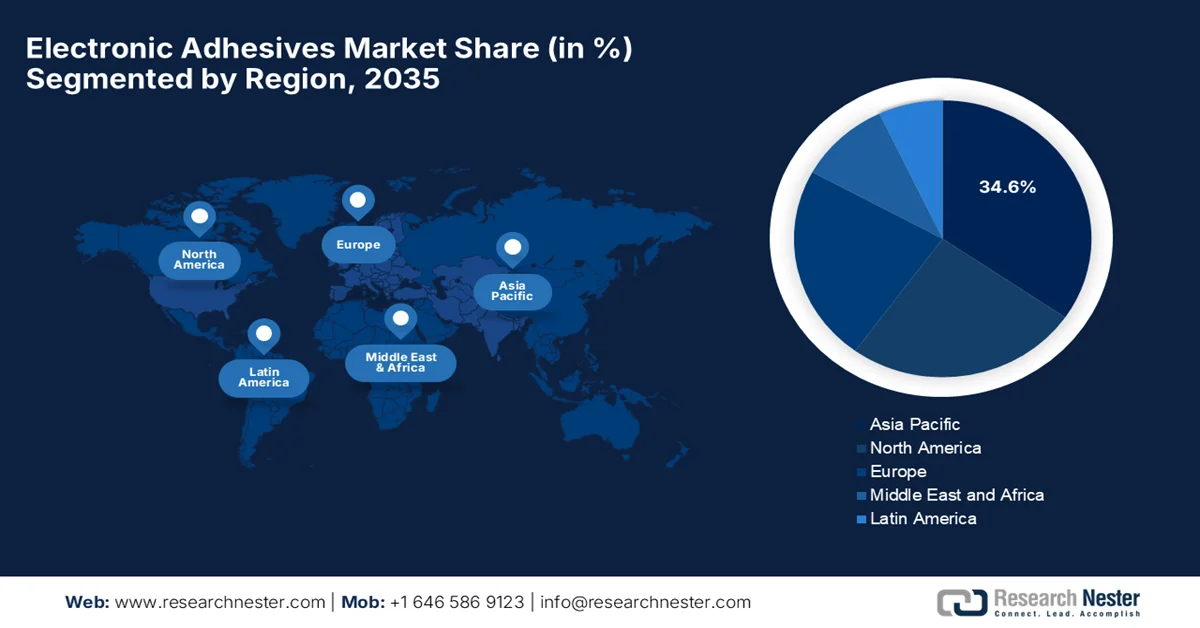

- The electronic adhesives market in Asia Pacific is expected to secure a 34.6% share by 2035, bolstered by its leadership in semiconductor fabrication and consumer electronics manufacturing across key economies such as China, Taiwan, South Korea, and Japan

- North America is poised for notable expansion throughout 2026-2035, stimulated by advancements in aerospace, defense, medical devices, and smart industrial automation requiring high-performance adhesive solutions

- The U.S. electronic adhesives market captures 80.5% of the share in North America owing to the extensive production of consumer electronics, automotive electronics, aerospace systems, and semiconductor components

Segment Insights:

- In the electronic adhesives market, the epoxy segment is forecast to account for 36.5% of the market by 2035, fueled by its superior mechanical strength, thermal stability, and dependable electrical insulation for high-density electronic assemblies

- The surface mounting segment is anticipated to hold a considerable revenue share by 2035, supported by increasing device miniaturization and the need for cost-efficient, high-speed, and precise electronics assembly processes

Key Growth Trends:

- Growth of electric vehicles and automotive electronics

- Expansion of consumer electronics

Major Challenges:

- Volatility in raw material prices

- Technical & engineering challenges

Key Players: Henkel AG & Co. KGaA (Germany), 3M Company (U.S.), H.B. Fuller Company (U.S.), Dow Inc. (U.S.), Sika AG (Switzerland), Arkema S.A. (Bostik) (France), DELO Industrial Adhesives (Germany).

Global Electronic Adhesives Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.7 billion

- 2026 Market Size: USD 7.3 billion

- Projected Market Size: USD 16.6 billion by 2035

- Growth Forecasts: 9.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (34.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, South Korea, Taiwan

- Emerging Countries: India, Vietnam, Thailand, Malaysia, Indonesia

Last updated on : 16 June, 2026

Electronic Adhesives Market - Growth Drivers and Challenges

Growth Drivers

- Growth of electric vehicles and automotive electronics: The heightening adoption of electric vehicles and automotive electronics deliberately fuels demand in the market. They are used extensively in battery systems, sensors, ECUs, and power electronics for vibration resistance, thermal stability, and durability. In this context, the International Energy Agency revealed that global electric car sales surpassed a significant value of 20 million in 2025, expanding around 20% from 2024, whereas EVs accounted for 25% of all new car sales worldwide. Besides, China was identified to be the dominant EV market, contributing more than half of global sales with over 13 million electric cars sold in 2025 and nearly 55% domestic sales share. Europe also saw strong growth of over 30%, whereas the U.S. showed relatively stable EV sales at around 1.5 million units, thus making it suitable for standard market growth.

- Expansion of consumer electronics: The demand for smartphones, laptops, tablets, and wearable devices has been surging, which is uplifting the overall market. These adhesives also improve aesthetics and device durability, thereby supporting rapid innovation cycles and high-volume manufacturing in the global industry. In January 2026, the article published by UN Trade & Development reported that global trade in ICT goods has surged, wherein the electronic components, such as chips and sensors, are driving growth and now accounting for over 12% of merchandise exports. The report also outlined that Asia dominates production, contributing nearly 80% of exports, whereas most of the developing economies are limited to low‑value assembly roles, risking exclusion from digital and energy transitions.

- Miniaturization of electronic devices: This is yet another major driver for the market. The components have become smaller and more complex, in which adhesives enable precise bonding in tight spaces, replace mechanical fasteners, and improve thermal management. Also, it enhances reliability in microelectronics, wearables, and semiconductor packaging, supporting continuous demand across advanced electronics manufacturing. In May 2025, the article published by Pacific Northwest National Laboratory disclosed that the semiconductor industry has introduced the MAPT Roadmap to provide unified strategic guidance for the next 5, 10, and 20 years. It was developed collaboratively by industry, academia, and government experts, and it sets ambitious goals for microelectronics and advanced packaging, propelling continued demand for electronic adhesives.

Challenges

- Volatility in raw material prices: One of the important hampering factors in the market is the volatility of raw material prices. These electronic adhesives are manufactured using epoxy resins, silicones, acrylics, polyurethanes, and specialty conductive fillers such as silver and copper. Therefore, any type of fluctuations in the prices of these materials, influenced by supply chain disruptions, geopolitical conflicts, energy costs, and changes in global demand, can significantly impact production costs and profit margins. Therefore, manufacturers find it difficult to pass these increased costs to customers owing to the intense market competition. In addition, dependence on a very limited number of suppliers for certain materials also creates procurement risks. As a result, companies need to optimize sourcing strategies and improve inventory management in order to maintain cost competitiveness and required performance standards.

- Technical & engineering challenges: The electronic devices are becoming smaller, lighter, and more powerful, posing technical challenges as an obstacle for the market. Extreme miniaturization of components reduces the available bonding area, and it forces manufacturers to develop adhesives with superior thermal conductivity, electrical insulation, and mechanical strength. In addition, any type of thermal-mismatch failure is considered to be a critical concern, especially in flexible and ultra-thin electronic assemblies where differences in the coefficient of thermal expansion between substrates and adhesives can lead to warping, cracking, or component failure. Apart from this, manufacturers need to operate within narrow process windows that require precise control over viscosity, dispensing accuracy, and curing conditions to avoid damaging heat-sensitive components.

Electronic Adhesives Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.5% |

|

Base Year Market Size (2025) |

USD 6.7 billion |

|

Forecast Year Market Size (2035) |

USD 16.6 billion |

|

Regional Scope |

|

Electronic Adhesives Market Segmentation:

Resin Type Segment Analysis

In the resin type segment, epoxy is anticipated to account for the largest share of 36.5% in the electronic adhesives market during the forecast period. The segment’s dominance is effectively propelled by its superior mechanical strength, strong adhesion to diverse substrates such as copper and silicon, excellent thermal stability, and reliable electrical insulation properties. This makes it highly suitable for compact and high-density electronic assemblies, including semiconductor packaging, PCB assembly, and surface mount technologies. In February 2026, the article published by World Metrics Organization reported that these epoxy resins play a critical role in the electronics sector, and it accounts for about 22% of global consumption, primarily used for encapsulation, die attach, underfill, and PCB laminates. This also enables miniaturized and high-density electronic assemblies, thus denoting a wider segment scope.

Application Segment Analysis

Under the application segment, surface mounting is projected to hold a considerable revenue share in the electronic adhesives market by the end of 2035. The ongoing miniaturization of electronic devices increases the need for precise and reliable adhesion. Surface mount technology is preferred due to its cost efficiency, high production speed, and reduced setup time, thereby enabling higher manufacturing output. In addition, it enhances overall device performance and functionality, making it a widely adopted assembly method in modern electronics manufacturing. Apart from this, surface mounting has the ability to support compact circuit designs, making it essential for smartphones, wearables, and advanced consumer electronics. It also reduces material usage and improves automation in assembly lines, further lowering production costs. The technology ensures better electrical performance by minimizing signal path lengths, making it feasible for standard market growth.

End user Segment Analysis

By the conclusion of forecasted years, consumer electronics are expected to grow with a noteworthy share in the electronic adhesives market. The widespread use of electronic products in daily life has strengthened this demand, with consumers prioritizing high-quality and durable devices. In addition, the growth of electric vehicles is also contributing significantly to market expansion, where high-performance adhesives are highly essential for securely bonding components and ensuring structural integrity in modern vehicle assemblies. In July 2023, Henkel expanded its portfolio of medical wearables by integrating advanced adhesives and electronic materials into healthcare applications such as smart patches, glucose monitors, and smart glasses. The company, with innovations like skin‑safe molding technology and ISO 10993‑tested medical device adhesives, delivers reliable, cost‑efficient solutions.

Our in-depth analysis of the electronic adhesives market includes the following segments:

|

Segment |

Subsegments |

|

Resin Type |

|

|

Application |

|

|

End user |

|

|

Form |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Electronic Adhesives Market - Regional Analysis

APAC Market Insights

The Asia Pacific electronic adhesives market is anticipated to capture the highest share of 34.6% during the discussed timeframe. The region’s upliftment is largely propelled by its status as the global hub for semiconductor fabrication and consumer electronics manufacturing. This momentum is being supported by industrial investments in mainland China, Taiwan, South Korea, and Japan, along with rapidly emerging assembly hubs in Southeast Asia and India. In April 2023, the George Washington University report revealed that Taiwan, South Korea, and Japan together account for more than 90% of global semiconductor production, underscoring the region’s central role in global chip supply chains. The report outlined that Taiwan leads advanced semiconductor manufacturing, South Korea dominates memory chip production, and Japan plays a key role in semiconductor materials and equipment, making it suitable for standard market growth.

The nation’s strong capacity for high-volume consumer electronics manufacturing and its leadership in vehicle electrification are responsibly uplifting China market. The country's surge in electric vehicle battery manufacturing and the widespread deployment of 5G telecommunications infrastructure are forcing a major shift toward high-performance, thermally conductive bonding solutions. For instance, in February 2022, Arkema announced the planned acquisition of Shanghai Zhiguan Polymer Materials, which is a specialist in hot‑melt polyurethane adhesives for consumer electronics, with the main goal of strengthening its engineering adhesives portfolio. These adhesives are widely used in bonding mobile phones, tablets, laptops, and connected devices, thereby supporting the country’s fast‑growing electronics market.

The country's strong government initiatives promoting localized production drive extensive growth in the market in India. This momentum is stimulated by the country’s nationwide rollout of 5G infrastructure and investments in aerospace and defense electronics, which are shifting industrial demand toward high-reliability die-attach and structural formulations. The government of India, in January 2026, approved 22 new proposals under the electronics component manufacturing scheme with projected investments of about USD 5 billion and production worth nearly USD 31 billion. These approvals generate close to 33,800 direct jobs and strengthen the country’s electronics manufacturing ecosystem, supporting its digital growth ambitions. Hence, with such government support and heightened electronic consumption, India will witness extensive growth in electronic adhesives in the next decade.

North America Market Insights

In North America, the electronic adhesives market is positioned for sustained and strategic growth mainly attributable to its strong emphasis on technological innovation, aerospace and defense manufacturing, and advanced automotive engineering. The region’s pioneering role in medical device technology, satellite communication hardware, and smart industrial automation readily accelerates the adoption of specialized, highly durable encapsulation and shielding adhesives. For instance, in September 2025, Power Adhesives announced the expansion of the U.S. distribution network to meet rising demand for Tecbond adhesives and applicators. The restructure consists of three exclusive partners, i.e., Applied Adhesives, GLS Products, and New Star Adhesives, each specializing in unique adhesive systems. These Tecbond solutions serve various applications, ensuring faster delivery and stronger technical support for customers in the U.S.

The aerospace innovation and high-tech automotive manufacturing are certain trends visibly reshaping the market in the U.S. In addition, the integration of complex computing hardware into autonomous driving systems and defense electronics forces a strong reliance on thermally conductive formulations for critical thermal management, which propels continued market growth. For instance, in May 2026, H.B. Fuller announced a new Aerospace Manufacturing Center of Excellence in Charlotte, North Carolina. This facility will integrate manufacturing, packaging, testing, and quality operations to support aviation, space, and defense customers under strict qualification and traceability standards. The center is designed to meet growing adhesive demand, thus allowing a steady cash influx in the U.S. electronic adhesives industry.

In Canada, the market has gained enhanced traction owing to the increasing miniaturization of electronic devices and the rapid expansion of the automotive electronics sector. Consumer demand for smart gadgets, wearables, and advanced healthcare devices fuels the need for reliable thermal management, electrically conductive, and encapsulating adhesive solutions. Major technological shifts toward automation and surface-mount technology encourage local manufacturers to adopt advanced UV-curing and eco-friendly adhesive formulations. For instance, in October 2023, Umicore announced a generous investment of USD 1.34 billion in a new EV battery materials plant in Loyalist, Ontario, to strengthen North America’s supply chain. The facility will produce both pCAM and CAM, critical components for high-performance rechargeable batteries, meeting rising EV battery demand, thus reflecting a steady demand for electronic adhesives.

Europe Market Insights

In Europe, the electronic adhesives market is growing due to the presence of stringent environmental regulations, which heavily influence the market, encouraging manufacturers to develop eco-friendly, halogen-free, and lead-free adhesive formulations. In addition, the regional push for industrial automation and smart grid infrastructure also drives innovation in high-precision, fast-curing adhesive technologies. In April 2026, DELO Industrial Adhesives announced the launch of five new IBOA- and TPO-free adhesives, enhancing biocompatibility for medical device applications. The company also notes that leading the lineup is DELO PHOTOBOND MG4202, offering ultra-fast curing and wide temperature resistance, while MG4191 provides versatile strength without skin-sensitizing substances, thus expanding its medical electronics portfolio. Hence, with continued innovations, the market is projected to experience unprecedented growth in the upcoming years.

The prominent automotive manufacturing sector and its transition toward electric vehicles and autonomous driving technologies are rearranging the growth dynamics of the Germany market. Apart from this, the high demand for advanced driver-assistance systems and battery pack assemblies intensely fuels the need for thermal management materials and electrically conductive adhesives. In May 2024, Dow commenced commercial operations of a new VORATRON™ adhesive and gap filler production line at its Polyurethanes Systems House in Ahlen, Germany, with a primary focus to increase the production capacity tenfold to meet rising demand from the electric vehicle battery sector. The company’s high-performance polyurethane adhesives and thermally conductive gap fillers are especially designed to support battery assembly by enhancing structural bonding, thermal management, safety, and reliability.

The UK market is unfolding remarkable growth opportunities owing to the advanced motorsport engineering, which significantly accelerates the demand for reliable thermal management and battery bonding solutions. Medical device manufacturing and Internet-of-Things hardware also propel the need for high-precision encapsulants and electrically conductive adhesives. Apart from this, a strong domestic focus on academic research and clean-energy innovation encourages local manufacturers to adopt smart, fast-curing, and environmentally compliant adhesive chemistries. For instance, Power Adhesives in June 2025 announced a distribution partnership with Antala Ltd. to expand the availability of its hot melt adhesive solutions across the UK market. Under the agreement, Antala will distribute Power Adhesives’ core product portfolio, which includes Tecbond biodegradable adhesives and specialized ranges such as Knottec, Casttec, and Foundrytec.

Key Electronic Adhesives Market Players:

- Henkel AG & Co. KGaA (Germany)

- 3M Company (U.S.)

- H.B. Fuller Company (U.S.)

- Dow Inc. (U.S.)

- Sika AG (Switzerland)

- Arkema S.A. (Bostik) (France)

- DELO Industrial Adhesives (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Henkel AG & Co. KGaA is the most influential player in the market, and it provides conductive adhesives, thermal management materials, and certain semiconductor packaging solutions. In addition, the company maintains a strong presence across Asia Pacific, North America, and Europe, and it serves applications, i.e., consumer electronics, automotive electronics, and industrial applications.

- 3M Company is a prominent supplier of electronic adhesives and tapes, which are being used in smartphones, displays, wearables, semiconductor assemblies, and automotive electronics. The firm possesses a diversified technology platform that enables the development of adhesive solutions with enhanced thermal conductivity, electrical performance, and durability.

- H.B. Fuller Company has established itself as a significant player in specialty electronic adhesives, and it is providing suitable solutions for circuit protection, semiconductor packaging, surface mounting, and electronic component assembly. The company is highly focused on strategic acquisitions, product portfolio expansion, and customer-focused innovation with the main goal of enhancing its market presence.

- Dow Inc. is yet another dominant force in this sector and is a leading provider of silicone-based electronic adhesives, encapsulants, and thermal interface materials that offer support for advanced electronics manufacturing. The firm leverages its knowledge in materials science to develop products that are capable of meeting stringent requirements.

- Sika AG deliberately expanded its presence in the electronic adhesives industry through continuous product innovation as well as strategic acquisitions that enhance its specialty chemicals portfolio. The company offers advanced bonding and protection solutions that are suitable for electronic components, automotive electronics, battery systems, and industrial equipment.

Here is a list of key players operating in the global market:

Henkel, 3M, Dow, H.B. Fuller, and Sika have registered themselves as the leading players in the electronic adhesives market as they compete through continuous product innovation, advanced material development, and strong global distribution networks. Market participants are making heavy investments in terms of R&D to develop high-performance conductive, thermally conductive, and environmentally sustainable adhesive solutions that are suitable for semiconductor packaging, electric vehicles, consumer electronics, and miniaturized devices. For instance, in January 2026, Henkel signed an agreement to acquire ATP adhesive systems, which is a prominent player in high‑performance water‑based specialty tapes, thereby expanding its adhesive technologies portfolio beyond liquid adhesives and thus strengthening the market’s growth potential.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, DELO introduced its next-generation light-activatable adhesives, which are designed for high-volume LiDAR production, and it achieves handling strength in minutes instead of an hour, thereby enabling up to five times faster throughput.

- In April 2026, Bostik won the ACS Innovation Award 2026 for its bio‑based instant adhesive Born2Bond Ultra K85, recognized at the ASC Convention & Expo in Nashville. The adhesive combines 60% renewable raw materials with exceptional durability, setting new benchmarks in sustainability and long‑term performance for the industry.

- Report ID: 8615

- Published Date: Jun 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.