Polyurethane (PU) Adhesives in Electronics Market Outlook:

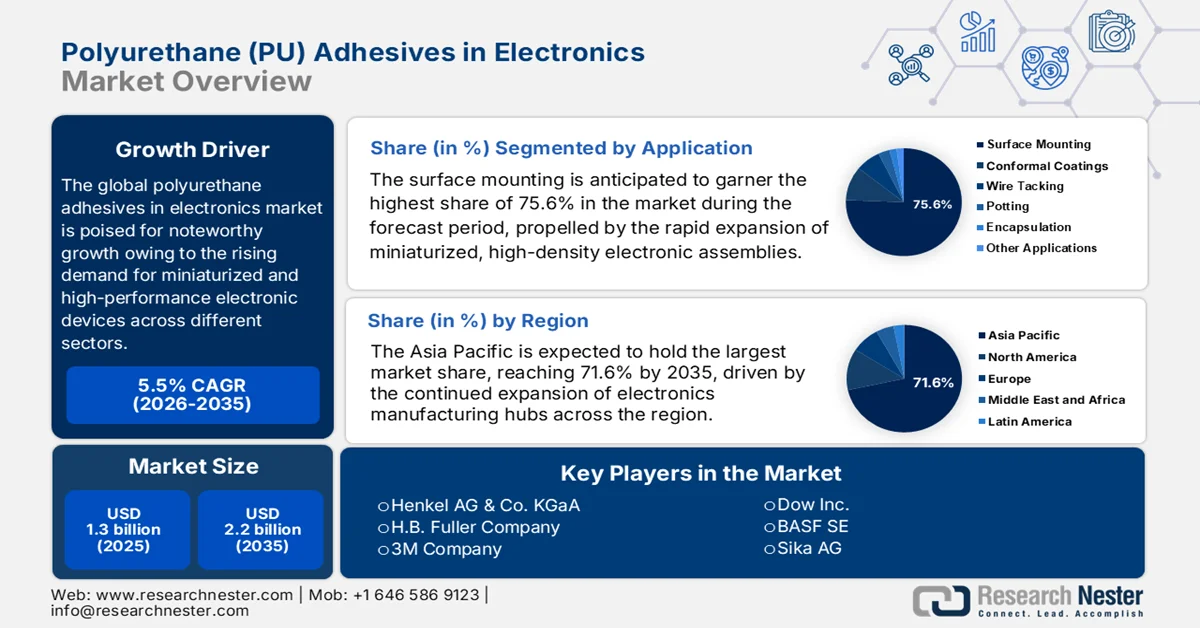

Polyurethane (PU) Adhesives in Electronics Market size was over USD 1.3 billion in 2025 and is projected to cross USD 2.2 billion by the end of 2035, growing at more than 5.5% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of polyurethane adhesives in electronics is estimated at USD 1.37 billion.

The global polyurethane adhesives in electronics market is projected for steady expansion in the next decade, owing to the heightened demand for lightweight and high-performance electronic devices in consumer electronics, automotive electronics, industrial equipment, and telecommunications applications. Manufacturers are also highly focused on developing innovative formulations with enhanced curing efficiency, improved thermal conductivity, and compatibility with advanced electronic materials, contributing to the market’s positive long-term outlook. For instance, in May 2023, Henkel introduced Loctite TLB 9300 APSi, which is a first‑of‑its‑kind injectable thermally conductive adhesive especially designed to enhance EV battery safety and performance. The company also outlined that this two‑component polyurethane adhesive combines strong structural bonding with 3 W/mK thermal conductivity, electrical insulation, and sustainability benefits through solvent‑free, room‑temperature curing.

Top Global Import Shipments of Polyurethanes -2024 Country-wise Trade Leaders & Rankings

|

Country |

Import Value (USD Million) |

|

China |

673 |

|

U.S. |

505 |

|

Vietnam |

451 |

|

Germany |

429 |

|

India |

337 |

|

Italy |

329 |

|

Mexico |

325 |

|

Canada |

217 |

|

France |

213 |

|

Indonesia |

199 |

Source: OEC

Key Polyurethane (PU) Adhesives in Electronics Market Insights Summary:

Regional Highlights:

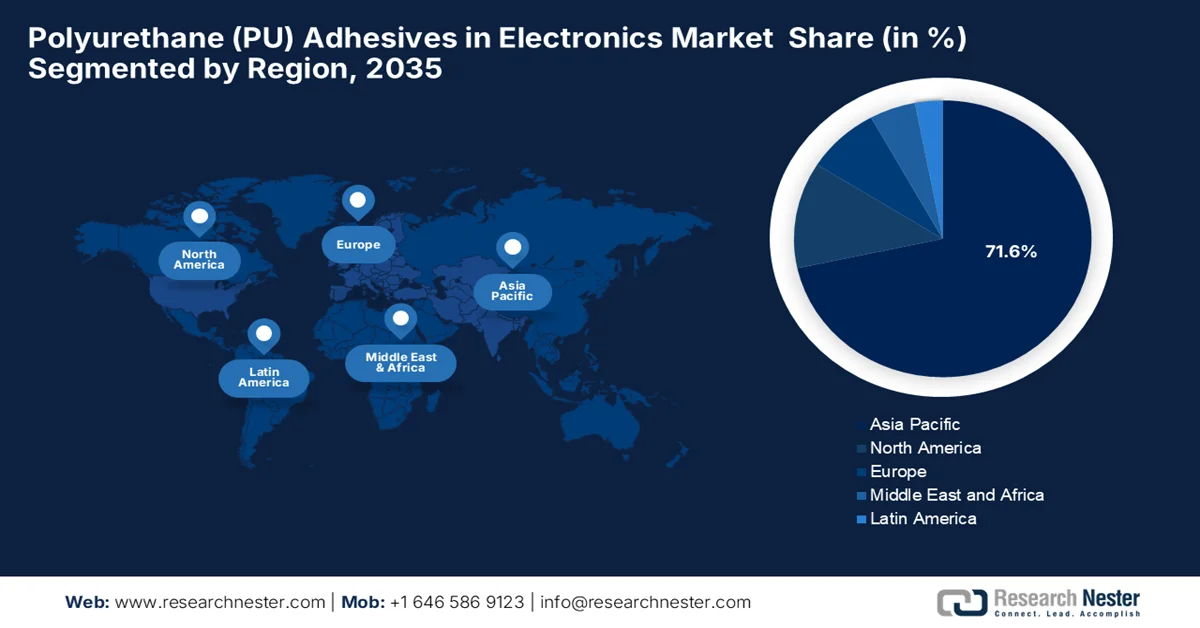

- The Asia Pacific is anticipated to capture 71.6% of revenue share by 2035, bolstered by the expansion of electronics manufacturing hubs across China, Japan, South Korea, and India

- North America is poised for steady growth in the polyurethane (pu) adhesives in electronics market throughout 2026-2035, catalyzed by the resurgence of domestic advanced manufacturing and aerospace electronics production

Segment Insights:

- In the polyurethane (pu) adhesives in electronics market, the surface mounting segment is projected to account for 75.6% share by 2035, underpinned by the rapid expansion of miniaturized, high-density electronic assemblies and increasing adoption of automated PCB assembly lines

- By 2035, the UV-curing PU adhesive segment is expected to secure a considerable revenue share, fueled by rising demand for rapid-curing, energy-efficient bonding solutions in high-speed electronics manufacturing environments

Key Growth Trends:

- Expansion of the consumer electronics industry

- Growth of electric vehicles and automotive electronics

Major Challenges:

- High performance and reliability requirements

- Volatility in raw material supply and pricing

Key Players: Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Dow Inc., BASF SE, Sika AG, Plexus, Arkema S.A. (Bostik), Avery Dennison Corporation, Huntsman Corporation, Ashland Inc., Panacol-Elosol GmbH, DELO Industrie Klebstoffe GmbH & Co. KGaA, Nitto Denko Corporation, ThreeBond Holdings Co., Ltd., Cemedine Co., Ltd., LG Chem Ltd., SKC Co., Ltd., Pidilite Industries Limited, Adhesive Technologies, Inc. Pty Ltd., Scigenics Sdn. Bhd.

Global Polyurethane (PU) Adhesives in Electronics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.3 billion

- 2026 Market Size: USD 1.37 billion

- Projected Market Size: USD 2.2 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (71.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, South Korea, Germany

- Emerging Countries: India, Vietnam, Mexico, Singapore, Malaysia

Last updated on : 8 June, 2026

Polyurethane (PU) Adhesives in Electronics Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of the consumer electronics industry: The growth in terms of smartphones, wearables, laptops, and smart home devices is readily increasing demand for PU adhesives. These adhesives are extensively used for bonding displays, batteries, and internal components, prompting a huge growth environment for the polyurethane (PU) adhesives in electronics market. As per the article published by the Press Information Bureau (PIB) in October 2025, India’s electronics sector witnessed a remarkable transformation wherein the production rose nearly sixfold to about USD 135 billion during the period 2024-25, driven by strong policy support such as PLI, SPECS, and ECMS. Mobile manufacturing and exports have surged dramatically, making India the world’s second-largest mobile phone producer as well as a key global export hub. This rapid expansion has strengthened domestic value chains, attracted more than USD 4 billion in FDI, and generated large-scale employment across manufacturing ecosystems. The sector now consists of consumer electronics, automotive, medical devices, and components, thereby supporting broad-based industrial growth.

- Growth of electric vehicles and automotive electronics: The expansion of electric vehicles and advanced automotive electronics is boosting the overall PU adhesive demand. These adhesives are extensively utilized in battery packs, sensors, and control units due to their thermal stability and vibration-damping properties. The article published by the International Energy Agency revealed that global electric car sales surged past 20 million units in 2025, accounting for one in four new cars, which is 25%, marking a 20% year-on-year growth and the fifth consecutive year of strong expansion. Besides, battery electric vehicles dominated this growth, which makes up about 65% of EV sales. The report also underscored that China remained the largest market, contributing over 13 million sales with nearly 55% of new cars being electric, while Europe saw a strong rebound to over 4.2 million sales driven by stricter CO₂ regulations, thus contributing to wider PU adhesives in electronics market expansion.

- Growth in automation, IoT, and 5G infrastructure: The growth of automation systems, IoT devices, and 5G networks is deliberately increasing PU adhesive usage in the electronics manufacturing sector. These technologies require highly reliable and fast-curing bonding materials for complex circuit assemblies, whereas the PU adhesives support high-frequency performance, mechanical stability, and efficient production processes. In May 2024, Ericsson, Qualcomm, and Dronus successfully demonstrated a 5G mm Wave-powered drone use case at the Ericsson U.S. 5G Smart Factory, thereby showcasing autonomous inventory checks in warehouse high racks. The company also outlined that it is powered by Qualcomm’s QRB5165 processor and Telit Cinterion’s mmWave data card; the drone leverages Ericsson’s private 5G network for live video streaming and barcode scanning, thus positively contributing to the polyurethane adhesives in electronics market expansion.

Challenges

- High performance and reliability requirements: One of the major challenges in the polyurethane (PU) adhesives in electronics market is the strict performance and reliability requirements. Modern electronic devices have become smaller, more powerful, and more complex, which exposes these adhesive materials to greater thermal stress, vibration, humidity, and mechanical loads. These PU adhesives need to maintain strong bonding performance, thereby providing electrical insulation and long-term durability under different types of operating conditions. Any type of failure of adhesive materials can result in device malfunction and reduced lifespan. Therefore, manufacturers need to make investments in terms of research and development in order to improve thermal stability, chemical resistance, and environmental durability.

- Volatility in raw material supply and pricing: The polyurethane adhesives in electronics market are mostly dependent on raw materials such as polyols, isocyanates, additives, and specialty chemicals, most of which are subject to price fluctuations and supply chain disruptions. Any type of variation in terms of crude oil prices, geopolitical conflicts, transportation issues, and regulatory changes can impact raw material availability as well as production costs. Electronics manufacturers need to operate on long-term supply agreements and demand consistent product quality, which makes these sudden cost increases difficult to pass on to customers. In addition, the supply shortages can disrupt production schedules and delay electronics manufacturing activities, negatively impacting the market’s growth and exposure.

Polyurethane (PU) Adhesives in Electronics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 1.3 billion |

|

Forecast Year Market Size (2035) |

USD 2.2 billion |

|

Regional Scope |

|

Polyurethane (PU) Adhesives in Electronics Market Segmentation:

Application Segment Analysis

The surface mounting in the application segment is anticipated to garner the highest share of 75.6% in the polyurethane adhesives in electronics market during the forecast period. The segment’s dominance is largely propelled by the rapid expansion of miniaturized, high-density electronic assemblies, which are used in modern devices. Increasing adoption of automated PCB assembly lines and high-speed manufacturing processes is also supporting this demand, as these adhesives deliberately support precision bonding, process efficiency, and compatibility with advanced production techniques. This particular trend is also strengthened by the integration of surface mount technology in consumer electronics, automotive ECUs, and industrial control systems. Apart from this, their compatibility with automated dispensing and curing systems enhances throughput in large-scale PCB production, thus positively influencing the segment’s dominance.

Product Type Segment Analysis

By the end of 2035, the UV-curing PU adhesive is forecasted to grow with a considerable revenue share in the PU adhesives in electronics market. The segment’s growth is largely attributable to the rising demand for rapid-curing, energy-efficient bonding solutions in high-speed electronics manufacturing environments. UV-curing polyurethane adhesives enable significantly reduced processing times, making them highly suitable for automated PCB assembly and surface-mount technology applications. For instance, in May 2026, Dymax expanded its HLC™ Adhesives portfolio with the launch of HLC‑M‑1004, which is a low‑viscosity medical adhesive especially designed for efficient assembly of complex devices. The company also notes that it leverages hybrid light‑curing technology, which enables reliable bonding in both light‑exposed and shadowed areas, with rapid UV/visible curing and controlled dispensing for tight gaps.

Formulation Type Segment Analysis

On the basis of formulation type, the water-based formulation is expected to grow with a noteworthy share in the polyurethane (PU) adhesives in electronics market during the forecast period. The segment’s growth is highly propelled by its low VOC content and environmentally friendly characteristics. These adhesives are widely adopted in applications where regulatory compliance, safety, and sustainability are the main priorities. Meanwhile, solvent-based adhesives, which are traditionally used for their strong bonding performance, are gaining renewed attention in certain high-performance electronics applications where fast adhesion, durability, and thermal resistance are essential. In addition, water-based PU adhesives are being integrated into automated electronics manufacturing processes due to their safer handling and improved workplace conditions, hence denoting a wider segment scope.

Our in-depth analysis of the polyurethane adhesives in electronics market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Product Type |

|

|

Formulation Type |

|

|

Properties |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polyurethane (PU) Adhesives in Electronics Market - Regional Analysis

APAC Market Insights

Asia Pacific polyurethane adhesives in electronics market is projected to dominate with the largest share of 71.6% during the discussed timeframe. The region’s upliftment in this field is effectively propelled by the expansion of electronics manufacturing hubs in countries such as China, Japan, South Korea, and India. In addition, the rising investments in consumer electronics, automotive electronics, and 5G infrastructure are supporting large-scale adoption. For instance, in February 2025, LG Chem signed an agreement with HL Mando to co‑develop advanced adhesives for automotive electronic components, thereby strengthening its position in the electronic adhesive industry. This collaboration will focus on thermal gap fillers for ADAS control units and insulating adhesives for steering and braking systems, ensuring high reliability under heat and stress, thus suitable for standard PU adhesives in electronics market growth.

The nation's status as the global epicenter for electrical circuit and gadget manufacturing is propelling the growth of China polyurethane adhesives in electronics market. The country’s market is highly accelerated by the rise of domestic electric vehicle battery assembly and the rollout of advanced driver-assistance systems, both of which depend on these specialized chemistries for structural bonding and component protection. Simultaneously, China's massive smart factories and robotic dispensing lines are driving a major technological shift toward reactive and rapid-cure formulations with the main goal of minimizing production times. Based on the government data published in August 2023, China’s action plan for stabilizing growth in the electronic information manufacturing industry 2023-2024 sets out measures to strengthen innovation and global competitiveness in electronics manufacturing. This particular plan targets 5% annual growth, more than USD 3.3 trillion in industry revenue, and higher market shares for 5G phones, large TVs, and solar cells.

The strong emphasis on high-precision engineering and advanced material technology is allowing the growth of the Japan polyurethane adhesives in electronics market. Growth in the country is primarily propelled by its leadership in high-end automotive electronics, electronic control units, and next-generation robotics, wherein PU adhesives are highly essential for dampening vibrations and protecting delicate circuitry. As per an article published by Influence Map, Japan has set certain vehicle electrification policies with an aim for 100% of new passenger car sales to be electrified, i.e., BEVs, FCEVs, PHEVs, HEVs by 2035, along with commercial vehicle targets reaching full electrification or decarbonized fuels by 2040. It also mentioned certain supporting measures, which include doubling EV charging ports to 300,000 by 2030, stricter CAFE fuel efficiency standards, and eco‑car tax breaks and subsidies, thus making it suitable for standard market growth.

North America Market Insights

The North America polyurethane (PU) adhesives in electronics market is projected for a steady expansion during the forecast period. The region’s growth in this field is largely propelled by a strong resurgence in domestic advanced manufacturing and aerospace electronics production. The region’s market also benefits from the rapid electrification of the automotive sector, where these adhesives are critical for structural bonding, thermal management, and vibration dampening in electric vehicle battery packs and advanced sensor systems. For instance, in September 2025, Henkel inaugurated its new North America Battery Application Center in Madison Heights, Michigan, thereby expanding its global footprint in EV innovation. This facility provides advanced application testing for thermal interface materials, sealants, structural adhesives, and debonding‑on‑demand solutions, helping OEMs optimize processes before scaling production.

The strong expansion in advanced manufacturing, EV electrification, and reliable electronics used in automotive and aerospace systems are some of the factors responsible for boosting the overall U.S. polyurethane adhesives in electronics market. In addition, the rising adoption of EV battery packs and electronic control modules is heightening demand for PU adhesives due to their vibration resistance, thermal stability, and insulation properties, which are highly essential for protecting sensitive components in harsh operating environments. In August 2024, DuPont announced that its BETAFORCE™ elastic structural adhesive had won the 2024 R&D 100 Award in the mechanical or materials category, recognized as one of the Oscars of innovation. It is especially designed for EV battery assembly, especially pouch cell bonding, and it uniquely bonds aluminum laminated film substrates without primers, while offering crashworthiness, durability, and sustainability benefits.

In Canada, polyurethane adhesives in electronics market are unfolding remarkable growth opportunities owing to the country’s aerospace sector and specialized medical device industry, which generate consistent demand for high-reliability PU formulations. In addition, the market’s growth is carried forward by a strong focus on environmental sustainability, which accelerates the transition toward bio-based, low-emission, and solvent-free adhesive technologies. Based on the government data published in May 2023, it generously invested in a GM‑POSCO joint venture to build a new cathode active materials facility in Bécancour, Quebec, strengthening Canada’s EV battery supply chain. This USD 600 million Ultium CAM project will create about 200 jobs and provide key materials such as nickel and lithium, which make up nearly 40% of battery costs, thus heightening the demand for PU adhesives in the country.

Europe Market Insights

Europe polyurethane adhesives in electronics market have acquired a prominent position in the global dynamics during the discussed timeframe. The region’s prominence in renewable energy electronics, such as wind and solar power inverters, generates consistent demand for durable PU formulations that shield complex circuitry from harsh outdoor environments. Innovation in the market is strongly stimulated by certain strict environmental and safety regulations, encouraging manufacturers to continuously invest in bio-based materials and circular-economy-compliant adhesive technologies. For instance, in April 2024, Evonik showcased advanced polyurethane additive solutions for electric vehicle batteries at UTECH Europe 2024, which include materials for structural adhesives, sealants, thermal interface materials, gap fillers, and battery potting applications. The company also highlighted new polyurethane additives based on renewable feedstocks with fully traceable supply chains and announced that its global amines production platform now operates on green electricity.

The nation's automotive sector and highly organized industrial automation landscape are propelling the growth of the PU adhesives in electronics market in electronics Germany. In addition, the country’s strong focus on Industry 4.0 and smart factory machinery generates high demand for durable PU formulations to protect intricate sensors and circuitry from intense mechanical vibrations and chemical exposure. Polyurethane adhesives are being used in electronic control units, sensors, and battery management systems propelled by their excellent bonding strength, flexibility, and resistance to harsh operating conditions. In addition, the expansion of electric vehicle manufacturing is efficiently driving demand for PU-based solutions in battery pack assembly, thermal management, and component encapsulation. Furthermore, continuous advancements in automated dispensing and precision assembly processes are also supporting the adoption of high-performance polyurethane adhesives across the country’s electronics and industrial sectors.

In the UK, the polyurethane adhesives in electronics market are growing exponentially on account of a high-value electronics manufacturing base, particularly in terms of aerospace-grade electronics, defense systems, and high-reliability industrial devices. A remarkable share of demand arises from applications that require long-term durability under harsh operating conditions, such as vibration-heavy environments and temperature cycling in advanced electronic assemblies. In addition, rising investments in semiconductor-related packaging, sensor systems, and communication equipment are encouraging the use of PU-based materials for insulation and component protection. In May 2024, Permabond introduced UV643, which is an ultra‑fast curing UV adhesive designed to bond rigid plastics, thermoplastics, and even dissimilar substrates such as metal to plastic. It has multi‑wavelength curing, i.e., 365 nm to 420 nm, thixotropic flow properties, and resistance to heat, humidity, and thermal cycling, ensuring durability and ease of application.

Key Polyurethane (PU) Adhesives in Electronics Market Players:

- Henkel AG & Co. KGaA (Germany)

- H.B. Fuller Company (U.S.)

- 3M Company (U.S.)

- Dow Inc. (U.S.)

- BASF SE (Germany)

- Sika AG (Switzerland)

- Plexus (U.S.)

- Arkema S.A. (Bostik) (France)

- Avery Dennison Corporation (U.S.)

- Huntsman Corporation (U.S.)

- Ashland Inc. (U.S.)

- Panacol-Elosol GmbH (Germany)

- DELO Industrie Klebstoffe GmbH & Co. KGaA (Germany)

- Nitto Denko Corporation (Japan)

- ThreeBond Holdings Co., Ltd. (Japan)

- Cemedine Co., Ltd. (Japan)

- LG Chem Ltd. (South Korea)

- SKC Co., Ltd. (South Korea)

- Pidilite Industries Limited (India)

- Adhesive Technologies, Inc. Pty Ltd. (Australia)

- Scigenics Sdn. Bhd. (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Henkel AG & Co. KGaA has registered itself as a leading participant in the PU adhesives in electronics market through its LOCTITE and BERGQUIST product portfolios. The company deliberately provides advanced adhesive, potting, encapsulation, and thermal management solutions for consumer electronics, industrial electronics, automotive electronics, and power devices.

- H.B. Fuller Company is one of the foundational global adhesives suppliers that has an enhanced portfolio to serve electronics assembly, semiconductor packaging, and electronic component manufacturing. The company provides specialty polyurethane adhesives especially designed to deliver excellent bonding strength and reliability in demanding electronic applications.

- 3M Company is yet another stronger player in this PU adhesives in electronics market, which benefits from expertise in materials science, enabling the development of polyurethane-based adhesive technologies. The firm’s extensive global customer network, continuous product innovation, and integration of adhesive technologies contribute significantly to its leading position in this market.

- BASF SE plays an important role in the PU adhesives in electronics market as a leading producer of polyurethane raw materials and specialty chemical solutions used in electronic adhesives. The company benefits from its strong vertical integration across the polyurethane value chain, which allows it to support adhesive manufacturers with advanced formulations.

- Sika AG is a prominent specialty chemicals company that offers polyurethane adhesive technologies, which are suitable for industrial and electronics applications. The company is constantly focused on product innovation, application engineering support, and customized bonding solutions that meet stringent reliability standards in both electronic assemblies and electrical systems.

Here is a list of key players operating in the global PU adhesives in electronics market:

The polyurethane adhesives in electronics market consist of global chemical and specialty adhesive manufacturers who are intensely competing in terms of product innovation, application-specific formulations, and geographic expansion. Leading companies in this field, such as Henkel, H.B. Fuller, 3M, BASF, Sika, and Bostik, leverage extensive R&D capabilities to develop high-performance PU adhesives that offer enhanced thermal stability, electrical insulation, flexibility, and durability for advanced electronic devices. Meanwhile, the strategic initiatives adopted by the market participants include investments in electronics-focused innovation centers, expansion of manufacturing capacity, and partnerships with electronics OEMs, with the main goal of strengthening their market presence. In May 2024, Dow began commercial operations of its new VORATRON™ polyurethane adhesive and gap filler production line at its systems house in Ahlen, Germany, with a collective goal to boost capacity tenfold to meet rising demand in EV battery assembly.

Corporate Landscape of the Polyurethane (PU) Adhesives in Electronics Market:

Recent Developments

- In May 2026, Plexus® introduced three new thermomechanical polyurethane structural adhesives, i.e., DT2325, DT2430, and DT2630LD, which are especially designed to address heat, stress, and durability challenges in modern assemblies. These formulations combine structural bonding with thermal management and offer toughness, stress relaxation under thermal cycling, and controlled heat dissipation.

- In January 2026, Henkel introduced Loctite STYCAST US 8000 A/B, which is a next-generation polyurethane potting solution designed to boost reliability in industrial and power electronics. The solution consists of ultra-low ionic content, high dielectric strength, and proven thermal endurance.

- Report ID: 8608

- Published Date: Jun 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.