Electric Vehicle Sensor Market Outlook:

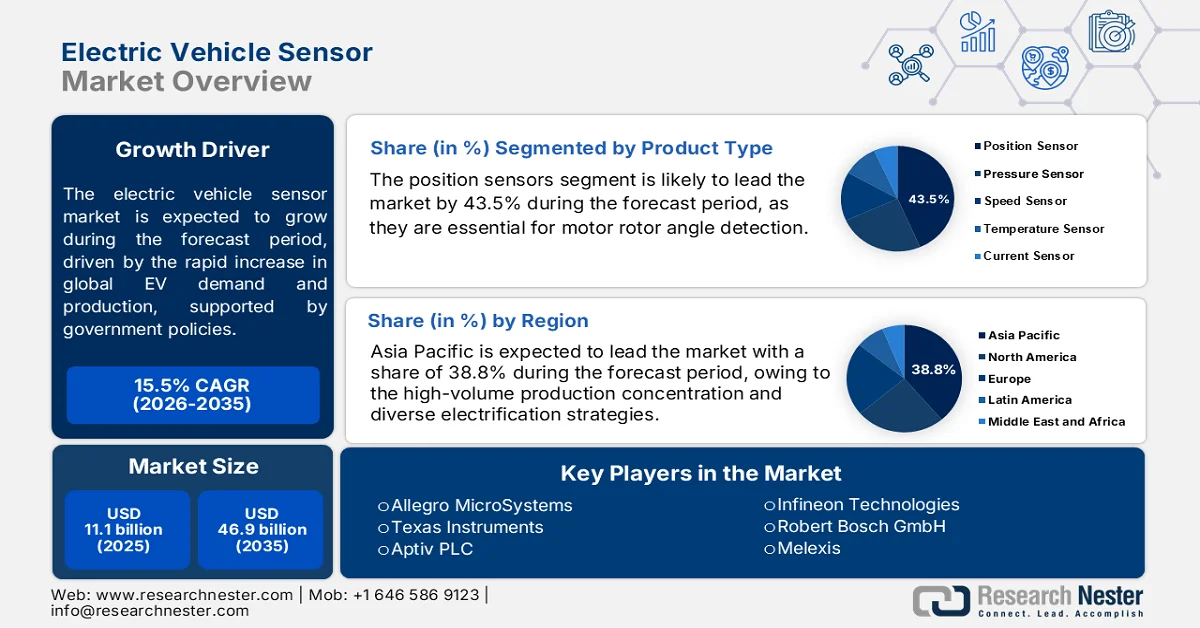

Electric Vehicle Sensor Market size was valued at USD 11.1 billion in 2025 and is projected to reach USD 46.9 billion by the end of 2035, rising at a CAGR of 15.5% during the forecast period, 2026-2035. In 2026, the industry size of electric vehicle sensor is estimated at USD 12.8 billion.

The electric vehicle sensor market is expanding in parallel with the rapid growth of global EV production, supported by government policies, vehicle electrification targets, and increasing deployment of advanced vehicle monitoring systems. According to the International Energy Agency (IEA) 2025 data, global electric car sales exceeded 17 million units in 2024, representing more than 20% of all new car sales worldwide. This increase directly supports demand for sensors used across battery management, thermal monitoring, powertrain control, safety systems, and vehicle performance optimization. Government-led electrification initiatives continue to strengthen market fundamentals. Similarly, the European Union continues to implement emissions reduction measures and transport electrification programs designed to increase EV adoption across member states. The growing emphasis on vehicle efficiency, battery longevity, and compliance with safety regulations is encouraging greater integration of sensing systems across both passenger and commercial EV segments.

Market demand is also being shaped by national commitments to decarbonization and transportation-sector emissions reduction. The International Energy Agency estimates that the global EV fleet surpassed 58 million vehicles in 2024, reflecting substantial growth in the installed base requiring ongoing monitoring and performance management. The U.S. Department of Transportation and National Highway Traffic Safety Administration continue to advance vehicle safety requirements, while the European Commission supports intelligent transportation and zero-emission mobility programs. As governments continue investing in charging networks, domestic manufacturing, and clean transportation infrastructure, the EV sensor market is expected to benefit from sustained vehicle production growth, stricter performance requirements, and increasing adoption of digitally managed vehicle architectures.

Key Electric Vehicle Sensor Market Insights Summary:

Regional Highlights:

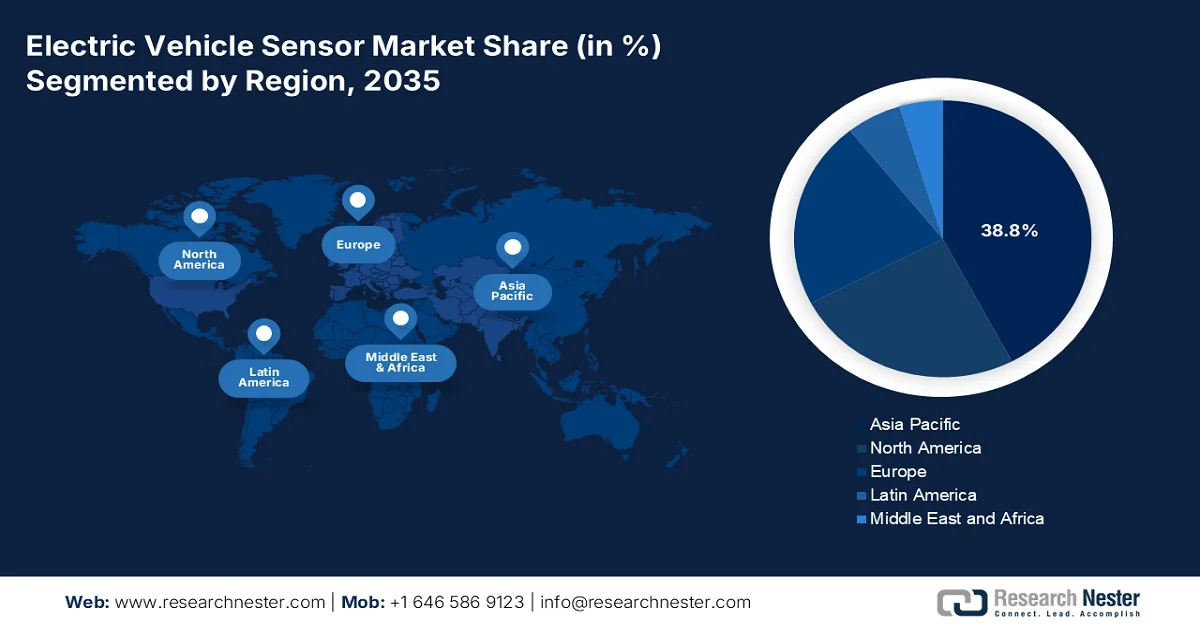

- Asia Pacific is anticipated to capture 38.8% of the electric vehicle sensor market revenue share by 2035, reinforced by high-volume EV production concentration and diverse electrification strategies across developed and emerging economies

- North America is expected to witness rapid growth in the market during 2026-2035, fueled by coordinated zero-emission vehicle mandates and increasing localization of battery and power electronics supply chains

Segment Insights:

- The Position Sensor segment is projected to account for 43.5% of the electric vehicle sensor market by 2035, supported by advancements in hybrid AMR-ANE sensing technologies enabling highly accurate 0–360° motor rotor angle detection

- The Battery Electric Vehicle segment is set to maintain its dominance throughout 2026-2035 in the market, stimulated by expanding BEV adoption driven by extended driving ranges that effectively address consumer range anxiety

Key Growth Trends:

- Expansion of public EV charging infrastructure

- National decarbonization and net-zero strategies

Major Challenges:

- High certification and functional safety standards

- Rapid Technology Shifts

Key Players: Allegro MicroSystems (U.S.),Texas Instruments (U.S.),Aptiv PLC (Ireland),Infineon Technologies (Germany),Robert Bosch GmbH (Germany),Melexis (Belgium),Sensata Technologies (U.S.),Denso Corporation (Japan),TDK Corporation (Japan),Hitachi Astemo (Japan),Nidec Corporation (Japan),Continental AG (Germany),Valeo (France),TE Connectivity (Switzerland),HELLA GmbH & Co. KGaA (Germany),Samyoung Electronics (South Korea),Hyundai Kefico (South Korea),Pricol Limited (India),CTS Corporation (U.S.),LEM Sensors (Switzerland).

Global Electric Vehicle Sensor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 11.1 billion

- 2026 Market Size: USD 12.8 billion

- Projected Market Size: USD 46.9 billion by 2035

- Growth Forecasts: 15.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: India, Canada, United Kingdom, France, Italy

Last updated on : 8 June, 2026

Electric Vehicle Sensor Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of public EV charging infrastructure: Government investment in charging infrastructure is increasing EV adoption and directly supporting sensor demand. According to the Drive Electric 2022-2023 data the U.S. National Electric Vehicle Infrastructure (NEVI) Formula Program provides USD 5 billion to states for EV charging deployment. Increased charging availability reduces range concerns and encourages broader EV ownership, resulting in higher vehicle production volumes. EVs require extensive sensor networks to manage battery performance, charging efficiency, thermal conditions, and electrical safety during charging cycles. Similar charging infrastructure investments are being made across Europe, China, India, and Canada. As charging networks become more sophisticated, sensor demand extends beyond vehicles into charging equipment and grid-management systems. This trend supports growth opportunities for manufacturers supplying automotive-grade sensing technologies across transportation electrification ecosystems.

- National decarbonization and net-zero strategies: Government climate policies are accelerating transportation electrification and supporting long-term demand for EV sensors. The European Commission May 2026 data establishes a legally binding target to reduce greenhouse gas emissions by at least 55% by 2030 compared, while numerous countries have adopted similar decarbonization strategies. These policies encourage automakers to accelerate EV production and invest in more efficient vehicle architectures. Sensor technologies play a critical role in improving energy management, battery performance, and vehicle efficiency. As governments continue implementing emissions reduction programs, automakers are increasing investments in electrified platforms with higher electronic content. This structural shift toward low-emission transportation provides sustained growth opportunities for sensor manufacturers serving global EV supply chains.

Challenges

- High certification and functional safety standards: Entering the EV sensor market requires compliance with ISO 26262 ASIL-D, the highest automotive safety integrity level. This demands massive investment in fault-tolerant design, redundant sensing, and rigorous validation. Small suppliers lack resources for multi-year certification cycles. Top companies have developed current sensors with ASIL-D readiness, requiring hours of failure mode testing.

- Rapid Technology Shifts: The transition from silicon IGBTs to silicon carbide and gallium nitride (GaN) inverters demands current sensors with higher bandwidth and dv/dt immunity. New magnetic technologies like TMR require different manufacturing expertise. Top companies have developed current sensor optimized for 1.2kV SiC inverters.

Electric Vehicle Sensor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15.5% |

|

Base Year Market Size (2025) |

USD 11.1 billion |

|

Forecast Year Market Size (2035) |

USD 46.9 billion |

|

Regional Scope |

|

Electric Vehicle Sensor Market Segmentation:

Product Type Segment Analysis

Under the product type segment, the position sensor is leading and is poised to hold the share value of 43.5% by the end of 2035 in the electric vehicle sensor market. The position sensors are essential for motor rotor angle detection. According to the NLM February 2024 data, the traditional single-bridge sensors struggle with full 0–360° measurement across wide magnetic fields. However, recent innovation using a single Wheatstone bridge from a ferromagnetic layer enables 0–360° detection by concurrently measuring anisotropic magnetoresistance (AMR) signals and anomalous Nernst effect (ANE) signals from transverse ports. This hybrid approach achieves a mean angle error of just 0.51–1.05° across a broad field range of 100 Oe to 10,000 Oe. For EV powertrain applications, such precision allows robust rotor position sensing even under variable motor currents, improving torque control and efficiency without requiring multiple sensor chips.

Vehicle Type Segment Analysis

In the electric vehicle sensor market, the battery electric vehicle dominates the vehicle type segment as modern BEVs can travel 150–400 miles on a full charge, depending on model, driving conditions, and habits. This range comfortably exceeds the 90% of all U.S. daily household trips, which average under 100 miles, effectively eliminating range anxiety for most consumers. Consequently, automakers are accelerating BEV production, directly driving demand for high-precision sensors, as per the U.S. DOE May 2024 data. Accurate current sensors optimize battery discharge efficiency, while temperature sensors prevent thermal runaway during extended trips. Position sensors ensure motor efficiency across varying loads. As BEV adoption grows, sensor content per vehicle increases to maintain safety and extend real-world driving range, solidifying BEVs as the largest revenue sub-segment in the market.

Application Segment Analysis

Within the application segment, powertrain holds the leading sub-segment share in the market. This application demands high-precision current sensors for phase current measurement and magnetic position sensors for permanent magnet synchronous motor (PMSM) rotor angle detection. Accurate sensor data ensures maximum torque-per-ampere efficiency and prevents motor demagnetization. Data from the U.S. Environmental Protection Agency indicates that EVs with optimized inverter sensor feedback achieve lower drivetrain energy losses compared to those using baseline calibration. Powertrain sensors must operate reliably under high electromagnetic interference, reinforcing this sub-segment's dominance.

Our in-depth analysis of the electric vehicle sensor includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Vehicle Type |

|

|

Propulsion Type |

|

|

Application |

|

|

Technology |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Electric Vehicle Sensor Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating and is poised to hold the regional revenue share of 38.8% by the end of 2035. The region is characterized by high-volume production concentration and diverse electrification strategies across developed and emerging economies. China leads with vertical integration of sensor manufacturing within domestic battery and EV assembly clusters. Japan and South Korea focus on high-precision magnetic position sensors for advanced traction motors, leveraging their robust electronics supply chains. India and Southeast Asian nations, including Malaysia and Indonesia, are emerging as cost-competitive bases for temperature and hall-effect current sensors, catering to entry-level EV platforms. The region also benefits from rapid two-wheeler and three-wheeler electrification, which demands compact, low-cost sensor solutions distinct from passenger car requirements.

The continued expansion of the country's new energy vehicle fleet is driving the market in China. According to the People’s Republic of China, the number of NEVs in use reached 31.4 million by the end of 2024, representing 8.9% of total vehicle ownership nationwide. The ministry also reported that 11.25 million NEVs were newly registered in 2024, a 51.49% increase compared with 2023. This strong growth in vehicle adoption is increasing demand for temperature, current, pressure, speed, and position sensors that support battery management, powertrain efficiency, safety systems, and vehicle performance monitoring across China's rapidly expanding electric mobility sector.

The transportation electrification and charging infrastructure deployment is driving the electric vehicle sensor market in Japan. According to Japan’s Ministry of Economy, Trade and Industry (METI) July 2024, the government allocated approximately USD 860.7 million for Clean Energy Vehicle (CEV) purchase subsidies, supporting wider adoption of battery electric, plug-in hybrid, and fuel-cell vehicles. In addition, public EV charging points in operation during 2024, reflecting continued investment in charging accessibility. These developments are increasing demand for temperature, current, pressure, speed, and position sensors used in battery management systems, power electronics, thermal control, and vehicle safety applications across Japan’s automotive sector.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the market. The region is driven by coordinated regulatory frameworks between the United States and Canada, mandating accelerated zero-emission vehicle adoption. Automakers are responding by localizing supply chains for battery packs and power electronics, directly increasing demand for domestically sourced current, position, and temperature sensors. The region is witnessing a strategic shift toward sensor redundancy for functional safety compliance, particularly in brake-by-wire and steer-by-wire systems adopted by premium EV platforms. Furthermore, extreme cold weather operation in northern states and Canadian provinces necessitates ruggedized thermal sensors and preconditioning controls, creating specialized product requirements distinct from other global regions.

The rising electrified vehicle adoption and expanding domestic EV production is shaping the electric vehicle sensor market in the U.S. According to the U.S. Energy Information Administration December 2024 data, the combined share of hybrid, plug-in hybrid, and battery electric vehicles reached a record 21.2% of total new light-duty vehicle sales in the third quarter of 2024, up from 19.1% in the previous quarter. Battery electric vehicles alone increased their market share from 7.4% to 8.9% during the same period. As EVs require significantly higher sensor content than conventional vehicles for battery management, thermal monitoring, and safety functions, growing EV penetration is accelerating demand for advanced automotive sensors across the U.S. market.

The accelerating vehicle electrification efforts and investments in clean transportation is shaping the market in Canada. According to Government of Canada January 2025 data, zero-emission vehicles (ZEVs) accounted for 16.5% of all new motor vehicle registrations in the fourth quarter of 2024, up from 13.4% a year earlier. In addition, Global News January 2025 data reports that the federal Incentives for Zero-Emission Vehicles (iZEV) Program has supported the purchase or lease of more than 546,000 zero-emission vehicles since its launch through 2025. Rising adoption of battery electric and plug-in hybrid vehicles is increasing demand for temperature, current, pressure, speed, and position sensors used in battery management, power electronics, thermal control, and vehicle safety systems, supporting continued growth of the Canada EV sensor market.

Europe Market Insights

The market in Europe is shaped by stringent CO2 fleet emission targets and aggressive internal combustion engine phase-out timelines across major economies. Automakers are transitioning to 800V architectures for faster charging, driving demand for high-isolation current sensors and robust thermal management components. The region emphasizes sensor functional safety under ISO 26262 ASIL-D, particularly for torque vectoring and autonomous emergency braking in EVs. Additionally, local content requirements for EV components are prompting non-European sensor suppliers to establish manufacturing facilities within the EU, ensuring compliance with evolving battery and electronics regulations.

The increasing electric vehicle adoption and continued expansion of the domestic automotive industry is shaping the electric vehicle sensor market in Germany. According to the Daily Sceptic January 2025 data, approximately 380,600 battery electric vehicles (BEVs) were newly registered in Germany in 2024, accounting for about 13.5% of all new passenger car registrations. Additionally, the GTAI 2025 data reported that Germany produced approximately 4.1 million passenger cars in 2024, maintaining its position as Europe's largest automotive manufacturing hub. As automakers expand production of electric and hybrid vehicles, demand for current, temperature, pressure, speed, and position sensors is increasing due to their critical role in battery management, powertrain control, thermal regulation, and vehicle safety systems.

The electric vehicle adoption accelerates and manufacturers increase the integration of advanced electronic systems is driving the electric vehicle sensor market in UK. According to the European Alternative Fuels Observatory March 2025 data, there were approximately 1.4 million licensed battery electric vehicles on UK roads at the end of 2024, representing a significant increase from previous years and highlighting the growing installed base requiring sensor-intensive technologies. Additionally, the battery electric vehicles accounted for 19.6% of new car registrations in 2024, reflecting sustained consumer adoption of zero-emission vehicles. Rising EV penetration is driving demand for current, temperature, pressure, speed, and position sensors used in battery management systems, thermal control, power electronics, and vehicle safety applications across the UK automotive sector.

Key Electric Vehicle Sensor Market Players:

- Allegro MicroSystems (U.S.)

- Texas Instruments (U.S.)

- Aptiv PLC (Ireland)

- Infineon Technologies (Germany)

- Robert Bosch GmbH (Germany)

- Melexis (Belgium)

- Sensata Technologies (U.S.)

- Denso Corporation (Japan)

- TDK Corporation (Japan)

- Hitachi Astemo (Japan)

- Nidec Corporation (Japan)

- Continental AG (Germany)

- Valeo (France)

- TE Connectivity (Switzerland)

- HELLA GmbH & Co. KGaA (Germany)

- Samyoung Electronics (South Korea)

- Hyundai Kefico (South Korea)

- Pricol Limited (India)

- CTS Corporation (U.S.)

- LEM Sensors (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Allegro MicroSystems is a leader in the electric vehicle sensor market, known for its advanced current and position sensors using Hall-effect and magnetoresistance technologies. The company has significantly advanced EV powertrain efficiency by developing high-bandwidth, low-noise current sensors for traction inverters and battery management systems.

- Texas Instruments plays a pivotal role in the market by integrating sensor signal chains with embedded processing for battery monitoring, temperature sensing, and current measurement. The company has advanced remote and real-time diagnostics in EVs through its precision ADC and isolation technology, enabling ambulatory-like monitoring of high-voltage systems without direct physical contact.

- Aptiv PLC has made strategic advancements in the electric vehicle sensor market by focusing on sensor fusion and high-voltage contactor monitoring. The company integrates current, temperature, and position sensors into compact modules for EV propulsion and charging systems. In 2025, the company made a net sale of USD 20,398 million.

- Infineon Technologies drives innovation in the market through its XENSIV™ sensor portfolio, including magnetic current sensors, pressure sensors, and radar-based cabin monitoring. The company has significantly advanced remote and real-time detection of electrical anomalies in EV inverters and onboard chargers by integrating sensor data directly into power module feedback loops.

- Robert Bosch GmbH is a dominant force in the market, leveraging its MEMS expertise and automotive heritage. Bosch has advanced real-time and ambulatory monitoring of EV battery cells and thermal systems using combined current, voltage, and temperature sensor clusters. In 2024, the company has made a sale of USD 105.7 billion.

Here is a list of key players operating in the global market:

The global electric vehicle sensor market is highly competitive, driven by rising demand for safety, autonomy, and battery efficiency. Key players from the US, Europe, and Asia are aggressively pursuing strategic initiatives, including mergers & acquisitions, R&D in MEMS and LiDAR, and long-term supply agreements with EV OEMs. For example, in February 2026, TE Connectivity acquired EV charging inlet assets from Phoenix Contact. Europe firms lead in current sensors for powertrains, while Japanese and South Korean companies dominate imaging and thermal sensors. US players focus on advanced LiDAR and radar. Malaysia and India manufacturers are emerging as cost-competitive suppliers of position and temperature sensors. Strategic pivots toward integrated sensor fusion and SiC-based current sensing are reshaping the landscape.

Corporate Landscape of the Market:

Recent Developments

- In September 2025, CTS Corporation announced the launch of COBROS™, a revolutionary new platform for electric motor control. Developed over seven years of intensive research and development, COBROS™ introduces a fundamentally new approach to motor control by using real-time, in-situ magnetic field sensing.

- In June 2025, Continental has developed a new sensor technology that measures the temperature inside permanently excited synchronous motors in electric vehicles (EVs) directly on the rotor for the first time.

- In September 2024, LEM sensors launches a new SMU sensor for accurate SOC with a single solution for the needs of FHEV, PHEV and BEV technologies. The company meets the needs of designers of automotive battery management systems (BMS) who are looking to extend as far as possible the maximum driving range of an electric vehicle.

- Report ID: 8145

- Published Date: Jun 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.