Agricultural Electric Vehicle Market Outlook:

Agricultural Electric Vehicle Market size was valued at USD 3.3 billion in 2025 and is projected to reach USD 10.8 billion by the end of 2035, rising at a CAGR of 12.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of agricultural electric vehicle is assessed at USD 3.7 billion.

The agricultural electric vehicle market is supported by a combination of farm decarbonization objectives, rising pressure to reduce operating costs, and expanding public investment in rural electrification and clean-energy infrastructure. According to the U.S. Department of Agriculture (USDA) February 2024 data, the U.S. has 1.9 million farms operating across more than 880 million acres, creating a substantial installed base for agricultural machinery replacement and modernization. In parallel, USDA’s Rural Energy for America Program (REAP) continues to provide grants and loan guarantees for renewable energy systems and energy-efficiency improvements, helping agricultural enterprises evaluate lower-emission equipment alternatives. Demand is also being influenced by broader transportation electrification trends.

The International Energy Agency (IEA) 2025 reported that global electric vehicle sales exceeded 17 million units in 2024, demonstrating continued progress in battery deployment, charging infrastructure expansion, and component manufacturing that can benefit off-road agricultural applications. For agricultural businesses, the ability to reduce exposure to fuel-price volatility and align with sustainability targets is becoming increasingly important, particularly for large farms, cooperatives, specialty crop producers, and greenhouse operators seeking predictable operating expenditures over the equipment lifecycle. Commercial uptake is therefore likely to be led by high-value farming operations and institutions seeking measurable reductions in fuel consumption, maintenance requirements, and operational emissions.

Key Agricultural Electric Vehicle Market Insights Summary:

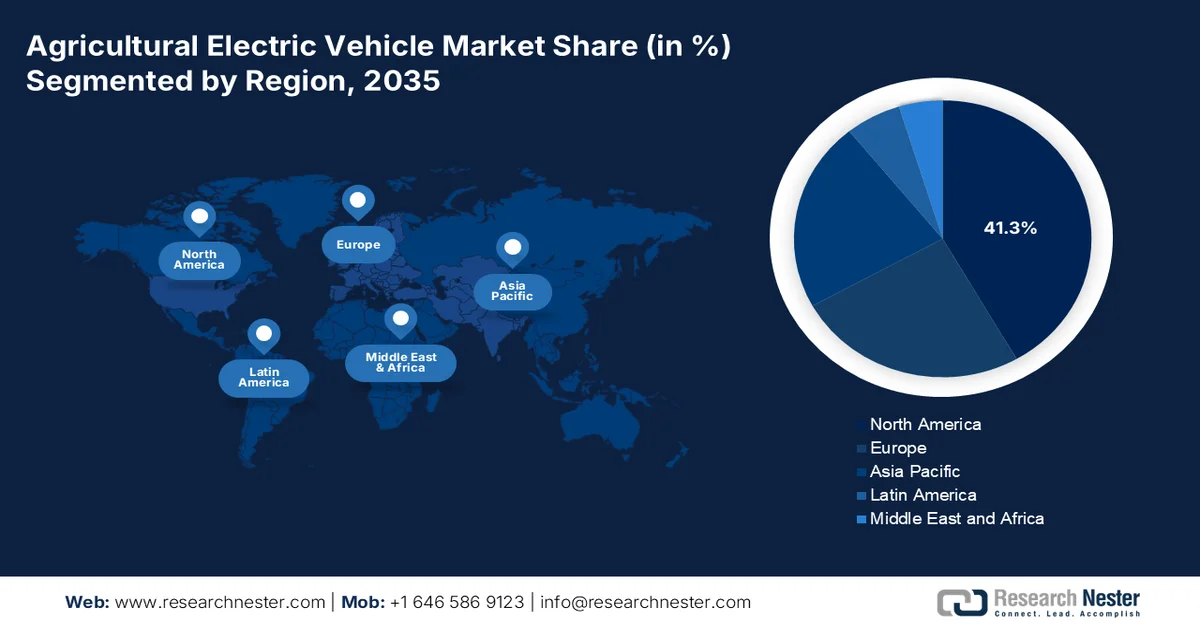

Regional Highlights:

- North America is anticipated to capture 41.3% revenue share by 2035 in the agricultural electric vehicle market, underpinned by expanding regulatory mandates, incentive-backed electrification programs, and growing deployment of compact electric tractors across farm operations

- Asia Pacific is set to witness rapid expansion across 2026-2035, accelerated by government subsidy initiatives for smallholder farming and the advancement of swappable battery standards to address rural infrastructure limitations

Segment Insights:

- In the agricultural electric vehicle market, the Four-Wheel Drive sub segment is projected to command 66.5% share by 2035, supported by superior traction capability, precise torque distribution, and improved energy efficiency for heavy-duty and all-terrain agricultural applications

- The Electric Tractor 30–100 HP segment is expected to maintain leadership through 2026-2035, fueled by its cost-efficient emission reduction potential and compatibility with currently available battery and motor technologies

Key Growth Trends:

- Government funding for clean energy and rural electrification

- Agricultural decarbonization policies

Major Challenges:

- High upfront battery costs

- Limited rural charging infrastructure

Key Players: CNH Industrial (U.S.),Solectrac Inc. (U.S.),Monarch Tractor (U.S.),Kubota Corporation (Japan,Mahindra & Mahindra (India).

Global Agricultural Electric Vehicle Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.3 billion

- 2026 Market Size: USD 3.7 billion

- Projected Market Size: USD 10.8 billion by 2035

- Growth Forecasts: 12.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, South Korea, Australia, Indonesia, Malaysia

Last updated on : 15 June, 2026

Agricultural Electric Vehicle Market - Growth Drivers and Challenges

Growth Drivers

- Government funding for clean energy and rural electrification: Government spending on clean energy infrastructure is creating favorable conditions for agricultural electric vehicle (AEV) adoption. In the United States, the Inflation Reduction Act and Bipartisan Infrastructure Law have directed billions of dollars toward clean energy deployment, battery manufacturing, and rural electrification. The RMI August 2023 data indicated that USD announced more than USD 11 billion in investments for rural electric co-ops, supporting renewable energy projects that can power electrified farm equipment. Electrified agricultural fleets become more economically attractive when farms have access to low-cost renewable electricity and grid upgrades. This driver is especially relevant for large commercial farms seeking long-term reductions in fuel costs and emissions while aligning with sustainability and procurement requirements.

- Agricultural decarbonization policies: Governments are increasingly linking agricultural productivity with climate objectives, accelerating demand for low-emission farm machinery. According to the Food and Agriculture Organization November 2024 data, agrifood systems account for approximately 31% of global greenhouse gas emissions, encouraging policymakers to support cleaner agricultural operations. Electrified farm vehicles help producers address operational emissions while improving compliance with environmental reporting requirements increasingly demanded by food processors and retailers. The shift is creating procurement opportunities for electric tractors, field transport vehicles, and farm logistics equipment. As carbon accounting becomes more important across food value chains, electric vehicle deployment is evolving from an environmental initiative into a business requirement that supports market access and long-term competitiveness.

Challenges

- High upfront battery costs: The initial purchase price of electric tractors remains 2–3x higher than diesel equivalents due to expensive lithium-ion battery packs. This discourages small and medium farmers with tight capital budgets. The global agricultural electric vehicle (EV) market is expected to grow, despite government pricing constraints, according to the International Energy Agency.

- Limited rural charging infrastructure: Most farms lack access to fast-charging stations or sufficient grid capacity, creating range anxiety for electric tractor operators during peak seasons. Top companies partners with other companies to deploy bidirectional chargers that also serve as farm energy storage.

Agricultural Electric Vehicle Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.6% |

|

Base Year Market Size (2025) |

USD 3.3 billion |

|

Forecast Year Market Size (2035) |

USD 10.8 billion |

|

Regional Scope |

|

Agricultural Electric Vehicle Market Segmentation:

Drive Type Segment Analysis

Within the drive type segment, the four-wheel drive sub segment is leading and is poised to hold the share value of 66.5% by the end of 2035. The Four-Wheel Drive (4WD) drive type is critically important for heavy-duty and all-terrain farming operations. Unlike two-wheel drive configurations, 4WD electric powertrains distribute torque independently to all wheels, delivering superior traction on soft, muddy, or sloped field conditions. This capability is particularly valuable for electric tractors operating in wet rice paddies, hilly orchards, or during spring tillage when soil moisture is high. Modern 4WD electric systems eliminate complex mechanical differentials by using individual wheel motors, which also enable precise torque vectoring for reduced soil compaction. While 4WD adds cost and weight compared to 2WD systems, the enhanced operational reliability and energy efficiency on challenging terrain make it the preferred choice for professional row-crop and livestock farms seeking zero-emission solutions.

Vehicle Type Segment Analysis

The electric tractor 30–100 HP leads the vehicle type segment, primarily because this power class represents the most cost-effective pathway for emission reductions. According to the California Air Resources Board January 2022 data, diesel equipment with 100 horsepower or lower accounts for 78% of the total off-road equipment population and 24% of annual diesel fuel consumption in California. The same research confirms that agricultural tractors under 100 HP can be fully electrified using currently available battery and motor components, offering lower dollars-per-ton emission reduction costs compared to larger machines. Consequently, CARB recommends targeting incentive and regulatory programs at this size class to accelerate electric adoption across farms.

Application Segment Analysis

The row crop farming is leading in the application segment in agricultural EV market. According to the IEEE March 2022 study, a 76kW electric orchard tractor achieved approximately 8% operating cost savings and 6% lifecycle cost savings under realistic component and energy prices. In contrast, a 175kW row crop tractor with medium-duty use yielded only 3% operating savings, while a 210kW heavy-duty row crop tractor generated negligible savings (0.5% operating, 0.1% lifecycle). The study concludes that powertrain electrification of high-power row crop tractors should probably be avoided, whereas it is highly beneficial for specialized orchard tractors operating in lower-power, intermittent-duty cycles typical of fruit and nut farming.

Our in-depth analysis of the agricultural electric vehicle (EV) market includes the following segments:

|

Segment |

Subsegments |

|

Drive Type |

|

|

Propulsion Type |

|

|

Vehicle Type |

|

|

Application |

|

|

Power Output |

|

|

Battery Chemistry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Agricultural Electric Vehicle Market - Regional Analysis

North America Market Insights

North America is dominating the agricultural electric vehicle market and is expected to hold the regional revenue share of 41.3% by the end of 2035. The region is characterized by a two-tier structure, with the United States and Canada pursuing distinct but complementary adoption pathways. In the US, state-level regulatory mandates, particularly in California, compel equipment dealers to stock electric tractors and loaders, while federal cost-share programs lower the upfront barrier for farm operators. Canada relies more heavily on federal-provincial incentive agreements and carbon tax savings to drive fleet conversions, especially in livestock and grain operations. Across both countries, the trend favors compact electric tractors under 100 horsepower for orchards, vineyards, and dairy farms, where short-duty cycles and low-speed, high-torque requirements align well with current battery capabilities. Infrastructure development for rural charging remains the primary constraint.

The increasing federal support for advanced vehicle manufacturing and rural clean-energy deployment is shaping the agricultural electric vehicle (EV) market in the U.S. In July 2024, the PBS data depicted that the U.S. Department of Energy announced up to USD 1.7 billion in funding to support the conversion of existing automotive facilities for electric vehicle production, strengthening domestic supply chains that can also support off-road and agricultural vehicle electrification. Additionally, the U.S. Environmental Protection Agency January 2026 data reported that transportation accounted for 28% of total U.S. greenhouse gas emissions in 2022, reinforcing policy momentum toward lower-emission vehicle technologies across sectors, including agriculture. Growing investment in electrification infrastructure, combined with sustainability goals among large farming operations, is supporting demand for electric agricultural equipment throughout the country.

The federal investments in clean transportation and agricultural sustainability continue to expand are driving the agricultural EV market in Canada. In January 2025, Government of Canada reported that more than 546,000 zero-emission vehicles (ZEVs) had been incentivized through the Incentives for Zero-Emission Vehicles (iZEV) Program since its launch, supporting broader electrification adoption and strengthening the domestic EV ecosystem. Additionally, Government of Canada October 2025 announced up to CAD 300 million under the Agricultural Clean Technology (ACT) Program through 2028, aimed at helping producers adopt clean technologies that reduce emissions and improve energy efficiency. These initiatives are encouraging agricultural businesses to evaluate electric tractors, utility vehicles, and farm transport equipment as part of long-term strategies to lower fuel costs, meet sustainability objectives, and improve operational efficiency.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the agricultural electric vehicle market. The region is highly diverse, spanning advanced manufacturing hubs like Japan and South Korea to rapidly adopting nations such as China and India, alongside smaller markets like Indonesia, Malaysia, and Australia. Asia Pacific is propelled by government subsidy schemes targeting smallholder farmers and plantation operators. Japan and South Korea lead in lightweight electric tractors for rice paddies and orchards, where soil compaction from heavier diesel models is a concern. India and China focus on cost-effective two-wheel electric tillers and compact utility vehicles for small farms. Malaysia and Indonesia prioritize electric haulers for palm oil estates. A key trend is the development of swappable battery standards to overcome inconsistent rural grid infrastructure.

The expanding EV policy framework and infrastructure investments is shaping the agricultural EV market in India. According to the India Brand Equity Foundation (IBEF) February 2026 data, public EV charging stations reached 29,151 by Q3 FY25, reflecting a 78% CAGR from FY22, which improves charging accessibility across rural and semi-urban regions. In addition, under the PM e-Bus Sewa Payment Security Mechanism Scheme, the Government of India has allocated ₹3,435.33 crore to support deployment of more than 38,000 electric buses, demonstrating continued public investment in vehicle electrification and supporting broader EV supply-chain development. These initiatives, combined with battery manufacturing investments and favorable import policies, are creating a stronger foundation for agricultural electric vehicle adoption.

The expanding electric mobility supply chain and strategic investment in advanced vehicle technologies is driving the agricultural electric vehicle market in China. According to the China Association of Automobile Manufacturers (CAAM) April 2026 data, China’s auto parts exports reached USD 16.76 billion during January–February 2026, representing a 14.1% year-on-year increase, reflecting the growing competitiveness of domestic automotive components used across electric vehicle segments. In addition, Horizon Robotics reported cumulative deliveries of 10 million driving-assistance system units by August 2025, including 4 million units shipped in 2025 alone, highlighting rapid progress in vehicle intelligence technologies. These developments strengthen China’s EV ecosystem, supporting future innovation, localization, and cost reductions for electric agricultural machinery.

Europe Market Insights

The Europe agricultural electric vehicle (EV) market is driven primarily by binding emissions reduction targets under the European Green Deal and Farm to Fork Strategy, which compel member states to subsidize zero-emission farm machinery. Europe benefits from a coordinated framework through the Common Agricultural Policy, allowing equipment manufacturers to deploy consistent product lines across multiple countries. The market favors medium-power electric tractors for mixed crop-livestock farms and specialized vineyard or orchard operations in France, Italy, and Germany. Northern European countries, including the NORDIC region, lead in cold-climate battery testing and solar-integrated charging depots. A notable trend is the rise of cooperative-owned battery-swapping stations serving multiple farms, reducing individual capital expenditure requirements for smallholders.

Germany’s agricultural electric vehicle market is supported by the country’s strong clean-energy transition and expanding electric mobility ecosystem. According to the Clean Energy Wire March 2025 data, Germany had approximately 1.65 million battery-electric passenger vehicles registered as of January 1, 2025, reflecting continued growth in the domestic EV industry and strengthening supply chains relevant to agricultural electrification. In addition, the Bundesnetzagentur January 2026 data reported that renewable energies accounted for approximately 54% of Germany’s gross electricity consumption in 2024, providing a growing source of low-carbon electricity for rural operations and vehicle charging. These developments are creating favorable conditions for electric agricultural machinery adoption as farms seek to reduce fuel dependence, lower emissions, and improve long-term operational efficiency.

The growth in electrification infrastructure and government-backed clean transport investment is driving the agricultural EV market in UK. According to the UK Government June 2025 data, the country had more than 79,000 public EV charging devices installed by January 2025, representing a year-on-year increase of approximately 32%. Additionally, the Renewable UK March 2025 data reported that renewable sources generated over 50% of the UK’s electricity during 2024, providing an expanding supply of low-carbon power that can support electric vehicle charging in rural and agricultural areas. These developments are strengthening the operating environment for electric farm machinery, helping agricultural businesses reduce fuel costs, improve energy efficiency, and align with sustainability objectives.

Key Agricultural Electric Vehicle Market Players:

- CNH Industrial (U.S.)

- Solectrac Inc. (U.S.)

- Monarch Tractor (U.S.)

- Kubota Corporation (Japan

- Mahindra & Mahindra (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- CNH Industrial is the top player in the agricultural electric vehicle market and focuses on modular electric architectures and hybrid conversions for its flagship brands Case IH and New Holland. In 2024, the company has made net sale of USD 17,060 million.

- Solectrac leads the agricultural EV market, focuses on compact, affordable battery-electric tractors (25–70 HP) for small to medium-sized farms and vineyards. The company emphasizes swappable battery packs to eliminate downtime for recharging, as well as grid-tied and off-grid solar charging solutions.

- Monarch Tractor is redefining the agricultural electric vehicle market by embedding autonomous driving, AI-based crop monitoring, and battery-electric power into a single platform (the MK-V series).

Here is a list of key players operating in the global agricultural electric vehicle (EV) market:

The global agricultural electric vehicle market is highly fragmented but seeing rapid consolidation through technology partnerships. Key players from North America and Europe lead in high-power autonomous EVs, while Asia manufacturers focus on small-scale, cost-effective electric tractors and two-wheelers. Strategic initiatives include vertical integration of battery manufacturing, AI-based precision farming software, and retrofitting legacy diesel fleets. For instance, U.S. and Germany firms are developing modular swappable battery systems to reduce downtime, while Japanese and Indian companies prioritize lightweight EVs for rice paddies and orchards. Simultaneously, startups from Australia and Malaysia are leveraging government subsidies to commercialize solar-assisted utility vehicles, intensifying regional competition.

Corporate Landscape of the Agricultural Electric Vehicle Market:

Recent Developments

- In December 2025, Montra Electric launched the Montra Electric E-27 tractor, marking its entry into the Northern India market. Unveiled at EIMA Agrimach India 2025, the E-27 is positioning itself as a game-changer for farmers looking to escape rising diesel costs.

- In November 2025, Carraro Group announced that it has signed a strategic partnership with Seederal, a French industrial startup specializing in high-performance fully electric tractors.

- In October 2024, Mahindra Last Mile Mobility Limited announced the launch of the Mahindra ZEO, a revolutionary new electric four-wheeler. The name ‘ZEO’, stands for "Zero Emission Option", displays the environmental benefits of the electric vehicle.

- Report ID: 8045

- Published Date: Jun 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.