Electric Insulator Market Outlook:

Electric Insulator Market size was valued at USD 17.2 billion in 2025 and is projected to reach USD 28.5 billion by the end of 2035, rising at a CAGR of 5.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of electric insulator is evaluated at USD 18.2 billion.

The market is sustaining huge growth based on factors such as the increasing demand for reliable power transmission and distribution infrastructure worldwide. The expansion in terms of electrification projects in different economies is also efficiently fueling the adoption of high-performance insulators. In this context, the U.S. Department of Energy (DOE) in September 2025 reported it has launched the Speed to Power initiative with a main aim to accelerate multi-gigawatt transmission and generation projects, making sure that the country can meet growing energy demand and support AI development. It also stated that blackouts could increase by 100 times by 2030 if additional firm capacity is not added. Therefore, this effort supports multiple presidential executive orders prioritizing grid reliability and national security, positively impacting market growth.

Furthermore, the integration of renewable energy sources such as solar and wind is increasing the need for high-performance insulators. Meanwhile, the government-funded grid modernization activities are also prompting a profitable business environment for the market. In December 2024, the U.S. DOE’s Office of Electricity announced three funding opportunities totaling an approximate amount of USD 18.4 million to advance grid modernization and renewable energy integration. This REIMAGINE BREAKERS program, jointly funded with an amount of USD 8 million, is mainly focused on reducing the cost of high-voltage direct current circuit breakers to improve the grid’s ability to transmit and deliver electricity from sources such as wind, hence denoting a positive market outlook.

Key Electric Insulator Market Insights Summary:

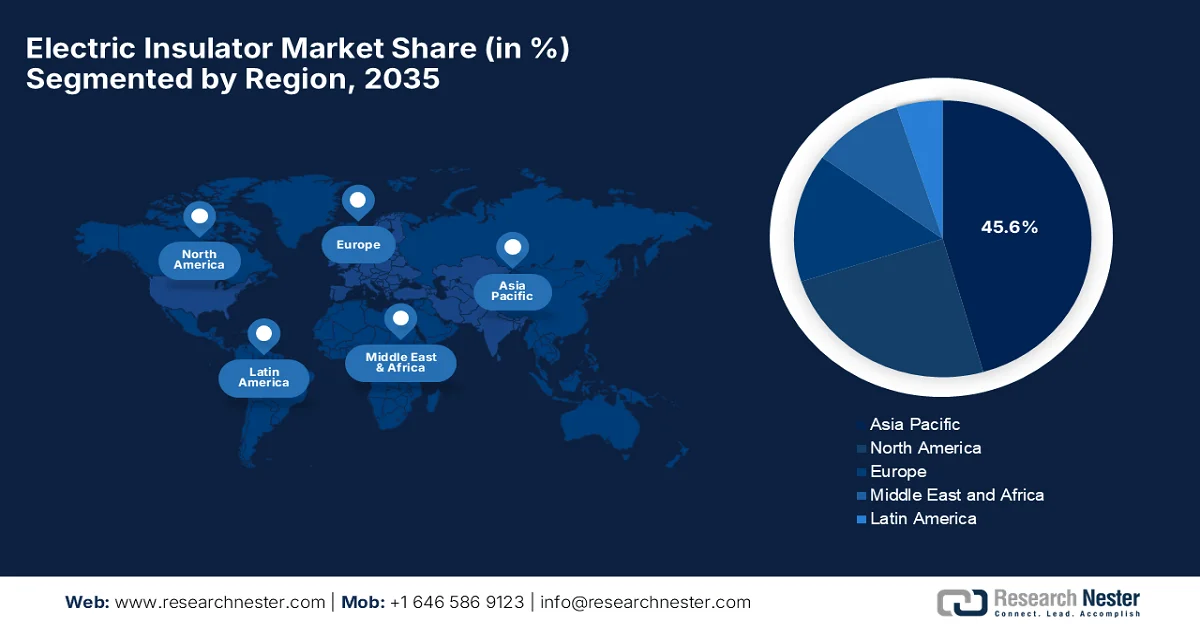

Regional Highlights:

- Asia Pacific is projected to command a 45.6% revenue share by 2035 in the electric insulator market, attributable to expanding solar manufacturing capacity, high installation volumes, and ongoing product innovations by key industry participants.

- North America is anticipated to witness notable growth through 2026–2035 in the electric insulator market, impelled by increasing integration of digital grid technologies and adoption of sensor-compatible insulators.

Segment Insights:

- The ceramic/porcelain segment is forecast to account for a dominant 48.5% share by 2035 in the electric insulator market, propelled by its high mechanical strength, proven dielectric performance, and extended service life across high and medium voltage networks.

- The medium voltage insulators segment is expected to expand at a considerable rate by 2035, supported by expanding electrification initiatives and rising deployment of distributed energy resources and microgrids.

Key Growth Trends:

- Rising electricity demand

- Shift to advanced insulator materials

Major Challenges:

- Supply chain disruptions

- Skilled workforce shortage

Key Players: ABB Ltd. (Switzerland), Siemens AG (Germany), NGK Insulators, Ltd. (Japan), Hubbell Incorporated (U.S.), General Electric Company (U.S.), Bharat Heavy Electricals Limited (India), Aditya Birla Insulators (India), MacLean-Fogg Company (U.S.), LAPP Insulators GmbH (Germany), Seves Group S.r.l. (Italy), Toshiba Corporation (Japan), PFISTERER Holding SE (Germany), TE Connectivity Ltd. (Switzerland), Krempel GmbH (Germany), Owens Corning (U.S.), Modern Insulators Ltd. (India), Electro Porcelain Industries Pvt. Ltd. (India), Hitachi Energy Ltd. (Switzerland), LS ELECTRIC Co., Ltd. (South Korea), Leader Cable Industry Berhad (Malaysia).

Global Electric Insulator Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 17.2 billion

- 2026 Market Size: USD 18.2 billion

- Projected Market Size: USD 28.5 billion by 2035

- Growth Forecasts: 5.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: Brazil, South Korea, Mexico, Indonesia, Saudi Arabia

Last updated on : 17 February, 2026

Electric Insulator Market - Growth Drivers and Challenges

Growth Drivers

- Rising electricity demand: The surging demand for electricity owing to population growth and industrial activities is bolstering the electric insulator market growth internationally. According to the official statistics published by the International Energy Agency in 2025, the total worldwide electricity demand surged by 4.3% in 2024, which is up from 2.5% in 2023 and well above the 2010-2023 average of 2.7%. It also notes that the total power consumption increased by 1,080 TWh, which is nearly double the average annual rise of the previous decade, reflecting accelerating electrification across buildings, industry, and transport. Moreover, China has been recognized as a leader in this expansion with a 550+ TWh (7%) increase, whereas advanced economies rebounded with a 230 TWh rise after a 140 TWh decline in 2023, hence denoting an optimistic market opportunity.

Global Electricity Demand Growth Statistics 2024 - Regional & Sector-wise Power Consumption Trends

|

Indicator |

2023 |

2024 |

Key Insight |

|

Global Electricity Demand Growth |

2.5% |

4.3% |

Strong acceleration |

|

Increase in Global Consumption |

- |

+1,080 TWh |

Nearly 2 times the decade average |

|

China Consumption Growth |

- |

+550+ TWh (7%) |

Largest global contributor |

|

Advanced Economies |

-140 TWh |

+230 TWh |

Sharp rebound |

|

Buildings Sector |

- |

+600+ TWh (5%) |

60% of total growth |

|

Industry Sector |

- |

4% growth |

40% of total growth |

|

Transport Sector |

- |

>8% growth |

EV-driven demand |

Source: IEA

- Shift to advanced insulator materials: The utilities and manufacturers across the globe are making a shift towards composite and polymeric insulators, benefiting from the advantages such as better pollution resistance, along with easier installation. This factor readily boosts the market growth at a robust pace, encouraging more players to make investments in this field. Hitachi Energy, in January 2025, announced that it is expanding its composite component factory in Piteå, Sweden, by increasing its workforce by 50% and investing in new machinery to meet rising global demand for power transmission equipment. This facility produces composite insulators used in transformers, circuit breakers, and power electronics, which are highly critical components for long-distance and cross-border electricity transmission. Hence, such expansion projects from the global pioneers are accelerating the shift toward improved insulation technologies, thereby strengthening export-import growth, globally.

Leading Electrical Insulators Exporters and Trade Surplus Data 2024

|

Country |

Export Value (USD million) |

Trade Surplus (USD million) |

|

China |

898 |

835 |

|

Italy |

231 |

138 |

|

Germany |

227 |

97.4 |

|

U.S. |

204 |

- |

|

India |

156 |

- |

Source: OEC

Leading Electrical Insulators Importers and Trade Deficit Data 2024

|

Country |

Import Value (USD million) |

Trade Deficit (USD million) |

|

U.S. |

440 |

-236 |

|

Saudi Arabia |

158 |

-157 |

|

Germany |

129 |

- |

|

India |

119 |

- |

|

Mexico |

108 |

|

Source: OEC

- Replacement of aging infrastructure: Many power grids across both developed and established economies were built several years ago. Therefore, this results in surface degradation and cracking and decreased mechanical strength, encouraging utilities to prioritize grid modernization programs, creating sustained demand in the market. In December 2025, the European Commission stated that it had proposed new initiatives to modernize and expand the region’s grid infrastructure to improve energy flow, lower prices, and strengthen energy independence. This package is mainly focused on increasing cross-border interconnectivity and accelerating permitting procedures to upgrade existing networks before adding new capacity. Such large-scale efforts are creating sustained demand for advanced power transmission components, including insulators.

Challenges

- Supply chain disruptions: The electric insulator market is mainly dependent on a proper supply of raw materials, components, and logistical networks. The disruptions in terms of cross-border conflicts, natural disasters, and transportation concerns can cause delay production. On the other hand, reliance on a limited number of suppliers exacerbates this vulnerability. In addition, the constant fluctuations in electricity as well as transportation costs also strain the supply chain. Therefore, to combat this, manufacturers need to make investments in risk management strategies, i.e., supplier diversification, inventory buffers, and alternative sourcing, to maintain production continuity. Furthermore, failure to manage these issues can result in delayed project deliveries and financial losses, negatively impacting market growth.

- Skilled workforce shortage: The electric insulator market requires skilled engineers, technicians, and quality control personnel to efficiently manage advanced manufacturing processes. Therefore, the shortage of qualified work professionals can cause a hindrance to production efficiency, R&D, and technology adoption. Also, the aspect of training new employees is both time-consuming and expensive, whereas retaining experienced staff is equally difficult in the competitive labor sectors. The adoption of automation and digital tools partially mitigates this challenge, but human expertise is considered to be highly essential for troubleshooting and quality assurance. In this context, companies that fail to attract or retain talent risk delays in innovation and operational inefficiencies, limiting their ability to meet the surging worldwide demand.

Electric Insulator Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.8% |

|

Base Year Market Size (2025) |

USD 17.2 billion |

|

Forecast Year Market Size (2035) |

USD 28.5 billion |

|

Regional Scope |

|

Electric Insulator Market Segmentation:

Material Type Segment Analysis

By the conclusion of forecast duration, the ceramic/porcelain, which is a part of the material type segment, is anticipated to lead, capturing the largest share of 48.5% in the electric insulator market. Their high mechanical strength, proven dielectric properties, and long service life make them highly suitable for both high and medium voltage networks. This is particularly witnessed in transmission systems, and these types of insulators perform well under different environmental conditions. In February 2025, Insulation Technology Group stated that it had acquired Cerisol Isoladores Ceramicos SA with a primary aim to expand production capacity and enhance worldwide service for high-voltage porcelain insulators. Therefore, this particular acquisition strengthens ITG’s position in this segment, supporting mission-critical applications in electrical substations and overhead transmission lines, hence highlighting the continued demand and strategic importance of ceramic insulators in modern power grids.

Voltage Level Segment Analysis

The medium voltage insulators based on voltage level are expected to grow at a considerable rate in the market by 2035. The growth is mainly subject to factors such as a significant portion of power distribution networks operate in this medium range, linking substation outputs to end distribution feeders. The subtype is identified as the backbone of grid interconnection within cities, towns, and industrial areas, where power is stepped down for end user consumption. On the other hand, the ongoing electrification initiatives, especially in rapidly urbanizing regions and developing rural areas, are solidifying the position of medium‑voltage lines. In addition, these insulators are also suitable for growing distributed energy resources, microgrids, and renewable interconnections, all of which rely on robust insulation solutions to maintain reliability, safety, and efficiency in expanding energy networks, hence denoting a wider segment scope.

Installation Environment Segment Analysis

Outdoor insulators are expected to garner a significant share over the discussed timeframe. The subtype leads the installation environment segment based on factors such as extensive overhead network installations, i.e., transmission lines, poles, and substations. Simultaneously, the weather exposure and pollution resistance requirements boost the preference for robust outdoor insulation solutions. In addition, the continued growth of renewable energy projects, which include wind and solar farms located in exposed outdoor environments, further reinforces the demand for robust outdoor insulators that are capable of long-term performance in diverse climatic and geographic conditions. Hence, the presence of all of these factors positions the subtype at the forefront of revenue generation in the electric insulator industry.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

|

|

Voltage Level |

|

|

Installation Environment |

|

|

Application |

|

|

End user Industry |

|

|

Product Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Electric Insulator Market - Regional Analysis

APAC Market Insights

The Asia Pacific electric insulator market is expected to hold the dominant revenue share of 45.6% during the stipulated timeframe. The region’s leadership is mainly driven by an extensive solar panel manufacturing base, capacity additions, and steady demand from mature markets. The region’s growth is also carried forward by high installation volumes and key market players making continued innovations in this field. In December 2024, PFISTERER Holding SE notified that it entered into a cooperation and licensing agreement with Nippon Katan Co., Ltd. to locally assemble and deliver composite insulators for overhead power lines. Therefore, this particular collaboration will streamline logistics and is expected to significantly increase composite insulator volumes in the country, hence making it suitable for the market’s growth and exposure in the region.

These factors, such as demand for electric insulators, utilities, and manufacturers' investments in insulation solutions to support both traditional and renewable power infrastructure, are responsibly uplifting the market in China. The country is a hub of solar panel manufacturing, and policy initiatives are promoting renewable energy integration, thereby supporting market growth. As stated by Solar Paces Organization in December 2025, the official policy roadmap, which was jointly issued by the country’s National Development and Reform Commission and the National Energy Administration, aims to accelerate large-scale deployment of concentrated solar power by targeting 15 GW of installed capacity by 2030. This plan promotes integration of CSP with wind and photovoltaic power, supporting grid stability and renewable energy expansion, hence boosting the demand for related infrastructure, including electric insulators, as part of building a new-type power system.

The decentralization of generation through microgrids and distributed energy systems in rural and semi-urban areas is supporting the market growth in India. This localized generation increases the need for medium and low voltage insulation infrastructure that is suitable for varied distribution topologies. According to the official statistics published by the Ministry of Power in January 2026, the country’s national power transmission network has surpassed 500,000 circuit kilometres (ckm) of lines (220 kV and above), with the commissioning of the 628 ckm 765 kV Bhadla II–Sikar II line to evacuate renewable power from Rajasthan’s solar zones. Therefore, this expansion increases grid transformation capacity and inter-regional transfer, supporting the integration of growing non-fossil power generation, positively impacting market growth.

North America Market Insights

The North America electric insulator market is growing at a notable pace, mainly influenced by the integration of digital grid technologies. Utilities in this region are the leading adopters of insulators that are compatible with sensors and monitoring systems. In this context, Ensto in January 2026 announced that it had launched the new generation pin insulators, which are reported to be compliant with the updated IEC 60383-1:2023 standard, consisting of increased creepage distance, insulation thickness, and semiconductive coatings to enhance durability and reduce partial discharge risks. These insulators are especially designed for modern overhead line applications, making sure of reliable performance under demanding conditions. Thus, such developments from the pioneers are suitable for bolstering the region’s expansion and exposure in the years ahead.

The aspects of infrastructure hardening, coupled with the proactive resilience initiatives, are efficiently boosting demand in the U.S. electric insulator market since they withstand extreme weather events and electromagnetic disturbances. Meanwhile, the focus on maintaining reliable service in critical urban, industrial, and data-intensive zones has elevated the need for high-performance insulation solutions in the country. In August 2024, CenterPoint Energy announced that it had launched the Greater Houston Resiliency Initiative that mainly to strengthen the electric grid and reduce outage risks in the hurricane season. The first phase included replacing 1,000 wooden poles with storm-resilient fiberglass poles, followed by doubling vegetation management near power lines, and installing 300 automated trip-saver devices to improve restoration times. Hence, the presence of these targeted infrastructure upgrades reflects efforts to enhance grid reliability, thereby increasing the growth potential for electric insulators.

The electric insulator market in Canada is poised for huge growth, propelled by the expansion of long-distance transmission lines connecting remote renewable generation sources, such as hydro and wind farms, to urban load centers. The challenging northern climate and ice-loading conditions increase reliance on durable, high-strength insulators, which have led to significant imports. Based on the government data, the country witnessed a significant import activity in 2023, with 22 major importers accounting for 80.35% of total imports, which were valued at CAD 22,030,641. Besides, the market is identified as moderately concentrated, with the top three importers responsible for over a third of total imports. Furthermore, the leading players in the country are Austin Insulators Inc., CO7 Technologies Inc., Hitachi Energy Canada Inc., and Hydro-Québec, which are provinces such as Ontario, Quebec, and Alberta; they are contributing to market expansion in Canada.

Leading Electric Insulator Importers in Canada: 2023

|

Number of Importers |

Value of Imports (CAD) |

Cumulative % of Imports |

|

3 |

9,963,162 |

36.34% |

|

6 |

13,863,663 |

50.57% |

|

10 |

17,420,315 |

63.54% |

|

15 |

20,203,874 |

73.69% |

|

22 |

22,030,641 |

80.35% |

|

All 22+ |

27,416,937 |

100% |

Source: Government of Canada

Europe Market Insights

Europe electric insulator market is anticipated to grow at a significant rate from 2026 to 2035. The region’s leadership is mainly fueled by cross-border grid reinforcement and harmonization efforts. The region is also witnessing extensive demand for standardized insulator solutions to ensure compatibility across multiple national networks while supporting the integration of proper renewable generation. European Commission in February 2025, stated that the GreenSwitch project, which was launched in March 2023 and supported by CEF Energy with a total amount of €73 million (approximately USD 85.6 million), is modernising and digitalising grid infrastructure across Austria, Slovenia, and Croatia with a main goal enhance reliability, observability, and renewable integration. It also mentioned the key developments, which include new primary substations in Winklern and Velden, and more than 20 secondary substations in Carinthia, which are already equipped with devices to improve supply security and support home renewable solutions, hence positively impacting market growth.

The offshore wind power integration is the main factor positively impacting the market in Germany. Also, the insulators that are used in coastal and offshore transmission networks must resist saline corrosion and harsh environmental conditions, prompting the adoption of specialized, high-durability products. This has further encouraged market players to pursue distinct growth strategies to capitalize on the electric insulator industry. In December 2025, GE Vernova reported that, along with Seatrium, it had been granted a contract by TenneT to deliver the BalWin5 offshore HVDC grid connection by transmitting 2.2 GW of North Sea wind power to Germany’s onshore grid. The project includes an offshore converter platform, an onshore converter station at Bremen-Werderland, and a 325 km sea and land cable system, designed for high-capacity, long-distance renewable transmission, denoting a lucrative opportunity for the market’s expansion.

The rising adoption of underground and subsea cabling to meet urban space constraints necessitates specialized insulators, fueling growth in the UK electric insulator market. The deployment of electric vehicle charging infrastructure is increasing the need for proper distribution networks that are equipped with robust insulation solutions. In this regard, Prysmian Group in February 2023 announced that it had entered into a three-year medium-voltage cable agreement with National Grid Electricity Distribution to support the modernization and expansion of the UK’s electricity grid. The project will be supplying cables from Prysmian’s Wrexham plant, mainly aiming to enhance grid reliability, enable greater integration of renewables, and support two-way energy flows across the network. From a strategic perspective, such collaborations in the country will boost the market growth by increasing demand for high-performance insulators and supporting emerging technologies such as electric vehicle networks.

Key Electric Insulator Market Players:

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- NGK Insulators, Ltd. (Japan)

- Hubbell Incorporated (U.S.)

- General Electric Company (U.S.)

- Bharat Heavy Electricals Limited (India)

- Aditya Birla Insulators (India)

- MacLean-Fogg Company (U.S.)

- LAPP Insulators GmbH (Germany)

- Seves Group S.r.l. (Italy)

- Toshiba Corporation (Japan)

- PFISTERER Holding SE (Germany)

- TE Connectivity Ltd. (Switzerland)

- Krempel GmbH (Germany)

- Owens Corning (U.S.)

- Modern Insulators Ltd. (India)

- Electro Porcelain Industries Pvt. Ltd. (India)

- Hitachi Energy Ltd. (Switzerland)

- LS ELECTRIC Co., Ltd. (South Korea)

- Leader Cable Industry Berhad (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Hitachi Energy Ltd. is one of the leading global providers of power grid technologies, which also includes high-voltage insulators and transformer insulation components. The company benefits from a strong expertise in terms of HVDC, substations, and grid integration to supply improved insulation solutions for transmission and renewable energy projects.

- NGK Insulators, Ltd. is also identified as a prominent player in this field that mainly concentrates on ceramic insulators for high-voltage transmission lines and substations. The company is best known for its improved ceramic technologies, and it has a strong presence in the Asia Pacific, North America, and Europe.

- ABB Ltd. is a multinational electrification and automation company that benefits from an extensive product portfolio that includes high-voltage insulators and grid components. The firm is sustaining its leadership, mainly attributable to digital grid technologies, eco-efficient solutions, and strategic partnerships, with a major aim to strengthen its market position.

- Siemens AG, through its energy-focused businesses, plays a highly important role in supplying insulation solutions for transmission and distribution systems. Besides, the company integrates improved materials and digital monitoring technologies with a primary focus on enhancing grid reliability and efficiency.

- Hubbell Incorporated is based in the U.S. and is a prominent manufacturer of electrical and utility infrastructure products, which include porcelain and polymer insulators. The company has a strong focus on product durability, grid resilience, and suitable solutions for utilities and industrial customers.

Below is the list of some prominent players operating in the global electric insulator market:

The electric insulator market hosts both of the global conglomerates and specialized regional manufacturers who are competing through technology innovation, capacity expansion, and geographic diversification. Leading pioneers such as ABB, Siemens, Hitachi Energy, and NGK mainly benefit from their extensive R&D capabilities and integrated power portfolios that efficiently support grid modernization and renewable energy integration. In addition, companies across the globe are making investments in composite and polymer insulators to enhance durability and reduce maintenance costs. In September 2024, Krempel announced that it had acquired 100% of EIC Insulation Company by including its commercial operations and ECC Conversion Center, enhancing its presence in North and South America. The acquisition strengthens Krempel’s product portfolio in electrical insulation for generators, transformers, and motors, hence positively impacting market growth.

Corporate Landscape of the Electric Insulator Market:

Recent Developments

- In January 2026, CNN International Commercial and NGK Insulators, Ltd. have launched a cross-platform campaign highlighting advanced ceramic technologies and their role in sustainability and digital transformation.

- In August 2025, Hitachi Energy India Ltd. announced a total of INR 300 crore (approximately USD 36 million) investment to expand its Mysuru facility, doubling the production capacity of EHV-class transformer-grade pressboard and laminated board to meet demand for transformer insulation materials.

- Report ID: 3736

- Published Date: Feb 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.