Digital Experience Management Market Outlook:

Digital Experience Management Market size was valued at USD 15.4 billion in 2025 and is projected to reach USD 37.8 billion by the end of 2035, rising at a CAGR of 9.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of digital experience management is assessed at USD 16.8 billion.

The global digital experience management market is shaped by the steady expansion of enterprise digital infrastructure, workforce digitization, and rising dependency on cloud-based applications. According to the ITU 2023 data, nearly 5.4 billion people were using the internet in 2023, representing 67% of the global population, creating a sustained pressure on enterprises to maintain consistent digital performance across distributed environments. The European Commission's January 2026 data depicts that the cloud computing services in the EU have surged to 7.42% in 2025, indicating the rising need for continuous monitoring of application responsiveness and employee-facing systems. On the other hand, the change in the work structure has reinforced the need for visibility into endpoint performance and user experience across geographies.

Individuals Using the Internet Worldwide (2023)

|

Year |

Number of Individuals (billion) |

|

2020 |

4.6 |

|

2021 |

4.9 |

|

2022 |

5.1 |

|

2023 |

5.4 |

Source: ITU 2023

Moreover, the governments and public sector digitalization programs are further stimulating the adoption of the market. The United Nations September 2024 data indicates that over 193 countries have implemented national digital transformation strategies, many of which prioritize public service delivery via digital platforms, increasing the scale and complexity of IT environments that must be monitored. Additionally, the cybersecurity and service reliability mandates are influencing procurement, which emphasizes continuous diagnostics and monitoring for federal systems. As organizations align IT operations with service level expectations and compliance requirements, DEM investments are increasingly tied to measurable outcomes such as reduced incident resolution time, improved application uptime, and workforce productivity metrics. This makes the market a critical component within the IT sector.

Key Digital Experience Management Market Insights Summary:

Regional Highlights:

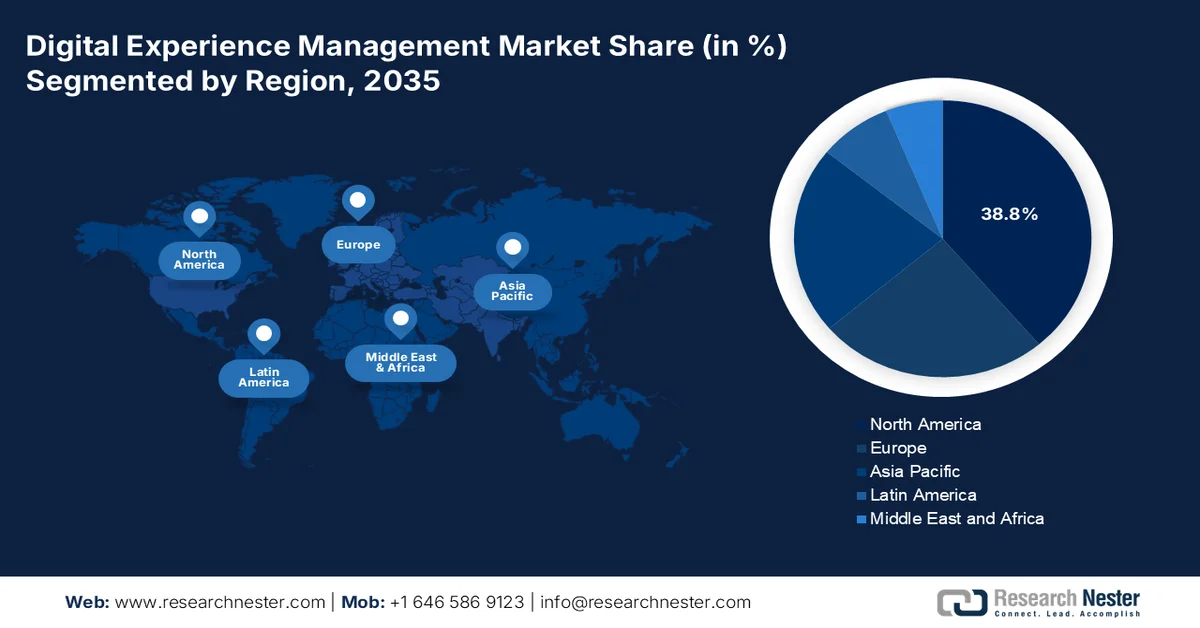

- North America digital experience management market is anticipated to command a 38.8% share by 2035, propelled by rapid cloud adoption and enterprise analytics maturity

- Asia Pacific is projected to witness a CAGR of 14.5% during 2026-2035, fueled by rapid digital government transformation and expanding e-commerce ecosystem

Segment Insights:

- Digital Experience Management Market cloud sub-segment under deployment mode is forecasted to capture 72.3% share by 2035, driven by scalability, AI integration, and lower cost of ownership.

- Large enterprises segment is expected to maintain its leading position through 2035, supported by complex journey orchestration needs and increasing adoption of AI-powered real-time decisioning.

Key Growth Trends:

- Expansion of government digital infrastructure programs

- Change in work structure

Major Challenges:

- Integration with legacy IT systems

- High initial investment and ROI uncertainty

Key Players: Adobe (U.S.), Salesforce (U.S.), Oracle (U.S.), SAP (Germany), Microsoft (U.S.), IBM (U.S.), OpenText (Canada), Sitecore (U.S.), Acquia (U.S.), Optimizely (U.S.), SDL (RWS) (UK), Episerver (Sweden), Liferay (U.S.), Squiz (Australia), Mitsui & Co. (Japan), LG CNS (South Korea), Contentstack (U.S.), Lakeside Software (U.S.), Atos (France), New Relic (U.S.).

Global Digital Experience Management Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 15.4 billion

- 2026 Market Size: USD 16.8 billion

- Projected Market Size: USD 37.8 billion by 2035

- Growth Forecasts: 9.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 1 April, 2026

Digital Experience Management Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of government digital infrastructure programs: Large-scale public investment in digital infrastructure is a primary demand driver for the digital experience management market, as governments require continuous monitoring of the citizen-facing platforms and internal systems. According to the U.S. Department of Commerce, April 2024 data, the U.S. spent USD 11.4 billion on digital infrastructure. Similarly, the European Commission is also supporting digital technologies across the member states. These investments increase the system complexity across cloud endpoints and applications, necessitating visibility into performance and service reliability. The DEM adoption is closely aligned with the government-funded IT transformation programs, mainly where the uptime latency and user satisfaction metrics are tied to public service outcomes.

- Change in work structure: Government-backed workforce digitization policies are stimulating the demand for the market, mainly as hybrid work becomes institutionalized. As per the report from the U.S. Career Institute, April 2024 data, nearly 36% of the employees work remotely, reflecting the sustained reliance on digital tools for productivity. Public sector agencies are also adopting the remote work framework, requiring secure and consistent access to applications across the distributed endpoints. This shift increases the need for monitoring employee experience, device performance, and network reliability. DEM solutions enable IT teams to identify bottlenecks affecting workforce productivity and ensure compliance with service level expectations.

- Cybersecurity and continuous monitoring mandates: Regulatory requirements for continuous diagnostics and monitoring are a significant driver in the market adoption in government environments. These programs require real-time visibility into system performance vulnerabilities and user activity. Similarly, the EU strengthens the requirements for monitoring and incident response across critical sectors. Further, the DEM tools complement cybersecurity frameworks by providing insights into system anomalies, performance degradation, and user-impacting issues. As compliance requirements tighten, organizations are integrating DEM capabilities into broader IT operations and security strategies.

Challenges

- Integration with legacy IT systems: Many enterprises still operate on fragmented legacy systems, making the market integration complex. Vendors must ensure interoperability with ERP, CRM, and ITSM platforms. For example, the top players focus on seamless integration with legacy IT environments. This creates a major hurdle for new players lacking robust APIs or middleware capabilities. Vendors must invest in the connectors APIs and professional services, increasing upfront costs and the implementation timelines, especially in large enterprises with multi-cloud or hybrid infrastructures.

- High initial investment and ROI uncertainty: The market requires an upfront investment in the analytics engines, AI, and cloud infrastructure. Buyers often hesitate due to the unclear ROI. The players bundle DEM into the broader ecosystems to justify value. Further, the enterprises can quantify ROI from digital experience tools, slowing adoption. Vendors entering the market must provide strong value propositions, pilot programs, and measurable KPIs to overcome buyers' skepticism and long sales cycles, mainly among mid-sized enterprises with budget constraints.

Digital Experience Management Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.4% |

|

Base Year Market Size (2025) |

USD 15.4 billion |

|

Forecast Year Market Size (2035) |

USD 37.8 billion |

|

Regional Scope |

|

Digital Experience Management Market Segmentation:

Deployment Mode Segment Analysis

Within the deployment mode segment, the cloud sub-segment is leading and is expected to hold the share value of 72.3% by the end of 2035 in the digital experience management market. The segment is driven by its scalability, AI integration, and lower cost of ownership. Time personalization and omnichannel orchestration are also fueling the segment. The cloud adoption is stimulated as enterprises migrate legacy systems to composable DXM architectures. According to the Eurostat January 2026 data, nearly 52.74% of businesses are using cloud computing services, enabling faster engagement. As AI-driven journey orchestration becomes standard, cloud’s share will continue rising. Further, the cloud will be the undisputed backbone of DXM, supporting billions of real-time interactions across web, mobile, and IoT devices.

Enterprise Size Segment Analysis

Under the enterprise size segment, the large enterprises are leading in the market as they require complex journey orchestration across global customer bases, multiple brands, and legacy systems. DXM spending among large enterprises grew due to post pandemic digital acceleration. The large enterprises have improved the customer journey completion rates after deploying unified DXM platforms. This improvement directly correlates with reduced churn and higher lifetime value. Unlike the SMEs, large firms need dedicated DXM for B2B portals, employee experience, and partner ecosystems. They also face stricter data privacy laws, making enterprise-grade governance essential. The large enterprises will continue leading DXM adoption, leveraging AI-powered real-time decisioning to prioritize millions of simultaneous interactions across web, mobile, and call centers.

Component Segment Analysis

The solutions component, specifically customer data platforms and advanced analytics hold the largest share value in the market. Organizations urgently need to unify siloed customer data for real-time personalization. Solutions include journey scoring, predictive analytics, and AI-driven next best action engines. According to the PIB March 2025 data, the IT sector in India has made a revenue of USD 283 billion in 2024, indicating companies providing innovative solutions for CDP to reduce data breaches and improve compliance with consumer privacy laws. Generative AI now automates content creation based on behavioral triggers, making analytics-rich solutions indispensable. Enterprises are replacing legacy web analytics with CDPs that offer identity resolution and real-time streaming, ensuring solutions remain the highest value component in the DXM market.

Our in-depth analysis of the digital experience management market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Deployment Mode |

|

|

Enterprise Size |

|

|

Application |

|

|

Vertical |

|

|

Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Digital Experience Management Market - Regional Analysis

North America Market Insights

North America is dominating the digital experience management market and is poised to hold the regional revenue share of 38.8% by the end of 2035. The region is driven by the rapid cloud adoption and enterprise analytics maturity. The primary drivers of the market include AI integration and regulatory pressure for data transparency. Moreover, the federal agencies have increased the DXM spending. The National Institute of Standards and Technology reported that enterprises unify customer data across silos. Key trends include a shift toward composable DXM architecture, real-time personalization, and privacy-compliant CDPs. Government digital service mandates in both countries continue to drive procurement, with the U.S. Office of Management and Budget requiring all federal websites to adopt unified experience platforms.

The increasing federal digital service delivery, expanding broadband infrastructure, and rising data utilization across public systems are driving the market in the U.S. According to the Center for Open Data Enterprise, July 2025 data, the U.S. government hosts over 300,000 open datasets reflecting the scale of digital platforms and the need to ensure consistent performance and accessibility across data-driven services. Moreover, the Information Technology & Innovation Foundation's December 2022 data shows that more than 92% of the U.S. population had access to fixed broadband services. Further GSA September 2025 data indicate that federal obligations for IT and digital-related contracts exceeded USD 110 billion in 2023, covering products and services that require continuous monitoring and optimization. These factors are driving demand for the market expansion and growth.

The federal investment in digital government services, broadband expansion, and cloud adoption across public institutions is driving the digital experience management market in Canada. Federal spending on information technology is reflecting the ongoing modernization of digital services and internal systems. According to the Government of Canada, March 2026 data, nearly 90% of households had access to high-speed internet in 2023, enabling broader reliance on digital platforms. Further Government of Canada's May 2025 data noted that 50.9% of businesses adopted at least one digital technology, including cloud computing and data analytics, increasing the need for performance monitoring and user experience optimization. These trends are driving demand for DEM solutions and helping organizations to manage complex digital ecosystems across distributed environments.

Size of Businesses (SMEs) Adopting New Technology (2023)

|

Size of Business |

At least one type of innovation over the last three years |

Held at least one type of intellectual property (as of December 2023) (%) |

Adopted at least one new technology over the last three years (2021 to 2023) (%) |

|

1-4 |

20.9 |

9.1 |

43.7 |

|

5-19 |

33.8 |

19.9 |

56.5 |

|

20-99 |

41.3 |

34.8 |

70.9 |

|

100-499 |

45.7 |

52.0 |

78.6 |

Source: Government of Canada, May 2025

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the digital experience management market and is expected to expand at a CAGR of 14.5% during the assessed period, 2026 to 2035. The region is driven by the rapid digital government transformation, expanding e-commerce ecosystem, and increasing enterprise adoption of AI-powered customer analytics. The key drivers include national digital identity initiatives, which require unified experience platforms for citizen service delivery. The ASEAN Digital Integration Framework reported that cross-border e-commerce has stimulated the adoption among the regional retailers using journey analytics platforms. Multilingual and multicultural service delivery remains a distinct regional requirement.

The large-scale government digitalization programs, growing internet penetration, and increasing enterprise adoption of cloud and digital platforms are fueling the growth of the market in India. According to the PIB April 2025 data, the government continues to invest heavily in digital infrastructure and public service delivery under the Digital India programme, with initiatives such as BharatNet aiming to connect over 250,000 village councils with broadband connectivity. According to the Telecom Regulatory Authority of India, 2024 to 2025 data, India recorded over 944.12 million broadband subscribers, reflecting a vast and growing digital user base. Moreover, the Unified Payments Interface (UPI) is demonstrating the scale and criticality of digital platforms in daily economic activity, thus bolstering the market exposure.

The extensive government-led digital infrastructure development, rapid expansion of internet usage, and large-scale enterprise digitalization are shaping the market in China. According to the NLM study, August 2025 data, the country had over 1.108 billion internet users, representing one of the largest digital user bases globally. Moreover, the National University of Singapore April 2022, reported that China deployed more than 1.43 million 5G base stations supporting high-speed connectivity and data-intensive applications. These developments are increasing the scale and complexity of digital ecosystems, driving demand for DEM solutions that enable real-time monitoring, optimize application performance, and ensure consistent user experience across large, high-traffic platforms in both public and private sectors.

Europe Market Insights

The digital experience management market is shaped by the strict data privacy regulations, public sector digital transformation mandates, and cross-border healthcare interoperability requirements. The key drivers include compliance with the General Data Protection Regulation, which has compelled organizations to implement privacy by design DXM architecture. The European enterprises now embed consent management directly into the customer journey platform. On the other hand, the healthcare digitalization is a significant trend that has stimulated investments in patient portals and unified health records. Additionally, multilingual service delivery drives demand for DXM platforms with localization capabilities. Further, the public sector spending on citizen experience platforms is reflecting the region's commitment to achieving fully digital public services under the European Digital Decade framework.

The strong public investment in digital infrastructure, enterprise digitalization, and increasing reliance on high-performance online services is shaping the market in Germany. According to the OECD 2024 data, Germany allocated over USD 3.27 billion toward digital infrastructure and national AI strategy, supporting the nationwide connectivity improvements. On the other hand, the ITA August 2025 data reported that 77% of enterprises in the country used cloud computing services, reflecting a significant shift toward the digital platforms that require continuous performance monitoring. Further Institut Arbeit und Technik April 2025 data depicts that Germany’s Online Access Act mandates the digitalization of over 575 administrative services, increasing the scale of citizen-facing digital systems. These data show an active market upliftment.

The government-led digital economy expansion, infrastructure development, and investment in innovation are shaping the digital experience management market in the UK. According to the Government of the UK, October 2022 data, superfast broadband coverage has exceeded 97% of premises, while over 67% have access to gigabit-capable broadband, ensuring widespread access to high-speed digital services. Additionally, 92% of the UK landmass is covered by 4G networks, enabling consistent connectivity across both urban and rural regions. On the investment side, government R&D funding accounted for USD 25.6 billion, supporting digital innovation and technology commercialization. The UK’s digital economy is also expanding rapidly, with USD 35.1 billion in private capital invested in tech in 2021, the highest in Europe. These developments collectively drive demand for DEM solutions to ensure a seamless user experience across increasingly complex and large-scale digital ecosystems.

Key Digital Experience Management Market Players:

- Adobe (U.S.)

- Salesforce (U.S.)

- Oracle (U.S.)

- SAP (Germany)

- Microsoft (U.S.)

- IBM (U.S.)

- OpenText (Canada)

- Sitecore (U.S.)

- Acquia (U.S.)

- Optimizely (U.S.)

- SDL (RWS) (UK)

- Episerver (Sweden)

- Liferay (U.S.)

- Squiz (Australia)

- Mitsui & Co. (Japan)

- LG CNS (South Korea)

- Contentstack (U.S.)

- Lakeside Software (U.S.)

- Atos (France)

- New Relic (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Adobe is a pioneer in the market, having significantly advanced the space by integrating generative AI across its Experience Cloud. This advancement ensures real-time personalization and customer journey analytics, enabling enterprises to orchestrate omnichannel content at scale. The company has invested USD 3.944 billion in R&D in 2024.

- Salesforce has redefined the market by embedding DXM data directly into its Customer 360 platform, mainly via Experience Cloud and Einstein AI. This advancement ensures unified real-time engagement across sales, service, and marketing channels, allowing businesses to build intelligent portals and community hubs.

- Oracle has made significant advancements in the market by covering DXM data with its enterprise cloud suite, notably via Oracle CX Unity and Infinity. This advancement ensures real-time behavioral tracking and identity resolution across web, mobile, and offline channels, enabling firms to activate unified customer profiles. The company in the third quarter of 2025 made a revenue of USD 15.9 billion.

- SAP is a strategic player in the market, having advanced the space by integrating DXM data with its backend ERP and customer experience solutions. This advancement ensures real-time contextual engagement that bridges front office experience data with supply chain and logistics insights.

- Microsoft has propelled the market forward by embedding DXM data into its Dynamics 365 Customer Insights and Power Platform, leveraging Azure AI and Copilot capabilities. This advancement ensures real-time sentiment analysis and proactive journey mapping across web app and contact center channels.

Here is a list of key players operating in the global market:

The global digital experience management market is highly competitive, dominated by U.S. based cloud giants, but with strong regional players from Europe and Asia. The key strategic initiatives include aggressive AI integration for predictive analytics and personalization, as seen with Adobe’s Sensei and Salesforce’s Einstein. Major vendors are also focusing on acquisitions to unify customer data platforms with journey analytics, while European firms emphasize GDPR compliant solutions. For example, in January 2025, Contentstack acquired Lytics, the leading real-time customer data platform powering hyper-personalization. Japan and Australia players differentiate via vertically specific offerings, and India players use cost-optimized, scalable platforms. The shift towards composable DXM architectures is a defining trend enabling greater flexibility.

Corporate Landscape of the Digital Experience Management Market:

Recent Developments

- In November 2025, Lakeside Software launched an AI reasoning engine built on 20+ years of expertise in edge telemetry and analytics. The platform lets enterprises rapidly diagnose IT issues that degrade end-user experience by connecting cause and effect across millions of real-time signals.

- In October 2024, Atos launches, in partnership with Nexthink, its state-of-the-art Experience Operations Center (XOC) offering. The joint XOC delivers digital workplace operations that enhance end-user experience through enabling real-time, AI-driven efficiencies and boosting workplace productivity.

- In July 2024, New Relic launched the industry’s first fully integrated, AI-driven Digital Experience Monitoring (DEM) solution to optimize app performance and proactively prevent interruptions to digital experiences.

- Report ID: 8495

- Published Date: Apr 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.