DC Circuit Breaker Market Outlook:

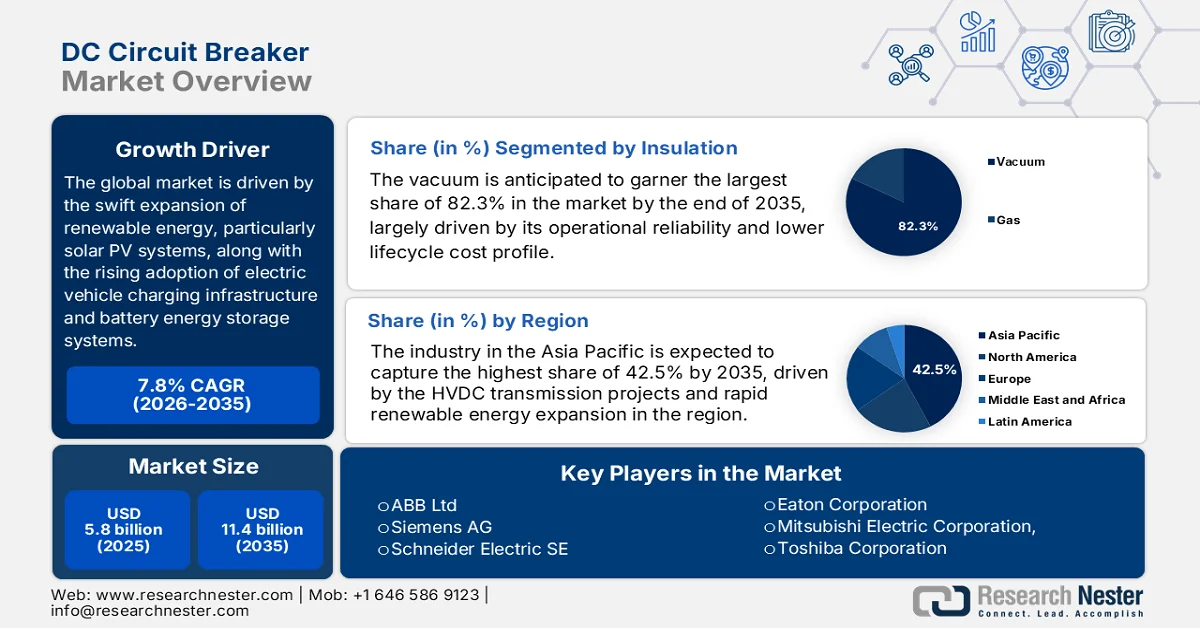

DC Circuit Breaker Market size was valued at USD 5.8 billion in 2025 and is expected to grow steadily to USD 11.4 billion by 2035, registering a CAGR of 7.8% during the forecast period from 2026 to 2035. In 2026, the industry size of DC circuit breaker is assessed at USD 6.2 billion.

The swift expansion of renewable energy, particularly solar PV systems, along with the rising adoption of electric vehicle charging infrastructure, battery energy storage systems, and the modernization of data centers, is responsibly uplifting the global DC circuit breaker market. According to the article published by the International Energy Agency (IEA) in 2024, the global renewable capacity additions are projected to increase from 666 GW in 2024 to nearly 935 GW by the end of 2030, wherein solar PV and wind contribute about 95% of total expansion. Besides, the article also underscores that from 2024 to 2030, cumulative renewable capacity is expected to grow by more than 5,520 GW, representing a 2.6 times increase when compared to the 2017 to 2023 deployment. Meanwhile, the distributed solar PV alone accounts for around 40% of total PV expansion, while utility-scale solar contributes around 80% of overall renewable electricity growth, thus driving huge demand for DC circuit breakers.

Most of the industries are making a shift towards current power distribution, due to which demand for high-speed protection solutions is rising, notably solid-state and hybrid breakers that provide faster switching and improved efficiency. In this context, the study published by the National Institute of Health (NIH) in July 2024 states that DC circuit breakers are highly critical for fast fault isolation in HVDC grids, where fault currents rise rapidly due to low system damping. Besides, the proposed current-injection multiport assembly design enables controlled zero-crossing of current, improving interruption capability, thereby efficiently reducing reliance on large series configurations of power electronic devices. The research indicates that conventional designs require handling fault currents that exceed 15 kA, sometimes demanding extensive IGBT arrays, which remarkably increase system cost and complexity. By replacing these with IGCT-based resonant current injection and optimized component sizing, the study demonstrates reduced component count, lower cost, and improved operational reliability, thus benefiting the overall market.

Key DC Circuit Breaker Market Insights Summary:

Regional Highlights:

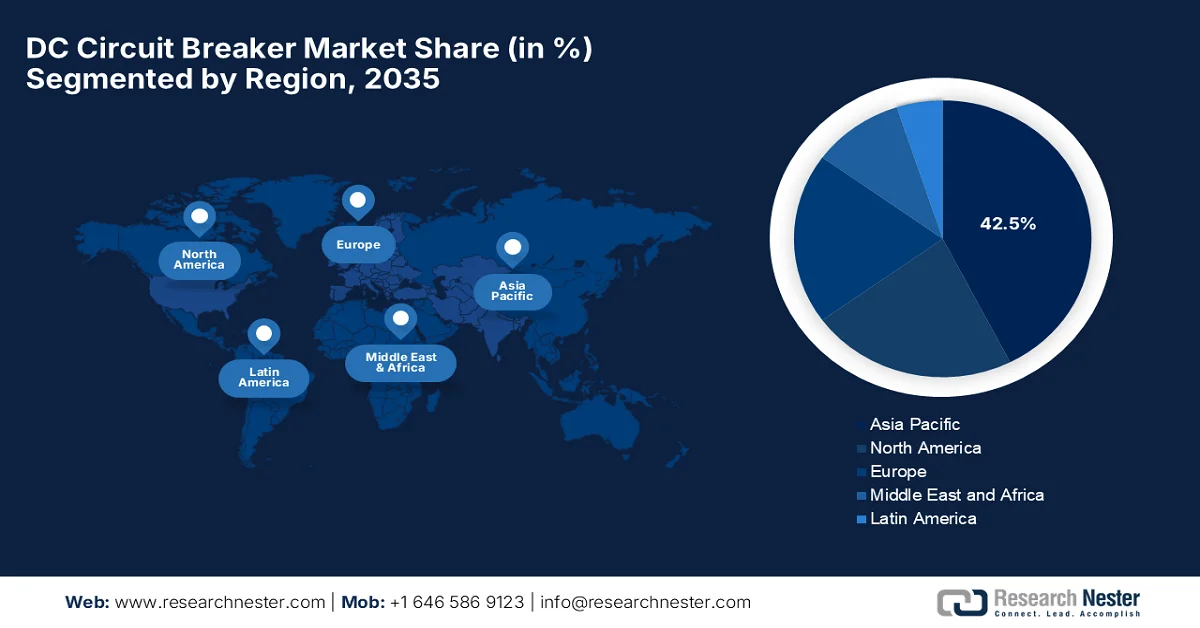

- Asia Pacific DC circuit breaker market is projected to hold a dominant 42.5% share by 2035, attributed to expanding HVDC infrastructure, accelerating renewable deployments, and robust EV ecosystem growth

- North America is anticipated to experience significant expansion over the forecast period, impelled by intensifying grid modernization initiatives and rising electric vehicle adoption

Segment Insights:

- The vacuum segment in the DC circuit breaker market is expected to command an 82.3% share by 2035, driven by its high operational reliability and lower lifecycle cost advantages

- The hybrid segment is forecast to secure a considerable revenue share by 2035, fueled by its balanced performance, cost efficiency, and suitability for large-scale DC applications

Key Growth Trends:

- Growth of electric vehicles and charging infrastructure

- Expansion of HVDC transmission systems

Major Challenges:

- Arc extinction challenge

- Rapid fault current rise in DC networks

Key Players: ABB Ltd (Switzerland), Siemens AG (Germany), Schneider Electric SE (France), Eaton Corporation plc (Ireland), Mitsubishi Electric Corporation (Japan), Toshiba Corporation (Japan), Fuji Electric Co., Ltd. (Japan), Hitachi Energy Ltd. (Switzerland), Larsen & Toubro Limited (India), CG Power and Industrial Solutions Limited (India), C&S Electric Limited (India), Powell Industries, Inc. (U.S.), Rockwell Automation, Inc. (U.S.), Sensata Technologies, Inc. (U.S.), Legrand SA (France), National Grid (UK), General Electric Company (U.S.), Hyundai Electric & Energy Systems Co., Ltd. (South Korea), ENTEC Electric & Electronic Co., Ltd. (South Korea), Schaltbau Holding AG (Germany), Sécheron Hasler Group (Switzerland).

Global DC Circuit Breaker Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.8 billion

- 2026 Market Size: USD 6.2 billion

- Projected Market Size: USD 11.4 billion by 2035

- Growth Forecasts: 7.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, India

- Emerging Countries: South Korea, Brazil, Mexico, Saudi Arabia, Indonesia

Last updated on : 17 April, 2026

DC Circuit Breaker Market - Growth Drivers and Challenges

Growth Drivers

- Growth of electric vehicles and charging infrastructure: The rise in EV adoption globally is readily accelerating demand in the DC circuit breaker market as EV batteries operate on DC systems. Also, the fast-charging stations require proper performing DC protection, and this creates heightened demand for advanced DC breakers in transport and charging networks. In this context, IEA in 2025 reported there is a continued expansion of charging infrastructure worldwide, wherein the public chargers doubled since 2022 and surpassed almost 5 million. It mentioned that China leads with 65% of global chargers and 60% of EV stock, whereas Europe grew over 35% in 2024, supported by regulations that are mandating fast-charging stations along major roads. The U.S. increased its network by 20%, whereas India and other emerging markets are accelerating deployment through strong policy support, thus benefiting the overall market upliftment.

- Expansion of HVDC transmission systems: Utilities are mostly deploying high-voltage direct current networks for long-distance power transmission with lower losses and cross-border electricity trade. These circuit breakers are considered to be highly essential for isolating faults in HVDC systems, driving growth in the market. In September 2023, the U.S. Department of Energy’s Office of Electricity and Wind Energy Technologies Office announced almost USD 10 million in funding to advance HVDC voltage source converter systems with a main goal to lower costs and boost renewable integration. It also underscores that HVDC offers efficiency over long distances, enables connections between asynchronous grids, and supports resilience by facilitating reserve sharing. Initiatives such as the HVDC CORE program target a 35% cost reduction by 2035, positioning HVDC as an important attribute for a reliable, carbon-free grid future.

- Grid modernization and smart grid deployment: The worldwide electricity infrastructure is being developed with a prime focus on improving automation and real-time fault detection. Modern grids necessitate advanced DC protection systems, prompting a profitable business environment for pioneers in the market. In this context, the UN Sustainable Development Solutions Network in March 2026 reported that smart grids are emerging as the backbone of modern energy systems, which are especially designed to enhance resilience, reliability, and sustainability in the face of climate change and rising demand. They integrate advanced monitoring, automation, and digital communication technologies to enable two-way interaction between utilities and consumers, thereby supporting renewable energy, storage, and distributed resources. Hence, these evidence-based studies denote that the accelerated global deployment of smart grids will drive demand for the DC circuit breakers as essential components for ensuring grid stability.

Challenges

- Arc extinction challenge: One of the most fundamental challenges in the DC circuit breaker market is the arc extinction. In the AC systems, the current naturally crosses zero many times per second, whereas in DC, current flows continuously without natural zero-crossing. This makes it extremely difficult to interrupt fault currents once an arc is formed. As a result, DC breakers must actively force current interruption by utilizing very complex mechanical or fully solid-state techniques. Also, this sustained arc energy increases the risks of overheating, insulation breakdown, fire hazards, and equipment damage. Therefore, to address this, improved arc management systems such as vacuum interrupters, power electronics, and ultra-fast switching devices are highly required. Moreover, these solutions significantly increase design complexity and cost, making expansion difficult for the market.

- Rapid fault current rise in DC networks: The DC systems, especially in terms of microgrids and renewable integrated networks, mostly witness huge, fast fault escalation. Also, in some cases, fault currents can rise to 100 times within milliseconds. This rapid surge adds extreme electrical and thermal stress on system components, which include cables, converters, and circuit breakers. The speed of fault propagation leaves very little reaction time for protective devices, requiring ultra-fast detection and interruption mechanisms. At the same time, the traditional protection systems are often inadequate for such conditions. As a result, DC circuit breakers must be designed with advanced sensing, predictive algorithms, and high-speed switching capabilities. This requirement significantly increases system complexity and makes real-world implementation more difficult.

DC Circuit Breaker Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.8% |

|

Base Year Market Size (2025) |

USD 5.8 billion |

|

Forecast Year Market Size (2035) |

USD 11.4 billion |

|

Regional Scope |

|

DC Circuit Breaker Market Segmentation:

Insulation Segment Analysis

The vacuum, which is based on the insulation segment, is anticipated to garner the largest share of 82.3% in the DC circuit breaker market by the end of 2035. The segment’s dominance is largely driven by its operational reliability and lower lifecycle cost profile. Their ability to interrupt DC arcs without the need for complex gas handling systems supports increased deployment across medium-voltage applications, including rail electrification, renewable integration, and industrial distribution networks. When compared to gas-insulated alternatives, vacuum breakers offer a more compact footprint and reduced maintenance burden, thereby making it suitable with procurement priorities focused on uptime and cost control. In addition, their established performance in handling frequent switching operations and fault isolation deliberately solidifies their position as the preferred insulation technology across utility as well as industrial installations, thus denoting a wider segment scope.

Type Segment Analysis

By the end of 2035, the hybrid segment is anticipated to grow with a considerable revenue share in the market. The hybrid DC circuit breakers offer an optimal balance between performance, cost, and operational reliability. Industry-validated analysis found that by combining conventional mechanical switching with power electronic components, hybrid breakers are capable of efficiently handling fault current interruption, thereby limiting the thermal and energy losses associated with fully solid-state solutions. This makes them highly suitable for large-scale deployment in renewable energy integration, electric vehicle charging infrastructure, and industrial DC distribution networks, where both fast fault isolation and economic feasibility are highly essential. At the same time, their comparatively lower cost and higher efficiency in continuous operation give them a clear advantage over solid-state DC circuit breakers, despite offering ultra-fast switching and superior control precision.

End user Segment Analysis

In terms of the end user, the transmission and distribution utilities segment is expected to grow with a considerable revenue share in the market during the discussed timeframe. The segment’s growth is largely propelled by ongoing grid modernization and electrification efforts worldwide. Increasing electricity demand and aging infrastructure are pushing utilities to upgrade their networks with advanced protection systems. In December 2023, the article published by the Press Information Bureau (PIB) reported India’s push toward a modern, smart electricity transmission system. The country has significantly expanded its transmission network, reaching 4.8 lakh circuit km and 1213 GVA transformation capacity, by efficiently integrating the entire nation into a single synchronized grid. To support modernization, a government task force led by POWERGRID has recommended advanced upgrades, including digital control centers, cybersecurity systems, and AI, ML-based predictive maintenance, thus making it suitable for standard segment growth.

Our in-depth analysis of the DC circuit breaker market includes the following segments:

|

Segment |

Subsegments |

|

Insulation |

|

|

Type |

|

|

End user |

|

|

Voltage |

|

|

Installation |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

DC Circuit Breaker Market - Regional Analysis

APAC Market Insights

The Asia Pacific DC circuit breaker market is predicted to capture the largest share of 42.5% by the end of the forecast period. The large-scale HVDC transmission projects, rapid renewable energy expansion, and strong EV ecosystem growth are the main factors behind the region’s leadership. Key factors fueling this surging growth are the urgent need for safe, efficient DC protection in solar power systems, data centers, and the expanding electric vehicle charging network. In March 2025, the article published by Climate Scorecard disclosed that Japan’s EV industry is anticipated to reach nearly USD 111.10 billion by 2030, growing at a CAGR of 15.5%. In 2023, the country had about 31,600 public EV chargers, and its EV charging equipment category is expected to hit USD 1.54 billion by 2030 and USD 3.50 billion by 2045, with a CAGR of 14.17%, hence denoting an optimistic market opportunity for DC circuit breakers.

The intense investments in renewable energy generation, electric vehicle charging infrastructure, and advanced smart grid modernization are responsible for uplifting the market in China. The country benefits from extensive manufacturing capabilities and increasing adoption of hybrid and solid-state, or advanced technology, circuit breakers for improved power reliability. For instance, in August 2024, Hitachi Energy delivered China’s first SF6-free 420 kV dead tank breaker to the State Grid Corporation of China, marking a major step in grid decarbonization. The breaker is a part of the EconiQ portfolio, and it replaces SF6 with a sustainable gas mixture by maintaining reliability and compact design. Therefore, such instances solidify the country’s carbon-neutrality goals and showcase eco-efficient innovation at the highest voltage levels.

The expansion in renewable energy projects, especially solar, and rapid industrial automation are certain factors that are supporting the development of the DC circuit breaker market in India. At the same time, rising demand for electric vehicles and infrastructure, along with the modernization of power grids, is boosting the need for low and medium-voltage direct current systems. In this context, BHEL, in partnership with Hitachi Energy India, in November 2024 announced that it secured an order from POWERGRID to set up a +800 kV, 6000 MW HVDC link between Khavda and Nagpur. Besides, this project will evacuate renewable power from Khavda’s energy zone and support the country’s target of 500 GW of renewable capacity by 2030. BHEL will supply key equipment such as converter transformers, thyristor valves, and design the 765/400 kV evacuation system, solidifying its leadership in HVDC projects under the Make in India initiative.

North America Market Insights

The North America DC circuit breaker market is expected to witness noteworthy growth during the stipulated timeline. The region’s market growth is mainly propelled by the urgent need for grid modernization and the increasing adoption of electric vehicles. The proliferation of solid-state and vacuum technologies for improved safety, and the growth of intelligent, connected devices to support smart grids are some of the visible trends uplifting the regional market’s growth. In April 2024, the article published by Gridwise Alliance stated that the U.S. is accelerating grid modernization with federal acts such as the IIJA and IRA, aiming for 100% carbon pollution-free electricity by 2035. Besides, the studies suggest grid capacity must double or even triple to meet this target, highlighting the urgency of smart, resilient networks. States such as Massachusetts, Colorado, New York, and California are leading with innovative policies, pilots, and flexibility goals, driving huge demand for DC circuit breakers.

Technological innovation towards hybrid and solid-state breakers allows for faster, more efficient interruption in high-power applications, thus driving the growth of the DC circuit breaker market in the U.S. The market is extensively supported by initiatives that are aimed at increasing grid stability and reducing overall carbon emissions across industrial and residential sectors. In this context, the U.S. Department of Energy’s Office of Electricity and Wind Energy Technologies Office, in February 2025, announced a total of USD 8 million in funding for R&D projects on high-voltage direct current circuit breakers. Out of this, USD 7 million comes from OE and USD 1 million from WETO, which target critical gaps in HVDC system protection. Projects will focus on creating technical standards for HVDC breakers and developing innovative, cost-effective designs to expand adoption.

Increased investments in solar photovoltaic projects and battery energy storage systems are elevating the demand in the DC circuit breaker market in Canada. At the same time, the expansion of data centers and the proliferation of DC-based microgrids are efficiently boosting the adoption of low-voltage and high-voltage DC breakers across various sectors. Based on the December 2024 data published by the country’s government, the University of Toronto, with ecoEII funding of USD 560,000 toward a USD 1.08 million project, developed two novel DC arc-free circuit breaker concepts for utility-grid battery storage systems. DC-CB-1 is a bidirectional electronic switch with an auxiliary suppression circuit for transient-free operation, whereas DC-CB-2 is a fast mechanical switch with arc suppression. These innovations enhance safety and reliability, supporting large-scale battery storage integration along with the renewable energy transition.

Europe Market Insights

The rise of hyperscale data centers and DC microgrids is readily accelerating the adoption of high-performance protection solutions with the main goal of minimizing energy conversion losses, benefiting the overall market in Europe. Technological innovation is a major contributor to this shift, with a clear move toward eco-friendly, SF₆-free, and solid-state breakers that best align with stringent environmental regulations. In the official study published in November 2023, WG2 reports that realizing multi-vendor HVDC systems requires a clear legal and regulatory framework by covering governance, competition law, and interoperability. In this context, standardization needs to follow FRAND principles to ensure fair IP access by balancing vendor confidentiality and licensing fees. These multi-vendor HVDC grids introduce shared responsibility and complex risk allocation, thus encouraging widespread adoption in this sector.

The nation's ambitious Energiewende energy transition is the main driving factor behind the market in Germany. The market is also energized by the accelerating rollout of electric vehicle charging infrastructure, specifically high-power DC fast-charging stations, and the proliferation of data centers that utilize DC-based microgrids for improved efficiency. In March 2024, Siemens Smart Infrastructure announced the launch of a new 400 kW SICHARGE D fast charger, which is capable of charging up to four vehicles simultaneously with one grid connection. The company notes that this product is especially designed for highway, destination, and public charging, and it delivers continuous stable output even at high ambient temperatures. Such innovations support the region’s Fit for 55 climate goals, reducing charging times for cars and trucks, thus driving demand for DC circuit breakers.

In the UK, the DC circuit breaker market is positioned for sustained strategic growth in the upcoming years, owing to the accelerated shift toward a low-carbon economy and modernized electrical infrastructure. On the other hand, technological advancements are steering the industry toward solid-state and hybrid circuit breakers, which offer faster interruption times and better integration with smart grid technologies. In 2023, SSEN Transmission secured USD 9 million from Ofgem’s Strategic Innovation Fund to advance two projects into the Beta phase. The Network DC Circuit Breakers project, which is worth about USD 7.6 million, enabled HVDC hubs to integrate offshore wind more efficiently, reducing infrastructure and costs. The Incentive project, which was valued at USD 1.4 million, tests advanced grid control and storage solutions to strengthen stability, hence suitable for bolstering the country’s overall market growth.

Key DC Circuit Breaker Market Players:

- ABB Ltd (Switzerland)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- Eaton Corporation plc (Ireland)

- Mitsubishi Electric Corporation (Japan)

- Toshiba Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Hitachi Energy Ltd. (Switzerland)

- Larsen & Toubro Limited (India)

- CG Power and Industrial Solutions Limited (India)

- C&S Electric Limited (India)

- Powell Industries, Inc. (U.S.)

- Rockwell Automation, Inc. (U.S.)

- Sensata Technologies, Inc. (U.S.)

- Legrand SA (France)

- National Grid (UK)

- General Electric Company (U.S.)

- Hyundai Electric & Energy Systems Co., Ltd. (South Korea)

- ENTEC Electric & Electronic Co., Ltd. (South Korea)

- Schaltbau Holding AG (Germany)

- Sécheron Hasler Group (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ABB Ltd leads with the strongest and most mature portfolio, which spans both high-voltage HVDC breakers and low-voltage solid-state DC protection systems. The company has successfully pioneered one of the first functional HVDC circuit breaker concepts, thereby enabling multi-terminal DC grids and large-scale renewable integration.

- Siemens Energy is a major force in HVDC transmission systems and DC grid protection, with strong knowledge in power electronics, grid automation, and HVDC infrastructure integration. Besides, the firm is highly focused on system-level HVDC solutions where DC breakers are incorporated into broader transmission architectures.

- Schneider Electric SE is a leading player in low-voltage DC circuit protection, particularly in emerging categories such as EV charging infrastructure, data centers, and industrial DC microgrids. The company dominates in terms of the LVDC segment through advanced digital protection devices and smart electrical distribution systems.

- Mitsubishi Electric Corporation is considered to be a prominent player in HVDC systems, industrial power electronics, and DC protection devices, with a very strong emphasis on high-reliability engineering. In addition, the company is proactively developing DC circuit breaker technologies for HVDC transmission, battery energy storage systems, and renewable integration projects.

- Eaton Corporation plc is a significant global player in electrical protection systems, which includes LVDC circuit protection for industrial, commercial, and data center applications. The firm is more concentrated on data centers, EV charging systems, aerospace, and industrial automation, where DC power demand is rapidly increasing.

Below is the list of some prominent players operating in the global market:

The DC circuit breaker market is being led by global electrical giants such as ABB, Siemens, Schneider Electric, and Mitsubishi Electric, which lead HVDC and solid-state breaker innovation. At the same time, Europe-based firms are highly focused on HVDC grid protection and hybrid breaker technologies, whereas companies from Japan emphasize high-reliability switching systems for industrial and energy storage applications. Meanwhile, the players originated from the U.S., such as Eaton and Rockwell, concentrate on LVDC protection for data centers and EV infrastructure. Joint development agreements, SF6-free technologies, digital monitoring integration, and expansion into EV charging and renewable energy grids are some of the tactical strategies adopted by leading pioneers in this sector. In March 2022, Siemens Energy and National Grid announced a collaboration to upgrade a Massachusetts substation with SF6-free blue circuit breakers by using clean air insulation and vacuum switching technology. This pioneering installation will cut greenhouse gas emissions and support both companies’ net-zero carbon goals.

Corporate Landscape of the DC Circuit Breaker Market:

Recent Developments

- In December 2025, Siemens announced the launch of data center solution 5.0 in China, debuting innovative DC power distribution products such as SENTRON 3VA series circuit breakers to support next-generation AI-driven data centers. The solution integrates software, hardware, and AI applications to make computing power smarter, greener, and safer.

- In August 2024, Mitsubishi Electric and Siemens Energy signed an agreement to co-develop DC Switching Stations and DC Circuit Breaker specifications with a main goal to accelerate the deployment of multi-terminal HVDC systems. This collaboration supports the efficient integration of large-scale renewable energy resources and contributes to global decarbonization efforts.

- Report ID: 5136

- Published Date: Apr 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.