Data Center Power Market Outlook:

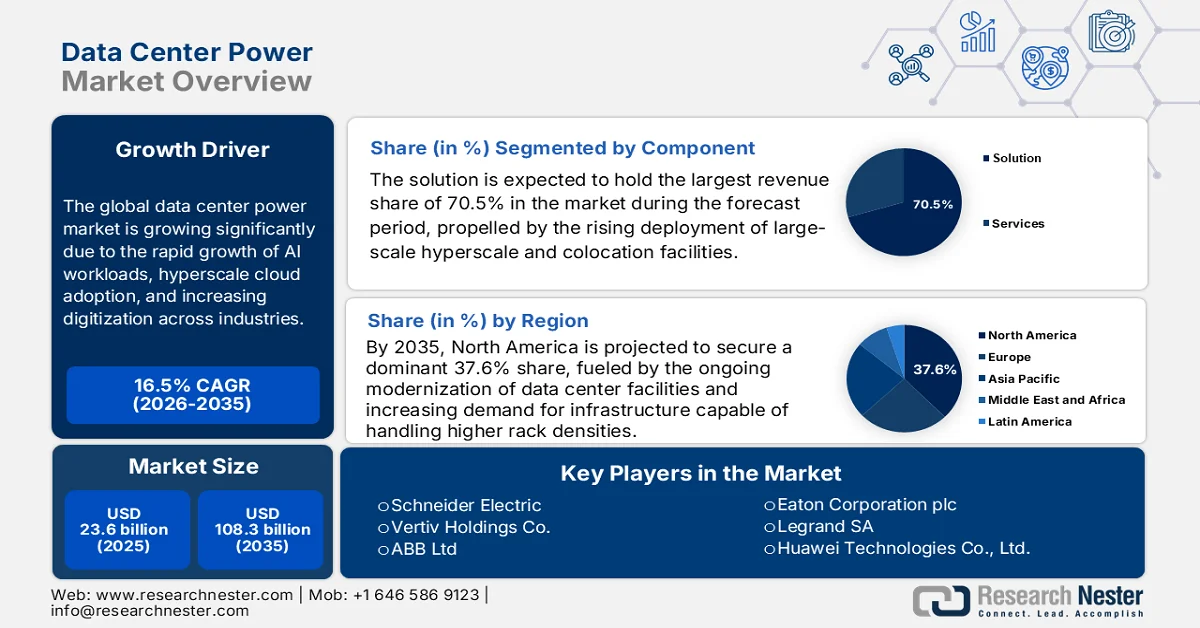

Data Center Power Market size was valued at USD 23.6 billion in 2025 and is projected to cross USD 108.3 billion by the end of 2035, expanding at more than 16.5% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of data center power is evaluated at USD 27.4 billion.

The data center power market is poised for extensive growth, effectively catalyzed by the rapid growth of AI workloads, hyperscale cloud adoption, and increasing digitization across industries. Power is becoming a core design constraint in data center planning, which in turn is shifting decision-making from connectivity-led site selection to electricity availability, grid interconnection speed, and long-term energy security. In this context, the report published by the International Energy Agency in April 2026 revealed that in 2025, electricity demand from data centers surged by 17%, whereas AI-focused centers grew even faster. It also mentioned that capital expenditure by five major tech firms exceeded a substantial value of USD 400 billion in 2025, with projections of a further 75% rise in 2026. By the end of 2030, overall data center electricity consumption is expected to double, with AI-specific centers set to triple, hence denoting a lucrative growth opportunity for the market.

Furthermore, utilities and regulators are adapting planning frameworks to manage concentrated load growth and ensure grid stability. On the other hand, to maintain operational continuity, the market is accelerating the adoption of alternative baseload technologies, fuel cells, and advanced liquid cooling systems. In January 2024, Caterpillar, in collaboration with Microsoft and Ballard Power Systems, announced the successful demonstration of the use of large-format hydrogen fuel cells to provide reliable backup power for multi-megawatt data centers. It was conducted at Microsoft’s Cheyenne, Wyoming facility, and the project validated performance under challenging conditions, which include 48 hours of continuous operation at 6,086 ft elevation and below-freezing temperatures.

Key Data Center Power Market Insights Summary:

Regional Highlights:

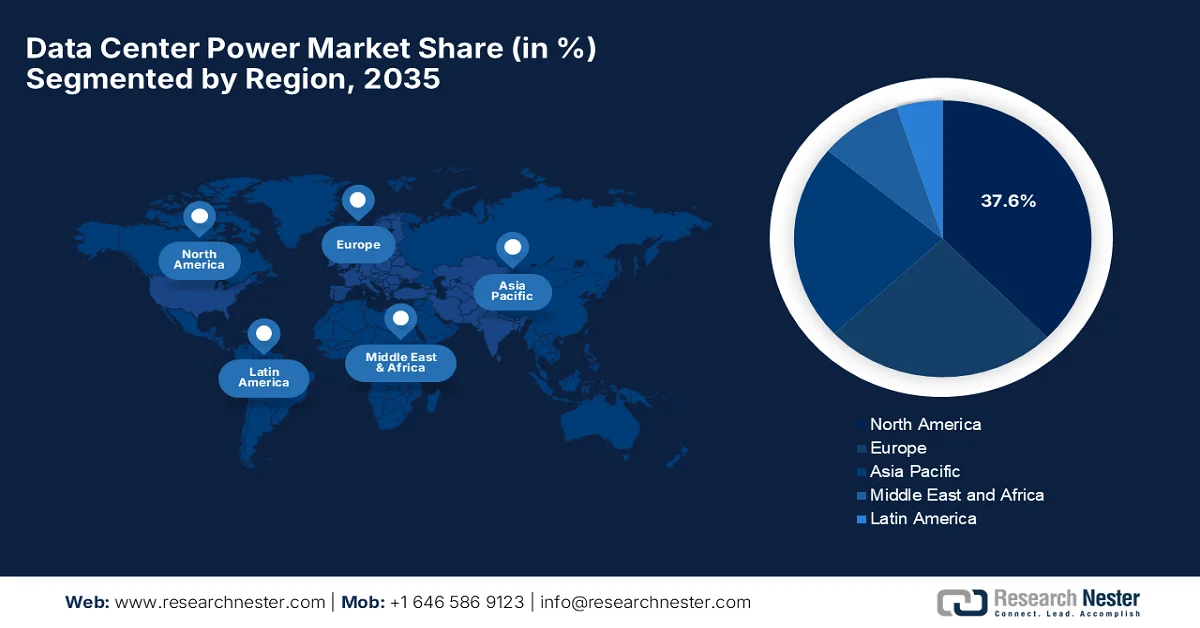

- North America is projected to command 37.6% of the data center power market by 2035, reinforced by the ongoing modernization of existing data center infrastructure and the need to support higher rack densities and next-generation workloads

- Asia Pacific is poised to witness the fastest growth in the market throughout 2026-2035, stimulated by digital transformation, widespread 5G rollouts, and escalating AI workloads of massive online populations

Segment Insights:

- The solution segment is forecast to capture 70.5% of the data center power market by 2035, bolstered by the rising deployment of large-scale hyperscale and colocation facilities that require fully integrated power infrastructure

- The UPS segment is expected to secure a considerable revenue share by 2035, accelerated by increasing adoption of edge computing and distributed infrastructure, which is boosting demand for compact UPS systems that can maintain reliability in decentralized environments

Key Growth Trends:

- Global edge computing and 5G rollouts

- Hyperscale footprint expansion

Major Challenges:

- Grid constraints and power availability

- Sustainability and carbon reduction pressures

Key Players: Schneider Electric (France),Vertiv Holdings Co. (U.S.),ABB Ltd. (Switzerland),Eaton Corporation plc (Ireland),Legrand SA (France),Huawei Technologies Co., Ltd. (China),Delta Electronics, Inc. (Taiwan),Siemens AG (Germany),Mitsubishi Electric Corporation (Japan),Cummins Inc. (U.S.),Generac Power Systems, Inc. (U.S.),Hitachi Energy Ltd. (Switzerland),Chevron Corporation (U.S.) ,Engine No. 1 (U.S.) ,NextEra Energy, Inc. (U.S.).

Global Data Center Power Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 23.6 billion

- 2026 Market Size: USD 27.4 billion

- Projected Market Size: USD 108.3 billion by 2035

- Growth Forecasts: 16.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (37.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Indonesia, Vietnam

Last updated on : 26 June, 2026

Data Center Power Market - Growth Drivers and Challenges

Growth Drivers

- Global edge computing and 5G rollouts: The continued rise of 5G, autonomous systems, and connected factory automation necessitates decentralized, localized data processing. This shift drives the deployment of compact edge data centers, which are situated closer to end users rather than in major tech hubs. Therefore, the demand has been booming for modular, weather-proof power units and self-contained microgrids worldwide, driving the market growth. For instance, in June 2026, Verizon, in partnership with AWS, announced the launch of the world’s first mobile edge computing platform by using AWS Wavelength on Verizon’s 5G Ultra Wideband network. This allows developers to build ultra-low latency applications directly at the edge, and hence the platform demonstrates the prominence of 5G-driven edge computing, requiring distributed, compact edge sites with reliable localized power and compute resources.

- Hyperscale footprint expansion: Cloud service providers across major nations are expanding their infrastructure, building massive industrial campuses that are designed to scale into gigawatt capacities. To secure a competitive edge, operators are purchasing regional power rights years before construction begins. This hyperscale shift is accelerated as corporations decommission legacy on-premise server closets for power-optimized third-party facilities, prompting a profitable business environment for pioneers in the market. In May 2023, AWS announced a major investment of USD 12.7 billion into cloud infrastructure in India by 2030, bringing its total commitment to USD 16.4 billion. This expansion is expected to contribute USD 23.3 billion to India’s GDP and support the consistent growth of the market globally.

Challenges

- Grid constraints and power availability: The rising number of hyperscale and colocation data centers is adding pressure on existing power grids worldwide. In most of the key markets, utilities are facing challenges to provide the large amounts of electricity which is required for new data center developments, resulting in project delays and connection bottlenecks. This challenge is particularly severe in regions that are experiencing rapid AI infrastructure expansion. In this context, data center operators are forced to explore alternative power sources, on-site generation, and energy storage solutions to ensure reliable operations. These alternatives often involve substantial capital investments, which in turn create barriers to market expansion.

- Sustainability and carbon reduction pressures: Data centers across most nations face pressure from governments and investors to reduce carbon emissions. The demand for computing power continues to rise, but still, organizations are expected to minimize their environmental impact through energy-efficient infrastructure and renewable energy integration. Achieving these objectives is challenging since high-density AI workloads consume huge amounts of electricity and generate significant heat. In this context, companies need to make investments in advanced power management systems, battery storage technologies, and renewable energy procurement strategies to meet sustainability targets. Hence, balancing operational reliability and environmental commitments is a major challenge in the global market.

Data Center Power Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

16.5% |

|

Base Year Market Size (2025) |

USD 23.6 billion |

|

Forecast Year Market Size (2035) |

USD 108.3 billion |

|

Regional Scope |

|

Data Center Power Market Segmentation:

Component Segment Analysis

The solution, which is under the component category, is expected to hold the largest revenue share of 70.5% in the data center power market during the forecast period. The segment’s dominance is effectively propelled by the rising deployment of large-scale hyperscale and colocation facilities that require fully integrated power infrastructure. These facilities demand end-to-end solutions that combine power conditioning, distribution, monitoring, and backup systems to ensure continuous operations under high-density computing loads. In December 2024, Meta announced that it is building its largest data center in Richland Parish, Louisiana, which is a 4 million-square-foot facility delivering over two gigawatts of compute power to accelerate AI innovation. This massive investment will strengthen Meta’s global infrastructure and boost northeast Louisiana’s economy, thus denoting a wider segment scope.

Solution Segment Analysis

In terms of solution, the UPS segment is anticipated to grow with a considerable revenue share in the market during the stipulated timeframe. The sub-type’s growth is majorly driven by increasing adoption of edge computing and distributed infrastructure, which is boosting demand for compact UPS systems that can maintain reliability in decentralized environments. In April 2024, Schneider Electric announced new AI-ready data center solutions to address energy and sustainability challenges. Besides, the company also introduced the Galaxy VXL UPS, which is a compact, high-density power system delivering 52% space savings, thus strengthening its mission to decarbonize digital infrastructure while enabling scalable AI deployments, and hence denoting a huge opportunity for the segment to grow in the next decade.

End use Segment Analysis

By the end of 2035, the BFSI segment is predicted to garner a noteworthy share in the market. The segment is supported by stringent regulatory compliance requirements and continuous uptime needs for financial transactions. In addition, the rapid digitization of banking services and the increasing deployment of secure and high-availability IT infrastructure across banking, financial services, and insurance institutions are also propelling the segment’s upliftment. For instance, in September 2023, Infosys completed the acquisition of Danske Bank’s IT center in India to strengthen its footprint in the Nordics. The center will accelerate Danske Bank’s digital transformation by enhancing IT operations and customer-facing solutions, and support the bank’s priorities of modernizing technology.

Our in-depth analysis of the data center power includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Solution |

|

|

End use |

|

|

Service |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Data Center Power Market - Regional Analysis

North America Market Insights

The North America data center power market is anticipated to garner the highest share of 37.6% during the forecast duration. The region’s dominance is fueled by the ongoing modernization of existing data center infrastructure and the need to support higher rack densities and next-generation workloads. To meet the demands of AI training, enterprise cloud adoption, and data sovereignty regulations, most of the legacy facilities are being retrofitted with advanced power systems. In May 2026, the government data revealed that U.S. data centers consumed about 176 TWh of electricity in 2023, which is equal to 4.4% of national usage, and the demand is projected to double or triple by 2028. Nearly half of this energy comes from IT equipment, whereas the rest is largely for cooling and thus positively impacts the market’s expansion.

The continued scaling of hyperscale campuses and high-density artificial intelligence workloads across major domestic infrastructure corridors is responsibly boosting the overall U.S. data center power market. This hyper-growth is readily transforming the electrical architecture of facilities, thereby driving a massive wave of procurement for high-capacity uninterruptible power supply systems, intelligent power distribution units, and heavy-duty switchgear. In February 2026, a Harvard Kennedy School policy brief stated that U.S. data center electricity demand could rise from 176 TWh in 2023 to 325 to 580 TWh by 2028, or up to 12% of national consumption. The report also highlighted certain risks to grid reliability, whereas the tech giants invested more than USD 200 billion in 2024 CapEx for hyperscale buildouts, hence making it suitable for standard market growth.

In Canada data center power market has gained immense exposure as international cloud providers and domestic enterprises capitalize on the country's abundance of clean, low-cost electricity and favorable ambient temperatures. Hyperscalers are deploying in certain digital corridors to support intensive artificial intelligence and high-performance computing workloads. Based on the government data published in October 2024, Canada’s energy regulator reported that the country had 239 operating data centers, wherein the demand was rising sharply due to AI workloads. It also mentioned that Canada’s appeal lies in its low-cost hydroelectric power, clean grid, and cool climate, while projects such as QScale’s Q01 in Quebec are pioneering waste heat recovery, redirecting nearly 100 MW to households.

APAC Market Insights

The Asia Pacific market is anticipated to grow at the quickest rate from 2026 to 2035. The region’s upliftment is majorly driven by the digital transformation, widespread 5G rollouts, and escalating AI workloads of the massive online populations. To power the region’s dense server architectures while moving toward corporate sustainability goals, operators are proactively transitioning toward hybrid energy strategies. Based on the government data published in September 2025, Singapore refreshed its Green Data Center Roadmap to balance digital growth with sustainability, targeting at least 300 MW of new capacity supported by green energy. It also mentioned key initiatives, which include the Green Mark for DCs 2024, raising sustainability standards; the Energy Efficiency Grant, co-funding upgrades to efficient IT equipment; and the new SS 715:2025 standard, which aims to cut IT energy use by 30%.

The synchronized push for deep digital transformation and national cloud integration, which is guided by state-level infrastructure blueprints, is uplifting the overall China data center power market. Under nationwide resource rebalancing initiatives, developers are shifting away to massive compute clusters toward inland regions rich in raw energy reserves, reshaping domestic transmission pipelines. Based on the government data published in July 2024, China introduced a national action plan for green data centers, thereby setting ambitious efficiency and sustainability targets. It also mentioned that the plan projects data center power use to rise 15% per year, with goals to reach internationally advanced efficiency and carbon standards by 2030, thus positively benefiting the country’s market.

India data center power market has gained enhanced traction, structurally driven by the explosive domestic data consumption and widespread 5G rollouts. This hyper-growth is concentrated within major coastal landing hubs and emerging Tier-2 cities, which in turn is creating immense demand for scalable uninterruptible power supply systems, high-capacity transformers, as well as intelligent power distribution units. As stated by Press Information Bureau (PIB) in March 2026, the national data center capacity grew from 375 MW in 2020 to 1,500 MW by 2025, reflecting rapid expansion to support AI workloads. The article also noted that under the AI compute framework, 38,231 GPUs were onboarded across 14 service providers, offered to startups and researchers, and thus elevating the growth potential of the data center power industry.

Europe Market Insights

In Europe, the market is undergoing a profound structural evolution, which is majorly influenced by the intense computational demands of sovereign cloud frameworks. As historical cornerstone hubs face severe geographic constraints, developers are aggressively pivoting toward secondary and northern regional markets where grid infrastructure is more accessible. In June 2026, Eurelectric announced that at the Power Summit in Helsinki is uniting Europe’s power and digital sectors to enable sustainable data center growth. It also stated that AI is expected to drive 28% of Europe’s electricity demand growth by 2030, and the initiative focuses on aligning infrastructure expansion with grid readiness. Furthermore, Europe aims to ensure reliable, affordable power, thereby advancing competitiveness and decarbonization goals.

The surge in high-performance computing is driving a massive wave of procurement for advanced electrical infrastructure, boosting the overall Germany data center power market. Domestic developers are proactively making investments in green power purchase agreements, deploying grid-stabilizing battery energy storage systems, and rapidly adapting facilities to capture and redirect waste server heat into municipal district heating networks. In March 2026, Siemens and Rittal announced a strategic partnership with the main goal of designing future-proof data center infrastructure by focusing on rapidly rising AI-driven power densities. Their first innovation is a next-generation sidecar power rack, which delivers fast, scalable, and standardized power directly in the data center white space, thus suitable for bolstering the country’s market growth.

In the UK the data center power market is growing exponentially through localized self-generation strategies and a stronger integration into the nation’s maritime energy network. At the same time, government recognition of data centers as important digital infrastructure is encouraging sustained investments in capacity expansion and sustainability-led designs. For instance, in October 2024, the UK witnessed a total of USD 7.6 billion investment from four major U.S. tech firms, i.e., CyrusOne, ServiceNow, CloudHQ, and CoreWeave, to expand data center infrastructure. This brought total investment in UK data centers to more than USD 30 billion, underscoring Britain’s role as a hub for AI innovation. Projects include CloudHQ’s campus in Oxfordshire, ServiceNow’s expansion with Nvidia GPUs, CyrusOne’s UK buildout, and CoreWeave’s investment, all boosting the data center power industry in the UK.

Key Data Center Power Market Players:

- Schneider Electric (France)

- Vertiv Holdings Co. (U.S.)

- ABB Ltd. (Switzerland)

- Eaton Corporation plc (Ireland)

- Legrand SA (France)

- Huawei Technologies Co., Ltd. (China)

- Delta Electronics, Inc. (Taiwan)

- Siemens AG (Germany)

- Mitsubishi Electric Corporation (Japan)

- Cummins Inc. (U.S.)

- Generac Power Systems, Inc. (U.S.)

- Hitachi Energy Ltd. (Switzerland)

- Chevron Corporation (U.S.)

- Engine No. 1 (U.S.)

- NextEra Energy, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Schneider Electric has registered itself as the global leader in data center power infrastructure, which is offering UPS systems, power distribution equipment, switchgear, and energy management software. The company provides its services to hyperscale, colocation, and enterprise data centers with integrated end-to-end power solutions.

- Vertiv Holdings Co. specializes in critical digital infrastructure by providing UPS systems, power distribution solutions, energy storage, and modular power systems. Besides, the firm strengthened its position by readily addressing the growing power requirements of AI and hyperscale data centers.

- ABB Ltd. is a foundational player that offers a broad portfolio of electrification solutions, i.e., switchgear, transformers, UPS systems, and digital energy management technologies. The company is highly focused on improving reliability, efficiency, and scalability for large data centers.

- Eaton Corporation plc provides UPS systems, rack PDUs, switchgear, and power quality solutions for data centers worldwide. In addition, the company has deliberately expanded its capabilities to support next-generation AI and cloud facilities.

- Legrand SA is considered to be a key provider of intelligent power distribution and electrical infrastructure solutions for data centers. The firm’s portfolio includes rack PDUs, busway systems, and monitoring technologies that enhance operational efficiency.

Here is a list of key players operating in the global market:

The global data center power market is being led by established players such as Schneider Electric, Vertiv, ABB, Eaton, and Legrand, which collectively are dominating through extensive product portfolios and global service networks. Vendors in this sector are making stronger investments in terms of high-efficiency UPS systems, intelligent power distribution, battery energy storage, and integrated power management platforms. Mergers and acquisitions, partnerships with cloud and AI infrastructure providers, and the development of modular, scalable, and energy-efficient solutions are certain strategies followed by the leading market participants. In March 2026, ABB and VoltaGrid announced the expansion of their partnership to deliver advanced power infrastructure for hyperscale AI data centers by signing the agreement at CERAWeek 2026 in Houston. In this collaboration, ABB will provide 35 synchronous condensers with flywheel technology and prefabricated eHouses, ensuring voltage stability and resilience for next-generation AI workloads.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, Chevron announced its plans to expand into the AI-powered energy sector by developing its first large-scale facility dedicated to supplying electricity to a Microsoft data center. The project is developed in collaboration with Engine No. 1 and will use domestically sourced natural gas to provide reliable, on-site power.

- In May 2026, NextEra Energy announced its agreement to acquire Dominion Energy in a transaction valued at USD 67 billion. The proposed merger is driven by rising electricity demand from AI-powered data centers, and it is expected to strengthen grid infrastructure and expand power generation capacity.

- Report ID: 8636

- Published Date: Jun 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Data Center Power Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.