Contact Adhesives Market Outlook:

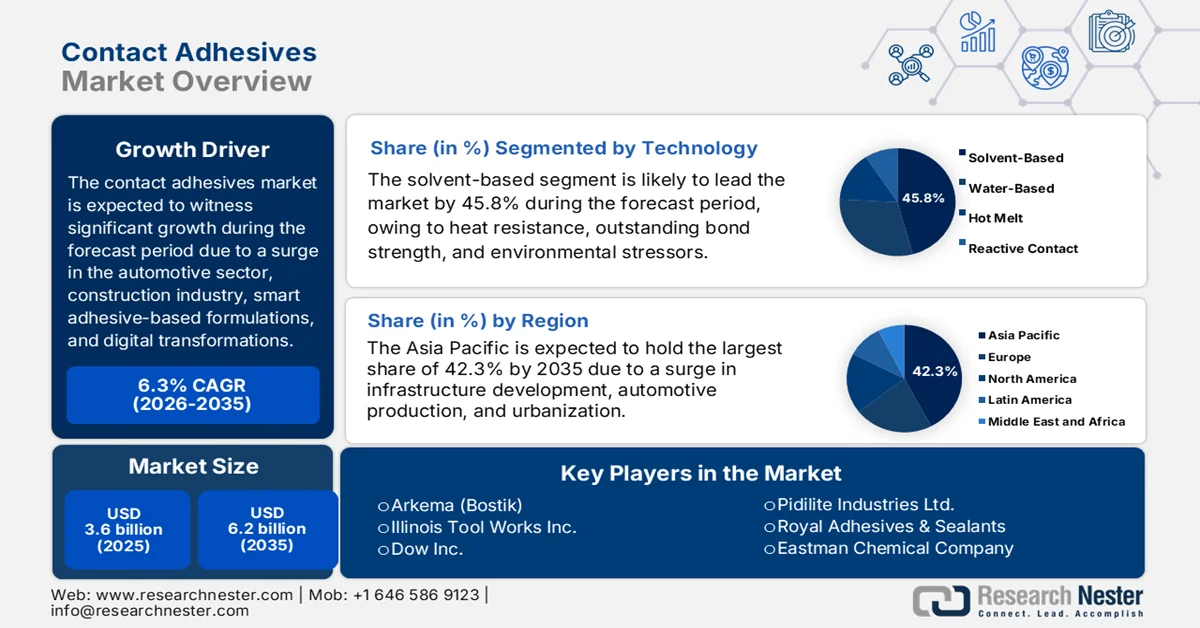

Contact Adhesives Market size was over USD 3.6 billion in 2025 and is expected to reach USD 6.2 billion by the end of 2035, growing at a CAGR of 6.3% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of contact adhesives is assessed at USD 3.8 billion.

The worldwide contact adhesives market is significantly propelled by automotive and construction demand, which is further extended beyond conventional volume-based expansions. According to official statistics published by the IEA Organization in November 2025, the global car sales successfully approached 80 million as of 2024. In addition, there has also been huge growth, which is exclusively driven by sales in hybrid and electric cars, which have made up nearly 30% of overall sales in the same year. Based on this growth, China currently accounts for 40% of international car manufacturing capacity, and meanwhile, North America and Europe each account for 15% of the capacity. Moreover, China effectively overtook Europe to emerge as the world’s largest car exporter as of 2024, and nearly 70% of electric cars have been purchased, thereby making it suitable for boosting the contact adhesives market globally.

2024 Cars Export and Import Growth Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Germany |

169 billion |

69.8 billion |

|

Japan |

116 billion |

- |

|

China |

90.3 billion |

- |

|

U.S. |

- |

216 billion |

|

UK |

- |

54.5 billion |

|

Global Trade Valuation |

973 billion |

|

|

Global Trade Share |

4.26% |

|

|

Product Complexity |

0.79 |

|

Source: OEC

Furthermore, the smart manufacturing and transformation integration, along with the proliferation of functional and smart adhesive formulations, are certain trends that are responsible for bolstering the contact adhesives market globally. As stated in an article published by OECD in January 2026, the adoption of artificial intelligence is widely spreading among consumers who are connected to the labor industry, including 41.1% people in employment, and further accounting for 36.7% unemployed people. Besides, as per the October 2024 World Manufacturing Foundation data report, there has been an increase in the worldwide share across developing countries, deliberately rising from 22% to 44% as of 2023. Moreover, in terms of social transformation, more than 50% of people currently reside in cities and are further expected to reach 70% by the end of 2050, thus proliferating the market growth.

Key Contact Adhesives Market Insights Summary:

Regional Highlights:

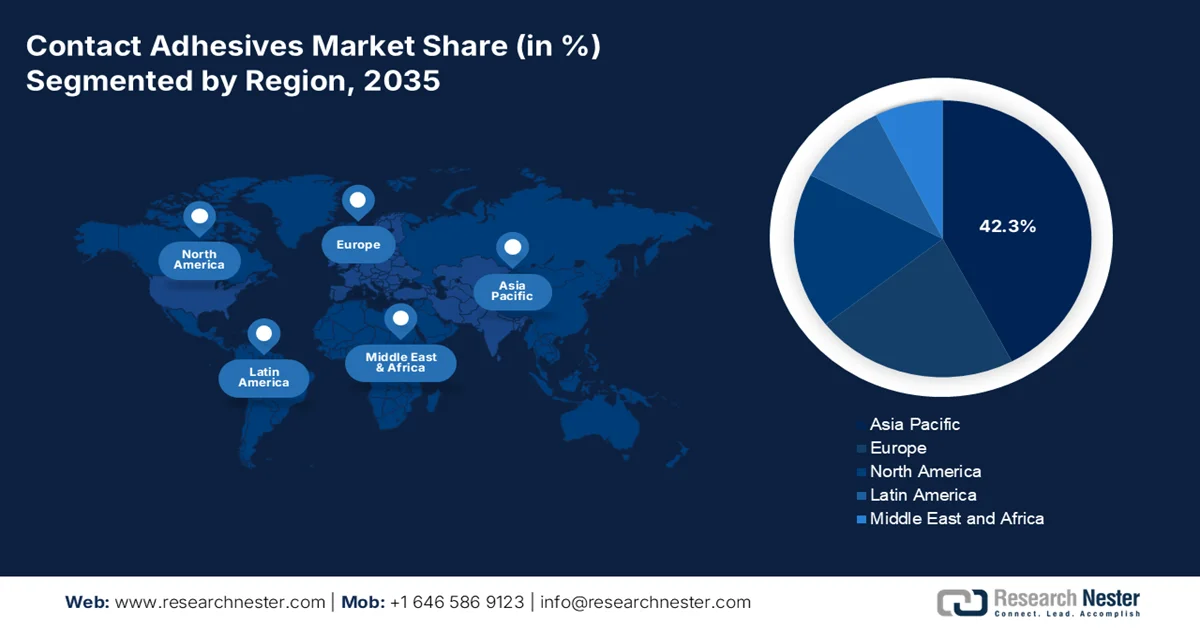

- Asia Pacific is projected to dominate the contact adhesives market with a 42.3% share by 2035, propelled by rapid urbanization, rising automotive production, and expanding infrastructure development across emerging economies.

- North America is anticipated to register the fastest growth in the forecast period of 2026–2035, impelled by increasing DIY activities, expanding automotive and construction sectors, and regulatory momentum toward eco-friendly and low-VOC adhesive formulations.

Segment Insights:

- The solvent-based sub-segment in the contact adhesives market is estimated to secure a 45.8% share by 2035, supported by its superior bond strength, high initial tack, and strong resistance to heat, moisture, and environmental stressors.

- The polyurethane sub-segment is expected to capture the second-largest share during 2026–2035, attributed to its high bond strength, exceptional flexibility, and ability to effectively bond dissimilar materials such as plastic, metal, and wood.

Key Growth Trends:

- Increased revolution in lightweight imperative

- Expansion in prefabricated construction

Major Challenges:

- Raw material price volatility and supply chain disruptions

- Stringent environmental regulations and VOC compliance costs

Key Players: Henkel AG & Co. KGaA (Germany), H.B. Fuller Company (U.S.), 3M Company (U.S.), Sika AG (Switzerland), Arkema (Bostik) (France), Illinois Tool Works Inc. (U.S.), Dow Inc. (U.S.), Huntsman Corporation (U.S.), Jowat SE (Germany), Avery Dennison Corporation (U.S.), Pidilite Industries Ltd. (India), Royal Adhesives & Sealants (U.S.), Eastman Chemical Company (U.S.), LORD Corporation (U.S.), Ashland Global Holdings Inc. (U.S.), Wacker Chemie AG (Germany), Permabond LLC (U.S.)

Global Contact Adhesives Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.6 billion

- 2026 Market Size: USD 3.8 billion

- Projected Market Size: USD 6.2 billion by 2035

- Growth Forecasts: 6.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Vietnam, Indonesia, Mexico

Last updated on : 9 March, 2026

Contact Adhesives Market - Growth Drivers and Challenges

Growth Drivers

- Increased revolution in lightweight imperative: The lightweight imperative is readily driving automotive design and also benefits the contact adhesives market demand. According to official statistics published by the IEA Organization in 2025, 2/3 wheelers are regarded as the most electrified road transport segment as of 2024, with over 9% of the worldwide electric fleet. Besides, the worldwide sales share of electric models remained at nearly 15% in 2024, with overall electric model sales significantly reaching 10 million. Moreover, India, Southeast Asia, and China remain the world’s largest 2/3 wheelers industry, significantly accounting for almost 80% as of international sales as of 2024, thus bolstering the market development.

- Expansion in prefabricated construction: The structural shift of the construction industry towards prefabricated and modular building methods has created sustained demand growth for the contact adhesives market. As stated in an article published by the Modular Organization in 2026, the modular construction industry, particularly in the U.S., has reached USD 20.3 billion as of 2024, further accounting for 5.1% of overall construction activity across different segments. This industrial forecast significantly indicates a 4.5% growth rate, with the industry projected to reach USD 25.4 billion by the end of 2029. This has readily outpaced the wide-ranging construction industry by 1.3%, thereby denoting an optimistic outlook for the market’s upliftment across different countries.

- Surge in the bio-based material adoption: There has been an acceleration of the bio-based adhesive development, with manufacturers generously investing in renewable feedstocks, which is positively driving the contact adhesives market globally. As stated in an article published by NLM in July 2024, the World Health Organization (WHO) effectively established an indoor air quality guideline for both long and short-term exposure to formaldehyde of 0.1 mg/m3, which is 0.08 ppm, for all 30-minute periods at lifelong exposure. Besides, the Canada Environmental Protection Act established increased levels for formaldehyde from composite wood products, ranging from 0.05 to 0.13 ppm depending on the type of product, thereby creating an optimistic outlook for the contact adhesives market expansion.

Challenges

- Raw material price volatility and supply chain disruptions: Raw material price volatility represents the most significant and immediate restraint on the contact adhesives market. This challenge disproportionately affects small and medium manufacturers who lack the leverage to secure long-term supply contracts, while even large multinational corporations face margin compression and delayed capital expenditure decisions amid uncertainty. The market relies heavily on petrochemical derivatives, including polymer-grade propylene, chloroprene, and natural rubber, all of which have experienced dramatic price swings due to supply cuts, weather events, logistics bottlenecks, and geopolitical tensions. Besides, manufacturers struggle to maintain stable pricing for customers, leading to strained buyer relationships and contract renegotiations, thus negatively impacting market expansion.

- Stringent environmental regulations and VOC compliance costs: Stringent volatile organic compound (VOC) and flammability regulations represent the second major roadblock in the contact adhesives market. While these regulations ultimately drive innovation toward sustainable formulations, the immediate compliance burden imposes high costs and operational challenges on manufacturers, particularly those serving multiple jurisdictions with varying requirements. Therefore, manufacturers must invest in new production equipment, retrain staff, update labeling and safety data sheets, and navigate complex certification processes across different jurisdictions. The U.S. Environmental Protection Agency's ban on trichloroethylene and perchloroethylene compounds eliminates entire classes of solvent-based adhesives, forcing companies to abandon established products with decades of performance data.

Contact Adhesives Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.3% |

|

Base Year Market Size (2025) |

USD 3.6 billion |

|

Forecast Year Market Size (2035) |

USD 6.2 billion |

|

Regional Scope |

|

Contact Adhesives Market Segmentation:

Technology Segment Analysis

The solvent-based sub-segment, which is part of the technology segment, is anticipated to garner the largest share of 45.8% in the contact adhesives market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its sustained leadership, which stems from its unparalleled performance characteristics, including high initial tack, superior bond strength, and exceptional resistance to heat, moisture, and environmental stressors. These adhesives utilize organic solvents to dissolve bonding agents, creating formulations that deliver immediate, durable bonds essential for demanding industrial applications across automotive assembly, aerospace manufacturing, heavy equipment fabrication, and high-stress construction environments. The persistence of solvent-based technology despite environmental pressures reflects its irreplaceable role in specialized applications.

Resin Segment Analysis

The polyurethane sub-segment is projected to hold the second-largest share in the contact adhesives market during the forecast period. The sub-segment’s growth is highly driven by its high bond strength, superior flexibility, and the capability to join dissimilar materials, such as plastic, metal, and wood. According to official statistics published by NLM in July 2024, the surface properties of polyurethane demonstrated 30% to 50% of the highest stability emulsion, and particles displayed a core-shell structure with dark and bright intersections. Besides, the tensile strength accounts for 23.2 MPa, with 50% of the fluorine content on the coating film surface, and the contact angle constitutes more than 98.5 degrees. Therefore, based on these characteristics, there is a huge growth opportunity for the sub-segment internationally.

End user Segment Analysis

By the end of the stipulated timeline, the building and construction segment under end user is expected to hold the third-largest share in the contact adhesives market. The segment’s development is highly propelled by its fundamental role in global economic development and its increasing reliance on advanced bonding solutions. Contact adhesives enhance construction processes by providing strong, durable bonds for diverse materials, facilitating quick and efficient installations across residential, commercial, and infrastructure projects. The expansion of this segment is propelled by multiple interconnected factors. Rapid urbanization, population growth, and economic development drive sustained demand for new construction worldwide.

Our in-depth analysis of the contact adhesives market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Resin |

|

|

End user |

|

|

Substrate |

|

|

Application |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Contact Adhesives Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the contact adhesives market is anticipated to garner the highest share of 42.3% by the end of 2035. The contact adhesives market’s upliftment in the region is highly attributed to rapid urbanization, expansion in automotive production, and infrastructure development across developing economies. According to official statistics published by the IEA Organization in 2025, China is regarded as the world’s largest electric car manufacturing center, significantly accounting for over 70% of worldwide production as of 2024. In addition, OEMs in the country also catered to more than 80% of domestic production, denoting an increase by an estimated 2/3rd. Besides, the electric car production by domestic OEMs readily account for less than 2% of their global output, and meanwhile, the continuous motor vehicles supply chain is also bolstering the market in the overall region.

2024 Motor Vehicle Export and Import in the Asia Pacific

|

Countries |

Export (USD) |

Import (USD) |

|

China |

54.2 billion |

18.9 billion |

|

Japan |

26.7 billion |

8.3 billion |

|

South Korea |

19.1 billion |

5.2 billion |

|

Thailand |

8.4 billion |

5.9 billion |

|

India |

7.9 billion |

5.7 billion |

|

Vietnam |

2.4 billion |

2.7 billion |

|

Malaysia |

865 million |

4.2 billion |

|

Indonesia |

2.2 billion |

3.1 billion |

Source: OEC

The contact adhesives market in China is growing significantly, owing to manufacturing dominance, unparalleled industrial scale, strong construction industry, governmental support, and nationwide infrastructure projects. As per an article published by the China’s State Council Information Office in November 2025, there has been an expansion in the country’s value-added industrial output by 4.9% year-on-year (YoY) as of October. Additionally, there has also been a surge in the country’s industrial output by 6.1% for the first 10 months of 2025. Moreover, the industrial output in the nation is readily utilized to measure the activity of large-scale enterprises, each with a yearly main business turnover of almost USD 2.8 million. Therefore, with these developments in the industrial sector, the market is continuing to expand in the overall country.

The existence of government manufacturing strategies, strong commitment towards sector development, focus on increased research and innovation, expanded research infrastructure, and increased industrialization are fueling the contact adhesives market in India. Based on government estimates published by the PIB Government in January 2025, the industrial sector in the country grew by 6.2% by the end of 2025, which is highly driven by strong growth in construction and electricity. Regarding this, the crude steel and finished steel production witnessed a registered growth by 3.3% and 4.6%, driven by continuous development projects and enhanced public infrastructure expenditure. Moreover, the domestic production of electronics goods has substantially increased from USD 22 billion to USD 115 billion, thereby uplifting the market expansion in the country.

North America Market Insights

North America in the contact adhesives market is expected to emerge as the fastest-growing region during the forecast duration. The market’s development in the region is highly propelled by an increase in the demand for DIY, automotive, and construction industries, along with a significant regulatory push for eco-friendly and low-VOC formulations. According to official statistics published by the U.S. Department of the Treasury in June 2023, there has been an increase in the total real non-residential construction expenditure by almost 15% under the Infrastructure Investment and Jobs Act (IIJA). Besides, the real public spending has also increased by 7% and further by 20%. Moreover, the IIJA delivered over USD 50 billion to the EPA, and meanwhile, the public expenditure has also surged by nearly 13%, thus bolstering the market’s exposure in the overall region.

The contact adhesives market in the U.S. is gaining increased traction, owing to strong industrial demand, regulatory advancement, technological evolution, expansion in the construction sector, and huge demand in countertop, paneling, and flooring installation. As per an article published by the U.S. Department of the Treasury in June 2024, nearly 90% of families in the country with yearly incomes below USD 20,000 spend over 30% of their incomes on housing. Besides, 60% of families with incomes ranging between USD 20,000 and USD 50,000 witness the same, placing the overall population on the brink of basic human needs. Furthermore, 90% of the population in the country resides in counties, wherein median rents and house prices increase more rapidly than median incomes. Therefore, based on these, there is a huge growth opportunity for the market in the overall country.

The robust government support for sustainable chemical manufacturing, clean energy investments, ensuring net-zero emissions, incorporating carbon capture technology, and reducing greenhouse gas emissions are certain factors that are developing the contact adhesives market in Canada. As stated in an article published by the Government of Canada in November 2023, Dow and partner organizations invested over USD 8.4 billion in expanding and retrofitting its Fort Saskatchewan facility to become net-zero. This results in significantly diminishing Scope 1 and 2 greenhouse gas emissions from its operations and developing 00 to 500 permanent employment opportunities in the country, along with nearly 8,000 construction-based jobs. Therefore, with such organizational contributions and generous investments, the market is expanding in the country.

Europe Market Insights

Europe in the contact adhesives market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by a robust emphasis on sustainability, an upsurge in industrial activities, advanced manufacturing capabilities, and strict environmental regulations. According to official statistics published by NLM in January 2023, municipal solid waste in the overall region amounts to 477 kg per capita per year, of which 46% are either recycled or composted. Additionally, 4.8 tons of waste have been generated per regional inhabitant, while 39.2% of waste was recycled and 31.3% landfilled. Besides, as per the October 2025 OECD data report, the region has significantly attracted 20% of worldwide clean tech investment, which is positively impacting the market.

The contact adhesives market in the UK is gaining increased exposure, owing to targeted government funding through suitable strategies, sustainable chemical development, reduction in industrial emissions, and the development of the latest infrastructure projects. As per an article published by the UK Government in 2026, the chemical industry in the country is considered a natural innovator, spending over USD 6.2 billion, particularly on research and development. This effectively accounts for more than 20% of the country’s R&D spending, which is positively impacting the market exposure. Besides, the industry has enabled green development by optimizing its own emissions by offering solutions and products, thus ensuring to save nearly 2 tons of greenhouse gas for every 1 ton of chemicals, thereby making it suitable for the market’s growth.

The presence of the automotive industry, the packaging sector, the footwear, and the woodworking manufacturing, along with expansion in the construction sector, and growth in residential segments, is responsible for boosting the contact adhesives market in Germany. Based on the May 2023 Statistisches Bundesamt (Destatis) article, the construction industry in the country accounts for 149,930 building permits, along with 0.996 million persons employed, with localized units of enterprises with more than 20 employees. In addition, the overall turnover of the industry in the country amounts to USD 4.0 billion. Moreover, in 2023, there has been the allowance of constructing 24,500 dwellings in the country. Meanwhile, a total of 68,700 building permits for dwellings have been readily issued, thereby denoting a huge growth opportunity for the market in the country.

Key Contact Adhesives Market Players:

- Henkel AG & Co. KGaA (Germany)

- H.B. Fuller Company (U.S.)

- 3M Company (U.S.)

- Sika AG (Switzerland)

- Arkema (Bostik) (France)

- Illinois Tool Works Inc. (U.S.)

- Dow Inc. (U.S.)

- Huntsman Corporation (U.S.)

- Jowat SE (Germany)

- Avery Dennison Corporation (U.S.)

- Pidilite Industries Ltd. (India)

- Royal Adhesives & Sealants (U.S.)

- Eastman Chemical Company (U.S.)

- LORD Corporation (U.S.)

- Ashland Global Holdings Inc. (U.S.)

- Wacker Chemie AG (Germany)

- Permabond LLC (U.S.)

- Bison International (The Netherlands)

- Permoseal (Australia)

- PLYFIT INDUSTRIES (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Henkel AG & Co. KGaA is aggressively pivoting towards sustainability and portfolio expansion, exemplified by its agreement to acquire ATP Adhesive Systems, a Swiss leader in high-performance water-based specialty adhesives. This strategic move aims to integrate ATP's platform, where its products feature low-VOC water-based technology, to strengthen Henkel's position in high-growth markets, such as automotive and electronics, while aligning with global green manufacturing trends.

- H.B. Fuller Company demonstrated strategic resilience by achieving double-digit earnings per share growth and hitting the higher end of its EBITDA guidance. The company remains on track to exceed EBITDA margin by 2026, driven by improved profitability and strategic execution across its Hygiene, Engineering, and Construction Adhesives segments.

- 3M Company maintains its position as a dominant force in the adhesives market through continuous innovation in high-performance and sustainable bonding solutions. The company is strategically shifting its portfolio towards advanced applications, including increasing investment in bio-based pressure-sensitive adhesive research and development, to capture growing demand for environmentally friendly products in sectors like electronics, automotive, and healthcare.

- Sika AG projects 2026 sales growth of one to four percent in local currencies, underscoring its steady market expansion. The company is transforming from a materials supplier into a comprehensive bonding, sealing, and protection system service provider, offering full lifecycle technical support to meet the rising demand for high-performance, sustainable solutions in modular construction and lightweight automotive design.

- Arkema has solidified its ambition to become a world leader in specialty chemicals through its strategic acquisition of Bostik. Through the Bostik platform, Arkema is aggressively expanding its sustainable offerings, including aggressively promoting solvent-free hot melt adhesives in textiles and filtration applications, positioning itself at the forefront of the industry's green transition.

Here is a list of key players operating in the global contact adhesives market:

The global contact adhesives market is moderately consolidated, with top players such as Henkel in Germany, H.B. Fuller and 3M in the U.S., accounting for the majority of the global market share. The competitive landscape is defined by a strategic pivot towards sustainability, driven by stringent environmental regulations like REACH in Europe and EPA guidelines in the U.S. Key players are aggressively expanding their portfolios of water-borne, solvent-free, and bio-based adhesives to replace traditional solvent-borne products. For instance, in August 2025, G2 Risk Solutions and EverC declared the signing of a deal to combine, displaying an effective innovation in the organization’s collective mission to defend worldwide e-commerce from fast-moving merchant as well as online marketplace events, thereby making it suitable for bolstering the contact adhesives industry.

Corporate Landscape of the Contact Adhesives Market:

Recent Developments

- In July 2026, Hoffmann Green Cement Technologies successfully achieved an increase in its 2025 volumes, including 50,000 tons of 0% clinker cement, which is equivalent to an estimated 145,000 m3 of concrete, along with over 330 construction facilities in France.

- In November 2025, Adani Cement and Coolbrook notified their delivery contract for the world’s first-ever commercial development of the revolutionary RotoDynamic Heater technology to advance cement decarbonisation at the Boyareddypalli Integrated Cement Plant in Andhra Pradesh, India.

- In July 2025, Terra CO2 proclaimed its series B funding by securing USD 124.5 million in the newest equity capital. Additionally, Breakthrough Energy Ventures, Eagle Materials, GenZero, and Just Climate are significantly co-leading this particular funding, with major investment from Barclays Climate Ventures.

- Report ID: 8420

- Published Date: Mar 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.