Construction Adhesives Market Outlook:

Construction Adhesives Market size was valued at USD 12.1 billion in 2025 and is anticipated to grow to USD 18.1 billion by 2035, registering a CAGR of 4.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of construction adhesives is evaluated at USD 12.6 billion.

The escalating demand for high-performance bonding solutions that offer superior structural integrity and faster curing times, coupled with rising investments in infrastructural developments, are certain drivers boosting the construction adhesives market globally. In September 2024, the article published by the Census Bureau revealed that in the U.S., the total construction spending in July 2024 was at a seasonally adjusted annual rate of USD 2,162.7 billion, which is a strong 6.7% increase when compared to July 2023. At the same time, private construction spending stood at USD 1,678.7 billion, which is largely driven by both residential and nonresidential segments. Meanwhile, public construction spending reached almost USD 484 billion, hence driving strong demand for construction adhesives.

U.S. Construction Spending July 2024: Total, Private, Public, Residential & Nonresidential Breakdown

|

Category |

July 2024 (Annual Rate, USD Billion) |

|

Total Construction |

2,162.7 |

|

Private Construction |

1,678.7 |

|

Residential |

941.6 |

|

Nonresidential |

737.2 |

|

Public Construction |

484.0 |

|

Educational Construction |

100.8 |

|

Highway Construction |

140.9 |

Source: Census Bureau

Furthermore, major shifts towards specialized products, which include hybrid polymers, smart adhesives with self-healing capabilities, and high-strength adhesives suitable for diverse materials, are certain factors stimulating consistent growth in the construction adhesives market. According to the article published by the National Institute of Health (NIH) in December 2022, research in adhesive technology is highly focused on sustainability and multifunctionality, along with mechanical strength. And this particular trend reflects a transition from conventional bonding agents to advanced, intelligent, and eco-efficient adhesive solutions. At the same time, this evolution is also driven by heightened demand for longer-lasting infrastructure and reduced maintenance costs in construction projects. As a result, manufacturers are making heavy investments in terms of R&D to develop adhesives that combine structural integrity with environmental responsibility.

Key Construction Adhesives Market Insights Summary:

Regional Highlights:

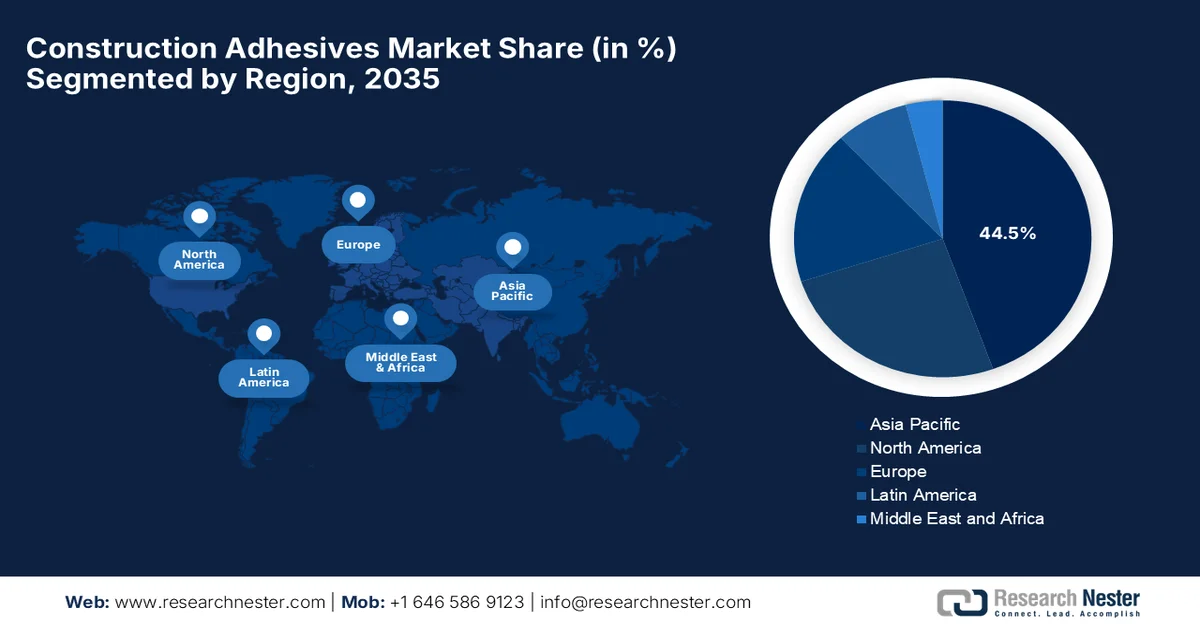

- The Asia Pacific construction adhesives market is projected to hold a 44.5% share by 2035, impelled by rapid urbanization, smart city development, and expanding infrastructure investments

- North America is anticipated to capture a significant share during 2026-2035, attributed to strong renovation activities and rising commercial infrastructure development

Segment Insights:

- The construction adhesives market’s water-based adhesive segment is projected to account for a 41.6% share by 2035, propelled by stringent environmental regulations and rising demand for low-VOC materials

- Acrylic adhesive segment is anticipated to secure a considerable share by 2035, fueled by superior durability, UV resistance, and strong bonding performance across diverse substrates

Key Growth Trends:

- Rise of modular & prefabricated construction

- Sustainability & green building regulations

Major Challenges:

- Volatility in raw material prices

- Stringent environmental and regulatory compliance

Key Players: Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema S.A., Dow Inc., BASF SE, Avantium, Will & Co, Evonik Industries, IMCD, RPM International Inc., Avery Dennison Corporation, Illinois Tool Works Inc., MAPEI S.p.A., Wacker Chemie AG, Soudal Group, Akzo Nobel N.V., DIC Corporation, Aica Kogyo Co. Ltd., Pidilite Industries Ltd., Pidilite Industries Limited, Selleys (DuluxGroup), Tex Year Industries.

Global Construction Adhesives Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 12.1 billion

- 2026 Market Size: USD 12.6 billion

- Projected Market Size: USD 18.1 billion by 2035

- Growth Forecasts: 4.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (44.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries:United States, China, Germany, Japan, India

- Emerging Countries: Brazil, Mexico, Indonesia, Vietnam, Saudi Arabia

Last updated on : 17 April, 2026

Construction Adhesives Market - Growth Drivers and Challenges

Growth Drivers

- Rise of modular & prefabricated construction: There has been strong growth in modular construction since it effectively reduces build time and labor costs. Therefore, the emergence of adhesives helps in factory-built components by enabling fast and durable bonding, which is highly essential for off-site construction systems. In November 2025, the Minns government announced sweeping building reforms with a prime focus to accelerate housing delivery in NSW, including a nation-leading adoption of modular and prefabricated homes. The reforms aim to simplify approvals, cut costs, boost consumer confidence, and modernize regulations, while also introducing tougher conflict‑of‑interest laws for certifiers. These changes are especially designed to speed up housing completions, thus denoting a huge opportunity for the construction adhesives market to grow in the upcoming years.

- Sustainability & green building regulations: Environmental concerns and stricter volatile organic compound regulations are heightening the demand for low-emission, water-based, and bio-based adhesives. At the same time, the green building certifications are also encouraging the utilization of eco-friendly construction materials. In March 2025, the article published by the UN Environment Program reviews global progress in aligning the buildings sector with Paris Agreement climate goals, and it underscores the role of policy frameworks, finance, and technologies in driving sustainable construction practices. At the same time, it notes that the sector remains a major contributor to global emissions, largely due to its dependence on high-impact materials such as cement and steel. The report emphasizes that global initiatives and frameworks are promoting low-carbon strategies, including the adoption of sustainable and eco-friendly construction materials, thus positively impacting the construction adhesives market’s growth.

- Renovation & repair activities: Aging infrastructure in developed countries is increasing demand for renovation, retrofitting, and maintenance. Adhesives are widely used in flooring, panel replacement, insulation upgrades, and interior refurbishment, thus prompting a profitable business environment for the construction adhesives market globally. In May 2024, Doka GmbH announced its involvement in the renovation of Austria’s Voest Bridge, where its Ringlock scaffolding system was used to provide safe working platforms for maintenance and repair of the 65-metre-high pylon. This particular project was highly focused on refurbishing an existing aging structure, reflecting the growing emphasis on infrastructure renovation in developed countries. The company also supplied formwork solutions for temporary bypass bridges to reduce traffic disruption, showcasing the prominence of modern renovation projects that rely on advanced construction systems to enable efficient repair and retrofitting of existing infrastructure.

Challenges

- Volatility in raw material prices: Construction adhesives mostly rely on petrochemical-based raw materials such as resins, solvents, and additives. Therefore, any type of fluctuations in terms of crude oil prices directly impact production costs, which makes pricing strategies extremely difficult for manufacturers. At the same time, the rise in costs can reduce profit margins, thereby forcing companies to add those costs to customers, which in turn affects demand. In addition, the supply chain disruptions which are caused by geopolitical tensions, trade restrictions, or logistical bottlenecks can also exacerbate raw material shortages and price instability. Therefore, the existence of this volatility creates uncertainty in long-term planning and contract pricing, making it very challenging for companies in the construction adhesives market to maintain profitability.

- Stringent environmental and regulatory compliance: Governments across almost all nations are tightening regulations on emissions, especially for volatile organic compounds, which are present in many solvent-based adhesives. At the same time, compliance with environmental standards such as green building certifications and chemical safety regulations requires continuous reformulation of products, which in turn necessitates significant investments. Meanwhile, the non-compliance can result in penalties, product bans, and negatively impact companies’ growth. In addition, the continuously changing regulations across regions complicate global operations, forcing companies to customize formulations for different markets. Therefore, making a shift to eco-friendly alternatives such as water-based or bio-based adhesives can also pose performance challenges, as maintaining the same bonding strength and durability is technically demanding and resource-intensive, thus affecting the growth dynamics of the construction adhesives market.

Construction Adhesives Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.6% |

|

Base Year Market Size (2025) |

USD 12.1 billion |

|

Forecast Year Market Size (2035) |

USD 18.1 billion |

|

Regional Scope |

|

Construction Adhesives Market Segmentation:

Technology Segment Analysis

In the technology segment, water-based adhesive is expected to lead the entire construction adhesives market with the largest share of 41.6% during the forecast period. The segment’s dominance is largely propelled by stringent environmental regulations and increasing demand for low-VOC materials. In addition, the improved performance parity with solvent-based systems supports widespread use of water-based adhesives. In September 2023, Henkel showcased its advanced pressure-sensitive adhesive technologies at Labelexpo Europe. The company also showed its water-based adhesive range (Aquence PS RE), which is especially designed to improve recyclability, enable efficient wash-off from PET bottles, and reduce environmental impact. Hence, such a launch reflects the real industrial adoption of water-based adhesive technologies, mainly driven by sustainability and circular economy goals.

Resin Type Segment Analysis

By the end of the forecast duration, acrylic adhesive, which is a part of the resin type segment, is anticipated to grow with a considerable revenue share in the construction adhesives market. Their superior durability, UV resistance, and bonding strength across diverse substrates are the main factors driving the sub-segment’s leadership in this category. These properties are critical for modern infrastructure exposed to harsh environmental conditions. For instance, in January 2025, Mitsui Chemicals ICT Materia developed a new surface protective tape by using water-based acrylic adhesive for fiber laser cutting of metals. This particular product maintains easy peeling and low noise while reducing VOC and CO2 emissions in production. Therefore, such constant innovations from the key construction adhesives market players will support both performance and sustainability goals of acrylic adhesives.

Application Segment Analysis

In terms of application, the commercial is predicted to grow at a significant rate in the construction adhesives market by the end of 2035. The growth of the segment is largely propelled by the extensive use of construction adhesives across offices, retail complexes, healthcare facilities, educational institutions, and hospitality infrastructure. In these places, high-performance bonding solutions are essential for flooring systems, wall panels, ceiling installations, insulation materials, and decorative finishes. In these applications, adhesives readily enhance installation efficiency and ensure long-term structural integrity and improved surface aesthetics when compared to conventional fastening methods. At the same time, large-scale commercial construction projects consist of a wide variety of substrates such as metal, glass, concrete, and composite materials, thereby increasing the need for versatile and high-strength adhesive systems that are capable of reliable multi-surface bonding.

Our in-depth analysis of the construction adhesives market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Resin Type |

|

|

Application |

|

|

End user |

|

|

Functionality |

|

|

Substrate Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Construction Adhesives Market - Regional Analysis

APAC Market Insights

The Asia Pacific construction adhesives market is expected to be the largest region, capturing a share of 44.5% by the end of 2035. The region’s dominance is largely propelled by massive urbanization, smart city development, and infrastructure expansion. At the same time, rapid residential construction and industrialization significantly increase adhesive consumption. In March 2025, as per an article published by UENSCAP, the aspect of urbanization across the region presents encouraging opportunities, with cities needing to adapt to demographic shifts while ensuring inclusive and sustainable growth. Besides, it emphasizes that the region is home to more than 2.2 billion urban residents, and will see continued urban expansion, requiring strong investment in resilient infrastructure, smart governance, and long-term urban planning. The report also notes that sustainable urban development depends on expanding green infrastructure and strengthening construction and housing systems to support the rising urban populations.

A shift toward sustainable, high-performance building materials is responsibly uplifting the construction adhesives market in China. The country’s market is extensively supported by the rising use of acrylic and polyurethane-based adhesives in roofing, flooring, and structural bonding, often replacing traditional mechanical fasteners. In February 2025, the Adhesives Organization reported that China’s construction market was valued at USD 5.5 trillion in 2025 and is expected to grow at a CAGR of 3.9% through 2028, supported by large-scale infrastructure and construction activities. It also mentioned that Sika has expanded its footprint in the country with the opening of a new plant in Xi’an, producing tile adhesives, waterproofing, as well as flooring solutions to serve the fast‑growing northwestern market. This facility is the second major site opened recently, bringing Sika’s total to 35 plants across China, thus making it suitable for standard construction adhesives market growth.

In India, the construction adhesives market is growing exponentially on account of expanding housing developments and commercial construction activities. At the same time, the country’s market also benefits from infrastructure modernization projects, which continue to rely on efficient adhesive solutions. In February 2025, the article published by the Press Information Bureau reported that India’s infrastructure investment reached USD 120 billion in 2023-24, whereas the capital expenditure rose to almost USD 36 billion, a 5.7-fold increase since the previous decade. The report also mentioned that the National Highway network expanded from 65,569 km a decade back to 1,46,145 km in 2024, whereas airport numbers grew to 157 in the same year. Overall, the data highlights large-scale, multi-sector infrastructure growth driving economic development in the country, thus suitable for bolstering the construction adhesives industry.

North America Market Insights

The North America construction adhesives market is expected to capture a significant revenue share from 2026 to 2035. The regional market growth is largely driven by strong demand from renovation activities and commercial infrastructure development. Contractors in the region are showcasing increased preference for adhesive solutions as they enable precise application. In this context, the reports published by the Construction Association reported that construction plays a major role in the U.S. economy, contributing about USD 1.3 trillion, which is 4.5% to the national GDP of USD 29 trillion in the 2nd quarter of 2024. Meanwhile, the total construction spending reached almost USD 1.1 trillion in nonresidential and USD 878 billion in residential projects in 2023. In addition, there were 943,000 construction establishments in the U.S. in the 1st quarter of 2024, showing the scale and widespread presence of construction activity that supports consistent demand for materials, services, and building solutions.

The robust renovation and remodeling activity across both residential and commercial sectors is responsibly uplifting the construction adhesives market in the U.S. At the same time, the presence of advanced construction technologies, along with strict regulatory and performance requirements, deliberately promotes the use of high-quality adhesive systems that ensure long-term durability with modern building materials. In April 2025, the Congress government article explained that building codes are legally enforceable rules governing the design, construction, and maintenance of buildings that are primarily aimed at protecting public health, safety, and welfare. Besides, it also notes that these codes are adopted and enforced by state, local, tribal, and territorial authorities, whereas the federal government plays a supportive role through standards, funding requirements, and technical guidance, thus driving demand for sustainable building solutions in the overall country.

The rapid adoption of modular construction techniques is effectively fueling the growth of the construction adhesives market in Canada. A significant trend is visible in the country’s market expansion of specialized applications, including mass-timber construction, flooring, and prefabricated assemblies, with key industry players concentrating on R&D for faster curing times and superior adhesion, particularly in cold-weather scenarios. Based on the government data published in September 2025, Build Canada Homes was launched, which is a new federal agency with USD 13 billion in initial funding to accelerate affordable housing construction and fight homelessness. This agency will leverage federal lands, modern construction methods such as modular and factory‑built housing, and a policy to strengthen domestic supply chains. Its first projects include 4,000 factory‑built homes on federal sites, rental protection initiatives, thus driving demand for construction adhesives in the overall country.

Europe Market Insights

The Europe construction adhesives market has acquired a prominent position in the global dynamics, positively influenced by a shift toward sustainable building practices, with waterborne technologies leading the market due to environmental regulations. Major demand stems from the adoption of prefabricated panels, flooring, and structural glazing. Meanwhile, the key industry players such as Sika AG, Henkel AG & Co. KGaA, and Arkema are mainly focused on high-performance bonding solutions to meet strict quality standards. In this context, Henkel Adhesive Technologies entered into a partnership with Sekab in February 2026, with the main goal of promoting the use of bio-based raw materials in adhesive production by focusing on replacing fossil-based ethyl acetate with a sustainable alternative. Also, this particular collaboration aims to integrate renewable, drop-in bio-based inputs into existing adhesive formulations without affecting performance.

The heightened demand for high-performing bonding solutions, supported by active infrastructure development, is responsibly boosting the overall construction adhesives market in Germany. The rising investments in automated application technologies, coupled with the presence of key market players and their strategic activities, have positioned the country for sustained market growth. In September 2024, Henkel showcased sustainable adhesive and coating solutions at InnoTrans 2024, which are suitable for the rail industry, emphasizing performance, safety, and environmental compliance. In addition, the firm also highlighted innovations in elastic and structural bonding that reduce reliance on mechanical methods, thereby meeting strict flame, smoke, and toxicity standards. Therefore, from a strategic perspective, such instances denote a broader industry transition toward advanced adhesive technologies, encouraging more players to establish their footprint in the country.

The UK construction adhesives market has gained immense exposure, which is facilitated by the rising adoption of construction methods such as prefabrication and lightweight building materials, boosting the need for more durable adhesive solutions. In addition, burgeoning investments in sustainable construction practices are readily encouraging the use of low-emission and environmentally compliant adhesive formulations. In September 2023, H.B. Fuller announced the acquisition of the business of Sanglier Limited, which is one of the largest independent manufacturers of sprayable industrial adhesives. This particular deal expands H.B. Fuller’s technology portfolio in construction and engineering adhesives, thereby strengthening innovation, manufacturing, and packaging capabilities across the region. Thus, such instances indicate a consolidation-led shift toward more advanced and application-ready adhesive solutions, which are highly suitable for modern UK construction practices.

Key Construction Adhesives Market Players:

- Henkel AG & Co. KGaA (Germany)

- 3M Company (U.S.)

- Sika AG (Switzerland)

- H.B. Fuller Company (U.S.)

- Arkema S.A. (France)

- Dow Inc. (U.S.)

- BASF SE (Germany)

- Avantium (Netherlands)

- Will & Co (Germany)

- Evonik Industries (Germany)

- IMCD (Netherlands)

- RPM International Inc. (U.S.)

- Avery Dennison Corporation (U.S.)

- Illinois Tool Works Inc. (U.S.)

- MAPEI S.p.A. (Italy)

- Wacker Chemie AG (Germany)

- Soudal Group (Belgium)

- Akzo Nobel N.V. (Netherlands)

- DIC Corporation (Japan)

- Aica Kogyo Co. Ltd. (Japan)

- Pidilite Industries Ltd. (India)

- Pidilite Industries Limited (India)

- Selleys (DuluxGroup) (Australia)

- Tex Year Industries (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Henkel AG & Co. KGaA is leading the sector owing to its strong presence in construction bonding solutions such as sealants, tile adhesives, and structural systems. The company maintains such a position, facilitated by its exclusive brands such as LOCTITE and TEROSON, to serve both residential and infrastructure segments.

- Sika AG is one of the most influential players in construction chemicals, also including adhesives and sealants for concrete, flooring, roofing, and structural bonding. The firm’s growth strategy is highly towards localized manufacturing, continuous product innovation, and acquisitions.

- 3M Company is yet another prominent player in this sector, which is offering solutions for insulation, panel bonding, and structural applications. The company is highly focused on advanced materials science and specialty adhesive technologies.

- H.B. Fuller Company has a strong position in construction, especially in terms of engineering adhesives, flooring solutions, and insulation bonding. The company’s strategy revolves around customer-focused solutions, technical service, and targeted acquisitions with the main goal of expanding its product portfolio.

- Arkema S.A., through its Bostik division, is also a major player in construction adhesives, particularly in tile adhesives, sealants, and waterproofing systems. The company is highly focused on specialty, high-margin adhesive solutions and has built a strong global presence through acquisitions and innovation.

Below is the list of some prominent players operating in the global construction adhesives market:

The global giants such as Henkel AG & Co. KGaA, 3M Company, and Sika AG are considered to be the dominating players in the construction adhesives market. These key pioneers lead the market through strong R&D, global distribution, and diversified portfolios. At the same time, companies are proactively opting for acquisitions, regional manufacturing expansion, and sustainability initiatives such as low-VOC and bio-based adhesives to solidify their market positions. Meanwhile, companies such as Arkema S.A. and H.B. Fuller Company are focused mainly on specialty solutions and customer-friendly innovations. In this context, Avantium and Will & Co in February 2026 entered into a tactical alliance to accelerate the adoption of bio‑based FDCA in coatings, adhesives, sealants, and elastomers by leveraging Avantium’s YXY® technology and Will & Co’s industry expertise.

Corporate Landscape of the Construction Adhesives Market:

Recent Developments

- In April 2026, Henkel completed the acquisition of ATP Adhesive Systems from Arsenal Capital Partners, with the main goal of strengthening its water-based adhesive tapes business. The deal enhances Henkel’s innovation and manufacturing capabilities.

- In March 2026 Evonik expanded its partnership with IMCD to distribute VISIOMER Specialty Methacrylates in the U.S., extending their collaboration from Brazil and Canada. The agreement improves access to methacrylate products for applications such as coatings, adhesives, and construction.

- In February 2026, Sika announced the acquisition of Akkim, which is a leading adhesives and sealants manufacturer, to accelerate its global expansion and strengthen its distribution presence. This particular deal will enhance Sika’s product portfolio and expand production capacity.

- Report ID: 3388

- Published Date: Apr 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.