Compressed Air Treatment Equipment Market Outlook:

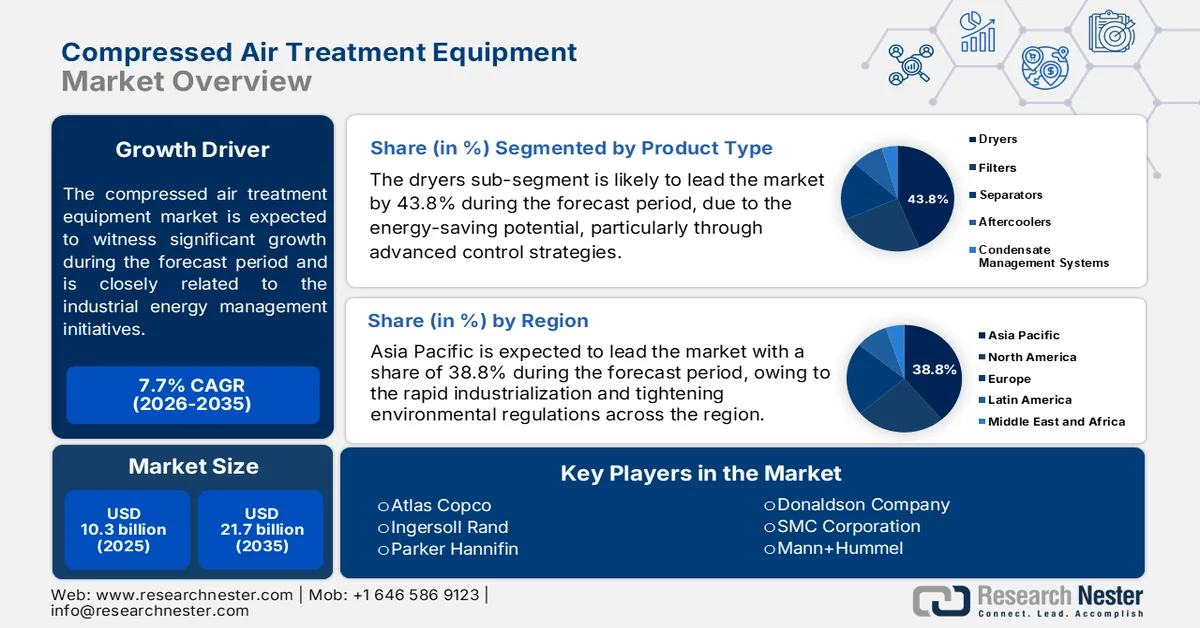

Compressed Air Treatment Equipment Market size was valued at USD 10.3 billion in 2025 and is projected to cross USD 21.7 billion by the end of 2035, rising at a CAGR of 7.7% during the forecast period, 2026-2035. In 2026, the industry size of compressed air treatment equipment is evaluated at USD 11.1 billion.

The compressed air treatment equipment market is closely related to the industrial energy management initiatives, as compressed air systems account for nearly 10% of industrial electricity consumption, according to the BPF November 2023 data. Rising electricity costs and pressure to improve operational efficiency are prompting manufacturers to deploy advanced dryers, filters, pressure regulators, and monitoring systems that reduce the unnecessary energy use across pneumatic operations. The Bureau of Energy Efficiency August 2022 data findings further indicate that a 1 bar (100 kPa) reduction in operating pressure can lower the energy costs by 8%, highlighting the financial impact of the optimized compressed air treatment and pressure management systems in the large industrial facilities. Industries are investing in efficient compressed air infrastructure to minimize energy losses, improve equipment reliability, and support long-term cost reduction strategies aligned with industrial sustainability targets.

The market is also benefiting from capital investments in industrial production and infrastructure modernization globally. According to the UNIDO April 2026 data, the industrial sector represented 37% of global final energy consumption, reinforcing the importance of efficiency-oriented equipment upgrades across factories and processing plants. Regulatory oversight surrounding workplace safety, emissions reduction, and wastewater handling is promoting the end users to adopt advanced condensate treatment and air purification systems to improve environmental compliance. Semiconductor fabrication, battery manufacturing, data centers, and pharmaceutical production facilities are among the major end-use segments expanding compressed air infrastructure investments because these facilities require a stable, dry, and contaminant-controlled air supply for production continuity. Growth opportunities remain strong in Asia-Pacific manufacturing hubs to meet modern operational and environmental performance standards.

Key Compressed Air Treatment Equipment Market Insights Summary:

Regional Highlights:

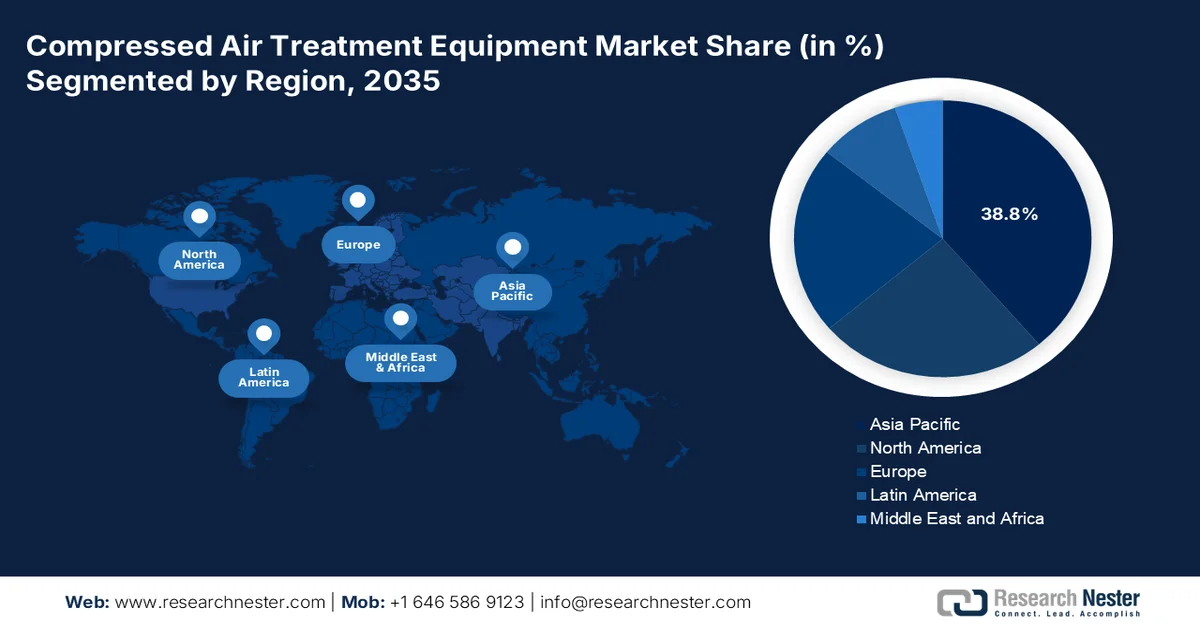

- The Asia Pacific region is anticipated to capture 38.8% revenue share by 2035 in the compressed air treatment equipment market, propelled by rapid industrialization, expanding manufacturing activities, and stricter environmental compliance standards across key industries

- North America is forecast to witness accelerated growth throughout 2026–2035, fueled by stringent energy efficiency mandates, industrial reshoring trends, and rising adoption of predictive maintenance technologies

Segment Insights:

- Dryers are projected to account for 43.8% share by 2035 in the compressed air treatment equipment market, owing to their energy-saving capabilities supported by advanced control strategies and upgraded refrigerated dryer systems

- The food and beverage industry is expected to remain the leading end user through 2035, stimulated by the growing emphasis on energy-efficient operations, moisture control, and enhanced product quality assurance

Key Growth Trends:

- Expansion of semiconductor and electronics manufacturing

- Growth in electric vehicle and battery manufacturing

Major Challenges:

- Complex technical requirements

- Stringent regulatory compliance

Key Players: Atlas Copco (Sweden), Ingersoll Rand (U.S.), Parker Hannifin (U.S.), Donaldson Company (U.S.), SMC Corporation (Japan), Mann+Hummel (Germany), Hitachi Global Air Power (Japan), Kaeser Kompressoren (Germany), Gardner Denver (U.S.), BOGE Kompressoren (Germany), SPX Flow (U.S.), Omega Air (Slovenia), Mikropor (Turkey), Van Air Systems (U.S.), BEKO Technologies (Germany), Zander (U.S.), New Logic Research (U.S.), Puregas (U.S.), Atlas Copco (Sweden), SAF-HOLLAND (Luxembourg).

Global Compressed Air Treatment Equipment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 10.3 billion

- 2026 Market Size: USD 11.1 billion

- Projected Market Size: USD 21.7 billion by 2035

- Growth Forecasts: 7.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, Germany, China, Japan, United Kingdom

- Emerging Countries: South Korea, Vietnam, Brazil, Mexico, Indonesia

Last updated on : 19 May, 2026

Compressed Air Treatment Equipment Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of semiconductor and electronics manufacturing: Government investments in semiconductor manufacturing are creating a substantial demand for high-purity compressed air treatment systems because the chip fabrication facilities require contaminant-free and moisture-free air environments. According to the HAI Stanford University August 2022 data, the U.S. CHIPS and Science Act allocated over USD 52 billion to strengthen domestic semiconductor manufacturing and research capabilities, leading to the construction of advanced fabrication plants requiring precision compressed air infrastructure. Similarly, other countries are increasing semiconductor funding to improve supply chain resilience. Semiconductor facilities depend on advanced filtration and drying systems to maintain cleanroom conditions and protect sensitive manufacturing equipment.

U.S. CHIPS and Science Act, 2022

|

CHIPS and Science Act Component |

Statistical Data |

|

Total CHIPS and Science Act Value |

USD 280 billion authorized spending |

|

Semiconductor Manufacturing Subsidies and Tax Credits |

USD 52 billion allocated for semiconductor manufacturing incentives |

|

Research Funding Allocation |

USD 200 billion allocated for AI, robotics, quantum computing, and scientific research |

Source: HAI Stanford University August 2022

- Growth in electric vehicle and battery manufacturing: Electric vehicle and battery manufacturing expansion is increasing demand for high-performance compressed air treatment systems. This is mainly because the production environments require clean, dry, and stable compressed air for the automation and assembly operations. Government incentive programs are supporting large-scale EV manufacturing investments and battery gigafactory development. According to the IBEF February 2026 data, the EV market in India is projected to rise at a CAGR of 54.94% by 2034. Battery manufacturing facilities require advanced air dryers and filtration systems to maintain product quality and reduce contamination risks in precision production lines. Moreover, multiple EV manufacturing projects supported by public funding are driving industrial utility infrastructure spending globally.

Challenges

- Complex technical requirements: The technical complexity of compressed air treatment systems presents significant entry barriers for new manufacturers who must develop expertise across multiple technologies, including refrigeration, desiccant drying, membrane separation, and filtration. Moreover, the end-users require skilled personnel to operate and maintain this equipment properly, yet a global shortage of qualified technicians limits market adoption. The company's approach recognizes that even superior equipment fails to perform without proper operator knowledge.

- Stringent regulatory compliance: Manufacturers entering the compressed air treatment equipment market must navigate a complex web of varying regulatory standards across different regions. However, achieving certification for each target market requires substantial investment in testing documentation and quality management systems. Non-compliance risks include product recalls, legal liabilities, and reputational damage. New entrants face the daunting task of replicating this compliance infrastructure independently.

Compressed Air Treatment Equipment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.7% |

|

Base Year Market Size (2025) |

USD 10.3 billion |

|

Forecast Year Market Size (2035) |

USD 21.7 billion |

|

Regional Scope |

|

Compressed Air Treatment Equipment Market Segmentation:

Product Type Segment Analysis

Dryers are the leading sub-segment in product type and are poised to hold the share value of 43.8% by 2035 in the compressed air treatment equipment market. The segment is driven by its energy-saving potential, particularly through advanced control strategies. As per the Government of Canada, January 2025 data, most facilities save 10% to 20% of their compressed air energy costs via routine maintenance that directly enhances refrigerated dryer performance. Even higher savings can be gained by upgrading air dryers and filters, which positions refrigerated dryers as the leading product sub-segment. Clogged filters force dryers to work harder, increasing pressure drop and energy consumption. Regular replacement of coalescing and particulate filters ensures that the refrigerated dryers receive clean oil-free air, maintaining dew point stability.

End user Segment Analysis

Under the end user segment, the food and beverage industry is leading in the compressed air treatment equipment market. According to the Energy.gov.au June 2022 data, energy use accounts for at least 15% of total operational costs in a food and beverage manufacturing business, making energy efficiency a strategic priority. Within the compressed air treatment equipment market, refrigerated dryers reduce electrical consumption compared to desiccant alternatives. By removing moisture via mechanical refrigeration rather than heat regeneration, these dryers consume less energy, directly improving profitability, reliability, and yield. Energy-efficient treatment also enhances final product quality by preventing moisture-induced bacterial growth and corrosion in pneumatic conveying lines. Furthermore, reduced energy inputs lower the facility's carbon footprint and the utility bills, freeing capital for production expansion.

Distribution Channel Segment Analysis

Indirect sales via distributors represent the leading distribution channel sub-segment in the compressed air treatment equipment market. Distributors provide localized inventory, technical support, installation services, and after-sales maintenance that original equipment manufacturers cannot efficiently deliver directly. Small and medium-sized industrial end-users prefer purchasing via regional distributors offering bundled solutions, including dryers, filters, condensate drains, and piping components. Manufacturing facilities purchase compressed air treatment components exclusively via authorized distributors rather than directly from OEMs. This preference stems from the distributors' ability to reduce the lead times and provide on-site troubleshooting.

Our in-depth analysis of the compressed air treatment equipment market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Technology |

|

|

Flow Rate |

|

|

End user |

|

|

Distribution Channel |

|

|

Dew Point Range |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Compressed Air Treatment Equipment Market - Regional Analysis

APAC Market Insights

The Asia Pacific compressed air treatment equipment market is dominating and is expected to hold the regional revenue share of 38.8% by 2035. The region is driven by rapid industrialization, expanding manufacturing bases, and tightening environmental regulations across the region. Nations continue to invest heavily in automotive electronics, pharmaceuticals, and food processing sectors, all requiring ISO compliant treated compressed air for quality assurance and export readiness. Government-led initiatives promoting energy efficiency and carbon reduction have accelerated the replacement of older, inefficient dryers and filters with modern variable-speed and dewpoint-controlled systems. The region's concentration of small and medium enterprises favors medium flow rate equipment that balances the capital cost with the operational flexibility.

Rapid industrial automation, manufacturing upgrades, and national energy efficiency policies targeting heavy industries are shaping the compressed air treatment equipment market in China. According to the People’s Republic of China, December 2025 data, the country’s industrial value-added output increased by 5.8%, supported by the growth in the equipment manufacturing and high technology industries that rely heavily on compressed air systems. The January 2026 report by the People’s Republic of China indicated that the equipment manufacturing sector accounted for 36.8% of total industrial output growth, increasing demand for the advanced air filtration and drying technologies in precision manufacturing facilities. Moreover, the EIA May 2024 data stated that China added over 356 GW of power generation capacity in 2024, therefore strengthening industrial electricity availability for manufacturing expansion. These developments are accelerating investments in the efficient compressed air treatment infrastructure across automotive electronics, chemicals, and battery production sectors.

The Japan compressed air treatment equipment market is growing rapidly and set to grow from USD 531.4 million in 2025 to USD 1,041.9 million by 2035 with a CAGR of 6.9%. In 2026, the market is projected to reach USD 571.3 million. The nation is driven by industrial automation, semiconductor investments, and energy efficiency initiatives across manufacturing sectors. According to the JILAF September 2025 data, industrial production increased by 2.8%, driven by machinery and electronic component manufacturing. The Japanese government also approved more than JPY 3.9 trillion in semiconductor and AI-related support programs as per the Universidad de Navarra 2024 report to strengthen domestic high-tech manufacturing capacity. Further, the total electricity consumption is increasing demand for efficient compressed air treatment systems in industrial facilities.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035. The region is driven by energy efficiency regulations, industrial reshoring, and stringent air quality standards across manufacturing sectors. Food and beverage processors, automotive plants, and electronics manufacturers require treated compressed air to prevent moisture-induced corrosion, microbial contamination, and product rejects. The shift toward predictive maintenance and real-time monitoring has gained traction with end users seeking equipment that minimizes unplanned downtime. Canada's carbon pricing mechanism further incentivizes the adoption of energy-efficient refrigerated dryers and condensate management systems. Distributors continue to dominate the sales channel, providing localized technical support, inventory management, and after-sales service that small and medium manufacturers rely upon for system reliability and compliance standards.

Industrial energy efficiency requirements and compressor optimization initiatives across manufacturing facilities are shaping the compressed air treatment equipment market in the U.S. The NREL January 2021 data note that most centrifugal compressors rely on inlet throttling systems that reduce airflow but continue to consume substantial power below approximately 70% of full-load capacity due to blow-off losses and constant-power operation. This operating inefficiency is encouraging industrial facilities to invest in advanced compressed air treatment systems, monitoring technologies, filtration units, and pressure optimization equipment to reduce unnecessary electricity consumption and improve system performance. The U.S. Energy Information Administration's July 2024 data reported that industrial sector electricity retail sales reached nearly 1,055 billion kWh in 2023, reinforcing demand for energy-efficient pneumatic infrastructure to reduce operating costs. Moreover, the Environmental Protection Agency allocated funds for Drinking Water State Revolving Fund programs supporting municipal utility upgrades that utilize compressed air systems for treatment and automation operations.

The industrial energy efficiency initiatives, manufacturing expansion, and government-backed clean technology investments are driving the compressed air treatment equipment market in Canada. As per the Canada Energy Regulator's March 2026 report, Canada’s industrial sector accounted for 52% of national energy demand and 39% of greenhouse gas emissions, making energy optimization a key priority for manufacturing facilities using compressed air systems. Moreover, Canada’s electricity generation mix remains nearly 80% non-emitting, supporting industrial decarbonization efforts and promoting the adoption of energy-efficient compressed air treatment technologies. Manufacturing capital expenditures are reflecting strong industrial infrastructure development requiring pneumatic and air treatment systems. Furthermore, the Government of Canada's May 2026 data indicates the federal government has invested USD 30 million to accelerate clean technology innovation across industrial and agricultural sectors, supporting the modernization of energy-intensive operations.

Europe Market Insights

The stringent energy efficiency directives, rigorous industrial air quality standards, and aggressive decarbonization targets across the member states are driving the compressed air treatment equipment market in Europe. Manufacturing sectors, including the automotive, pharmaceuticals, food and beverage, and chemicals, require certified compressed air to maintain the product quality and export competitiveness. The region's focus on reducing industrial energy consumption has driven the widespread adoption of dewpoint-controlled refrigerated dryers and heat regenerative desiccant systems that minimize electricity use. Replacement of aging treatment equipment continues as facilities respond to the mandatory energy audit requirements and carbon reduction obligations. Countries in the region represent mature markets where end users prioritize total cost of ownership over initial purchase price.

Industrial automation, energy efficiency regulations, and continued investment in advanced manufacturing sectors are shaping the compressed air treatment equipment market in Germany. According to Germany’s Federal Statistical Office (Destatis), the April 2026 report, manufacturing industries made USD 2.29 trillion in sales, reinforcing demand for pneumatic and compressed air infrastructure across automotive machinery and chemical production facilities. The European Commission's March 2025 data indicates that more than USD 4.58 billion is allocated toward industrial decarbonization and energy-efficiency programs supporting the modernization of production systems. Moreover, the industrial consumers are increasing their focus on energy-efficient compressed air treatment technologies that reduce operational power usage and improve production reliability across industrial plants.

EU Innovation Fund Statistics Supporting Germany’s Compressed Air Treatment Equipment Market, 2025

|

Category |

Statistical Data |

|

Signed Decarbonization Projects |

77 projects signed grant agreements under Innovation Fund 2023 |

|

Additional Reserve Projects |

6 additional projects invited for grant preparation |

|

Participating Countries |

Projects span 18 European countries |

|

Total Emissions Reduction Target |

397.6 million tonnes CO₂ equivalent reduction over first 10 years |

|

Additional Reserve Project Emissions Reduction |

24.6 million tonnes CO₂ equivalent potential reduction |

|

Innovation Fund Estimated Revenue |

Approximately €40 billion expected from EU ETS between 2020–2030 |

|

Innovation Fund Portfolio Size |

Around €12 billion supporting more than 200 projects across the EEA |

Source: European Commission March 2025

The manufacturers prioritization of energy efficiency and emissions reduction across industrial operations is driving the compressed air treatment equipment market in the UK. As per the BPF November 2023 report, the compressed air systems account for a smaller percentage of industrial electricity use in the UK, with businesses collectively spending around USD 1.92 billion annually on compressed air operations. Industry estimates further indicate that 20% to 30% of compressed air is lost through system leaks, significantly increasing operational costs and driving demand for advanced dryers, filters, leak detection systems, and condensate management technologies. Rising electricity prices have intensified investment in energy-efficient compressed air infrastructure, particularly across automotive, food processing, pharmaceuticals, and manufacturing facilities. These data show a rising demand in the UK market.

Key Compressed Air Treatment Equipment Market Players:

- Atlas Copco (Sweden)

- Ingersoll Rand (U.S.)

- Parker Hannifin (U.S.)

- Donaldson Company (U.S.)

- SMC Corporation (Japan)

- Mann+Hummel (Germany)

- Hitachi Global Air Power (Japan)

- Kaeser Kompressoren (Germany)

- Gardner Denver (U.S.)

- BOGE Kompressoren (Germany)

- SPX Flow (U.S.)

- Omega Air (Slovenia)

- Mikropor (Turkey)

- Van Air Systems (U.S.)

- BEKO Technologies (Germany)

- Zander (U.S.)

- New Logic Research (U.S.)

- Puregas (U.S.)

- Atlas Copco (Sweden)

- SAF-HOLLAND (Luxembourg)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Atlas Copco is a dominant player in the compressed air treatment equipment market, driving advancements through its smart IoT-integrated drying and filtration systems. The company has enhanced real-time performance monitoring by embedding sensors and cloud-based analytics into its compressed air treatment units. In 2024, the company has showed 8% rise in revenue growth.

- Ingersoll Rand has made significant advancements in the compressed air treatment equipment market by integrating compressed air treatment data into its advanced control and telemetry platforms. The company leverages X-Series controllers to wirelessly capture real-time parameters from dryers, filters, and condensate management systems. In 2025, the company has a revenue of USD 6.1 billion.

- Parker Hannifin is a technology leader in the compressed air treatment equipment market, pioneering the adoption of real-time treatment equipment data into its mobile and wireless monitoring ecosystems. Through its Airtek and domnick hunter product lines, the company has embedded Bluetooth and industrial IoT modules into filters, dryers, and separators.

- Donaldson Company has driven significant advancements in the Compressed Air Treatment Equipment Market by incorporating compressed air treatment data into wireless, real-time filtration management systems. The company utilizes its Digital Controller and Smart Filter technologies to capture differential pressure, humidity, and temperature data from air treatment assets.

- SMC Corporation has made notable advancements in the Compressed Air Treatment Equipment Market by integrating compressed air treatment data into its compact, wireless-enabled monitoring platforms. The company has developed modular air treatment units equipped with embedded sensors and IO-Link communication protocols.

Here is a list of key players operating in the global compressed air treatment equipment market:

The global compressed air treatment equipment market is moderately consolidated, with leading players focusing on energy efficiency and IoT-enabled monitoring to reduce operational costs. Intense competition drives strategic initiatives such as mergers & acquisitions, geographic expansions in Asia-Pacific, and the launch of oil-free, low-pressure-drop dryers and filters. For example, in February 2024, Ingersoll Rand announced the acquisition of Friulair to expand air treatment capabilities. Key players are also integrating digital twin technology for predictive maintenance. Regional manufacturers in India and Malaysia are gaining ground through cost-competitive certified products, challenging incumbents in price-sensitive segments, while Europe and Japan firms lead in high-efficiency premium solutions.

Corporate Landscape of the Compressed Air Treatment Equipment Market:

Recent Developments

- In February 2026, ELGi Compressors expanded its EG Series with higher-capacity, new additions to the EG Permanent Magnet (PM) Series and the EG Super Premium (SP) Series oil-lubricated screw compressor ranges.

- In May 2025, Atlas Copco announced the launch of a portable desiccant air dryer, which is setting a new benchmark in on-site air treatment for industries working in the toughest conditions. The line-up includes 6 models, three twin tower models, and three units with Cerades™ technology.

- In March 2025, SAF-HOLLAND announced the launch of the ApolloSDx™ Super-Duty Air Treatment System, which joins the Haldex family of air treatment systems, and includes the DRYest®, GeminiMDx®, and PURest®. These air treatment systems efficiently remove water vapor, moisture, oil particles, and other contaminants from the compressed air generated by the truck’s compressor before it enters the air brake reservoirs.

- Report ID: 5945

- Published Date: May 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.