Co-Packaged Optics (CPO) Market Outlook:

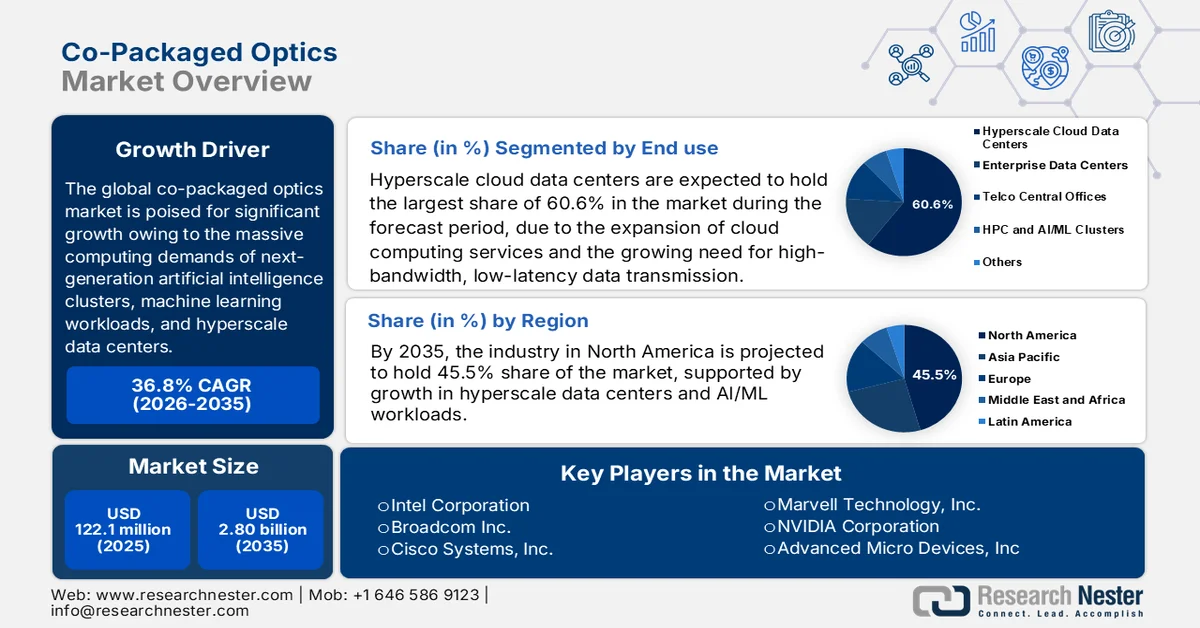

Co-Packaged Optics Market size was valued at USD 122.1 million in 2025 and is projected to reach USD 2.80 billion by the end of 2035, registering around 36.8% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of co-packaged optics is evaluated at USD 167 million.

The co-packaged optics market is projected for extensive growth owing to the massive computing demands of next-generation artificial intelligence clusters, machine learning workloads, and hyperscale data centers. The traditional pluggable transceivers hit physical limitations in power consumption and bandwidth density, due to which CPO is transitioning from a niche technological concept into a critical architectural necessity. As per an article published by Optica Publishing Group in January 2024, a simulation-based study highlights how co-packaged optics can transform data center and AI supercomputer networks by boosting bandwidth and reducing reliance on copper interconnects. In this context, results show that CPO enables 50T switches and beyond, doubling network capacity while cutting switch counts by 64%, leading to simplified architectures with better locality. In addition to AI clusters, throughput improvements crossed 90% in large-node configurations, thereby proving CPO’s critical role in scaling high-performance computing.

Furthermore, early adoption in the co-packaged optics (CPO) market is being led by major cloud service providers and semiconductor giants who are integrating optical engines directly onto the silicon substrate with high-performance network switches and accelerators. Overall, the market reflects strong momentum toward co-design of optics and electronics at the system level, in which the ecosystem collaboration and packaging innovation are becoming increasingly central to enabling AI-based network infrastructure. For instance, in March 2025, Coherent was recognized as one of NVIDIA’s ecosystem innovation collaborators for advancing co-packaged optics in silicon photonics networking switches. This partnership was announced at GTC 2025, and it aims to connect millions of GPUs in next-generation AI factories by overcoming copper interconnect limitations, thus positively benefiting the market’s expansion.

Key Co-Packaged Optics Market Insights Summary:

Regional Highlights:

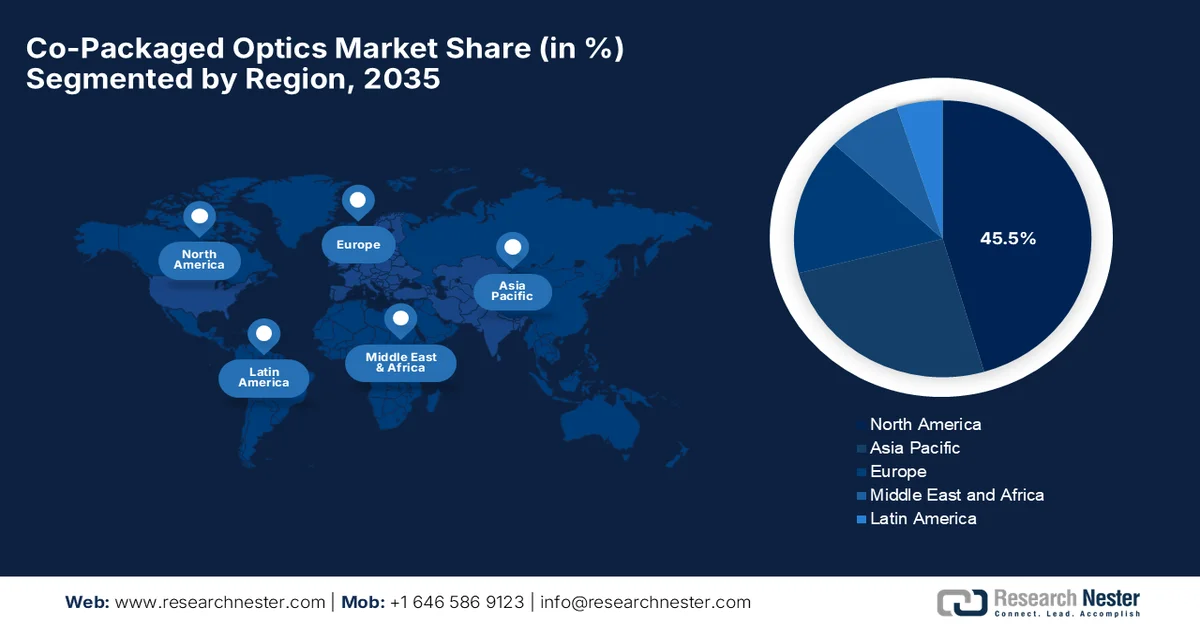

- North America is projected to capture 45.5% of the co-packaged optics market by 2035, reinforced by the massive expansion of hyperscale data centers and surging computational demands of AI and ML workloads

- The co-packaged optics market in the U.S. accounts for almost 29.5%, which is driven by its dominance in hyperscale cloud infrastructure and AI-based data center expansion

- Asia Pacific is set to witness the fastest growth in the market throughout 2026-2035, underpinned by massive expansion of hyperscale data centers, 5G infrastructure, and intensive artificial intelligence deployments across the region

Segment Insights:

- The hyperscale cloud data centers segment is anticipated to account for 60.6% of the co-packaged optics market by 2035, fueled by the expansion of cloud computing services and the growing need for high-bandwidth, low-latency data transmission within large-scale data center infrastructures

- Co-packaged architectures are expected to maintain a considerable share of the market by 2035, stimulated by the increasing need to overcome signal integrity challenges associated with conventional pluggable transceivers

Key Growth Trends:

- AI/ML and high-performance compute demand

- Bandwidth scaling and Ethernet evolution

Major Challenges:

- Integration & thermal challenges

- Standards & adoption barriers

Key Players: Intel Corporation (U.S.), Broadcom Inc. (U.S.), Cisco Systems, Inc. (U.S.), Marvell Technology, Inc. (U.S.), NVIDIA Corporation (U.S.), Advanced Micro Devices, Inc. (U.S.), Coherent Corp. (U.S.), Nokia Corporation (Finland), Huawei Technologies Co., Ltd. (China), Synopsys, Inc. (U.S.) , GlobalFoundries Inc. (U.S.) , Fujitsu Limited (Japan).

Global Co-Packaged Optics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 122.1 million

- 2026 Market Size: USD 167 million

- Projected Market Size: USD 2.80 billion by 2035

- Growth Forecasts: 36.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Italy, Germany, Japan, Iceland

- Emerging Countries: India, Germany, Singapore, Taiwan, United Kingdom

Last updated on : 24 June, 2026

Co-Packaged Optics (CPO) Market - Growth Drivers and Challenges

Growth Drivers

- AI/ML and high-performance compute demand: Co-packaged optics market growth is being strongly catalyzed by the rapid expansion of AI/ML workloads in hyperscale data centers. Massive GPU and accelerator clusters require extremely high-bandwidth, low-latency interconnects to enable faster data movement and improved compute efficiency for AI training systems. In March 2025, NVIDIA reported that its Spectrum-X Photonics networking switches, which were unveiled at GTC 2025, integrate co-packaged optics to scale AI factories to millions of GPUs with unprecedented efficiency. It will deliver 1.6 Tb/s per port, and they achieve 3.5x energy savings, 10x resilience, and superior bandwidth density, thus making it suitable for bolstering the global market’s growth.

- Bandwidth scaling and Ethernet evolution: There has been a rising adoption of 800G and emerging 1.6T Ethernet standards, which are pushing conventional optical modules to their limits. CPO readily addresses bandwidth scaling challenges by reducing electrical trace lengths and signal degradation, which in turn enables higher port density and sustained performance. In May 2023, the article published by IEEESA revealed that Ethernet has evolved over 50 years into the backbone of modern networking by powering everything from homes to hyperscale data centers. It has been supported by the IEEE 802.3 standards, which is why it advanced from 10 Mbps coaxial systems to today’s 400 Gb/s Ethernet, with work underway on 800 Gb/s and 1.6 Tb/s. Further, its adaptability across telecom, enterprise, automotive, and IoT has made Ethernet affordable and fast, thus benefiting the overall co-packaged optics (CPO) market.

Challenges

- Integration & thermal challenges: One of the major obstacles hampering the growth of the co-packaged optics market is the extreme complexity of integrating optical components with high-performance electronic ASICs within a single package. This requires precise co-design of silicon photonics, electrical circuits, and advanced packaging technologies, which increases both engineering difficulty and development time. These CPO systems necessitate tight alignment between optical engines and switch silicon, which leaves little margin for design error. Apart from this, thermal management is also a major issue since placing optics and high-power processors in proximity generates intense heat density. This can degrade signal integrity, reduce component lifespan, and impact system reliability, thereby negatively impacting the market’s growth and exposure.

- Standards & adoption barriers: Another major challenge in the co-packaged optics (CPO) market is the absence of mature industry standards and a fully developed ecosystem. Different vendors across nations utilize proprietary designs for optical engines, packaging approaches, and switch ASIC integration, which in turn is making interoperability very difficult. Hence, the existence of this fragmentation slows down adoption, especially in the case of hyperscale data center operators who require consistent and scalable solutions. In addition, the supply chain is also specialized, which is dependent on semiconductor fabs, silicon photonics manufacturing, and precision packaging facilities, all of which have limited global capacity. Therefore, transitioning from established pluggable optics to CPO also requires a major redesign of data center architectures, thereby leading to high capital expenditure.

Co-Packaged Optics (CPO) Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

36.8% |

|

Base Year Market Size (2025) |

USD 122.1 million |

|

Forecast Year Market Size (2035) |

USD 2.80 billion |

|

Regional Scope |

|

Co-Packaged Optics (CPO) Market Segmentation:

End use Segment Analysis

In the end use category, hyperscale cloud data centers are expected to hold the largest share of 60.6% in the co-packaged optics market during the forecast period. The segment’s dominance is largely propelled by the expansion of cloud computing services and the growing need for high-bandwidth, low-latency data transmission within large-scale data center infrastructures. Co-packaged optics technology enables hyperscale operators to overcome the limitations associated with traditional electrical interconnects by reducing signal losses and supporting higher data transfer rates. In May 2025, Broadcom introduced its third-generation 200G/lane co-packaged optics, which is considered to be a major leap in optical interconnect performance for AI-driven networks. In this context, Broadcom demonstrated improvements in manufacturing, thermal design, and fiber routing, thus contributing to the segment’s expansion.

Integration Approach Segment Analysis

In terms of integration approach, co-packaged architectures are expected to lead with a considerable share in the co-packaged optics market by the end of 2035. The increasing need to overcome signal integrity challenges associated with conventional pluggable transceivers is the main factor boosting the segment’s leadership. Additionally, the architecture supports more compact network equipment designs, facilitates scalability for next-generation switching platforms, and helps optimize thermal management in high-density networking environments. In January 2025, Marvell introduced a co-packaged optics architecture for its custom AI accelerators, thereby enabling scale-up connectivity from tens of XPUs in a rack to hundreds across multiple racks. The company integrates 3D SiPho engines with high-bandwidth memory and chiplets, and delivers 2x bandwidth, 30% lower power per bit, and 100x longer reach compared to copper interconnects.

Component Segment Analysis

By the conclusion of the forecast period, the optical engines segment is anticipated to grow with a considerable revenue share in the co-packaged optics market. The increasing demand for compact, high-performance optical interconnect solutions that are capable of supporting next-generation network speeds is fueling the segment’s growth. Growth is further driven by ongoing advancements in silicon photonics, improved integration of optical and electronic components, and the need for enhanced thermal efficiency within high-density networking equipment. In March 2024, MediaTek introduced an ASIC design platform at OFC 2024 by integrating both high-speed electrical and optical I/Os in a single implementation. It consists of 8x800G electrical links and 8x800G optical links with Ranovus’ Odin® optical engines, and the solution reduces board space, cuts system power by up to 50%, and boosts bandwidth density.

Our in-depth analysis of the co-packaged optics market includes the following segments:

|

Segment |

Subsegments |

|

End use |

|

|

Integration Approach |

|

|

Component |

|

|

Data Rate |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Co-Packaged Optics (CPO) Market - Regional Analysis

North America Market Insights

North America co-packaged optics market is anticipated to dominate with a total share of 45.5% during the forecast period. The region’s leadership is mainly propelled by the massive expansion of hyperscale data centers and the surging computational demands of AI and ML workloads. Therefore, key industry players, major semiconductor manufacturers, along with cloud service providers across the U.S. and Canada, are proactively collaborating to establish standardized ecosystems and deployment frameworks. For instance, in March 2026, Lightmatter announced the launch of a reference architecture initiative within the Open Compute Project in order to establish open specifications for co-packaged optics in next-generation AI systems. It partners with leaders such as Dell, Corning, Foxconn, Qualcomm, and Celestica, with a collective goal to overcome integration and interoperability challenges.

Investments from domestic cloud service giants and federal high-performance computing initiatives to address the physical bottlenecks of networking hardware are driving growth in the U.S. co-packaged optics market. The presence of major silicon design firms and optical component manufacturers within the country has been fostering a local supply chain and accelerating the commercialization of these solutions. In May 2026, the U.S. Department of Commerce generously allocated USD 2 billion to scale quantum foundries under the CHIPS and Science Act, in which IBM will be receiving USD 1 billion for superconducting wafer fabrication, and GlobalFoundries will gain a total of USD 375 million for multi-modality quantum foundry development. Other recipients are Infleqtion, PsiQuantum, Quantinuum, Atom Computing, D-Wave, Rigetti, and Diraq, who will share conditional support tied to milestones. Hence, such instances boost the market’s growth by expanding domestic photonics foundry capacity and powering AI/HPC systems with higher bandwidth and lower energy use.

Canada co-packaged optics market has gained immense exposure as telecommunications firms and technology providers are increasingly turning to CPO architectures. Key growth drivers boosting the country’s market are robust national investments in quantum computing infrastructure, the expansion of high-performance computing clusters across major tech hubs, and a strong ecosystem of local semiconductor research. In May 2026, the government of Canada announced the spin-off of the Canada Photonics Fabrication Centre into a commercial entity to expand domestic photonic semiconductor manufacturing. The CPFC will attract private investment, strengthen Canada’s supply chain, and create high-quality jobs while supporting AI, quantum, defense, and advanced manufacturing sectors, thus making it suitable for standard market growth.

APAC Market Insights

The Asia Pacific co-packaged optics market is anticipated to grow at the fastest rate from 2026 to 2035. The region benefits from massive expansion of hyperscale data centers, 5G infrastructure, and intensive artificial intelligence deployments across the region. Market momentum is also supported by robust governmental initiatives for semiconductor self-sufficiency and substantial manufacturing investments in key electronics hubs. In February 2026, Japan’s Information-technology Promotion Agency generously invested a total of USD 660 million in Rapidus Inc. to support the mass production of next-generation semiconductors, along with USD 1.1 billion from 32 private companies. This coordinated public-private funding strengthens Japan’s domestic manufacturing base for advanced chips critical to AI, autonomous driving, and digital infrastructure, thus elevating the growth potential for co-packaged optics.

As hyperscale data centers and domestic cloud giants face immense power and thermal challenges from pluggable transceivers, CPO has emerged as a critical architecture to deliver high bandwidth density with minimal latency. China co-packaged optics market strongly benefits from substantial state-backed investments in silicon photonics research and a prominent local electronics manufacturing ecosystem. In September 2025, Huawei introduced its F5G-A product series and ten global all-optical network showcases at HUAWEI CONNECT 2025, highlighting the role of fiber-powered networks in driving inclusive AI adoption. It also mentioned that from data centers and smart homes to healthcare, education, and energy systems, F5G-A solutions deliver higher bandwidth, lower latency, and AI-enhanced connectivity, thus benefiting the overall market’s exposure.

In India, the co-packaged optics market has gained enhanced traction, majorly attributable to the country’s explosive digital transformation, accelerated data center localization policies, and the rapid expansion of 5G and artificial intelligence infrastructure. The country’s market also benefits from central government initiatives such as Make in India and semiconductor design incentive schemes, which are consistently stimulating local semiconductor packaging ecosystems and silicon photonics research. In this context, in June 2026, the article published by Press Information Bureau (PIB) revealed that India has rapidly evolved into a global technology power owing to the mission-mode investments in AI, semiconductors, quantum technologies, and supercomputing. Simultaneously, the Digital India Programme has deliberately laid the backbone with expanded fiber networks, affordable internet, and nationwide 5G rollout, connecting over a billion citizens.

Europe Market Insights

Europe co-packaged optics (CPO) market is poised for steady growth in the next decade, owing to the stringent regional energy efficiency regulations, strict sustainability mandates, and the rapid growth of high-performance computing clusters. The region’s market is highly supported by collaborative, multi-national research frameworks that fund silicon photonics innovation and advanced semiconductor packaging techniques. The advanced co-packaged optics project, which was funded under the region’s Digital, Industry, and Space program, is driving innovation in high-efficiency cloud computing by integrating optics directly with processors. The project began in January 2023 and will run until December 2026, with a total budget of USD 6,850,000 and an Europe Comission contribution of USD 5,970,000 coordinated by University College Cork. This particular project supports key EU policy priorities, i.e., the digital agenda, artificial intelligence, climate action, and biodiversity.

The nation's intensive industrial digitization initiatives and strict federal energy efficiency laws for digital infrastructure are responsibly uplifting Germany co-packaged optics market. The country’s data centers and automotive tech sectors have hit thermal and power units; therefore, CPO provides a crucial solution by integrating silicon photonics directly with electronic chips to minimize latency and power consumption. Germany’s market also benefits from the presence of world-class research institutes and microelectronics clusters, which receive substantial backing from national funding frameworks aligned with the European Chips Act. Furthermore, the country's pioneering advancements in automated manufacturing technology and advanced optical packaging are positioning local enterprises as important suppliers in the global high-bandwidth interconnect supply chain.

The UK co-packaged optics market is poised for exceptional growth with a higher focus on advanced academic-commercial spin-offs, bespoke compound semiconductor fabrication, and telecommunications network modernization. The country’s ecosystem leverages its world-leading universities and specialized tech clusters to pioneer the complex material sciences required for silicon photonics integration. In February 2024, the UK launched two new Innovation and Knowledge Centers, which are led by the Optoelectronics Research Centre at Southampton and the University of Bristol, with a mission to transform silicon photonics. This is backed by a total of USD 14 million in funding from EPSRC and Innovate UK, and will accelerate the commercialization of semiconductor technologies, thus making it suitable for standard market growth.

Key Co-Packaged Optics (CPO) Market Players:

- Intel Corporation (U.S.)

- Broadcom Inc. (U.S.)

- Cisco Systems, Inc. (U.S.)

- Marvell Technology, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Coherent Corp. (U.S.)

- Nokia Corporation (Finland)

- Huawei Technologies Co., Ltd. (China)

- Synopsys, Inc. (U.S.)

- GlobalFoundries Inc. (U.S.)

- Fujitsu Limited (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Intel Corporation is a foundational player in the sector, which benefits from its capabilities in CPUs, GPUs, and silicon photonics to integrate optical interconnects directly with high-performance compute and networking chips. The company is highly focused on reducing power consumption and latency in hyperscale data centers and AI workloads.

- Broadcom Inc. is also a dominant force in networking silicon and high-speed switching solutions. Besides, the firm has been playing a central role in enabling CPO architectures for cloud and AI data centers, and it integrates high-bandwidth Ethernet switching ASICs with emerging optical technologies to improve data throughput and energy efficiency.

- Cisco Systems, Inc. is focused on end-to-end networking solutions and is proactively exploring co-packaged optics to enhance its data center switching and routing portfolio. Strategic initiatives opted by the company include ecosystem development and integration of CPO into its networking platforms.

- Marvell Technology, Inc. is also a central player in this field and is a critical semiconductor supplier for data infrastructure, with strong capabilities in custom ASICs, interconnects, and optical DSP technologies relevant to CPO deployment. The firm actively collaborates with cloud hyperscalers to design application-specific silicon that integrates optical and electrical functions.

- NVIDIA Corporation is rapidly emerging as a key driver of demand for co-packaged optics, readily propelled by its dominance in AI accelerators and GPU-based computing systems. The company has been working deliberately to integrate high-speed optical interconnects into its AI data center platforms with the main goal of overcoming bandwidth and power limitations of traditionally utilized copper-based links.

Here is a list of key players operating in the global co-packaged optics (CPO) market:

The co-packaged optics market is extremely competitive, which is dominated by well-established semiconductor leaders such as Intel, Broadcom, NVIDIA, and Marvell. These firms are making heavy investments in silicon photonics and advanced packaging to integrate optics closer to switch ASICs. Apart from this, networking firms such as Cisco and Nokia are forming ecosystem partnerships, whereas optical specialists, including Coherent and Lumentum, are highly focused on component innovation. Asia-based manufacturers such as TSMC and ASE provide critical packaging capabilities. Key strategies followed by the market participants are vertical integration, acquisitions, and co-development with cloud providers to reduce power and latency. For instance, in March 2026, Ayar Labs and Wiwynn entered into a partnership to deliver rack-scale AI systems powered by co-packaged optics, thereby moving beyond component-level innovation to deployable hyperscale infrastructure.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, Synopsys announced the launch of its first Multiphysics Fusion™ solutions by integrating golden signoff Multiphysics analysis directly into timing signoff, design closure, multi-die, and analog workflows. The platform delivers SPICE-accurate timing analysis up to 3 times faster and design closure up to 10 times faster.

- In May 2026, GlobalFoundries introduced its SCALE™ co-packaged optics solution, which is the industry’s first OCI MSA-capable platform built on silicon photonics to boost bandwidth density and scalability for advanced AI data centers. It enables high-speed optical interconnects with DWDM and CWDM, and the solution accelerates the adoption of energy-efficient connectivity.

- Report ID: 8628

- Published Date: Jun 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Co-Packaged Optics Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.