Cloud POS Market Outlook:

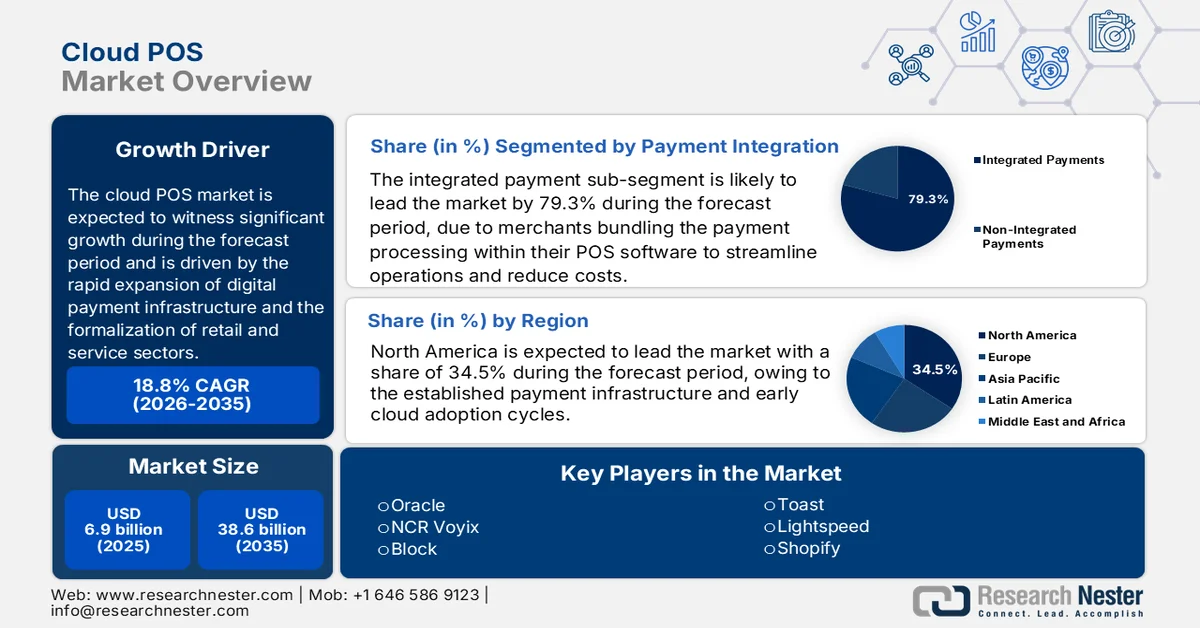

Cloud POS Market size was valued at USD 6.9 billion in 2025 and is projected to reach USD 38.6 billion by the end of 2035, rising at a CAGR of 18.8% during the forecast period 2026 to 2035. In 2026, the industry size of cloud POS is evaluated at USD 8.2 billion.

Cloud-based point of sale adoption is being shaped by the rapid expansion of digital payment infrastructure and the formalization of retail and service sectors. Government-backed payment ecosystems continue to scale transaction volumes, creating a sustained demand for centralized, remotely managed transaction systems. According to the IBEF April 2024 data, India’s Unified Payments Interface processed over 131 billion transactions, reflecting a sharp rise in merchant-side digital acceptance infrastructure. Similarly, the U.S. Federal Reserve Financial Services 2026 data indicates that the card and digital payments collectively accounted for more than 80% of non-cash transactions in recent years, indicating a structural shift away from cash-intensive systems. This transition is reinforced by the regulatory initiatives promoting transparency and tax compliance, mainly among small and medium enterprises.

Besides, the shift toward centralized retail and hospitality management is reinforcing the demand for scalable transaction systems that can integrate inventory, billing, and customer data across multiple outlets. The report from the U.S. Census Bureau, March 2026, depicts that the e-commerce sales accounted for USD 316.1 billion in Q4 of 2025, underscoring the need for unified online and offline transaction management frameworks. Moreover, the labor cost pressures and workforce digitization initiatives are driving the business to adopt systems that reduce manual reconciliation and improve operational accuracy. The labor costs in retail trade have shown a consistent upward pressure, prompting enterprises to invest in automation-enabled transaction systems. This expanding base of digitally enabled merchants is creating sustained demand for interoperable, cloud-based transaction platforms that can support compliance, scalability, and multi-channel operations.

U.S. Retail E-Commerce Sales and Total Retail Sales Overview, 2025

|

Metric Category |

Time Period |

Value |

Growth Rate |

Share of Total Retail Sales |

|

E-commerce Sales (Seasonally Adjusted) |

Q4 2025 |

USD 316.1 billion |

+1.7% QoQ; +5.3% YoY |

16.6% |

|

Total Retail Sales (Seasonally Adjusted) |

Q4 2025 |

USD 1,900.5 billion |

+0.4% QoQ; +2.7% YoY |

— |

|

E-commerce Sales (Not Adjusted) |

Q4 2025 |

USD 365.2 billion |

+21.8% QoQ; +5.6% YoY |

18.3% |

|

Total Retail Sales (Not Adjusted) |

Q4 2025 |

— |

+2.8% YoY |

— |

|

Total E-commerce Sales |

Full Year 2025 |

USD 1,233.7 billion |

+5.4% YoY |

16.4% |

|

Total Retail Sales |

Full Year 2025 |

— |

+3.5% YoY |

— |

|

E-commerce Share of Retail Sales |

Full Year 2024 |

— |

— |

16.1% |

Source: U.S. Census Bureau, March 2026

Key Cloud POS Market Insights Summary:

Regional Highlights:

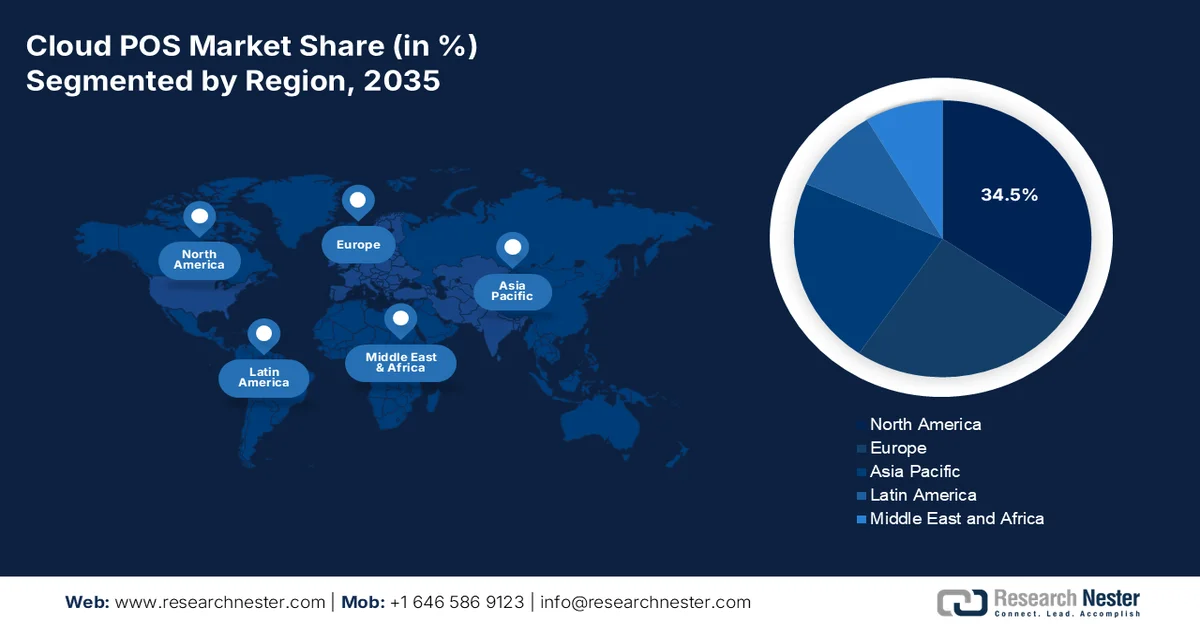

- North America is anticipated to secure a 34.5% share of the cloud POS market by 2035, propelled by established payment infrastructure and early cloud adoption cycles

- Asia Pacific is projected to witness the fastest growth at a CAGR of 14.5% during 2026–2035, fueled by government-backed digital payment infrastructure, large SME base, and mobile-first consumer behavior

Segment Insights:

- Integrated payments under the payment integration segment are expected to command a 79.3% share of the cloud POS market by 2035, driven by merchants increasingly embedding payment processing within POS systems to streamline operations and reduce costs

- Public cloud within the deployment type segment is set to capture the largest share by 2035, owing to its low upfront costs, automatic updates, and scalable infrastructure

Key Growth Trends:

- Expansion in digital payment infrastructure

- Government led SME digitization programs

Major Challenges:

- High initial implementation and infrastructure costs

- Internet connectivity and infrastructure dependency

Key Players: Oracle (U.S.), NCR Voyix (U.S.), Block (Square) (U.S.), Toast (U.S.), Lightspeed (U.S.), Shopify (U.S.), Clover Network (U.S.), Intuit (QuickBooks POS) (U.S.), SAP (Germany), SumUp (UK), B2B Soft (U.S.), Cegid (France), Toshiba Global Commerce Solutions (Japan), Kounta (Australia), N Kids (South Korea), Toreta (Japan), Mosambee (India), Salesforce (U.S.), Zebra Technologies Corporation (U.S.), Aptos (U.S.).

Global Cloud POS Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.9 billion

- 2026 Market Size: USD 8.2 billion

- Projected Market Size: USD 38.6 billion by 2035

- Growth Forecasts: 18.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (34.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, Brazil, Indonesia, Mexico, Vietnam

Last updated on : 30 April, 2026

Cloud POS Market - Growth Drivers and Challenges

Growth Drivers

- Expansion in digital payment infrastructure: Government-backed payment modernization programs are accelerating merchant digitization. The U.S. Federal Reserve's November 2024 report indicated that the noncash payments reached USD 128.51 trillion in 2021, growing at the fastest rate, with card payments rising with 10% per year. This surge requires a scalable transaction system capable of handling high-frequency payments across the distributed retail networks. These developments are pushing enterprises toward centralized transaction environments to ensure real-time processing and reconciliation. Moreover, the vendors should align offerings with national payment rails and interoperability standards, particularly in high-growth economies where governments are actively promoting cashless adoption through regulatory incentives and infrastructure investments.

- Government led SME digitization programs: Public sector initiatives aimed at formalizing small businesses are a key driver for cloud POS market growth. The World Bank July 2022 data reports that in the developing countries, nearly 71% of the people have an account, which is a rise from 42% a decade ago, largely driven by the government-backed financial inclusion programs. Moreover, policies such as India’s GST e-invoicing mandate that digital onboarding schemes, which require SMEs to maintain digital transaction records. This creates a sustained demand for the systems that can support the compliance reporting and tax integration. Cloud-enabled POS platforms align with these requirements by enabling centralized data storage and audit readiness. Vendors targeting SMEs should prioritize the compliance-ready configurations and localized integrations with tax authorities. The demand is mainly strong in the emerging markets where the informal retail sectors are transitioning into the regulated frameworks supported by public funding and policy enforcement.

- Broadband and connectivity investments: National broadband expansion programs are reducing the infrastructure barriers for cloud-based systems. According to the NTU February 2026 data, the U.S. Federal Communications Commission allocated over 65 billion toward broadband deployment under federal infrastructure initiatives targeting underserved regions. Improved connectivity enables real-time transaction synchronization across multi-location enterprises, which is critical for centralized POS operations. In developing regions, similar government-backed connectivity programs are enabling rural and semi-urban retailers to adopt digital transaction systems. This expands the addressable market beyond the urban centers. Strategic alignment with the public infrastructure rollouts can help prioritize geographic expansion. Reliable connectivity also supports the integration with payment gateways, inventory systems, and remote management tools, making it a foundational driver for adoption across retail hospitality and service sectors.

Challenges

- High initial implementation and infrastructure costs: Despite cloud solutions being marketed as cost-effective, the initial implementation costs remain a major roadblock. The high upfront deployment expenses for hardware, software integration, and staff training deter many potential adopters. Tariffs on the imported POS terminals and payment hardware further increase the deployment costs, mainly in North America and European retailers relying on imported equipment. For SMEs, ongoing subscription fees add to the financial burden, slowing the market penetration.

- Internet connectivity and infrastructure dependency: Cloud POS systems require reliable high-speed internet connectivity to function properly, creating a critical vulnerability in regions with unstable networks. In developing markets or rural areas, connectivity issues can hinder smooth operations, causing transaction delays and data synchronization problems. This dependency limits the addressable cloud POS market providers and creates operational risks that traditional on-premises systems don’t face. Businesses in connectivity-challenged regions may delay cloud adoption despite recognizing the benefits.

Cloud POS Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

18.8% |

|

Base Year Market Size (2025) |

USD 6.9 billion |

|

Forecast Year Market Size (2035) |

USD 38.6 billion |

|

Regional Scope |

|

Cloud POS Market Segmentation:

Payment Integration Segment Analysis

Under the payment integration segment, the integrated payments dominate the cloud POS market and are expected to hold the share value of 79.3% by the end of 2035. The segment is driven due to the merchants increasingly bundling the payment processing directly within their POS software to streamline operations and reduce costs. This sub-segment eliminates the third-party gateways, enabling faster checkout, unified reporting, and embedded BNPL options. According to the U.S. Department of the Treasury Report, September 2022 data, in 2021, nearly 28% of the people in the U.S. used credit card payments, and 29% of the people used debit card payments. This high and nearly equal reliance on card-based transactions stimulates the merchant demand for integrated cloud POS solutions that can natively process both credit and debit without separate terminals. The sustained consumer preference for plastic and digital wallets over cash directly fuels the dominance of integrated payments in the cloud POS market.

Share of Payment Use (%), 2016 to 2021

|

Year |

Cash |

Credit |

Debit |

ACH |

Mobile Payment App |

Others |

|

2016 |

31 |

18 |

27 |

10 |

|

13 |

|

2017 |

31 |

22 |

27 |

10 |

|

11 |

|

2018 |

26 |

23 |

28 |

11 |

|

11 |

|

2019 |

26 |

24 |

30 |

11 |

|

9 |

|

2020 |

19 |

27 |

28 |

12 |

3 |

11 |

|

2021 |

20 |

28 |

29 |

11 |

3 |

9 |

Source: U.S. Department of the Treasury Report, September 2022

Deployment Type Segment Analysis

Within the deployment type segment, the public cloud is leading and is expected to capture the largest share value in the cloud POS market by the end of 2035. The segment is driven due to its low upfront costs, automatic security updates, and seamless scalability for seasonal peaks. SMEs and multi-location chains prefer public cloud for centralized management and PCI DSS compliance without dedicated IT staff. As per the CSIS July 2023 data, the U.S. government spent USD 100 billion in 2022 on IT, and USD 12 billion went to cloud-related services. This federal investment validates cloud infrastructure as secure and reliable, supporting the private retail and hospitality sectors to accelerate their own public cloud POS migrations. Moreover, the confidence reinforced by government-scale cloud adoption directly supports public cloud dominance.

Component Segment Analysis

The software sub-segment is dominating the component segment in the cloud POS market, as recurring subscription licenses and value-added analytics features outpace one-time services. The cloud POS software now includes AI-driven inventory forecasting, employee scheduling, and customer loyalty tools, making it indispensable for retailers and restaurants. This software-centric model ensures the merchants benefit from over-the-air updates, new feature rollouts, and real-time performance analytics without the disruptive hardware replacements. As competition intensifies, the cloud POS providers are differentiating via software innovation, including predictive ordering and automated marketing workflows. By 2035, software will remain the primary revenue driver as hardware commoditizes and value shifts entirely to intelligent, cloud native applications.

Our in-depth analysis of the cloud POS market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Organization Size |

|

|

Application |

|

|

Deployment Type |

|

|

End user Industry |

|

|

Payment Integration |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cloud POS Market - Regional Analysis

North America Market Insights

North America is dominating the cloud POS market and is projected to hold the regional revenue share of 34.5% by the end of 2035. The region is driven by the established payment infrastructure and early cloud adoption cycles. The U.S. accounts for the majority of regional revenue. The primary drivers include mandatory PCI DSS compliance updates, which cloud systems automate, and the shift away from legacy on-premises terminals. The U.S. General Services Administration reports that cloud-based point of sale deployments across federal retail operations reduced transaction reconciliation time. Moreover, Canada’s Digital Adoption Programme, with USD 4 billion allocated directly, subsidizes cloud POS implementation for small retailers based on the Knowledge-Based Consulting January 2026 data. The NIST notes that the North America retailers now prioritize cloud POS vendors offering automated security patching. Cross-border retail operations between the U.S. and Canada increasingly require a unified cloud POS platform that handles dual currency transactions and respective sales tax calculations.

The sustained digital transaction growth, expanding retail digitization, and public investment in payment infrastructure are driving the cloud POS market in the U.S. According to the Federal Reserve's November 2024 data, the value of card payments reached USD 9.76 trillion, reflecting a continued reliance on electronic payment systems across commercial environments. The U.S. Census Bureau April 2026 data reported that total retail sales increased by 1.9% from February 2026 and a 4.2% from last year, indicating a large and increasingly digitized transaction base requiring centralized management systems. Additionally, the Federal Deposit Insurance Corporation's November 2024 data noted that nearly 96% of U.S. households were banked in 2023, supporting widespread access to digital payment methods. These factors are positively driving the cloud POS market growth and expansion.

A strong digital payment adoption, retail sector growth, and government-backed connectivity expansion are driving the cloud POS market in Canada. According to the Payments of Canada October 2025 data, nearly 86% of the total transaction volume reflects a widespread reliance on the digital payment infrastructure across businesses. Moreover, the Government of Canada's August 2025 data indicates that USD 3.225 billion is allocated towards the Universal Broadband Fund, which improves the internet infrastructure in rural areas, directly enabling the cloud POS adoption where previously impossible. The broadband investment is expected to connect millions of rural households, unlocking thousands of new retail locations previously reliant on offline or dial-up POS terminals. These factors collectively support sustained demand for scalable and integrated transaction platforms across Canada enterprises.

Canada Digital Payments and Consumer Commerce Trends, 2025

|

Metric Category |

Key Statistic |

|

Share of Digital Payments (Volume) |

86% of total payment volume |

|

Share of Digital Payments (Value) |

77% of total payment value |

|

Contactless Payment Usage |

58% of total transactions |

|

E-commerce Transactions |

USD 77 billion (6% of retail sales) |

|

Smart Device/Social Commerce Usage |

13% of Canada people monthly |

|

Credit Cards in Circulation |

112 million (+5% YoY) |

|

Consumer Interest in AI Shopping Support |

28% find it appealing |

|

Business Adoption of Agentic AI |

64% exploring implementation |

Source: Payments of Canada, October 2025

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the cloud POS market and is expected to expand at a CAGR of 14.5% during the assessed period, 2026 to 2035. The region is driven by the government-backed digital payment infrastructure, massive SME populations, and mobile-first consumer behavior. China leads in absolute transaction volume, with the People’s Bank of China reporting that mobile QR code payment is processed via cloud-connected POS terminals. Japan and South Korea are migrating from advanced but aging proprietary POS systems to open cloud platforms driven by labor shortage automation needs. Emerging trends include integration with digital invoicing mandates and AI-driven inventory forecasting for multi-location chains. Further, e-commerce is expanding the cloud POS into underserved markets.

Large scale digital payment adoption, expanding online commerce, and government-backed financial infrastructure are shaping the cloud POS market in China. According to the MBER May 2023 study, the e-wallets accounted for 83% of e-commerce transactions in 2021, making them the primary payment method across digital commerce channels. Adoption is further strengthened by the expanded credit access, with 84.14% of offline consumers and 78.38% of online consumers without credit cards gaining access to e-wallet-based credit, enabling broader participation in digital transactions. Moreover, 43.54% of offline merchants that previously did not accept credit cards now accept e-wallet credit, improving payment flexibility. Additionally, 90.21% of online transactions that cannot be completed via credit cards are enabled via e-wallet credit reinforcing the transaction completion rates. These trends are driving the demand for POS systems capable of integrating diverse digital payment methods and supporting high-volume multichannel transaction environments.

The rapid growth in formal digital payments, retail scale, and government-backed infrastructure is shaping the cloud POS market in India. According to the PIB July 2025 data, the digital payments index (RBI-DPI) rose to 465.33 in September 2024, indicating a sustained expansion in payment adoption. The World Bank 2026 data noted that over 1.24 billion Aadhaar-based authentications are conducted, supporting secure digital transaction ecosystems. Additionally, the Factly February 2024 data reported that FASTag transactions crossed 3.4 billion in 2022 to 2023, reflecting widespread digital toll and payment integration. These developments are strengthening the need for centralized, interoperable transaction systems across retail transport, linked commerce, and service sectors.

Europe Market Insights

The cloud POS market in Europe is driven by the mandatory real-time VAT reporting mandates, government-subsidized SME digitalization, and cross-border payment harmonization. France led with its anti-fraud law requiring all restaurants and retailers to use certified cloud-connected cash registers, which is affecting millions of businesses. Germany and Italy are implementing similar real-time reporting frameworks, pushing the merchants to upgrade legacy systems. According to the NLM November 2024 study, USD 8.6 billion is allocated to advanced technologies supporting digital skills and cybersecurity in the healthcare sector. This healthcare-specific funding creates a secondary cloud POS demand channel as pharmacies, hospital cafeterias, and medical retail outlets must now comply with both tax reporting and patient data security standards. Moreover, the cloud POS vendors with healthcare compliance certifications are uniquely positioned to capture this parallel cloud POS market segment across various countries in the region.

Steady digital payment adoption, retail sector scale, and public investment in digital infrastructure are supporting the growth of the cloud POS market in Germany. According to the Deutsche Bundesbank, June 2022 data, the card payments accounted for 29% of transactions and 40% of turnover, highlighting increasing reliance on electronic payments in physical and online retail environments. Debit cards represented 23% of transactions and 30% of turnover, while credit cards contributed 10% of turnover, driven by higher value and ecommerce transactions. Online commerce has expanded significantly, with its share of total turnover rising to 24%, reinforcing the need for unified transaction systems across channels. Moreover, the mobile payment adoption is growing, with 17% of smartphone users utilizing devices for in-store payments. These trends are driving the demand for centralized multi-channel transaction management systems across Germany’s retail and service sectors.

The widespread financial inclusion and a structural shift toward digital payments are fueling the cloud POS market in the UK. According to the UK Finance 2026 data, nearly 97% of adults in the UK hold a bank account, with only 2.3 % unbanked, enabling broad access to electronic payment systems across retail environments. Payment behavior has shifted significantly, with cash usage reducing from 51% of all payments in 2013 to 12% in 2023, reflecting a strong transition toward digital and card-based transactions. Moreover, the debit card usage in retail increased from 32% in 2013 to 62% in 2023, reinforcing the reliance on electronic payment infrastructure as per the UK Parliament's April 2025 data. These trends are stimulating the demand for integrated, scalable transaction systems that can support high volumes of digital payments across multi-location retail and service operations.

Key Cloud POS Market Players:

- Oracle (U.S.)

- NCR Voyix (U.S.)

- Block (Square) (U.S.)

- Toast (U.S.)

- Lightspeed (U.S.)

- Shopify (U.S.)

- Clover Network (U.S.)

- Intuit (QuickBooks POS) (U.S.)

- SAP (Germany)

- SumUp (UK)

- B2B Soft (U.S.)

- Cegid (France)

- Toshiba Global Commerce Solutions (Japan)

- Kounta (Australia)

- N Kids (South Korea)

- Toreta (Japan)

- Mosambee (India)

- Salesforce (U.S.)

- Zebra Technologies Corporation (U.S.)

- Aptos (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Oracle leverages its strong enterprise database and ERP backbone in the cloud POS market to offer Oracle MICROS and Oracle Retail Xstore Cloud, which unify point of sale inventory and customer data across hospitality and retail. Oracle’s strategic focus is on embedding AI-driven analytics and seamless omnichannel capabilities into its cloud POS market solutions, enabling large-scale synchronization of online and in-store transactions in real time.

- NCR Voyix is a dedicated digital commerce player in the cloud POS market, offering NCR Counterpoint and Aloha Cloud for retail and hospitality. Its key strategic initiative is the one platform approach, unifying payments, ordering, and back office management on a single cloud native POS system. The company highlights open APIs and partnerships with third-party delivery services, enabling firms to adapt quickly to changing consumer behavior.

- Block dominates the cloud POS market for small and medium businesses via its Square ecosystem, which integrates payments, inventory, employee management, and analytics. Block’s strategic initiative includes embedding financial services directly into its cloud POS market offering, creating a sticky all-in-one platform. The company targets omnichannel retail with Square Online and offline sync, making its solution cost-effective. In 2024, the company made a revenue of USD 24,121,053.

- Toast is a specialized leader in the cloud POS market exclusively for the restaurant industry, offering a purpose-built platform that combines front of house ordering, kitchen display systems, online ordering, and payroll. Toast’s key strategic initiative is its vertically integrated software plus payments model, where its solution eliminates monthly minimums and provides contactless dining tools. In 2024, the company made a revenue of USD 4,960 million.

- Lightspeed operates in the cloud POS market with a focus on retail hospitality and golf businesses, offering a cloud native platform known for its rich catalog management and multi-location sync. Its strategic initiatives involve aggressive expansion via acquisitions to build a B2B e-commerce layer on top of its cloud POS market solution. The company targets growth-oriented SMBs that need advanced inventory and omnichannel tools without enterprise complexity.

Here is a list of key players operating in the global cloud POS market:

The global cloud POS market is highly competitive and is driven by the shift from legacy on-premises systems to omnichannel contactless and data-driven retail solutions. The key players from the U.S. dominate the comprehensive ecosystem, integrating payments inventory and analytics, while the Europe and Asia players excel in regional compliance and specialized verticals such as hospitality. Strategic initiatives include AI-powered demand forecasting, seamless third-party app marketplace integrations, and aggressive M&A to consolidate market share. For instance, in August 2024, Salesforce completed its acquisition of PredictSpring. Moreover, the startups from Australia and India focus on mobile-first, affordable scalability for SMEs, intensifying price and innovation competition.

Corporate Landscape of the Cloud POS Market:

Recent Developments

- In October 2025, Zebra Technologies Corporation, a global leader in digitizing and automating workflows to deliver intelligent operations, announced that it is working with Salesforce to deliver a first-of-its-kind joint solution, Retail Cloud Point of Sale (POS) on Android, at Dreamforce 2025. The solution is designed to improve store operations, empower store associates, and elevate customer engagement for retailers globally.

- In July 2025, SAP launches a new cloud-based point-of-sale solution. The new cloud edition of SAP Customer Checkout provides customers a seamless, efficient, and scalable point-of-sale (POS) solution for the future. From payments, article handling, and coupons to returns, loyalty points, and gift cards, the solution addresses all comprehensive POS needs.

- In May 2024, Aptos, a leader in unified commerce solutions, announced that EE is introducing a new cloud-based POS solution from Aptos in its retail stores. The technology will enhance EE’s customer engagement capabilities and reduce the IT infrastructure footprint in each store.

- Report ID: 8546

- Published Date: Apr 30, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.