Clean Meat Market Outlook:

Clean Meat Market size was valued at USD 27.4 million in 2025 and is projected to reach USD 127.2 million by the end of 2035, rising at a CAGR of 16.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of clean meat is evaluated at USD 31.9 million.

The clean meat market is advancing under the increasing regulatory clarity and public sector research support, mainly in Europe, North America, and parts of Asia. In the U.S., the USDA and FDA have established a joint regulatory framework with the FDA overseeing the cell culture processes and the USDA supervising post-harvest production and labeling. According to the NLM November 2023 study, the FDA announced that it is safe for consuming the cultivated meat for human consumption in November 2022. Moreover, the meat consumption is expected to increase by 70% by 2050. This demand further increases the production of the livestock system. Moreover, compared to plant based the animal-based products have a larger environmental footprint related to greenhouse gas and nitrogen emissions, land and water usage. Cultivated meat is increasingly positioned by public sector agencies as a potential method for decoupling protein production from the environmental burden of traditional agriculture.

Moreover, the global protein consumption continues to rise and is driven by population growth and urbanization, driving the growth of the clean meat market. According to the FAO 2021 data, the global meat production is expected to reach 374 million tons by 2030, placing pressure on conventional livestock systems. Clean meat is being evaluated by the public agencies as a complementary production method to address land use emissions and food security challenges. Further, the government-backed life cycle assessments indicate that the cultivated meat could address the land use compared to traditional livestock, depending on the production methods. Additionally, the public-private partnerships are expected to play a critical role in advancing industrial-scale manufacturing capacity and ensuring regulatory compliance across key markets.

Key Clean Meat Market Insights Summary:

Regional Highlights:

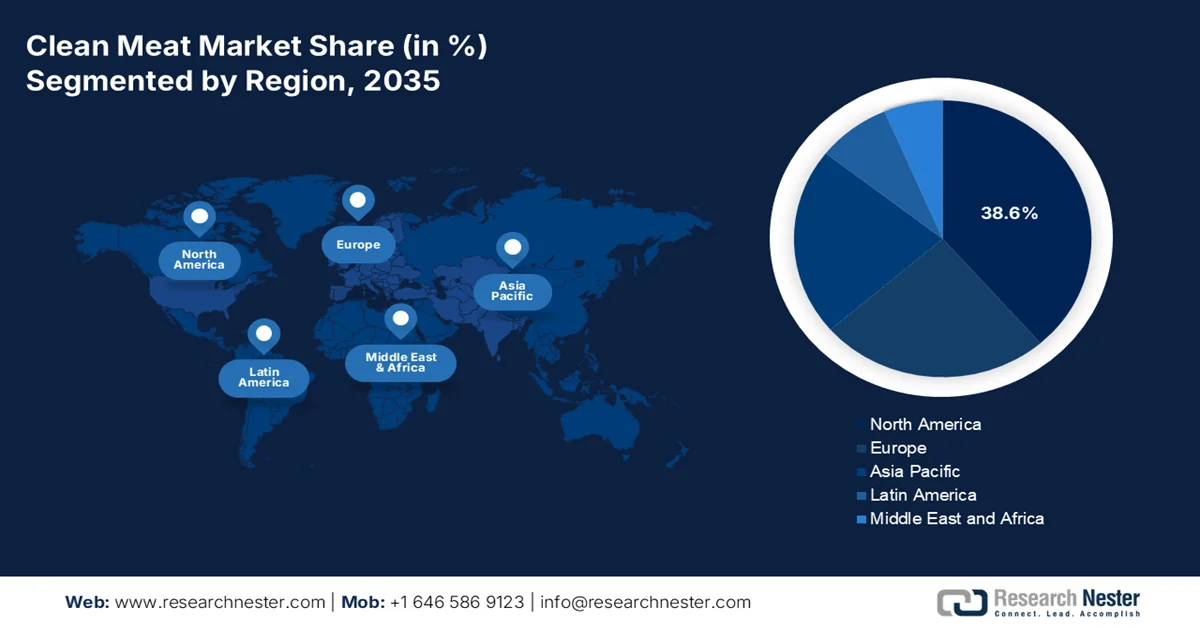

- North America clean meat market is projected to capture 38.6% share by 2035, attributed to the established joint regulatory framework and rising consumer interest in alternative proteins

- Asia Pacific is anticipated to witness the fastest growth during 2026–2035 with a CAGR of 19.8%, fueled by increasing protein demand and strong government investment in cellular agriculture

Segment Insights:

- Commercial/Mass Production sub-segment in the clean meat market is expected to account for 52.4% share by 2035, propelled by large-scale bioreactor expansion enabling cost-efficient production

- Food Service segment is projected to maintain a leading position by 2035, supported by its role as a primary consumer introduction channel offering premium pricing opportunities

Key Growth Trends:

- Public R&D funding for cellular agriculture

- Infrastructure and biomanufacturing investments

Major Challenges:

- Increasing production cost

- Consumer acceptance and education

Key Players: UPSIDE Foods (U.S.), Eat Just, Inc. (GOOD Meat) (U.S.), Mosa Meat (Netherlands), Aleph Farms (Israel), Believer Meats (Israel), Wildtype (U.S.), BlueNalu (U.S.), SuperMeat (Israel), MeaTech 3D / Peace of Meat (Israel), Meatable (Netherlands), IntegriCulture (Japan), Gourmey (France), Finless Foods (U.S.), Vow (Australia).

Global Clean Meat Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 27.4 million

- 2026 Market Size: USD 31.9 million

- Projected Market Size: USD 127.2 million by 2035

- Growth Forecasts: 16.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: U.S.,China, Germany, UK, Japan

- Emerging Countries: Singapore, South Korea, Netherlands, Israel, Canada

Last updated on : 24 March, 2026

Clean Meat Market - Growth Drivers and Challenges

Growth Drivers

- Public R&D funding for cellular agriculture: Government-backed research funding is a primary demand driver in the clean meat market. The USDA and National Science Foundation have funded multiple cellular agriculture and alternative protein projects to improve the bioprocessing efficiency and scalability. According to the GFI April 2022 data, the Dutch government has allocated USD 65.4 million towards cellular agriculture. This public investment reduces reliance on private capital and accelerates pilot-scale manufacturing. Demand is strengthened as companies align with publicly funded innovation ecosystems, ensuring long-term viability and regulatory preparedness. These initiatives are also creating skilled labor pipelines and infrastructure, critical for scaling production capacity and meeting future protein demand.

- Infrastructure and biomanufacturing investments: Government investment in biomanufacturing infrastructure is enabling large-scale production capabilities for the clean meat market. The U.S. Department of Commerce and related agencies have supported bio industrial manufacturing initiative that focuses on scaling bio-based production systems, including food applications. In Europe, the public funding under Horizon Europe supports pilot facilities and bioprocessing infrastructure for alternative proteins. These investments reduce capital expenditure burdens for companies and shorten the commercialization timelines. Infrastructure development also facilitates technology transfer and standardization across regions. As governments prioritize domestic manufacturing resilience, clean meat production is being integrated into broader bioeconomy strategies.

- Rising environmental concerns: Government climate policies are significantly influencing the demand for the low impact protein sources. According to the NLM November 2023 study the livestock accounts for nearly 14.5% of the global greenhouse gas emissions, prompting policymakers to promote sustainable alternatives. The European Commission’s Green Deal and Farm to Fork strategy highlights reducing the environmental impacts of food systems, with the funding directed towards sustainable protein innovation including cultivated meat. The public sector life cycle assessments suggest that cultivated meat could reduce the amount of land used compared to traditional livestock. As governments tighten emissions regulations and introduce sustainability reporting requirements, food producers and retailers are increasingly incorporating clean meat into long-term sourcing strategies. This regulatory pressure is directly shaping procurement decisions and accelerating demand across institutional and commercial buyers.

Challenges

- Increasing production cost: The single greatest barrier to the clean meat market entry is the surging cost of production, mainly cell culture media. The cost for the cultured meat has dropped, but the clean meat remains expensive and confined to small-scale production. Top companies have tackled this challenge by developing an animal-free growth medium that reduces the media costs, aiming to achieve price parity with the conventional beef. Moreover, companies' focus on food-grade ingredients represents a critical pathway toward economic viability.

- Consumer acceptance and education: Limited consumer awareness and willingness to purchase the cultivated meat products presents a substantial market adoption barrier. Only a few consumers globally know about the cell cultured meat, and even after the product introduction average willingness to purchase is less. This gap requires significant marketing investment. Companies have addressed this via high-profile chef and restaurant partnerships introducing cultivated meat in controlled dining environments where chefs can highlight the ethical and sustainability credentials while masking the taste variations.

Clean Meat Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

16.6% |

|

Base Year Market Size (2025) |

USD 27.4 million |

|

Forecast Year Market Size (2035) |

USD 127.2 million |

|

Regional Scope |

|

Clean Meat Market Segmentation:

Production Scale Segment Analysis

The commercial/mass production sub-segment is dominating and is poised to hold a share value of 52.4% by the end of 2035 in the clean meat market. This dominance is driven by the construction of large-scale bioreactor facilities capable of producing millions of pounds of cultivated meat annually, which is essential for achieving the economies of scale needed to lower the production costs to parity with conventional meat. According to the NLM November 2023 study, the U.S. is the second country in the world to allow the in vitro cultivated meat products for commercial sales. Moreover, the companies that successfully scale first will establish undefeatable cost advantages and supply chain relationships, effectively becoming the low-cost producers in a market historically dominated by thin margins. This sub-segment's growth directly correlates with declining production costs and increasing regulatory approvals worldwide.

Distribution Channel Segment Analysis

Within the distribution channel, the food service is dominating in the clean meat market, serving as the primary gateway for consumer introduction to clean meat products. The restaurants and food service operators offer a controlled environment where chefs can prepare cultivated meat alongside familiar ingredients, masking any subtle taste or texture variations while emphasizing the product's ethical and sustainability credentials. This channel eliminates the retail challenges of consumer packaging, labeling education, and direct shelf comparison with conventional meat. According to the NLM June 2024 data, nearly 70% of people have responded that they will try the artificial meat at the restaurants. Moreover, the food service also provides premium pricing opportunities, as restaurant margins accommodate higher ingredient costs while the industry scales toward retail price competitiveness.

Source Segment Analysis

The poultry is projected to dominate the source segment in the clean meat market and is driven by the biological, economic, and cultural factors that position the cultivated chicken as the industry’s flagship product. Chicken cells multiply rapidly in culture compared to mammalian cells, requiring shorter production cycles and lower resource inputs per pound of final product. The familiarity of chicken across global cuisines reduces consumer resistance, while its processed forms, nuggets, patties, and strips align perfectly with current scaffolding and structuring technologies. According to the USDA June 2025 report, the total poultry sales reached 70.2 billion in 2024. Additionally, the lower biological complexity of avian cell culture has enabled poultry producers to achieve faster regulatory approvals globally, establishing first-mover advantages that will be difficult for other source segments to overcome.

Our in-depth analysis of the clean meat market includes the following segments:

|

Segment |

Subsegments |

|

Source |

|

|

End use Product |

|

|

Technology |

|

|

Production Scale |

|

|

Distribution Channel |

|

|

Stage of Development |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Clean Meat Market - Regional Analysis

North America Market Insights

The North America is the dominant player in the clean meat market and is projected to account for 38.6% of regional revenue by the end of 2035. The dominance stems from the combined regulatory and market maturity of the U.S. and Canada. The key drivers include the established joint regulatory framework between the USDA and FDA, which provides commercial certainty for manufacturers. Consumer interest in alternative proteins is supported by the concerns over environmental impact and animal welfare, as documented by government research. The primary trend is the escalating discussion around labeling and fair competition as traditional agricultural subsidies for livestock remain significant. Further, the public research funding is beginning to flow into cellular agriculture, aiming to solve critical production challenges and support the sector’s path to commercial scalability.

The significant federal investments are driving the clean meat market in the U.S. and are aimed at strengthening the broader protein supply chain and processing infrastructure. According to the USDA July 2024 data nearly USD 110 million is funded under the Meat and Poultry Processing Expansion Program and Local Meat Capacity grants, contributing to a cumulative over USD 700 million investment across 48 states and Puerto Rico to expand processing capacity and improve supply chain resilience. While primarily directed at conventional meat systems, these investments enhance shared infrastructure, workforce capabilities, and regulatory frameworks that are also critical for cultivated meat scale-up. For instance, MPPEP alone has supported over USD 291 million across 59 projects. Such government-backed capacity building is improving market access for emerging protein technologies by enabling hybrid production models and facilitating integration into existing distribution networks, including food service and retail. Therefore, these data are fueling the market expansion in the country.

U.S. Government Investments Supporting Protein Processing Infrastructure, 2024

|

Program |

Funding Amount |

Scope |

Key Focus Areas |

|

Total Federal Investment (Biden-Harris Administration) |

USD 700+ million |

48 states & Puerto Rico |

Expansion of independent meat and poultry processing capacity |

|

Meat and Poultry Processing Expansion Program (MPPEP) |

USD 83+ million (latest round) |

24 processors across 15 states |

New processing plants, job creation, capacity expansion |

|

MPPEP (Cumulative – USDA Rural Development) |

USD 291.4+ million (59 awards) |

Nationwide |

Infrastructure expansion, modernization, supply chain strengthening |

|

Local Meat Capacity (Local MCap) – Round 2 |

USD 26.9 million (33 projects, 23 states) |

Regional/local processors |

Equipment upgrades, facility expansion, workforce training |

|

Local MCap – Round 1 |

USD 9.5 million (42 projects) |

U.S. regional |

Small-scale processing support |

|

Local MCap (Total Program Allocation) |

Up to USD 75 million |

Nationwide |

Supply chain resilience, local processing access |

|

Example: North State Processing (NC) |

USD 10 million grant |

North Carolina |

New multi-species processing facility |

|

Example: White Oak Pastures (GA) |

Not disclosed (within Local MCap) |

Georgia |

Facility conversion, +30% capacity increase |

Source: USDA

The strong public investment and global agricultural positioning are driving the clean meat market in Canada. According to the Invest Canada 2026 data, Protein Industries Canada, one of the country’s five Global Innovation Clusters, manages approximately USD 500 million in innovation investments, co-funding projects that accelerate the commercialization of plant-based and alternative protein solutions. Additionally, the government has committed around USD 353 million specifically to support plant protein projects, strengthening R&D capabilities, scaling production technologies, and expanding global clean meat market access. The country’s plant-based food sector, currently valued at approximately USD 1 billion, is benefiting from coordinated public-private partnerships that support product innovation and export expansion. These data show a strong uplift in the market growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is expected to grow at a CAGR of 19.8%. the region is driven by the unprecedented protein demand, food security concerns and concentrated government investment. Moreover, the meat imports are creating an economic vulnerability that cultivated meat production can address, and the localized manufacturing can address. The region’s traditional cuisine, which heavily features processed meat formats such as dumplings, nuggets, and surimi-based products, aligns with the current cultivated meat production capabilities. Governments across the region are actively funding research infrastructure and establishing regulatory pathways. The Singapore Food Agency established the world's first regulatory approval, creating a regional template. These coordinated government initiatives are positioning Asia-Pacific as both a production hub and primary consumption market for cultivated meat products.

The policy-driven biotechnology framework supported by the increasing protein demand and government-backed innovation initiatives is fueling the clean meat market in India. According to the NLM study published in November 2021, the meat consumption contributes to 35% of the total protein intake of the India population, indicating a substantial and growing demand base for the diversified protein sources. Moreover, the PIB August 2024 data depicted that the Government of India approved the BioE3 (Biotechnology for Economy, Environment and Employment) Policy, aimed at boosting the high-performance biomanufacturing with a specific focus on smart proteins, including cultivated meat. The cultivated proteins offer significant resource efficiency, requiring less than 1% of land and around 5% of water compared to conventional red meat, aligning with India’s sustainability and food security priorities, therefore positioning itself as a developing market for clean meat innovation and future scale-up.

The strong government support for cellular agriculture and sustainable protein innovation is shaping the clean meat market in Japan. Japan has expanded funding under its biotechnology and food innovation programs to support cell-based food production and biomanufacturing capabilities. Moreover, Japan imports a significant portion of its food supply, with the country’s food self-sufficiency ratio at 38%, highlighting the need for domestic, scalable protein alternatives based on MAFF 2022 data. Additionally, food manufacturing industry accounts for a substantial share of the industrial output, creating a strong downstream market for protein innovation. These data show Japan as a key Asia-Pacific market for clean meat development and early commercialization.

Europe Market Insights

The clean meat market in Europe is expanding rapidly and is advancing via a complex regulatory and funding environment shaped by the European Commission’s Farm to Fork strategy and the European Green Deal. The livestock product creates a policy pressure for alternative protein development. The food safety authority in Europe is actively developing cultivated meat assessment protocols. This regulatory caution contrasts with significant public investment in foundational research. The European Innovation Council has funded multiple cellular agriculture projects via its EIC Accelerator program. According to the European Commission's Knowledge Centre for Bioeconomy, member states demonstrate varying levels of research activity and industry development, with investment concentrated in countries possessing strong biotechnology infrastructure and agricultural technology expertise.

The public investment in alternative protein innovation and net-zero transition strategies is driving the clean meat market in the UK. According to the Government of the UK, March 2021 data, USD 1.65 billion is allocated under the Net Zero Innovation Portfolio, supporting priority technologies that contribute to decarbonization, including sustainable food production systems. On the other hand, the GFI August 2024 report depicts that the government announced a USD 19.1 million investment in the National Alternative Protein Innovation Centre to accelerate the commercialization of alternative proteins, including cultivated meat, by strengthening R&D collaboration and scaling capabilities. These investments are enhancing the UK’s research infrastructure and also supports academia industry partnerships, facilitating faster translation from lab-scale innovation to pilot production, thus driving the market growth.

The clean meat market in Germany is advancing within the alternative protein ecosystem, supported by federal initiatives and a large-scale food processing industry. As per the Proveg November 2023 data, the government has allocated USD 41.04 million towards the promotion of alternative proteins, which also include cultivated meat, to accelerate the research product development and sustainable food system transformation. This funding aligns with the national priorities to reduce the environmental impact and diversify the protein sources. Moreover, Germany’s food processing sector, which is the fifth-largest industry in the country, generated approximately USD 252.1 billion in 2023 based on the USDA March 2025 data. This substantial industrial base provides a strong downstream market for integrating alternative proteins, including hybrid and cultivated meat products.

Share of Major Segments in Germany Food Processing Industry, 2025

|

Segments |

Percentage |

|

Meat and Meat Products |

21.8 |

|

Milk and Dairy Products |

16.1 |

|

Bakery Products |

9.5 |

|

Confectionary |

7.9 |

|

Readymade Meals |

7 |

|

Alcoholic Beverages |

6.5 |

|

Pet Foods |

6.1 |

Source: USDA

Key Clean Meat Market Players:

- UPSIDE Foods (U.S.)

- Eat Just, Inc. (GOOD Meat) (U.S.)

- Mosa Meat (Netherlands)

- Aleph Farms (Israel)

- Believer Meats (Israel)

- Wildtype (U.S.)

- BlueNalu (U.S.)

- SuperMeat (Israel)

- MeaTech 3D / Peace of Meat (Israel)

- Meatable (Netherlands)

- IntegriCulture (Japan)

- Gourmey (France)

- Finless Foods (U.S.)

- Vow (Australia)

- Stämm (Argentina)

- CellX (China)

- TissenBioFarm (South Korea)

- ClearMeat (India)

- Shiok Meats (Singapore)

- Umami Meats (Singapore)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- UPSIDE Foods is a leading player in the clean meat market, distinguished by its comprehensive approach to production and go-to-market strategy. As the first company to receive a USFDA No Questions letter for its cultivated chicken, it has set a regulatory benchmark. The company’s strategic initiatives focus on building large-scale production capacity in California.

- Eat Just Inc., operating under its GOOD Meat brand, holds a pioneering position in the global clean meat market as the first company to secure the regulatory approval for the sale of cultivated meat in Singapore. This first mover advantage has been pivotal, allowing it to gather real-world consumer data. The company’s strategy centers on expansion and diversification.

- Mosa Meat is a foundational player in the clean meat market. The company’s strategic focus is deeply rooted in cost reduction and sustainability to achieve price parity with conventional beef. Its key initiative involves developing and scaling up the use of food-grade animal-free growth media.

- Aleph Farms is a technological innovator in the clean meat market, uniquely positioned by its focus on producing the whole muscle cultivated steaks rather than just ground meat. Its strategic initaitve the Biofarm platform, leverages a proprietary 3D printing-like technology to create complex tissue structure including the thin slices of steak preferred in dishes.

- Believer Meats is a formidable competitor in the clean meat market, known for its radical approach to lowering the production costs via its proprietary media regeneration technology. This innovation allows for the continuous removal of waste and replenishment of nutrients to higher cell densities and lower costs per pound.

Here is a list of key players operating in the global clean meat market:

The global clean meat market is defined by intense innovation and a race to achieve commercial scale and regulatory approval. The competitive landscape is a mix of well-funded startups and established food players. The key strategic initiatives include heavy investment in research and development to reduce production costs, forming partnerships with traditional meat processors to use existing distribution networks, and active regulatory engagement to secure market authorization. For example, in November 2024, Betagro became the first meat company in Asia to invest in Meatable. Companies are also focusing on product diversification, moving beyond ground meats to develop structured products such as steaks and filets.

Corporate Landscape of the Clean Meat Market:

Recent Developments

- In October 2025, Gourmey has acquired Vital Meat to form PARIMA, a global leader in protein innovation. Bringing together two of Europe’s foremost innovators, PARIMA combines complementary strengths in scalable cell cultivation and validated production economics.

- In August 2025, Meatable acquired Uncommon Bio’s cultivated meat platform as the latter pivoted to therapeutics, including key technology, several IP assets, select cell lines, and key staff, for an undisclosed sum.

- In February 2025, Stämm announced the collaboration with SuperMeat to accelerate cultivated meat biomanufacturing, with support from mutual investor Varana Capital. The companies partnered to further enhance SuperMeat’s cultivated chicken meat process with Stämm’s novel bioreactor.

- Report ID: 8465

- Published Date: Mar 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.