Cultured Meat Market Outlook:

Cultured Meat Market size was valued at USD 292.6 million in 2025 and is projected to reach USD 416.7 million by the end of 2035, rising at a CAGR of 33.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of cultured meat is estimated at USD 303.1 million.

The cultured meat market is growing steadily and represents a transformative segment within a broader alternative protein industry, which is focused on producing animal protein via cellular agriculture. The cultivated meat and seafood companies have raised USD 225.9 million globally in 2023, as per the GFI data 2023. Further 83% of all cultivated meat investment occurred in just the last three years, reflecting accelerating investor confidence despite a year-over-year decline in total capital raised. In 2024, public sector investment continued to expand in the governments of the EU, Singapore, and the U.S., increasing the funding for cellular agriculture research and regulatory readiness, boosting the commercialization pathway for cultured meat. Further, regulatory pathways are also a vital area for the development, as the U.S. markets are establishing a precedent for future market entrants and providing a clearer framework for investment and commercial planning.

Investment Capital in Cultivated Meat

|

Category |

2023 |

2022 |

All-time (since 2013) |

2023 Highlights |

|

Total |

USD 226 million |

USD 922 million |

USD 3.1 billion |

83% of cultivated meat investment occurred in the last three years. |

|

Invested capital deal count |

53 |

72 |

416 |

2023’s largest investment was USD 35 million (Meatable). |

|

Unique investors |

111 |

204 |

590 |

Number of all-time unique investors grew by 13%. |

|

Growth stage deals (Series B and above) |

2 |

2 |

13 |

Included Meatable and BlueNalu. |

Source: GFI 2023

The market growth is fueled by the long-term macro trends that are concerning global protein demand and environmental sustainability. The report from the GFI 2025 states that compared to traditional beef production, cultivated meat can reduce greenhouse gas emissions by 92% and land use by 90%. This addresses the challenges in the resource and supply chains. Government bodies in several regions are identifying this strategic potential and are investing heavily to lead the market. For example, the national policies, such as those in Singapore, explicitly support the local production of alternative proteins to boost the food system resilience, creating a conducive environment for industry development. The near-to mid-term commercial strategy for producers is predominantly B2B, aiming for partnerships with the top food manufacturers and food service distributors to incorporate the cultivated products as ingredients, thereby utilizing the distribution networks and ensuring market penetration.

Key Cultured Meat Market Insights Summary:

Regional Highlights:

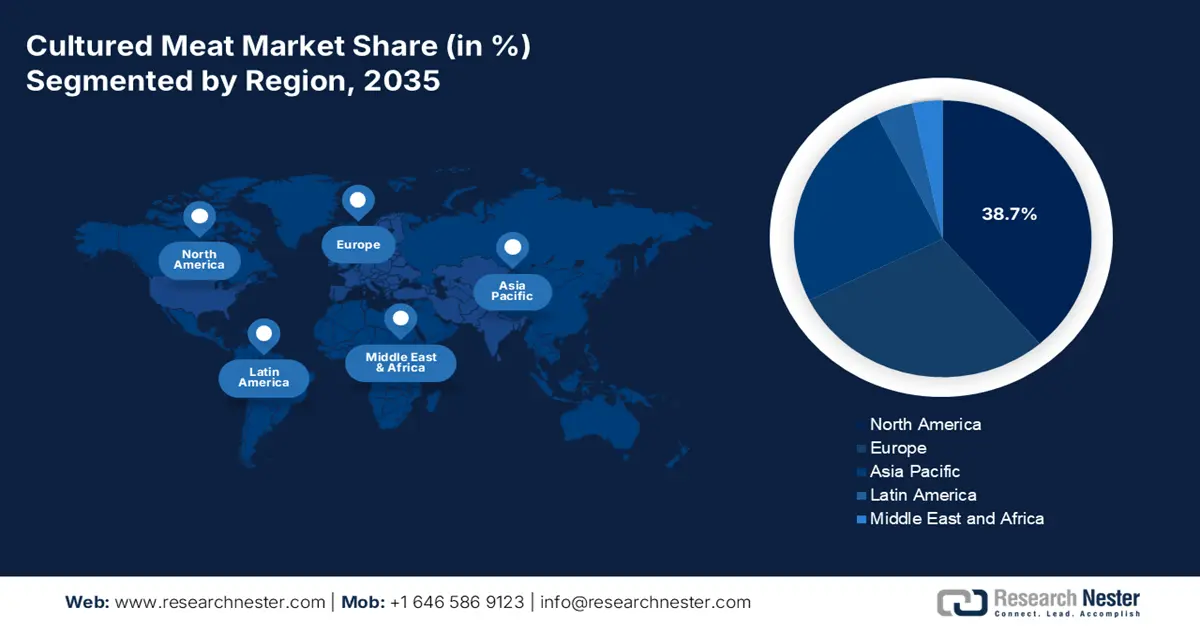

- By 2035, North America is set to capture a 38.7% share of the cultured meat market owing to its pioneering regulatory clarity and strong venture capital backing.

- Asia Pacific is anticipated to expand at a 53.3% CAGR from 2026–2035 as it accelerates adoption in response to food-security pressures and proactive government endorsement.

Segment Insights:

- By 2035, the business-to-business segment in the cultured meat market is expected to secure a 60.4% share as it leverages established distribution networks to achieve scalable commercial deployment.

- The food service segment is projected to lead the end-use category by 2035 as it gains momentum through professional preparation settings that streamline early consumer introduction.

Key Growth Trends:

- Strategic government investment and policy support

- Expansion of strategic B2B partnerships

Major Challenges:

- Achieving product quality and complex structures

- Supply chain and technical expertise gaps

Key Players: UPSIDE Foods (U.S.), Eat Just (GOOD Meat) (U.S.), Mosa Meat (Netherlands), Meatable (Netherlands), Vow (Australia), Aleph Farms (Israel), Memphis Meats (Upside Foods) (U.S.), Future Meat Technologies (Believer Meats) (Israel), Shiok Meats (Singapore), BlueNalu (U.S.), Finless Foods (U.S.), SuperMeat (Israel), Avant Meats (Hong Kong), BioTech Foods (Spain), Higher Steaks (United Kingdom), Wildtype (United States), IntegriCulture (Japan), Cubiq Foods (Spain), Peace of Meat (Belgium), New Age Eats (U.S.).

Global Cultured Meat Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 292.6 million

- 2026 Market Size: USD 303.1 million

- Projected Market Size: USD 416.7 million by 2035

- Growth Forecasts: 33.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: Singapore, South Korea, Netherlands, Canada, Australia

Last updated on : 27 November, 2025

Cultured Meat Market - Growth Drivers and Challenges

Growth Drivers

- Strategic government investment and policy support: To ensure food resilience and take the lead in the food industry, governments are now actively funding research and development in the field of cellular agriculture. The prime example is the Dutch government, which has allocated over €60 million to the National Growth Fund program for cellular agriculture, based on the TUDelft data in October 2022. This funding supports a shared R&D facility, boosting the public-private partnerships. Such direct investment minimizes the risk of private ventures and surges the foundational research, hence creating a fertile ecosystem for companies such as Mosa Meat to scale. This trend signals to investors that alternative proteins are a national strategic priority. Further, these state-level initiatives are directly catalyzing the transition from research to commercial reality.

- Expansion of strategic B2B partnerships: Cultured meat companies are raising the adoption of the B2B ingredient supplier model to surge market access. The partnerships with the established food processors and restaurant chains provide immediate scale and consumer reach. SuperMeat, an Israeli startup, established a strategic cooperation with Ajinomoto, a major Japanese food manufacturing company, to produce farmed meat products and boost R&D skills. This strategy bypasses the slow build-out of consumer retail and leverages existing brand trust, allowing cultivated meat to reach a wide audience faster and more efficiently. This symbiotic relationship is crucial for embedding cultivated ingredients into mainstream food products at scale.

Summarizing Cultured Meat Company Partnerships

|

Year |

Company/Partnership |

Focus |

Key Notes |

|

2022 |

GOOD Meat (Eat Just) & ADM |

Cell culture nutrient optimization |

Partnership to accelerate cultivated chicken production through enhanced cell culture media |

|

2022 |

Wanda Fish signed licensing agreements with Tufts University. |

Development of sustainable, scalable cultivated seafood |

Collaboration aims to accelerate product development and manufacture cell-based finless fish fillets |

|

2025 |

SuperMeat & Stamm |

Enhance muscle fiber growth, elongation, and fusion into mature muscle tissue. |

Collaboration represents cross-industry technological synergy, accelerating cultivated meat commercialization. |

Source: GFI 2022, Labiotech June 2025

- Shifting consumer ethics and animal welfare awareness: Growing public awareness of industrial livestock farming’s ethical issues drives the demand for cruelty-free alternatives. A study in Nature Food has stated that animal welfare is a key motivator for consumer interest in cultured meat. Companies are highly utilizing this by indicating their slaughter-free promise. This ethical driver is mainly potent among the younger demographics, hence shaping long-term purchasing trends and pushing major food brands to consider integrating cultivated products to future-proof their portfolios. This generational shift in values is creating a durable, long-term demand signal for the industry. As a result, ethical positioning is becoming a non-negotiable component of brand identity for new entrants.

Challenges

- Achieving product quality and complex structures: The whole cut products, such as the streaks, have an authentic texture and taste that is far more complex than minced meat. Further, the production of such items requires advanced scaffolding and fat and muscle cell co-culturing. Aleph Farms showcased its rib-eye in 2023, a technical milestone demonstrating progress on this front. However, one of the most critical technical challenges for the industry today is being able to replicate a conventional steak's complex marble and mouthfeel at affordable prices.

- Supply chain and technical expertise gaps: The industry lacks a mature supply chain for specialized inputs such as food-grade bioreactors and affordable growth factors. Manufacturers don’t just repurpose the existing food or pharma infrastructure. Eat Just company has addressed this issue by partnering with the bioreactor manufacturers and supply chain experts to scale the production of its GOOD Meat product in Singapore. Building such a dedicated supply chain from scratch requires a significant capital investment and collaboration with partners outside the traditional food sector.

Cultured Meat Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

33.6% |

|

Base Year Market Size (2025) |

USD 292.6 million |

|

Forecast Year Market Size (2035) |

USD 416.7 million |

|

Regional Scope |

|

Cultured Meat Market Segmentation:

Distribution Channel Segment Analysis

Under the distribution channel, the business-to-business segment is leading the segment and is expected to hold the share value of 60.4% by 2035. The segment is dominating as it is the most efficient route to market for the producers. The cultured meat companies operate as ingredient suppliers to large food processors and restaurant chains, integrating their products into the existing value chains. This model evades the need for individual consumer packaging and marketing at scale initially. It allows producers to aim on manufacturing while using the established distribution networks, marketing power of large corporate partners to achieve volume and reduce the time to market significantly. This strategic symbiosis is crucial for achieving the economies of scale needed for long-term viability.

End use Segment Analysis

The food service sector, which includes the restaurants, fast food chains, and catering, is leading the end use segment by 2035. This segment is important for presenting new food products to consumers as it is the main source that allows for professional preparation in a controlled and experience-driven setting. The foodservice facilities contributed USD 1.06 trillion, based on the USDA data in September 2025. Further partnerships between cultured meat makers and the major culinary brands, such as those demonstrated in Singapore with Eat Just, provide scale and validation. For businesses, it offers a consistent, supply-chain-resilient, and marketing-friendly product that appeals to environmentally conscious consumers, making it a strategic addition to menus before widespread retail availability. This makes food service a crucial starting point for the introduction of cultured meat into the general diet.

Source Segment Analysis

By 2035, poultry is leading the source segment and is poised to dominate the market. The dominance is mainly due to its widespread global consumption, relatively simpler cellular structure compared to red meat, and lower production costs. Top global players such as UPSIDE Foods and Eat Just are actively focusing their commercial efforts on chicken, achieving vital regulatory approvals. High consumer familiarity and the product’s versatility in dishes from nuggets to grilled breasts facilitate faster market adoption. The USDA data in July 2025 states that the total poultry sector sales in 2024 reached USD 70.2 billion, highlighting the rising demand for poultry products. Investment in its cultured counterpart as a more sustainable protein source is further motivated by the environmental costs associated with conventional poultry farming, including emissions and land consumption, which are in line with global sustainability objectives.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Source |

|

|

Type |

|

|

End use |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cultured Meat Market - Regional Analysis

North America Market Insights

North America is the global leader in the cultured meat market and is expected to hold the revenue share of 38.7% by 2035. The market is driven by a pioneering regulatory framework and concentrated venture capital investment. The region’s progress is solidified when the U.S. Food and Drug Administration completed its first pre-market consultations for cultivated chicken, establishing a vital pathway to the market. This regulatory clarity has spurred private sector activity, with U.S. cultivated meat companies receiving a significant amount of venture capital investment in 2023. This data indicates that there is strong financial backing for scaling production and R&D. The strategic focus for the market is now on achieving industrial-scale manufacturing and forging B2B partnerships with major food service and ingredient suppliers to ensure commercial distribution upon full regulatory authorization.

The U.S. cultured meat market is propelled by a clear regulatory pathway established by the USDA and FDA. This framework culminating in historic pre-market consultations, provides the certainty required for the significant capital investment. The market trends are defined by the strategic partnerships among the cultivated meat producers and the food service distributors, aiming for the initial placement in the high-end culinary and food service venues. The Congress.gov data in September 2023 states that the U.S. Food and Drug Administration (FDA) has provided the premarket review and approval for 2 companies, GOOD Meat and UPSIDE Foods, in 2022 to sell the cell-cultivated chicken in U.S. markets. Further, the Good Food Institute has projected that from 2010 to 2022, nearly USD 3 billion was invested in private capital in cell-cultivated meat and seafood companies. This confluence of regulatory milestones and financial backing strengthens the U.S. as the top market for commercialized cultivated products.

Canada’s cultured meat market is defined by the strong federal support for the broader alternative protein ecosystem as part of its economic and innovation strategy. The Protein Industries Canada is expected to invest over USD 30 million by 2027 into these artificial intelligence projects, benefiting the plant-based and agrifood sector, according to the Protein Industry Canada data in September 2022. The investment has reliance on the cultivated meat ecosystem as AI tools are used for ingredient optimization, bioprocessing, and food-safety modelling, and can be applied across both plant-based and cell-based protein production systems. The key trends are the significant research leadership from the academic institutions and a strategic focus on using Canada’s strength in agricultural biotechnology and fermentation.

APAC Market Insights

Asia Pacific is forecasted to be the fastest growing cultured meat market and is expected to grow at a CAGR of 53.3% during the forecast period 2026 to 2035. The market is driven by the processing food security challenges, dense urban populations and proactive government endorsements. With nations such as China integrating cellular agriculture into their national food security plans, APAC is under tremendous pressure to find sustainable protein sources. Singapore has emerged as a global leader after its regulatory office granted Eat Just the world's first commercial permission for the sale of grown chicken, setting a strong precedent. Further, the consumer acceptance is also notably high and companies are also forming B2B partnerships with the major local food conglomerates to integrate cultivated products into existing supply chains and familiar product formats, ensuring faster and wider market penetration.

China’s cultured meat market is strategically developing under the guidance of its national food security agenda. The government in China formally included cellular agriculture in its Five-Year Agricultural Plan in 2022, signaling a high-level endorsement and directing public research funding. This state-led initiative aims to minimize the dependence on imported protein. According to the NLM study in February 2021, the acceptance rate of artificial meat in China is 52.9% considering it as an alternative source to conventional meat. This data depicts that more than half of the population in China would opt for the cultivated meat and seafood over the traditional option. Further, the top-down approach defines the market's trajectory, with the main focus on R&D to master the key technologies and secure a long-term domestic protein supply, followed by commercial applications.

The cultivated meat market growth in Japan is due to the significant government R&D investment and proactive industry consortia. In 2024, the Japan Association of Cellular Agriculture was officially started with the support of the Ministry of Agriculture, Forestry and Fisheries, to develop the safety standards and public acceptance. The Asia Pacific Society for Cellular Agriculture report in February 2024 has indicated that 42.2% of the people in Japan are willing to try the cultivated meat, with the condition that it is proven safe to consume. Further, rising R&D funding by the government on cellular agriculture surges the development of such innovative products. This fusion of public funding and structured industry collaboration positions Japan as a key future innovator in the sector.

Europe Market Insights

Europe is rapidly expanding in the cultured meat market and is defined by a strong research foundation and a cautious science-driven regulatory pathway led by the European Food Safety Authority. The sustainable and resilient food system built by the European Union’s strategic policy objectives is driving the market growth. Further, the public funding is a critical driver; for instance, the EU’s Horizon Europe research program has allocated significant funding to cellular agriculture projects to develop sustainable growth factors. Consumer demand-driven is evolving, and people in Italy, Spain, and Germany are willing to purchase cultivated meat. However, the market faces a complex landscape of member-state opinions, with countries such as the Netherlands actively promoting public-private R&D partnerships, while others remain more conservative, resulting in a patchwork of national-level support that influences the pace of commercial rollout across Europe.

UK is projected to hold the largest share in the Europe cultured meat market and is driven by its proactive regulatory policy and concentrated research excellence. The UK has moved to streamline its novel food regulatory process under the Food Standards Agency, which aims to become a more agile environment for approvals compared to the EU. According to statistics from UK Research and research in August 2024, the government has authorized the creation of a £15 million national alternative protein research hub. This data demonstrates the growing support for R&D, scale-up, and commercialization of plant-based, fermentation-derived, and cultured meat technologies. Further, the combination of regulatory clarity and targeted public investment creates a fertile ecosystem for companies to scale in the market and position the UK top player in cellular agriculture advancements.

Germany is expected to be the second-largest market, and the growth is fueled by the significant federal R&D funding and a strong industrial biotechnology sector. The country’s National Bioeconomy strategy explicitly supports the development of alternative protein sources. This top-down support is amplified by Germany’s inherent strengths in the industrial biotechnology and precision engineering that are critical for scaling up the production processes, such as the bioreactor design and process automation. Furthermore, the presence of a large and environmentally conscious people base provides a ready market for the sustainable proteins. This combination of the strategic government direction, technical expertise, and the market demand creates a powerful ecosystem for companies to innovate and scale, setting Germany’s role as a key hub for the cultured meat industry.

Key Cultured Meat Market Players:

- UPSIDE Foods (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Eat Just (GOOD Meat) (U.S.)

- Mosa Meat (Netherlands)

- Meatable (Netherlands)

- Vow (Australia)

- Aleph Farms (Israel)

- Memphis Meats (Upside Foods) (U.S.)

- Future Meat Technologies (Believer Meats) (Israel)

- Shiok Meats (Singapore)

- BlueNalu (U.S.)

- Finless Foods (U.S.)

- SuperMeat (Israel)

- Avant Meats (Hong Kong)

- BioTech Foods (Spain)

- Higher Steaks (United Kingdom)

- Wildtype (United States)

- IntegriCulture (Japan)

- Cubiq Foods (Spain)

- Peace of Meat (Belgium)

- New Age Eats (U.S.)

- Upside Foods is a frontrunner in the cultured meat market and has achieved a key U.S. regulatory milestone. Their primary strategy involves scaling the production within their engineered pilot plant to bring cultivated chicken and eventually other products to market. By reducing the cost of growth media and developing cell lines, the company aims to make its products commercially viable and accessible.

- Eat Just, via its Good Meat division, has made history with the first-ever commercial sales of cultured chicken in Singapore. Its strategic initiatives in the market include aggressive global expansion and pursuing regulatory approvals in multiple countries. The company uses its established consumer brand to build market trust and is investing in large-scale production capabilities.

- Mosa Meat, co-founded by the creator of the first cultured beef burger, is a prime player in the European cultured meat market. Their strategic focus is on reducing the fetal bovine serum from their process, which is the key to ethical scaling and cost reduction. Mosa Meat is also pioneering a cellular agriculture approach and is aiming to create a completely animal-free supply chain for growth factors.

- Meatable has distinguished itself in the market by its proprietary opti-ox technology that bypasses the need for fetal bovine serum by using pluripotent stem cells. This method allows them to speed up the cultivation process by producing fat and muscle cells in days instead of weeks.

- Vow is taking a distinctive approach in the cultured meat market and is not focusing on replicating the common meats but creating entirely new culinary experiences. Their primary strategy involves using cells from non-traditional and exotic species such as Japanese quail and kangaroo to develop flavor profiles. The company accounted for the revenue share during the second quarter of 2024 was 533.1 million.

Here is a list of key players operating in the global market:

The cultured meat market is highly dynamic and competitive, defined by a global race for commercial scale and regulatory approvals. The key players from Europe, Israel, and the U.S. are leading the market. Their prime strategic initiatives focus on achieving cost reduction via technological innovation in cell culture media and bioreactor design. Partnerships are vital, and companies are actively forming alliances with the top players in the food industry, pharmaceutical firms, and biotechnology suppliers to access expertise and scale production. For example, in November 2025, Hub71’s Orbillion and Fork & Good have partnered to bring cultivated red meat to their global customer base. Furthermore, significant investment is directed into securing regulatory approvals in major markets, which is the vital step preceding the consumer launch. The predominant goal is to switch from the pilot scale production to building large-scale commercial facilities which is capable of bringing products to market at a competitive price point.

Corporate Landscape of the Cultured Meat Market:

Recent Developments

- In October 2025, The Good Food Institute (GFI) has announced that it has acquired the cultivated meat cell lines and growth media developed by SCiFi Foods to make them available to the whole sector.

- In August 2025, Meatable announced the acquisition of Uncommon Bio’s cultivated meat platform, including its key technology, several intellectual property assets and high performing cell lines, and expert staff.

- In May 2024, GOOD Meat began the World’s first retail sales of cultivated chicken. GOOD Meat has partnered with Huber’s Butchery in Singapore to sell the new, lower cost formulation using just 3% cultivated chicken while maintaining the same delicious taste, texture and experience as conventional chicken.

- Report ID: 8272

- Published Date: Nov 27, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.