Chemical Catalyst Market Outlook:

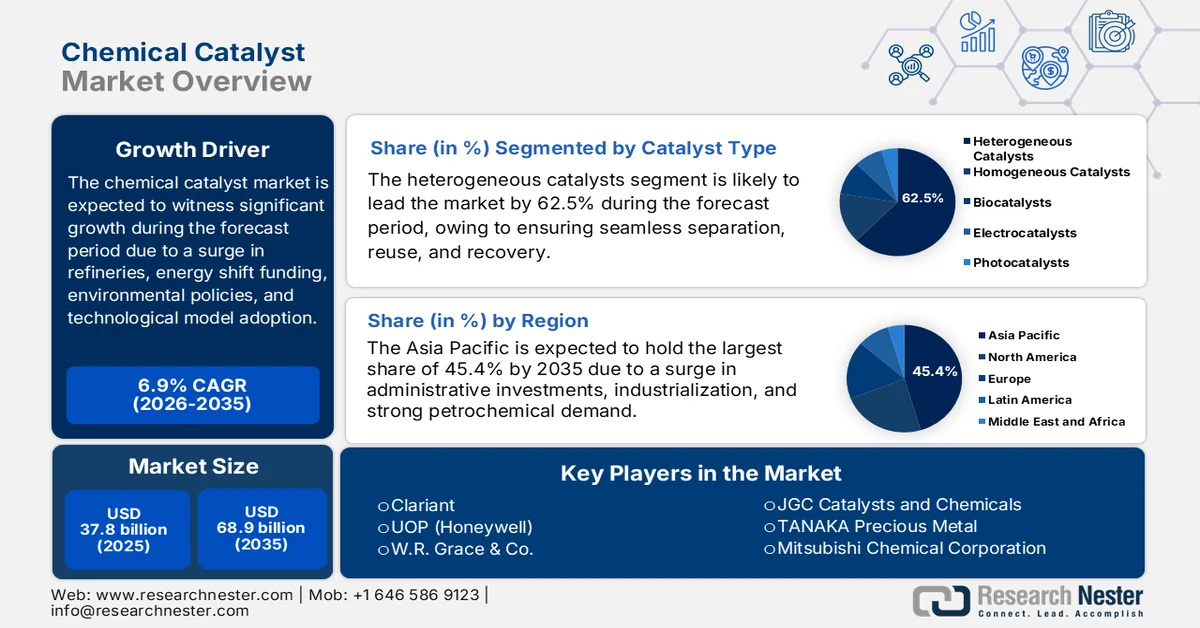

Chemical Catalyst Market size was valued at over USD 37.8 billion in 2025 and is expected to reach USD 68.9 billion by the end of 2035, growing at a CAGR of 6.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of chemical catalyst is assessed at USD 40.4 billion.

The worldwide chemical catalyst market is continuously expanding, owing to factors such as energy transition investments, expansion in refineries, environmental regulations, and a shift in business and technological models. According to official statistics published by the U.S. Energy Information Administration (EIA) in August 2024, the global refining capacity was estimated to account for 103.5 million barrels per day as of 2023. Additionally, the planned bulk growth in refined product output has been witnessed in the Asia Pacific, especially in India and China, as well as in the Middle East. However, it has been estimated that between 2.6 million barrels per day and 4.9 million barrels per day of refining capacity will be available online by the end of 2028. Moreover, an increase in refinery projects has been planned to be accomplished by the same year, which denotes an optimistic outlook for the market upliftment globally.

Planned Global Refinery Projects Analysis by 2028

|

Country |

Refinery Operator (Site Location) |

Estimated Crude Distillation Unit Capacity |

Start-Up Year |

Capacity Type |

|

China |

Yulong (Shandong) |

400,000 barrels per day |

2025 |

New |

|

China |

Sinopec Zhenhai (Zhejiang) |

250,000 barrels per day |

2026 |

Expansion |

|

India |

Indian Oil (Gujarat) |

86,000 barrels per day |

2025 |

Expansion |

|

India |

Chennai Petroleum (Nagapattinam) |

180,000 barrels per day |

2027 |

New |

|

Bahrain |

Bahrain Petroleum (Sitra) |

110,000 |

2025 |

Expansion |

|

Iran |

National Iran-based Oil Refining and Distribution Company (Bandar Abbas) |

120,000 barrels per day |

2025 |

Expansion |

|

Iraq |

Iraqi Ministry of Oil (Haditha) |

20,000 barrels per day |

2024 |

Expansion |

|

Jordan |

Jordan Petroleum Refinery Company (Zarqa) |

50,000 barrels per day |

2027 |

Expansion |

|

Oman |

Oman Oil Company, Kuwait Petroleum International (Duqm) |

17,000 barrels per day |

2024 |

Expansion |

|

Saudi Arabia |

Saudi Aramco Total Refining and Petroleum Company-SATORP (al Jubail) |

40,000 barrels per day |

2026 |

Expansion |

|

Nigeria |

Dangote Group (Lagos) |

650,000 |

2024 |

New |

|

Mexico |

Pemex Olmeca refinery (Dos Bocas) |

340,000 barrels per day |

2025 |

New |

Source: U.S. Energy Information Administration (EIA)

Furthermore, the AI-based and digital twin catalyst formulation, the on-site catalyst regeneration and mobile services, along with multifunctional and bifunctional catalyst design, are a few trends that are responsible for bolstering the chemical catalyst market globally. As stated by a data report published by the Asia Development Bank Organization in May 2025, the estimated industrial growth for digital twins was 36% of the yearly growth as of 2025. This has deliberately resulted in unlocking an additional benefit of USD 1.3 trillion in terms of economic valuation and the imminent reduction in 7.5 gigatons of carbon dioxide, which is equivalent by the end of 2030. Besides, companies are focused on incorporating cloud computing, with a predicted 50% of global enterprises poised to utilize the technology by the end of 2028, thus denoting a huge growth opportunity for the chemical catalyst market.

Key Chemical Catalyst Market Insights Summary:

Regional Highlights:

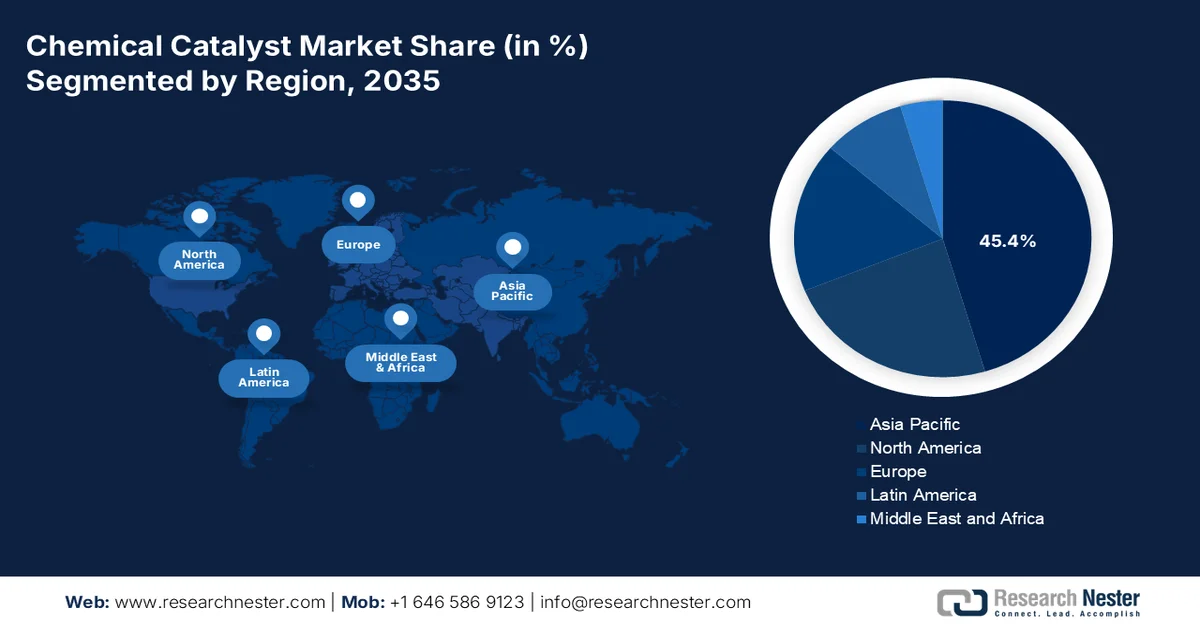

- Asia Pacific chemical catalyst market is projected to dominate with a 45.4% share by 2035, bolstered by rapid industrialization, refining capacity expansion, and rising petrochemical demand

- Europe is anticipated to register notable expansion through 2035, stimulated by strong decarbonization initiatives and growing emphasis on green hydrogen production

Segment Insights:

- The heterogeneous catalysts segment in the chemical catalyst market is expected to hold a dominant 62.5% share by 2035, reinforced by its ability to enable efficient separation, recovery, and reuse without disrupting industrial processes

- The metal and metal oxides sub-segment is projected to secure the second-largest share market during 2026-2035, accelerated by its versatile catalytic properties and increasing application in advanced industrial and environmental technologies

Key Growth Trends:

- Transition towards recycled feedstocks in catalyst manufacturing

- Labor shortage in catalysis science and engineering

Major Challenges:

- Volatility and geopolitical concentration of precious metal supplies

- Stringent environmental regulations accelerating obsolescence

Key Players: BASF Germany, Johnson Matthey UK, Clariant Switzerland, UOP Honeywell U.S., W.R. Grace & Co. U.S., Evonik Industries Germany, Shell Catalysts & Technologies Netherlands, LyondellBasell Industries Netherlands/U.S., Umicore Belgium, Haldor Topsoe Denmark, Axens France, Ineos UK, JGC Catalysts and Chemicals Japan, TANAKA Precious Metal Japan, Mitsubishi Chemical Corporation Japan, Sinopec China, CNPC China, Cataler Japan, Heraeus Germany, Sasol South Africa, Honeywell U.S., Ecovyst Inc..

Global Chemical Catalyst Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 37.8 billion

- 2026 Market Size: USD 40.4 billion

- Projected Market Size: USD 68.9 billion by 2035

- Growth Forecasts: 6.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.4% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Saudi Arabia, Indonesia, Vietnam

Last updated on : 13 April, 2026

Chemical Catalyst Market - Growth Drivers and Challenges

Growth Drivers

- Transition towards recycled feedstocks in catalyst manufacturing: The chemical catalyst market is undergoing a feedstock-based shift, denoting the ultimate growth driver. According to official statistics published by NLM in February 2025, the optimized catalyst usually receives a bisphenol A (BPA) conversion rate of 100%, along with a hydrogenated bisphenol A (HBPA) selectivity rate of 96.4%. Besides, bismuth titanate perovskite is deliberately prepared by a green synthesis methodology and also utilized as a photocatalyst for hydrogen production through a photochemical cell reactor, and accounts for a hydrogen yield of 39.24 µmol/g that is obtained with methanol. Therefore, with the capability of such developments, there is a huge growth opportunity for the market across different regions.

- Labor shortage in catalysis science and engineering: A silent structural constraint is the global shortage of skilled catalysis researchers and process engineers. In this regard, university programs in heterogeneous catalysis, surface chemistry, and kinetic modeling have declined in enrollment over the past decade, as students gravitate toward software and data science. Simultaneously, the average age of experienced catalyst engineers at refineries and chemical plants is gradually increasing. This talent gap delays the commercialization of novel catalyst formulations and extends troubleshooting times when reactor performance degrades. However, to combat this, chemical companies are currently partnering with technical institutes to fund dedicated catalysis chairs and online certification programs, which are positively driving the chemical catalyst market globally.

- Insurance and liability expenses for catalyst failures: The rising cost of insuring large-scale catalytic reactors is yet another growth driver for the chemical catalyst market worldwide. This readily caters to catalyst utilization for converting plastic waste into hydrogen, which eventually boosts the market demand globally. In this regard, and as per the June 2025 NLM article, plastic production is continuously increasing and has been estimated to reach 413.8 million tons as of 2023. Therefore, the catalytic reactor range for plastic intake usually ranges from 1 to 10 tons regularly, and for batch reactors, the range is between 5 and 30 tons per day in continuous reactors. Hence, there has been an increase in utilizing catalysts for converting plastic waste into high-value products, thus denoting an optimistic outlook for the chemical catalyst market expansion.

Challenges

- Volatility and geopolitical concentration of precious metal supplies: The chemical catalyst market remains heavily dependent on platinum group metals (PGMs) such as platinum, palladium, and rhodium, which are essential for automotive emission control, petrochemical reforming, and hydrogen production. Besides, the push for electric vehicles diminishes long‑term PGM demand in exhaust systems, discouraging new mining investments and tightening supply for industrial catalytic processes. While recycling of spent catalysts, particularly for urban mining, is growing, recovery rates for rhodium remain low due to technical complexity. Moreover, without rapid commercialization of PGM‑free or low‑PGM catalyst formulations, the market faces recurring cost shocks and supply insecurity, slowing down capacity expansions in emerging economies.

- Stringent environmental regulations accelerating obsolescence: The aspect of regulatory pressure is intensifying faster than catalyst R&D cycles, which is causing a hindrance in the chemical catalyst market globally. Besides, Europe’s REACH revision, China’s Dual Carbon goals, and the U.S. EPA’s tightened emission norms are phasing out traditional metal‑based catalysts containing lead, chromium, or high levels of rare earths. Simultaneously, new rules targeting volatile organic compounds (VOCs) and nitrous oxide (N₂O) emissions require catalyst systems that did not exist commercially five years ago. For instance, catalytic decomposition of nitrous oxide in nitric acid plants is now mandated in several regions, but retrofitting existing plants is capital‑intensive, thus limiting the chemical catalyst market growth.

Smart Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.9% |

|

Base Year Market Size (2025) |

USD 37.8 billion |

|

Forecast Year Market Size (2035) |

USD 68.9 billion |

|

Regional Scope |

|

Chemical Catalyst Market Segmentation:

Catalyst Type Segment Analysis

The heterogeneous catalysts segment, part of the catalyst type, is expected to account for the largest share of 62.5% in the chemical catalyst market by the end of 2035. The segment’s upliftment is primarily attributed to enabling seamless separation, recovery, and reuse without halting industrial processes. This particular segment delivers substantial operational cost savings and continuous production uptime, which is critical for large-scale applications such as petroleum refining, ammonia synthesis via the Haber-Bosch process, and methanol-to-olefins conversion. Besides, as refineries upgrade to process heavier, sourer crude slates and produce cleaner fuels, heterogeneous catalyst demand will remain robust. Their reusability also aligns with circular economy goals, minimizing hazardous waste generation compared to homogeneous alternatives, thus driving the market development.

Material Segment Analysis

Based on the material segment, the metal and metal oxides sub-segment is projected to account for the second-largest share in the chemical catalyst market during the forecast period. The sub-segment’s growth is highly driven by its ability to modernize technology, electronics, and industry, owing to versatile catalytic properties, structural strength, and high thermal or electrical conductivity. According to official statistics published by NLM in March 2025, almost 85% to 90% of all freshwater is readily utilized for irrigation in agricultural land across Asia and Africa. Additionally, agriculture continues to be considered the predominant user of worldwide freshwater resources, demonstrating an estimated 70% of overall withdrawals. Besides, to effectively maintain this, metals, such as silicon dioxide and its composites, are increasingly utilized as absorbents for removing pesticides from freshwater, which is positively driving the sub-segment’s growth.

Silicon Dioxide and Composites Analysis as Absorbents for Pesticide Removal (2025)

|

Absorbent Type |

Structure |

Pesticide |

Absorption Removal |

|

MgO NPs |

Magnesium oxide nanoparticles |

Thiamethoxam |

60.13% |

|

Chlorpyriphos |

80.53% |

||

|

Fenpropathrin |

92.49% |

||

|

MTBC |

Triadimefon and Dinotefuran |

Triadimefon |

86.42% |

|

Dinotefuran |

87.86% |

||

|

MgO/Fe3O4-synthesized porous carbons |

MgO/Fe3O4 modified coconut shell biochar |

Atrazine |

90.24% |

|

MgFe2O4 |

Mesoporous magnesium ferrite |

Chlorpyrifos |

91.0% |

Form Segment Analysis

By the end of the stipulated timeline, the power sub-segment, which is part of the form segment, is expected to hold the third-largest share in the chemical catalysts market. The sub-segment’s development is highly propelled by its importance in the modernized industry for ease of transport, long-lasting shelf-life, and high stability in comparison to liquids. As stated in an article published by NLM in May 2024, on average, 75% of global manufacturing processes across chemical industries are significantly involved in powders or particulate solids almost once or twice throughout the cycle. Moreover, the aspect of mixing the blade with mixed lubricated and unlubricated granules led to optimizing the powder flow, which has the capability to diminish the overall manufacturing operation by 75%, thereby making it suitable for bolstering the sub-segment’s exposure.

Our in-depth analysis of the chemical catalyst market includes the following segments:

|

Segment |

Subsegments |

|

Catalyst Type |

|

|

Material |

|

|

Form |

|

|

Application |

|

|

End use Industry |

|

|

Process |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Key Chemical Catalyst Market Players:

APAC Market Insights

The Asia Pacific in the chemical catalyst market is anticipated to garner the highest share of 45.4% by the end of 2035. The market’s upliftment is primarily attributed to rapid industrialization, expansion in refining capacities, the strong demand from petrochemical and automotive industries, the green chemistry adoption, significant government investments, and a shift towards high-value and specialty catalysts. According to official statistics published by the Institute for Energy Economics and Financial Analysis in March 2026, India is considered the net importer of petrochemicals and chemicals, with nearly 45% of the nation’s petrochemical-based intermediate products imported. However, to diminish this import reliance, the country planned a significant capacity extension and enabled an increase in its petrochemical intensity index to 13% as of 2025, which is responsible to uplift the market in the overall region.

The chemical catalyst market in China is growing significantly, owing to the presence of national oil organizations, the enforcement of strict environmental regulations, strategies to lower emissions, the competitive pricing to support catalyst export, and a massive domestic demand for refining. As stated in an article published by the Observatory of Economic Complexity in March 2026, the country significantly exports reactions and catalysts, which are worth USD 1.3 billion, while the import valuation is worth USD 1.6 billion. Besides, based on the March 2024 U.S. EIA article, in terms of refinery facilities or crude oil processing, the country has averaged 14.8 million barrels per day as of 2023. Moreover, domestic organizations have planned LPG and naphtha capacities, including the 400,000-b/d Yulong refining and petrochemical complex, thus proliferating the chemical catalyst market upliftment.

The aspects of an increase in the chemical production, massive government investment in the construction and infrastructure industry, focus on organic and inorganic chemical export valuation, a surge in the demand for oil, and the need for advanced hydrotreating catalysts are drivers that are responsible for proliferating the chemical catalyst market in India. As per an article published by the IBEF Organization in December 2025, the country is regarded as the 6th largest chemical-producing nation globally and the 3rd largest in the region, effectively contributing 7% to domestic GDP. Besides, the chemicals industry in the country was worth USD 250 billion as of 2024, which further grew to USD 300 billion by the end of 2025, and is anticipated to surge to USD 1 trillion by 2040. Moreover, the 2030 vision is focused on making the nation emerge as the ultimate chemical manufacturing powerhouse with a 5% to 6% worldwide chemical value chain, which is positively driving the market upliftment.

Major Chemicals and Petrochemicals Production Analysis in India (2018-2024)

|

Year |

Production (Million metric tons) |

|

2018 |

47.88 |

|

2019 |

49.1 |

|

2020 |

55.46 |

|

2021 |

53.4 |

|

2022 |

57.33 |

|

2023 |

53.65 |

|

2024 |

40.58 |

Source: IBEF Organization

Europe Market Insights

Europe in the chemical catalyst market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the robust decarbonization agenda, circular economy mandates, the existence of notable catalytic solutions for carbon dioxide utilization, and a shift from commodity catalysts to high-value specialty formulations for green hydrogen production. According to official statistics published by the Europe Commission in 2025, hydrogen readily accounted for less than 2% of the region’s energy consumption as of 2022 and was primarily utilized for producing chemical products, including fertilizers and plastics. Besides, the 2022 REPowerEU Strategy has aimed out in both producing and import 10 million tons by the end of 2030, thereby making it suitable for developing the market in the region.

The chemical catalyst market in Germany is gaining increased traction, owing to its status as the largest chemical producer and automotive manufacturing facility, the notable producer of platinum catalysts by valuation, administrative support for industrial decarbonization, and generous expenditure on sustainable catalysts. As stated in an article published by the Clean Energy Wire Organization in February 2025, the country has effectively set an interim objective of reducing emissions by almost 65% by the end of 2030 and 88% by the end of 2040. Besides, the domestic government presented an approach to ensuring long-lasting negative emissions, resulting in the reduction of greenhouse gases in the atmosphere to successfully reach the 1.5-degree Celsius target that has been set as part of the Paris Agreement, thereby positively catering to the chemical catalyst market growth.

The significant establishment of major automotive manufacturing facilities, industrial investment through suitable tax policies, and an increase in attracting foreign direct investment in chemical manufacturing are trends that are responsible for fueling the chemical catalyst market in Slovakia. As per a data report published by the Adapt Institute Organization in February 2024, the country comprises 4 leading original equipment manufacturers (OEMs), including Jaguar Land Rover, Kia, Stellantis, and Volkswagen, along with Volvo and nearly 400 localized suppliers. Besides, a standard battery electric vehicle drivetrain utilizes more than 100 fewer moving parts in comparison to an internal combustion engine vehicle. Moreover, with the adaptation to the impending transition to battery electric vehicles, the country’s GDP is poised to increase by more than 10%, thereby positively impacting the chemical catalyst market development.

North America Market Insights

North America in the chemical catalyst market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by the presence of strict environmental regulations, an expansion of petrochemical refining capacities, the adoption of advanced catalytic solutions, and the shift towards shale gas-driven feedstocks. According to official statistics published by the U.S. EIA in July 2024, the operable atmospheric crude oil distillation capacity in the U.S. accounted for a total of 18.4 million barrels per calendar day at the beginning of 2024, denoting a 2% surge in comparison to 2023. Moreover, there are three large-scale refineries in the country, including ExxonMobil, Valero, and Marathon, all of which reported an upsurge in refinery capacity, which is positively driving the market in the overall region.

Production Capacity Analysis of Operable Petroleum Refineries in the U.S. (2020-2025)

|

Petroleum Product |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

|

Alkylate |

1,349,148 |

1,313,769 |

1,293,931 |

1,301,541 |

1,316,691 |

1,368,437 |

|

Aromatics |

331,976 |

327,156 |

311,656 |

290,956 |

348,556 |

349,509 |

|

Asphalt & Road Oil |

651,049 |

642,049 |

689,649 |

659,335 |

644,335 |

641,104 |

|

Isomers |

772,440 |

744,358 |

758,218 |

767,518 |

778,968 |

767,468 |

|

Lubricants |

260,545 |

263,545 |

263,545 |

263,545 |

263,545 |

262,895 |

|

Marketable Petroleum Coke |

908,574 |

893,979 |

882,940 |

883,320 |

889,671 |

876,696 |

|

Hydrogen (Million Cu. Ft. per day) |

3,126 |

2,893 |

2,893 |

2,875 |

2,913 |

3,022 |

|

Sulfur (Short tons per day) |

41,917 |

40,578 |

40453 |

40437 |

40376 |

39,872 |

Source: U.S. EIA

The chemical catalyst market in the U.S. is gaining increased exposure, owing to the overall industrial catalyst consumption, expansion in refineries across the Midwest and Gulf Coast, the incorporation of advanced zeolite, the presence of supportive metal catalysts, investments in environmental catalyst technologies, and growth in the polymer industry. As stated in an article published by the America’s Plastic Makers Organization in September 2025, products in the polymer industry supported almost 5 million employment opportunities in the country as of 2024. Based on this, the domestic plastics manufacturing industry operated across more than 11,600 facilities, further employing about 670,000 workers directly and effectively generating USD 48.6 billion. Moreover, the industry produced almost USD 380 billion of plastic products and resins, and also invested USD 17.5 billion in the latest equipment and facilities, thus fueling the market growth.

The demand for efficient chemical processes across automotive, pharmaceuticals, and petrochemical industries, an increase in the demand for environmentally friendly catalysts, the promotion of sustainable manufacturing practices, and the continuous growth in chemical industries are factors that are responsible for bolstering the chemical catalyst market in Canada. As per an article published by the Environmental Defense in April 2024, the Government of Canada offered almost USD 30 billion in terms of public financing and direct subsidies to the oil and gas industry. Moreover, the government also provided nearly USD 29.6 billion as a financial support to the petrochemical and fossil fuel organizations. This comprises USD 21 billion in financing for the TransMountain expansion pipeline, as well as USD 7.5 billion in public financing through Export Development Canada. This caters to more than required resources to develop interprovincial electricity infrastructure, which roughly amounts to USD 24 billion, thus uplifting the chemical catalyst market expansion.

Key Smart Packaging Market Players:

- BASF (Germany)

- Johnson Matthey (UK)

- Clariant (Switzerland)

- UOP (Honeywell) (U.S.)

- W.R. Grace & Co. (U.S.)

- Evonik Industries (Germany)

- Shell Catalysts & Technologies (Netherlands)

- LyondellBasell Industries (Netherlands/U.S.)

- Umicore (Belgium)

- Haldor Topsoe (Denmark)

- Axens (France)

- Ineos (UK)

- JGC Catalysts and Chemicals (Japan)

- TANAKA Precious Metal (Japan)

- Mitsubishi Chemical Corporation (Japan)

- Sinopec (China)

- CNPC (China)

- Cataler (Japan)

- Heraeus (Germany)

- Sasol (South Africa)

- Honeywell (U.S.)

- Ecovyst Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF is a dominant force in the chemical catalyst sector, offering an extensive portfolio that spans refinery, petrochemical, emission control, and specialty catalysis solutions. The company focuses heavily on next-generation catalyst technologies for sustainable chemistry, including applications for green hydrogen and plastic recycling.

- Johnson Matthey has long been a global leader in precious metal catalysts, particularly for automotive emission control and hydrogen fuel cell systems. The firm is strategically pivoting its catalyst business toward high-growth areas like net-zero transport and sustainable fuels.

- Clariant differentiates itself through high-performance catalysts for syngas, ethylene oxide, and propylene production, with a strong emphasis on process efficiency. The company actively pursues innovative catalyst designs that reduce energy consumption and byproduct formation in large-scale chemical plants.

- UOP provides integrated catalyst and process technology solutions, particularly for petroleum refining and petrochemical production, often bundling catalysts with proprietary reactor designs. Its offerings are engineered to maximize yields from heavy feedstocks while meeting tightening fuel specifications.

- W.R. Grace & Co. is a specialist in fluid catalytic cracking (FCC) catalysts and additives, serving the global refining industry with products that enhance gasoline yield and reduce emissions. The company continuously refines its catalyst formulations to help refiners process lower-quality crude slates more profitably.

Here is a list of key players operating in the global chemical catalyst market:

The global chemical catalyst market is highly consolidated, with the top five players, BASF, Johnson Matthey, Clariant, UOP (Honeywell), and Grace, controlling a significant share. Besides, notable strategic initiatives include a decisive pivot from volume-based sales to performance-based catalyst-as-a-service models. Major players are also heavily investing in R&D for sustainable solutions, including green hydrogen, carbon capture, and bio-based feedstocks, to align with stringent environmental regulations. For instance, in May 2025, Honeywell acquired Johnson Matthey’s Catalyst Technologies business for USD 2.4 billion in terms of an overall cash transaction. This acquisition demonstrates an estimated 11 times roughly 2025 EBITDA, which underscored the chemical catalyst market trend toward consolidation and portfolio expansion in advanced process technologies, thus driving the chemical catalyst industry worldwide.

Corporate Landscape of the Chemical Catalyst Market:

- Report ID: 8510

- Published Date: Apr 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.