Catalysts Market Outlook:

Catalysts Market size was over USD 43.9 billion in 2025 and is poised to exceed USD 68.8 billion by the end of 2035, growing at over 4.6% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of Catalysts is estimated at USD 45.9 billion.

The rapid expansion of the green hydrogen economy, advanced plastic recycling, and bio-based chemical production is creating encouraging opportunities for growth in the catalysts market globally. Also, the market is making a shift towards a highly innovative and sustainability-driven future, propelled by the industrial transition toward green chemistry and renewable energy sources. In 2024, the article published by the International Energy Administration revealed that global hydrogen production reached about 97 Mt in 2023, with less than 1% being low-emissions, whereas electrolyser capacity stood at 1.4 GW, with potential announced capacity rising to 520 GW by 2030. The article also mentions that the cost of renewable hydrogen was 1.5 to 6 times higher than fossil-based production, and thus such unprecedented production capabilities elevate the growth potential of the catalyst industry.

Global Hydrogen Production Statistics 2022 - 2026: Production, Energy Use, and Clean Hydrogen Trends

|

Statistic |

Value |

|

Total hydrogen production |

95 million metric tons (Mt) |

|

Grey hydrogen share |

95% (from natural gas via SMR) |

|

Coal-based hydrogen share |

2% (2021) |

|

Biomass hydrogen share |

<1% (2022) |

|

SMR with CCS vs grey hydrogen |

90% reduction |

|

Energy required |

6 - 8 GJ per kg H₂ |

|

Electricity required |

40 - 50 kWh per kg H₂ |

|

Water consumption |

3 - 5 m³ per kg H₂ |

|

Share of global industrial CO₂ |

3% |

|

PEM electrolysis efficiency |

90% (small-scale, round-trip) |

|

Industrial emissions reduction potential |

80% in hard-to-abate sectors |

|

Global hydrogen investment |

USD 38 billion (2022) |

|

US clean hydrogen support |

USD 3 billion (Inflation Reduction Act) |

|

EU green hydrogen target |

10 Mt by 2030 |

|

China share of production |

30% (2022) |

Source: Worldmetrics.org

In addition, expanding industrial manufacturing and automotive sectors in emerging economies secures long-term demand for high-performance chemical agents, thus benefiting the overall market. As global supply chains stabilize with significant trade, the market is poised to evolve from traditional petroleum refining toward cleaner applications that support global net-zero goals. For instance, in July 2024, BASF Environmental Catalyst and Metal Solutions announced the beginning of construction of its first advanced green hydrogen production facility in Budenheim, Germany, to manufacture catalyst-coated membranes for PEM electrolyzers and membrane electrode assemblies for fuel cells. This investment supports the global energy transition by expanding ECMS's capabilities in terms of hydrogen technologies, precious metals, catalysts, and recycling, offering integrated end-to-end solutions.

Top Global Exporters of Supported Precious Metal Catalysts in 2023 by Shipment Value and Quantity

|

Reporter |

Trade Value (1000 USD) |

Quantity (Kg) |

|

Germany |

3,533,150.81 |

15,405,200 |

|

North Macedonia |

2,163,903.74 |

10,082,500 |

|

U.S. |

1,960,920.71 |

17,657,400 |

|

Europe |

1,948,981.16 |

13,018,800 |

|

Poland |

1,803,494.31 |

- |

|

Canada |

891,915.13 |

5,165,170 |

|

Sweden |

855,434.08 |

1,147,620 |

|

Japan |

620,394.76 |

2,997,480 |

|

Italy |

618,252.64 |

4,639,090 |

|

France |

551,490.06 |

10,008,200 |

|

Thailand |

435,359.36 |

1,780,460 |

|

Czech Republic |

424,526.07 |

1,395,710 |

|

South Africa |

411,430.73 |

3,177,590 |

|

UK |

283,969.20 |

1,889,370 |

|

China |

250,789.32 |

2,137,610 |

|

Malaysia |

248,236.35 |

2,541,820 |

|

Belgium |

243,350.93 |

4,780,000 |

|

Netherlands |

198,277.99 |

3,663,100 |

Source: WITS

Key Catalysts Market Insights Summary:

Regional Highlights:

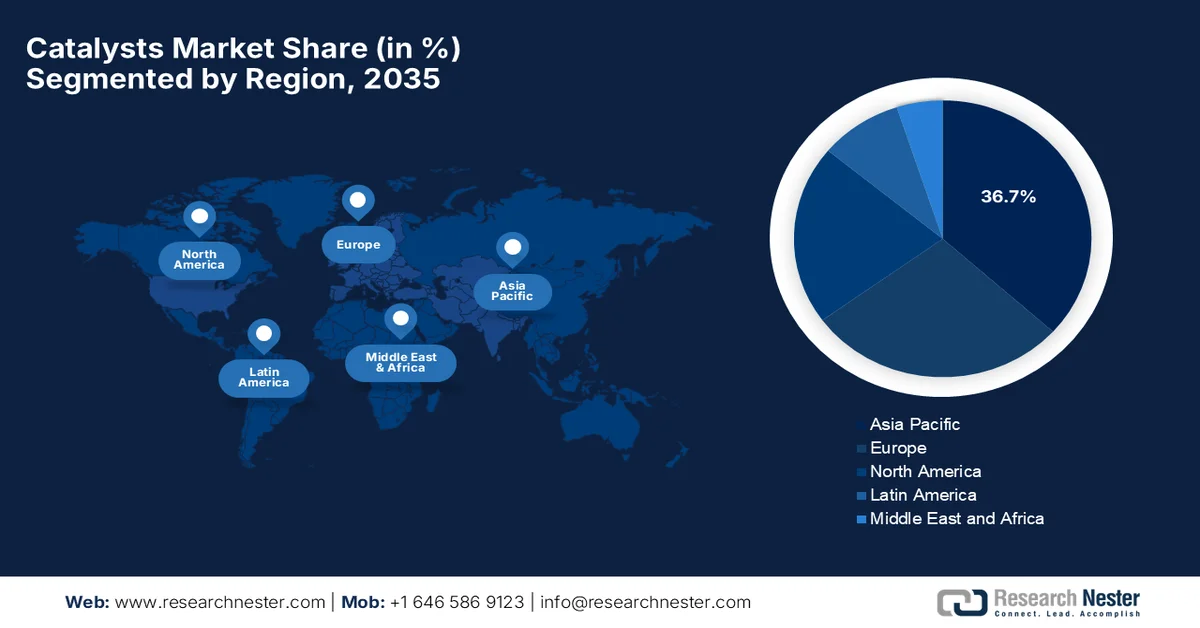

- The catalysts market in Asia Pacific is projected to account for 36.7% market share by 2035, bolstered by extensive industrialization, rising investments in localized plastic parks, and the ongoing modernization of chemical manufacturing hubs

- North America is anticipated to register remarkable growth in the 2026-2035 period, fueled by advanced refinery retrofitting, stringent environmental enforcement, and a highly sophisticated pharmaceutical synthesis sector

Segment Insights:

- The catalysts market heterogeneous catalyst segment is projected to capture 70.4% market share by 2035, reinforced by its widespread adoption across petroleum refining, petrochemical processing, polymer manufacturing, and environmental treatment

- The chemical compounds segment is anticipated to hold a considerable share by 2035, underpinned by its extensive application across chemical manufacturing processes

Key Growth Trends:

- Petrochemical expansion & refinery modernization

- Complex drug synthesis pathways

Major Challenges:

- High R&D intensity and cost pressure

- Volatility in raw material and feedstock availability

Key Players: BASF, Johnson Matthey, W. R. Grace & Co., Clariant, Haldor Topsoe, Evonik Industries, Honeywell UOP, Albemarle Corporation, Sinopec Catalyst Company, Ketjen, Saudi Aramco Technologies Company, Zeolyst International.

Global Catalysts Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 43.9 billion

- 2026 Market Size: USD 45.9 billion

- Projected Market Size: USD 68.8 billion by 2035

- Growth Forecasts: 4.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (36.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: India, South Korea, Saudi Arabia, Brazil, Vietnam

Last updated on : 7 July, 2026

Catalysts Market - Growth Drivers and Challenges

Growth Drivers

- Petrochemical expansion & refinery modernization: There is a surging demand for plastics and chemicals, and it drives global refinery runs, requiring high volumes of fluid catalytic cracking catalysts. At the same time, rapid industrialization and the expansion of plastic manufacturing hubs in the area are significantly boosting bulk market volume requirements for these refining materials. According to the article published by the Plastics Industry Association in May 2025, the global plastic products and packaging market is projected to rise from a significant USD 722.14 billion in 2024 to a substantial USD 1,146.18 billion by 2034, largely propelled by rising demand across packaging, healthcare, automotive, and electronics industries. The surging demand for plastics is due to their durability and cost-effectiveness, with increasing use in medical equipment, protective gear, and lightweight automotive components, thus elevating the demand in the market.

- Complex drug synthesis pathways: Pharmaceutical manufacturing needs certain specialized asymmetric catalysts in order to synthesize complex, high-purity molecules that also adhere to strict regulatory standards. These advanced catalysts and enzymes ensure high target yields, minimize toxic by-products, and prevent unwanted side-reactions during the production process of active pharmaceutical ingredients. For instance, in May 2024, Willow Biosciences announced a multi-product development and licensing partnership with Laurus Labs to manufacture high-value APIs by using engineered enzymes and biocatalytic processes. Willow states that its BioOxi biological hydroxylation platform enables highly selective C–H hydroxylation, a difficult asymmetric transformation, thus elevating the growth potential for the market.

Challenges

- High R&D intensity and cost pressure: The catalysts market is highly dependent on continuous innovation, which requires remarkable investment in research and development to improve efficiency and environmental performance. Therefore, developing catalysts such as those used in hydrogen production, emission control, and sustainable fuels needs advanced materials science capabilities and long development cycles. This creates entry barriers for new players and cost pressure on established manufacturers to be competitive. In addition, frequent reformulation is required to meet continuously evolving regulatory standards, especially in terms of emissions and carbon reduction. These factors increase operational costs and reduce overall profit margins in industries such as refining and chemicals that witness cyclical demand fluctuations and pricing volatility.

- Volatility in raw material and feedstock availability: The manufacturing process of catalysts is mostly dependent on certain critical raw materials such as precious metals, i.e., platinum, titanium, palladium, rhodium, zeolites, and rare earth elements, which are subject to price volatility as well as supply chain disruptions. At the same time, geopolitical conflicts, mining restrictions, and concentrated supply sources also amplify procurement risks. Fluctuations in terms of raw material prices impact production costs and profitability, and it forces manufacturers to adopt hedging strategies or alternative formulations. In addition, supply chain instability can ultimately cause delays to production schedules and affect long-term contracts with end use industries, thus negatively impacting adoption in this market.

Catalysts Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.6% |

|

Base Year Market Size (2025) |

USD 43.9 billion |

|

Forecast Year Market Size (2035) |

USD 68.8 billion |

|

Regional Scope |

|

Catalysts Market Segmentation:

Product Segment Analysis

The heterogeneous catalyst segment is projected to account for the largest market share, representing a 70.4% share in the catalysts market during the forecast period. The surging adoption across petroleum refining, petrochemical processing, polymer manufacturing, and environmental treatment is propelling the subsegment’s leadership. These catalysts are preferred due to their ease of separation from reaction mixtures, high thermal stability, and suitability for continuous production processes, making them highly suitable for high-volume manufacturing. For instance, in August 2024, BASF announced the launch of Fourtiva™, which is a new FFC catalyst designed for gasoil to mild resid feedstock, and it helps refiners maximize butylene yields, improve naphtha octane, and reduce coke and dry gas formation.

Raw Material Segment Analysis

The chemical compounds that are under the raw material segment are anticipated to hold a considerable share in the catalysts market by the end of 2035. The segment’s growth is highly driven by its higher application ranges and chemical manufacturing processes. Compounds such as peroxides, acids, and amines are some of the essential raw materials in chemical synthesis, polymer production, and environmental applications, thereby supporting a wide range of industrial operations. In December 2023, Evonik announced the acquisition of its former joint venture, Thai Peroxide Company Limited (TPL), in Saraburi, Thailand, to strengthen its production network for specialty hydrogen peroxide and peracetic acid in the Asia Pacific. This expansion supports surging demand for these chemicals, which are extensively used in microchip and solar cell manufacturing, wastewater treatment, and food safety.

Application Segment Analysis

In terms of application, chemical synthesis is expected to capture a significant share of the catalysts market during the discussed timeframe. This segment includes core industrial chemical processes and raw material transformations, such as the production of nitric acid from ammonia, which is dependent on catalysts. In addition, the ability of chemical synthesis processes to enable advanced reaction control also drives adoption and strengthens their role in the market. In June 2023, BASF and Yara Clean Ammonia jointly announced that they are evaluating a low-carbon blue ammonia project on the U.S. Gulf Coast by targeting a large-scale facility with a capacity of 1.2 to 1.4 million tons per year to meet rising global demand for cleaner ammonia. The primary aim of this project is to capture and permanently store around 95% of CO₂ emissions generated during production, significantly reducing the carbon footprint.

Our in-depth analysis of the catalysts market includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Raw Material |

|

|

Application |

|

|

Process |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Catalysts Market - Regional Analysis

APAC Market Insights

Asia Pacific catalysts market is projected to dominate with a total share of 36.7% during the forecast period. The region’s dominance is effectively propelled by extensive industrialization, burgeoning investments in localized plastic parks, and the continuous modernization of chemical manufacturing hubs. In addition, the rising downstream demand for consumer goods as well as high-performance polymers is also increasing the reliance on advanced fluid catalytic cracking and reforming processes. As of the government data published in April 2026, Australia’s recycling modernization fund is a national initiative that has generously invested a sum of USD 1 billion, including government, state, and industry funding, to expand infrastructure for recycling glass, plastics, tires, paper, and cardboard. This program aims to boost Australia’s annual recycling capacity by more than one million tons, thus supporting large-scale demand for catalysts in the country.

The country’s massive chemical manufacturing base, rising refinery modernization, and extensive development of integrated petrochemical complexes are propelling the expansion of the market in China. The country witnessed a major shift toward high-value chemical production and advanced polymer manufacturing, due to which the dependency on processing catalysts to maximize raw material yields has surged. According to an article published by the Information Technology and Innovation Foundation in April 2024, China accounted for almost 44% of global chemical production in 2022, which positions it as the largest chemical producer and market in the world. The nation's share expanded remarkably by 3.8%, showing rapid industrial expansion over the past two decades. Apart from this, China also dominates investment flows, accounting for a substantial 46% of global chemicals capital investment in 2022, thus reflecting a lucrative opportunity for catalysts players to capitalize.

In India, the market has a strong opportunity to expand owing to the rapid industrialization, massive government investments in localized chemical regions, and the aggressive expansion of domestic refining capacities. Increased demand for automotive emission-control systems and high-performance plastics also fuels a strong reliance on specialized refining and petrochemical catalysts. As per an article published by the Press Information Bureau in April 2025, India’s plastic parks scheme, which was implemented by the Department of Chemicals and Petrochemicals, aims to develop dedicated industrial zones for the plastics sector using a cluster-based development model. The article also outlined that under this scheme, the government provides up to 50% funding support to create modern infrastructure and common facilities that help strengthen downstream plastic processing industries and boost investment, production, exports, and employment.

India Plastic Parks Funding & Investments: State-Wise Project Costs, Government Grants, and Fund Disbursement Data 2020 to 2022

|

Plastic Park Location |

Approval Year |

Total Project Cost (USD million) |

Approved Grant-in-aid (USD million) |

Amount Released (USD million) |

|

Sitarganj, Uttarakhand |

2020 |

0.82 |

0.41 |

0.37 |

|

Raipur, Chhattisgarh |

2021 |

0.51 |

0.25 |

0.14 |

|

Ganjimutt, Karnataka |

2022 |

0.76 |

0.38 |

0.08 |

|

Gorakhpur, Uttar Pradesh |

2022 |

0.84 |

0.42 |

0.23 |

Source: PIB

North America Market Insights

North America catalysts market is anticipated to witness an unprecedented growth rate in the next decade, positively driven by advanced refinery retrofitting, strict environmental enforcement, and a highly sophisticated pharmaceutical synthesis sector. The region depends on certain innovative hydrotreating and fluid catalytic cracking technologies to produce ultra-low-sulfur fuels and maximize shale gas processing efficiency. For instance, in March 2023, ExxonMobil started up its USD 2 billion Beaumont refinery expansion by adding 250,000 barrels per day of new capacity and making it one of the largest refinery upgrades in the U.S. in over a decade. This expansion raises Beaumont’s total processing capacity to over 630,000 barrels per day, strengthening production of gasoline, diesel, and jet fuel while heightening the demand for suitable catalysts.

The massive shale gas utilization, extensive petrochemical manufacturing infrastructure, and stringent federal environmental regulations are certain visible factors reshaping the growth dynamics of the U.S. market. In addition, the substantial national funding and corporate net-zero commitments are accelerating the deployment of specialized catalytic systems for carbon capture technologies and sustainable aviation fuel production. In this context, the U.S. Department of Energy in January 2025 announced up to USD 100 million in funding under FOA DE-FOA-0003495 to accelerate carbon dioxide conversion technologies that transform captured emissions into useful products. This program supports pilot-scale development in biological, catalytic, and mineralization pathways and thus presents a lucrative opportunity for the catalyst industry to grow in the country.

In Canada, the catalysts market is being supported by various factors, which include the intensive modernization within its oil sands operations, large-scale biomass conversion projects, and strict provincial environmental mandates. Meanwhile, industrial facilities utilize advanced hydrotreating and cracking catalysts to upgrade heavy crude bitumen into cleaner, low-sulfur transport fuels. Based on the government data published in January 2025, Canada’s Bitumen Beyond Combustion and Valorization program is focused highly on turning low-value oil sands by-products such as asphaltenes, petcoke, hydrogen sulfide (H₂S), and light hydrocarbons into higher-value materials instead of simply burning them for fuel. The data also mentions the key research areas, which include asphaltene valorization for use in carbon fibers, supercapacitors, and construction materials; petcoke conversion into advanced carbon and nanomaterials; and hydrogen production from unconventional petroleum sources to support lower-carbon refining processes, thus elevating the growth potential of the country’s market.

Europe Market Insights

Europe catalysts market is forecasted to witness significant expansion from 2026 to 2035. The region’s growth is mainly attributable to stringent decarbonization targets, strict industrial emission regulations, and a highly advanced specialty chemical sector. Also, the region's transition toward a circular economy is rapidly accelerating the deployment of specialized biocatalysts, green hydrogen electrolyser components, and advanced recycling catalysts for plastic circularity. For instance, in July 2025, the European Commission announced the launch of a Chemicals Industry Action Plan with the main goal of strengthening Europe’s chemical sector by improving competitiveness, innovation, and sustainability. This plan includes measures such as forming a Critical Chemical Alliance, boosting clean energy and decarbonization, which includes low-carbon hydrogen and carbon capture, and expanding support for circular and bio-based chemicals, chemical recycling, and industrial innovation funding.

Europe Export Statistics for Supported Nickel-Based Catalysts by Country in 2023

|

Partner |

Trade Value (1000 USD) |

Quantity (Kg) |

|

World |

476,996.48 |

22,147,600 |

|

U.S. |

83,448.54 |

5,537,750 |

|

Mexico |

57,600.45 |

1,727,120 |

|

China |

52,106.32 |

2,050,320 |

|

India |

36,855.73 |

2,122,470 |

|

Indonesia |

28,980.75 |

1,490,520 |

|

Turkey |

26,621.99 |

1,051,910 |

|

Korea, Rep. |

23,642.15 |

1,057,990 |

|

Brazil |

15,936.91 |

913,644 |

Source: WITS

Europe Titanium Oxides Exports by Country - 2023 Trade Value and Volume Breakdown

Source: WITS

As the region’s primary chemical manufacturing powerhouse, the market in Germany is being fueled mainly by stringent federal climate action laws and rapid industrial automation. In addition, massive corporate investments in power-to-X (PtX) test plants require highly specialized catalysts to convert captured carbon dioxide into synthetic kerosene, which also propel the market’s expansion. In October 2025, Evonik announced the launch of Noblyst® F, which is a new catalyst portfolio specifically designed for flow chemistry applications, aimed at improving efficiency and performance in continuous industrial processes. This product line includes precious metal catalysts on carbon supports, and it drives customization for applications in pharmaceuticals and fine chemicals manufacturing, thus making it suitable for standard market growth.

In the UK, the market is growing at a rapid pace of progress owing to the development of localized industrial carbon capture clusters, such as the Net Zero Teesside and HyNet projects, which require advanced solvent-purification and reforming catalysts. In addition, there has been a national push toward maritime decarbonization, which is accelerating the adoption of specialized catalysts for ammonia-to-hydrogen cracking and marine biofuel synthesis. In December 2024, the UK government signed contracts for its first major carbon capture, usage and storage projects in Teesside. This project is backed by about USD 27.6 billion in government support and is expected to unlock around USD 5.1 billion in supply chain contracts, thus heightening demand for suitable catalysts.

Key Catalysts Market Players:

- BASF (Germany)

- Johnson Matthey (UK)

- W. R. Grace & Co. (U.S.)

- Clariant (Switzerland)

- Haldor Topsoe (Denmark)

- Evonik Industries (Germany)

- Honeywell UOP (U.S.)

- Albemarle Corporation (U.S.)

- Sinopec Catalyst Company (China)

- Ketjen (U.S.)

- Saudi Aramco Technologies Company (Saudi Arabia)

- Zeolyst International (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF is one of the most dominant players in the global market that has a strong portfolio structured around refinery, chemical, and emission control solutions. The company benefits from its integrated R&D Verbund structure to accelerate innovation in fluid catalytic cracking, automotive catalysts, and sustainable process technologies.

- Johnson Matthey is yet another leading catalyst manufacturer that has a strong global presence in clean air, hydrogen, and process catalysts. The company is well recognized for its automotive emission control catalysts and expanding capabilities in sustainable technologies.

- W. R. Grace & Co. is a major catalyst supplier that is strong in refining catalysts, especially fluid catalytic cracking technologies. The firm is highly focused on improving refinery yield, operational efficiency, and feedstock flexibility through advanced zeolite-based catalyst systems.

- Clariant also holds a strong position in petrochemical and specialty catalysts, along with diversified offerings in syngas, emissions reduction, and sustainable chemistry applications. Besides, the company focuses on innovation in energy-efficient and low-emission catalytic processes.

- Haldor Topsoe is a technology-intensive catalyst company that specializes in refining, hydrogen production, and industrial decarbonization solutions. The firm is particularly strong in hydroprocessing, ammonia, and methanol catalysts and is supported by advanced process licensing capabilities.

Here is a list of key players operating in the global catalysts market:

The catalysts market is being dominated by a handful of multinational chemical and materials science companies, which benefit from strong proprietary technologies and extensive R&D capabilities. Competition in this field is mainly driven by product performance efficiency, emission reduction capabilities, and feedstock flexibility. Leading market participants differentiate themselves through advanced zeolite systems, precious metal catalysts, and process optimization solutions. The global leaders have been maintaining a strong cross-regional presence, whereas several specialized players compete in niche segments such as emission control and sustainable fuel catalysts. In January 2026, Technip Energies completed the acquisition of Ecovyst’s Advanced Materials & Catalysts (AM&C) business to strengthen its position in advanced catalyst technologies. This acquisition enhances its portfolio in terms of sustainable fuels, circular chemistry, and carbon capture.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, BASF inaugurated a new R&D center for refinery catalysts in Attapulgus, Georgia, which is strategically located at its largest global production site. The facility focuses on advanced fluid catalytic cracking catalyst development, and it enables faster innovation cycles and improved process efficiency.

- In April 2026, Evonik announced the launch of a new generation of high-performance isodewaxing catalysts, which are designed to improve fuel and lubricants production efficiency. The catalysts were developed using Zeopore’s mesoporized zeolite technology, and they enhance product yields, improve cold-flow properties, and reduce CO₂ emissions.

- In March 2026, Ketjen and Saudi Aramco Technologies Company signed a joint agreement to co-develop next-generation FCC catalysts and additives, which are aimed at improving refinery efficiency and reducing environmental impact. This particular collaboration focuses on increasing yields of high-value fuels such as gasoline and propylene.

- Report ID: 8655

- Published Date: Jul 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.