Cardiac Valve Market Outlook:

Cardiac Valve Market size was over USD 14.4 billion in 2025 and is anticipated to exceed USD 43.9 billion by the end of 2035, growing at over 11.8% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of cardiac valve is assessed at USD 16.1 billion.

The cardiac valve market is being shaped by the growing burden of structural heart disease, population aging, and expanding treatment volumes across developed and emerging healthcare systems. According to the NLM November 2023 study, heart disease was responsible for 702,880 deaths in the U.S., remaining the leading cause of mortality and sustaining demand for cardiovascular diagnostic and interventional services. In parallel, the CDC January 2026 data reports that valvular heart disease affects approximately 2.5% of the U.S. population, with prevalence increasing significantly among older adults. Demographic trends further reinforce long-term demand. These factors are creating a stable demand environment for cardiac valve-related interventions, clinical services, and associated healthcare infrastructure.

From a healthcare system perspective, investment in cardiovascular care remains substantial. The NLM April 2026 study estimates that the total economic burden of cardiovascular disease in the United States exceeded USD 400 billion annually when healthcare expenditures and productivity losses are combined. At the same time, government-supported research continues to advance the clinical evidence base for structural heart interventions. Market activity is also influenced by hospital modernization programs, workforce training initiatives, and efforts to reduce cardiovascular mortality through earlier intervention and improved treatment accessibility, creating a favorable environment for continued growth in cardiac valve-related healthcare services.

Key Cardiac Valve Market Insights Summary:

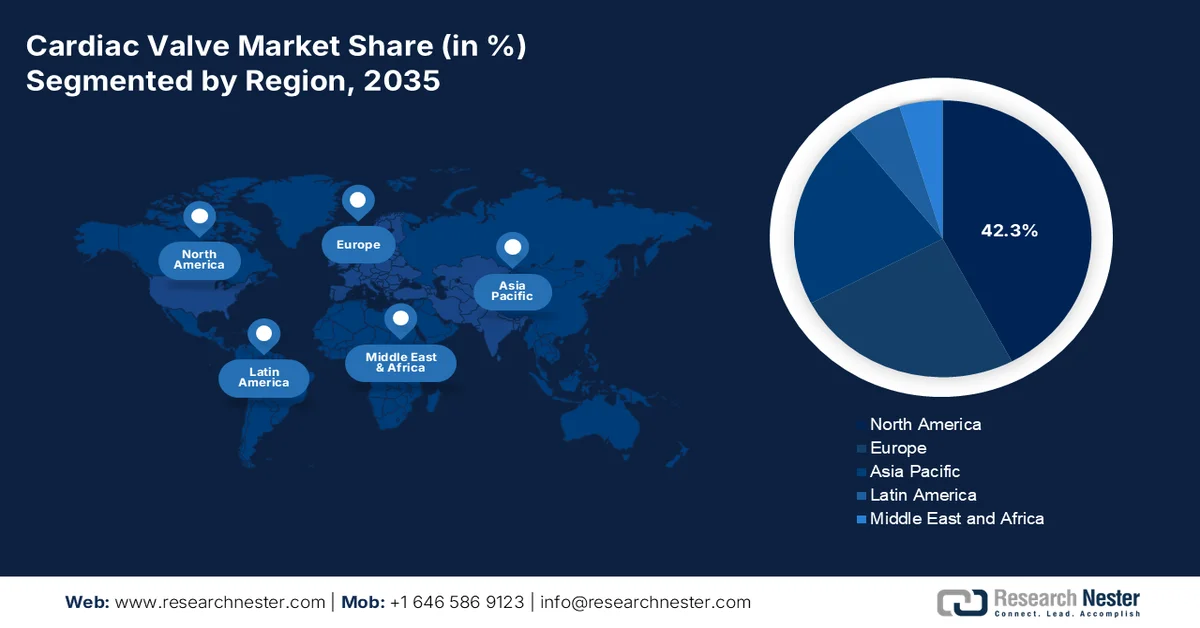

Regional Highlights:

- North America is anticipated to secure 42.3% of the cardiac valve market share by 2035, bolstered by well-established healthcare infrastructure, early adoption of cutting-edge transcatheter technologies, and a strong presence of leading device manufacturers

- Asia Pacific is expected to witness the fastest expansion throughout 2026-2035, fueled by rapid urbanization, rising healthcare expenditure, and increasing awareness of valvular heart disease

Segment Insights:

- The transcatheter heart valves segment is projected to capture 43.2% of the cardiac valve market share by 2035, propelled by expanded FDA approvals for low-risk and asymptomatic patients

- The cardiac valve replacement segment is expected to experience notable growth during 2026-2035, supported by the increasing adoption of minimally invasive and transcatheter techniques

Key Growth Trends:

- Rising government expenditure on cardiovascular disease management

- Rising aging population

Major Challenges:

- Stringent regulatory approvals

- High R&D & clinical trial costs

Key Players: Edwards Lifesciences (U.S.),Medtronic (U.S.),Abbott (U.S.),Boston Scientific (U.S.),LivaNova (UK),CryoLife (U.S.).

Global Cardiac Valve Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 14.4 billion

- 2026 Market Size: USD 16.1 billion

- Projected Market Size: USD 43.9 billion by 2035

- Growth Forecasts: 11.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, China, South Korea, Indonesia, Malaysia

Last updated on : 7 July, 2026

Cardiac Valve Market - Growth Drivers and Challenges

Growth Drivers

- Rising government expenditure on cardiovascular disease management: Government healthcare spending on cardiovascular diseases is a major demand driver for the cardiac valve market because valvular heart disease diagnosis and treatment are typically delivered through publicly funded hospital systems. In the U.S., the AMA April 2025 data reported national health expenditures of approximately USD 4.9 trillion in 2023, representing 17.6% of GDP. A significant portion of this expenditure supports cardiovascular care, including valve replacement procedures and post-operative management. Public investments also enable hospitals to acquire specialized imaging systems, hybrid operating rooms, and structural heart programs needed for valve procedures. These funding mechanisms reduce treatment barriers and encourage earlier intervention, supporting long-term procedural growth.

- Rising aging population: Population aging is a primary structural driver because degenerative valve disorders increase substantially among older adults. According to the PRB January 2024 data, the number of Americans aged 65 and older is projected to exceed 82 million by 2050. Older populations require more echocardiography screenings, surgical valve replacements, and transcatheter valve interventions. Governments are responding through expanded geriatric healthcare funding and long-term care programs. Public reimbursement systems increasingly prioritize cardiovascular disease management to reduce disability and hospital readmissions among elderly populations. This demographic shift creates sustained demand for cardiac valve procedures across North America, Europe, Japan, and other aging economies.

Challenges

- Stringent regulatory approvals: Navigating FDA and CE Mark approvals demands extensive clinical trials with long-term durability data. The rigorous premarket review process delays market entry by 3–5 years. Companies must invest in large-scale randomized controlled trials to demonstrate safety and efficacy. Smaller firms struggle with the financial and administrative burden of global regulatory submissions across multiple jurisdictions simultaneously.

- High R&D & clinical trial costs: Developing next-generation valves requires substantial investment in biomaterials, computational modeling, and animal studies. Clinical trials involve hundreds of patients with multi-year follow-up, costing upwards of tens of millions. Startups often lack capital to complete pivotal trials, forcing partnerships with larger incumbents or venture capital to sustain product development pipelines.

Cardiac Valve Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.8% |

|

Base Year Market Size (2025) |

USD 14.4 billion |

|

Forecast Year Market Size (2035) |

USD 43.9 billion |

|

Regional Scope |

|

Cardiac Valve Market Segmentation:

Type Segment Analysis

Under the type segment, the transcatheter heart valves are leading in the cardiac valve market and is poised to hold the share value of 43.2% by the end of 2035. The segment is driven by the expanded FDA approvals for low-risk and asymptomatic patients. Continuous innovations in delivery systems, anti-calcification tissue treatments, and commissural alignment have enhanced long-term durability, now projected beyond 10 years. The clinical shift from surgical aortic valve replacement to TAVR has been dramatic, TAVR is use for most of the aortic valve procedures in the U.S. According to the NLM January 2024 study TAVR implant volumes surged by 22%, cementing its leadership in the market.

Treatment Segment Analysis

Cardiac valve replacement is the definitive treatment for severe valvular dysfunction caused by congenital defects, degenerative calcification, or rheumatic heart disease. The procedure involves excising the diseased native valve and implanting a mechanical or bioprosthetic substitute to restore unidirectional blood flow and relieve cardiac pressure overload. Replacement is indicated when valve repair is anatomically infeasible or when stenosis or regurgitation leads to symptomatic heart failure or ventricular dysfunction. Prosthesis choice depends on patient age, lifestyle, and anticoagulation tolerance. Traditionally performed via open-heart surgery, replacement has evolved with minimally invasive and transcatheter techniques, expanding eligibility to high-risk patients. Lifelong follow-up is essential due to risks of thrombus, valve deterioration, endocarditis, and patient-prosthesis mismatch, yet replacement significantly improves survival and quality of life.

Valve Segment Analysis

The aortic valve dominates the valve segment due to the high prevalence of degenerative and congenital pathologies. Its thin leaflets endure extreme hemodynamic forces each cardiac cycle, yet age-related calcification and congenital defects most commonly bicuspid aortic valve (BAV), affecting 1% to 2% of the population with male predominance compromise function, leading to stenosis or regurgitation, as per NLM May 2023 study. BAV frequently correlates with aortic dilation and coarctation, with accelerated calcific degeneration from abnormal flow dynamics. These complications often remain asymptomatic until age 50 to 60, but severe disease necessitates intervention. With BAV-associated infective endocarditis incidence at 12% to 39%, the aortic position drives over 58% of global valve procedures, cementing its market leadership.

Our in-depth analysis of the cardiac valve market includes the following segments:

|

Segment |

Subsegments |

|

Treatment |

|

|

Type |

|

|

Valve |

|

|

End user |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cardiac Valve Market - Regional Analysis

North America Market Insights

North America is dominating the cardiac valve market and is projected to hold the regional revenue share of 42.3% by the end of 2035. The region is driven by the well-established healthcare infrastructure, early adoption of cutting-edge transcatheter technologies, and a strong presence of leading device manufacturers. The region benefits from robust clinical research ecosystems, extensive physician training programs, and collaborative registries that continuously improve patient outcomes. Favorable reimbursement frameworks and clinical guidelines support the expanding use of minimally invasive valve replacement and repair procedures across diverse patient populations. The market is characterized by intense competition, with incumbents and emerging players investing heavily in next-generation platforms, including polymer valves, sutureless designs, and transcatheter mitral/tricuspid solutions.

The underdiagnosed patient population requiring ongoing cardiovascular care is shaping the cardiac valve market in the U.S. According to the Centers for Disease Control and Prevention (CDC) January 2026 data, heart valve disease affects certain percentage of the U.S. adult population, while more than 28,000 deaths annually are attributed to the condition. The disease burden is expected to increase as the population ages, particularly among adults aged 65 years and older who face the highest risk of valvular disorders. Diagnosis and treatment gaps remain evident among African American, Hispanic, and Asian populations, while women are more likely to experience delayed diagnosis and poorer outcomes. These factors are increasing demand for screening, diagnostic imaging, and valve intervention procedures across U.S. healthcare systems.

The substantial cardiovascular disease burden and increasing demand for specialized cardiac interventions is shaping the market in Canada. According to the Government of Canada July 2022 report, approximately 2.6 million Canada adults (about 1 in 12 people aged 20 years and older) are living with diagnosed heart disease, creating a large population requiring ongoing cardiac assessment and treatment. In addition, Government of Canada February 2022 data reported 53,704 deaths from heart diseases, making cardiovascular conditions one of the leading causes of mortality nationwide. The continued prevalence of cardiac disorders is driving demand for echocardiography services, structural heart programs, and valve repair and replacement procedures across major Canada healthcare institutions.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the cardiac valve market. the region is rapid urbanization, rising healthcare expenditure, and increasing awareness of valvular heart disease. The region presents a unique dichotomy, with developed nations like Japan, Australia, and South Korea exhibiting mature adoption of transcatheter technologies, while emerging economies such as India, China, Indonesia, and Malaysia are witnessing surging demand for cost-effective surgical and transcatheter solutions. Local manufacturers are gaining prominence by offering affordable alternatives to global brands, intensifying price competition. Expanding cardiac care infrastructure, growing medical tourism, and government-led screening initiatives are improving access to valve interventions.

The high cardiovascular disease burden and expanding access to advanced cardiac treatment services is shaping the cardiac valve market in India. According to the NLM June 2024 study, cardiovascular diseases accounted for approximately 28.1% of all deaths in India, underscoring the large patient pool requiring long-term cardiac care and intervention. In addition, the AMA May 2024 data reported that more than 8.6 million cardiac-related treatment authorizations had been approved under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) since program inception, reflecting increasing utilization of cardiovascular services across the country. Rising detection of structural heart conditions, improved referral networks, and broader access to specialized cardiac centers are supporting demand for cardiac valve diagnosis, repair, and replacement procedures.

The large cardiovascular disease burden and increasing procedural capacity within tertiary hospitals is driving the cardiac valve market in China. According to the NLM June 2023 study, cardiovascular diseases affect approximately 330 million people nationwide, making them the leading cause of death and creating a substantial patient base requiring diagnostic and interventional cardiac care. Additionally, the ManuLife September 2025 data reported China had more than 38,000 hospitals operating across the country, reflecting continued expansion of healthcare infrastructure capable of supporting complex cardiac procedures. The combination of a large cardiovascular patient population, improving hospital capabilities, and greater access to specialized heart centers is driving demand for cardiac valve diagnostics, repair procedures, and replacement interventions throughout China.

Europe Market Insights

Europe represents a highly sophisticated and well-regulated cardiac valve market, characterized by strong clinical research traditions, early adoption of transcatheter technologies, and a dense network of high-volume structural heart centers. The region benefits from harmonized regulatory frameworks through the Medical Device Regulation (MDR), ensuring rigorous safety and performance standards for all valve devices. Leading manufacturers maintain significant R&D and manufacturing footprints across Germany, France, Italy, and the UK, fostering continuous innovation in surgical and transcatheter platforms. The market is shaped by aging populations, proactive cardiovascular screening programs, and strong professional societies that publish evidence-based guidelines. However, price sensitivity varies across countries, with national health systems negotiating stringent reimbursement packages.

The high burden of cardiovascular disease and strong utilization of specialized cardiac services is driving the cardiac valve market in Germany. According to the ESMED September 2025 data, diseases of the circulatory system were responsible for approximately 358,219 deaths, remaining the leading cause of death nationwide. In addition, Destatis February 2023 data reported that Germany hospitals treated more than 1.44 million inpatient cases related to circulatory system diseases, highlighting the substantial volume of patients requiring cardiovascular diagnosis, monitoring, and intervention. This large clinical workload supports demand for advanced cardiac imaging, structural heart programs, and valve repair and replacement procedures, particularly within Germany’s network of specialized hospitals and university medical centers.

The significant cardiovascular disease burden and growing utilization of specialized cardiac care services is driving the cardiac valve market in the UK. According to the UK Government July 2025 data, cardiovascular diseases accounted for approximately 155,000 deaths in England and Wales in 2023, maintaining their position among the leading causes of mortality. Furthermore, NHS England's November 2025 data Diagnostic Imaging Dataset for 2024 reported more than 49.9 million imaging tests conducted annually, including large volumes of echocardiography and cardiac imaging procedures that support the detection and management of valvular heart conditions. Increasing identification of structural heart disease, combined with established referral pathways to specialist cardiac centers, is supporting demand for cardiac valve diagnostics, repair procedures, and replacement interventions across the UK healthcare system.

Key Cardiac Valve Market Players:

- Edwards Lifesciences (U.S.)

- Medtronic (U.S.)

- Abbott (U.S.)

- Boston Scientific (U.S.)

- LivaNova (UK)

- CryoLife (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Edwards Lifesciences remains the undisputed leader in the global cardiac valve market, driven by its pioneering SAPIEN transcatheter aortic valve replacement (TAVR) franchise. The company’s strategic initiatives focus on expanding TAVR indications to low-risk and asymptomatic patients, while aggressively investing in next-generation valves with improved durability and commissural alignment.

- Medtronic competes fiercely in the cardiac valve market with its CoreValve/Evolut TAVR platform, emphasizing supra-annular leaflet design and long-term hemodynamic performance. The company’s key strategic initiative is the "Structural Heart & Aortic" division’s focus on product lifecycle management, including the Evolut FX+ system, which offers enhanced deliverability and coronary access.

- Abbott has carved a differentiated niche in the cardiac valve market through its leadership in transcatheter mitral and tricuspid therapies, anchored by the MitraClip and TriClip systems, alongside its surgical and TAVR portfolios (Portico and Navitor).

- Boston Scientific is a formidable contender in the cardiac valve market, primarily through its ACURATE neo2 TAVR platform, which features a self-expanding, supra-annular design with active PV sealing to reduce paravalvular leak.

- LivaNova maintains a steady, specialized presence in the cardiac valve market, concentrating on mechanical and bioprosthetic surgical valves, particularly its Perceval sutureless valve, which reduces cross-clamp times in minimally invasive aortic surgeries.

Here is a list of key players operating in the global cardiac valve market:

The cardiac valve market is highly consolidated, with Edwards and Medtronic dominating surgical and TAVR segments through continuous innovation and expansive clinical trials. Strategic initiatives focus on next-generation transcatheter technologies, durability enhancements, and minimally invasive delivery systems. Key players aggressively pursue regulatory approvals, geographic expansion, and acquisitions. Indian manufacturers like Meril and Sahajanand compete on cost-effective devices for emerging markets, while European firms emphasize premium precision. Competitive differentiation increasingly relies on real-world evidence, digital health integration, and partnerships with interventional cardiologists to accelerate adoption and shorten hospital stays.

Corporate Landscape of the Market:

Recent Developments

- In December 2025, Edwards Lifesciences announced the company’s SAPIEN M3 mitral valve replacement system is the first transcatheter therapy utilizing a transseptal approach to receive U.S. Food and Drug Administration (FDA) approval for the treatment of mitral regurgitation (MR).

- In September 2025, Medtronic announced the launch of its new transcatheter aortic valve, Evolut™ FX+, in India. The valve is designed to help improve treatment for patients with severe aortic stenosis, especially those who may need future coronary procedures.

- In January 2025, Abbott announced the launch of Navitor Vision in India for the treatment of patients with symptomatic severe aortic stenosis who are at high or extreme surgical risk. The device is the latest iteration of the company’s Navitor transcatheter aortic valve implantation/replacement (TAVI/TAVR) system.

- Report ID: 8654

- Published Date: Jul 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.