Business Cloud Storage Market Outlook:

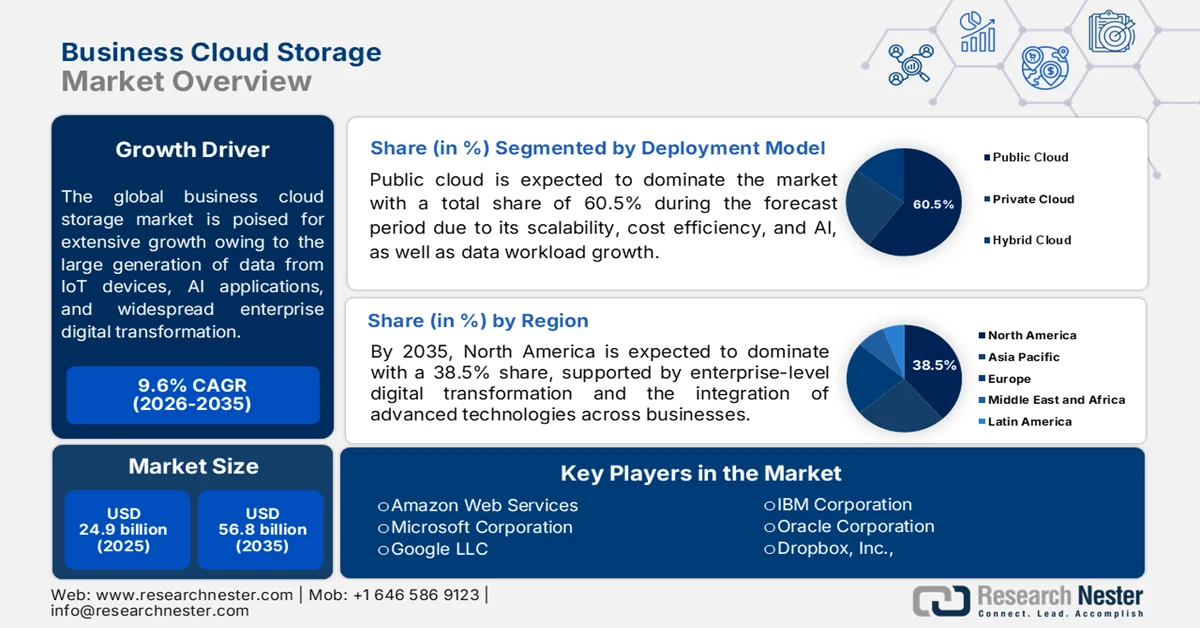

Business Cloud Storage Market size was valued at USD 24.9 billion in 2025 and is expected to reach USD 56.8 billion by 2035, growing at a CAGR of 9.6% during the forecast period, 2026-2035. In 2026, the industry size of business cloud storage is assessed at USD 27.2 billion.

The exponential generation of data from IoT devices, AI applications, and widespread enterprise digital transformation are the main factors behind the robust growth of the business cloud storage market. The clear movement towards hybrid and multi-cloud architectures is a visible trend in the global market. As per an article published by the National Institute of Health (NIH) in October 2023, global data generation has reached the zettabyte scale, wherein the daily generation is considered to be 400+ million TB per day owing to the rapid digitalization, streaming, and AI systems. The study shows that major contributors include large platforms, cloud services, and scientific infrastructures, wherein organizations such as CERN alone generate hundreds of petabytes per year, comparable in scale to big tech data flows. It also emphasizes that data streaming, i.e., video, email, IoT, and scientific transfers already form a dominant share of global data production, thus positively impacting the market’s upliftment.

Furthermore, the integration of artificial intelligence is revolutionizing the market with the presence of automated storage tiering and intelligent data classification, which remarkably enhances operational efficiency. Also, there has been a strong focus on sustainability that is influencing vendor selection, with businesses prioritizing providers that offer energy-efficient green data centers as well as transparent carbon-impact reporting. In February 2024, Microsoft introduced new data and AI solutions in its cloud for sustainability, with the main goal to help organizations accelerate ESG progress. Besides, it states that companies can unify data, automate reporting, and identify reduction opportunities more efficiently with Microsoft Fabric, Copilot in Sustainability Manager, and intelligent insights. These innovations, along with ESG value chain solutions, strengthen businesses with measurable sustainability outcomes, thus benefiting the overall market growth.

Key Business Cloud Storage Market Insights Summary:

Regional Highlights:

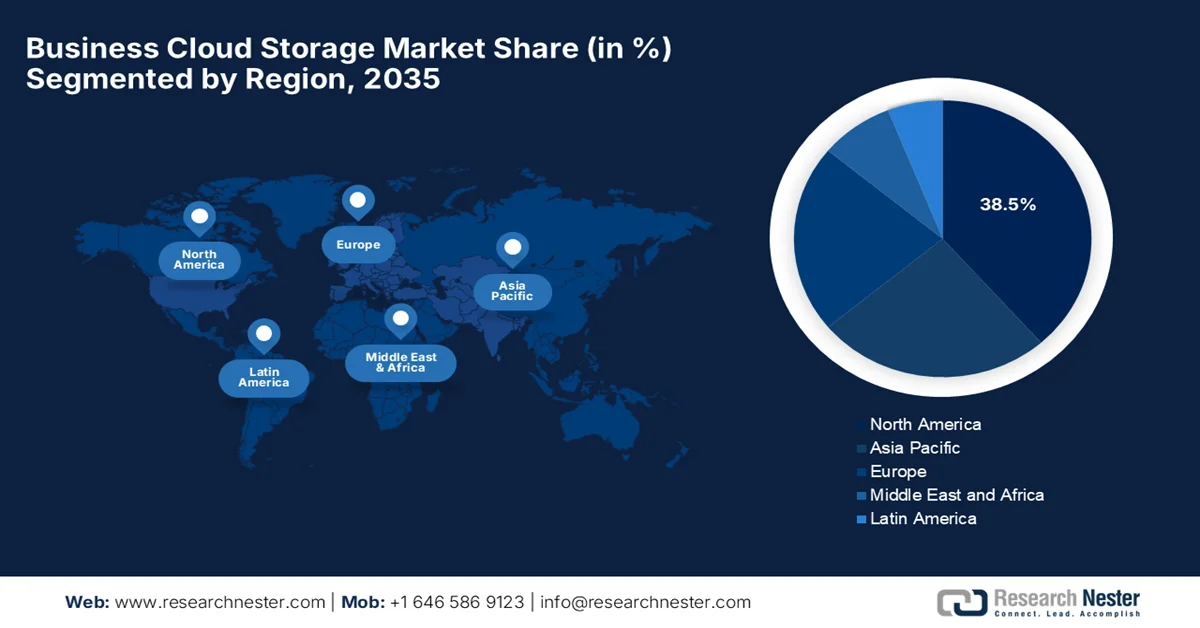

- North America is projected to account for a 38.5% share of the business cloud storage market by 2035, fueled by accelerating enterprise digital transformation initiatives and rising demand for secure, scalable data storage solutions

- Asia Pacific is expected to witness robust expansion in the forecast period 2026-2035, stimulated by rapid growth of mobile-first digital economies and supportive government cloud-first policies

Segment Insights:

- Public cloud segment is anticipated to hold a dominant 60.5% share of the business cloud storage market by 2035, propelled by its scalability, cost efficiency, and rising AI-driven data workload growth

- Large enterprise segment is set to capture a considerable share by 2035, driven by increasing data volumes, stringent compliance requirements, and growing adoption of multi-cloud strategies

Key Growth Trends:

- Digital transformation across industries

- Remote work and distributed workforce adoption

Major Challenges:

- High costs and infrastructure complexity

- Data migration and integration issues

Key Players: Amazon Web Services (AWS) (U.S.), Microsoft Corporation (U.S.), Google LLC (U.S.), IBM Corporation (U.S.), Oracle Corporation (U.S.), Dropbox, Inc. (U.S.), Box, Inc. (U.S.), Hewlett Packard Enterprise (U.S.), Dell Technologies (U.S.), Wasabi Technologies (U.S.), NetApp (U.S.), Lenovo (China), Infinidat (Israel), GB Labs (UK), Wasabi Technologies (U.S.), Seagate (U.S.), Scality SA (France).

Global Business Cloud Storage Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 24.9 billion

- 2026 Market Size: USD 27.2 billion

- Projected Market Size: USD 56.8 billion by 2035

- Growth Forecasts: 9.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Brazil, United Arab Emirates

Last updated on : 30 April, 2026

Business Cloud Storage Market - Growth Drivers and Challenges

Growth Drivers

- Digital transformation across industries: Organizations across sectors, i.e., BFSI, healthcare, retail, and manufacturing, are digitizing operations and moving workloads to the cloud. This aspect readily drives growth in the business cloud storage market. As per an NIH article published in February 2023, digital transformation in healthcare is being effectively driven by rapid technological innovation such as IoT, AI, cloud computing, wearable devices, and telemedicine, which enable more efficient and patient-centric care delivery. At the same time, the growing volume of healthcare data and the need for improved data storage, processing, and security are also accelerating the adoption of digital health systems. In addition, the rising demand for personalized healthcare, remote monitoring, and improved patient participation is reshaping traditional healthcare models, thus making it suitable for bolstering the overall market’s growth.

- Remote work and distributed workforce adoption: There is an exponential surge in remote work opportunities, which necessitates proper access to files from anywhere. In this context, cloud emerges as a reliable solution since it enables real-time collaboration and data sharing across geographies, making it a core enterprise productivity tool. In January 2024, the article published by the World Economic Forum revealed that the rise of global digital jobs means that an increasing number of work tasks can now be performed entirely online. It underscores that by 2030, such roles are expected to rise by around 25% to more than 92 million jobs, especially in fields such as software development, finance, design, and customer service. Hence, this shift creates new opportunities for workers to access a wider range of jobs globally, thereby contributing to the market expansion.

- Cost efficiency and reduced IT infrastructure burden: The solutions from the market reduce the overall expenses in terms of physical hardware and remarkably lower maintenance costs. The pricing models, such as pay-as-you-go and elastic scaling, are making it attractive for both large enterprises and SMEs, thereby increasing adoption. In this context, NIH in May 2023 stated that cost reduction is a key driver of cloud computing integration in SMEs, whereas these cloud services help firms reduce upfront infrastructure investment and ongoing maintenance costs. In addition, the study also underscores that cloud adoption reduces the overall need for internal servers, software installation, and system maintenance, effectively lowering overall IT operational burden and improving efficiency. Moreover, it concludes that SMEs can reallocate saved resources for core business activities, hence denoting an optimistic market opportunity.

Challenges

- High costs and infrastructure complexity: The cost of cloud storage can escalate as enterprises scale their data utilization rates, making unpredictability of pricing a major challenge for the business cloud storage market. The cloud models reduce upfront infrastructure investment, but long-term storage, data transfer, and retrieval costs can become substantial, making it burdensome for small-scale operators in the industry. Therefore, businesses often struggle with optimizing workloads across multiple providers to control expenses. Apart from this, companies such as Oracle Corporation and other hyperscalers offer tiered pricing models, but complexity in billing structures leads to cost management difficulties. In addition, integrating cloud storage with legacy systems increases operational complexity, thereby negatively impacting the market’s growth and exposure.

- Data migration and integration issues: Migrating large volumes of enterprise data from on-premises systems to cloud environments is a major obstacle for the upliftment of the market. Data migration is sometimes time-consuming, expensive, and prone to disruption, especially for organizations that have old or aging infrastructure. Compatibility issues between different cloud platforms intensely complicate integration in multi-cloud environments. Enterprises using solutions from prominent architectures need to ensure seamless interoperability between systems. The aspect of improper or poor migration planning can result in downtime and even data loss. In addition, integration of cloud storage with existing enterprise applications necessitates technical knowledge and careful architecture design, making digital transformation efforts ultimately slower for many organizations.

Business Cloud Storage Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.6% |

|

Base Year Market Size (2025) |

USD 24.9 billion |

|

Forecast Year Market Size (2035) |

USD 56.8 billion |

|

Regional Scope |

|

Business Cloud Storage Market Segmentation:

Deployment Model Segment Analysis

Public cloud is expected to dominate the entire business cloud storage market with a total share of 60.5% during the forecast period. The segment’s dominance is largely propelled by its scalability, cost efficiency, and AI, as well as data workload growth. There has been an increasing enterprise migration to cloud platforms owing to the digital transformation and data-intensive applications. In April 2026, Google Cloud announced the expansion of its agentic enterprise ecosystem with a total of USD 750 million innovation fund to accelerate AI agent development across industries. This initiative is highly focused on enabling partners such as Accenture, Deloitte, SAP, Salesforce, and others to build and deploy enterprise AI agents using the Gemini Enterprise Agent Platform, supporting automation across business processes. Such instances raise the adoption of public cloud infrastructure, as organizations are dependent on Google Cloud’s scalable AI and data platforms for large-scale digital transformation.

Organization Size Segment Analysis

Large enterprise in the organization size category is anticipated to grow with a considerable revenue share in the business cloud storage market by the end of 2035. The growth of the segment is largely attributable to high data volumes, compliance needs, and multi-cloud strategies. The large firms adopt cloud at significantly higher rates due to advanced IT budgets and cybersecurity requirements. These companies also make heavy investments in hybrid and distributed cloud architectures, thereby boosting storage demand. Apart from these factors, large enterprises are prioritizing cloud storage to manage massive and continuously growing datasets generated from AI, analytics, and global operations. Their adoption of multi-cloud and hybrid environments is also driven by the need to avoid vendor lock-in while ensuring high availability and resilience, thus denoting a wider segment scope.

Industry Vertical Segment Analysis

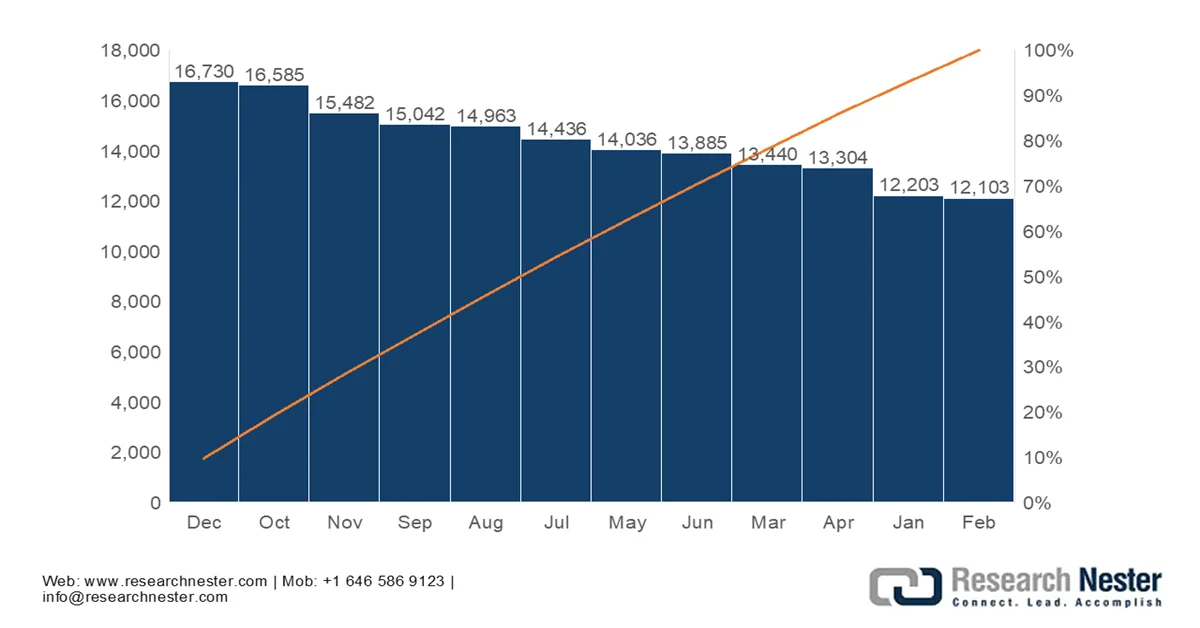

By the conclusion of 2035, BFSI, which is under the industry vertical segment, is predicted to grow with a considerable revenue share in the market. Data sensitivity, regulatory requirements, and digital banking expansion are the main factors behind the segment’s leadership. The continued surge in digital financial services worldwide is readily increasing data storage needs, positioning the segment as the gold standard of revenue generation in this field. In this context, an article published by Press Information Bureau (PIB) in January 2025 stated that India’s rapid expansion in digital transactions reflects a strong shift toward a cashless economy, influenced by the presence of platforms such as UPI, IMPS, and NETC FASTag. At the same time, it mentioned that UPI processed around 16.73 billion transactions in December 2024, reflecting a massive nationwide adoption and deep penetration across consumers, merchants, and small businesses, positively contributing to the segment’s expansion.

Monthly UPI Transaction Volume in India (2024): NPCI Official Data in Millions

Source: PIB

Our in-depth analysis of the business cloud storage market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Model |

|

|

Organization Size |

|

|

Industry Vertical |

|

|

Storage Type |

|

|

Service Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Business Cloud Storage Market - Regional Analysis

North America Market Insights

The North America business cloud storage market is anticipated to lead with the largest share of 38.5% during the stipulated timeframe. The region’s dominance is mainly propelled by enterprises that are opting for advanced technologies and accelerating digital transformation initiatives. This factor is driving strong demand for scalable, efficient, and secure storage solutions to effectively manage growing data volumes with a primary focus on reliability and data protection. In this context, the U.S. Department of the Treasury in February 2023 reported that there has been a growing adoption of cloud-based technologies in the financial sector, driven by the need for improved access, reliability, and operational efficiency. In addition, it stated that financial institutions are making a shift to cloud platforms with a main goal to enhance scalability and strengthen service delivery, at the same time enabling smaller banks to compete more effectively with fintech firms.

The rising adoption of artificial intelligence and machine learning technologies, which necessitate high-performance infrastructure for processing massive datasets, is the main factor driving the business cloud storage market in the U.S. The country’s market is also bolstered by a strong focus on data sovereignty and the presence of major domestic hyperscalers who continue to expand their regional data center footprints. In July 2023, the article published by the Centers for Strategic Studies & International Studies stated that accelerating federal cloud adoption is highly essential for modernizing U.S. government IT systems, with the main goal of improving security and reducing costs by replacing decades-old legacy infrastructure with scalable cloud-based solutions. Apart from this, it emphasizes that cloud computing enhances efficiency, resilience, and service delivery at the same time, enabling agencies to better manage cybersecurity risks and operational demands.

In Canada, the business cloud storage market is growing remarkably owing to the movement toward a sovereign cloud model, which has led major global hyperscalers to expand their physical footprints with new data centers to ensure data residency. At the same time, the federal government's cloud-first strategy and the rapid digital transformation of small and medium-sized enterprises also propel continued growth in the country’s market. Based on the government data published in October 2025, its cloud adoption strategy proactively promotes a cloud-first approach, prioritizing public cloud to modernize IT services, improve scalability, security, and efficiency, and better meet growing digital service demands across departments. It supports a hybrid model where public, private, and non-cloud systems are used based on data sensitivity and operational needs, thereby enabling innovation and on-demand resource provisioning, thus suitable for standard market growth.

APAC Market Insights

The market in the Asia Pacific is being propelled by a massive surge in mobile-first digital economies and the rapid expansion of e-commerce and fintech sectors. Apart from these, governments across the region are fueling this growth through cloud-first mandates and national digitalization programs, which in turn encourage enterprises to modernize legacy IT infrastructure. In this context, the Asia Development Bank Institute in January 2024 reported that government policies promoting cloud adoption in the region readily enhance economic performance by improving public sector efficiency and generating positive spillover effects across industries. The article also underscored that in 2023, cloud computing contributed between 0.25% and 2.23% of GDP in economies such as India, Japan, Singapore, and others, wherein a greater impact was observed in countries that witnessed higher cloud penetration supported by enabling government policies.

The government's backing for technological self-reliance is responsibly uplifting the market in China. In addition, the integration of 5G-edge computing and the rise of autonomous AI agents are fostering a new ecosystem of real-time, data-intensive applications across smart factories and urban infrastructure. Based on the government data published in November 2023, the country’s digital economy strategy is readily accelerating the growth of the cloud computing industry, owing to the strong government support, advanced telecom infrastructure, and large-scale adoption of computing power across industries. The industry is reflecting rapid expansion fueled by applications such as AI, virtual reality, and intelligent driving. Overall, the development of computing power infrastructure, including widespread 5G deployment and national digital policy initiatives, is enabling large-scale cloud adoption and thus strengthening the country’s position in the cloud storage category.

In India, the business cloud storage market is witnessing exponential growth owing to the digital transformation of its sprawling small and medium enterprise sector and a startup ecosystem that prioritizes cloud-native architectures for scalability. A pivotal factor escalating the country’s market is the government's push for data localization, which necessitates that sensitive financial and personal data be stored within domestic borders. PIB article in February 2026 revealed that the country’s union budget 2026-27 introduced a major policy push to position India as a global hub for cloud and AI infrastructure by offering a tax holiday till 2047 for eligible foreign cloud service providers using India-based data centers. This framework is especially designed to attract large-scale, capital-intensive investments in data centers, supported by continued taxation of domestic operations, thus indicating an optimistic opportunity for the market’s growth.

Europe Market Insights

The market in Europe is being reshaped by a stringent regulatory environment and a strong emphasis on digital sovereignty. In the region, the General Data Protection Regulation is acting as a primary catalyst for secure, localized storage solutions. This focus on privacy has led to the rise of specialized regional providers and collaborative projects that aim to build a transparent and interoperable data ecosystem. Based on the March 2026 published government data, the region aims to strengthen secure, sustainable, and interoperable cloud and edge computing infrastructures to support businesses and public authorities, with a major shift toward processing data closer to users through edge computing. By the end of 2030, the region has set a target of 75% enterprise cloud adoption and the deployment of 10,000 highly secure edge nodes, along with expanding data centre capacity to meet growing data demands, thus increasing the demand for interoperable storage solutions.

The rigorous commitment to data privacy and digital sovereignty is a certain driver behind the robust growth of the market in Germany. The country’s enterprises, especially within the automotive manufacturing sector, are opting for sovereign cloud solutions that guarantee data residency within national borders to protect high-value intellectual property. In March 2025, the country’s government announced the launch of Germany’s government cloud (Deutsche Verwaltungscloud, DVC), which effectively strengthens digital sovereignty by offering secure, standardised multi-cloud services for public administration with open standards and interoperability. It enables agencies to easily procure and scale cloud solutions, thereby avoiding vendor lock-in through a multi-cloud, open-standards architecture. It consolidates demand across federal and state systems, and strengthens bargaining power and promotes joint procurement and economies of scale for cloud services, thus suitable for standard market growth.

The business cloud storage market in the UK is poised for solid growth in the next decade, primarily fueled by the cloud-first government procurement policy, nationwide 5G roll-outs, and massive investment in hyperscale data centers. The country’s market is also being reshaped by the surge in generative AI and IoT workloads, which necessitate high-throughput storage solutions along with advanced data analytics capabilities. In September 2024, Amazon Web Services announced an almost USD 10 billion investment in UK data centres to expand cloud infrastructure and support rising AI and digital workloads across businesses and public sector users. The company also notes that this investment will contribute about USD 17.5 billion to UK GDP and sustain over 14,000 jobs annually, reinforcing large-scale cloud capacity growth. Therefore, this real-world expansion of hyperscale cloud infrastructure directly strengthens demand for high-performance storage.

Key Business Cloud Storage Market Players:

- Amazon Web Services (AWS) (U.S.)

- Microsoft Corporation (U.S.)

- Google LLC (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Dropbox, Inc. (U.S.)

- Box, Inc. (U.S.)

- Hewlett Packard Enterprise (U.S.)

- Dell Technologies (U.S.)

- Wasabi Technologies (U.S.)

- NetApp (U.S.)

- Lenovo (China)

- Infinidat (Israel)

- GB Labs (UK)

- Wasabi Technologies (U.S.)

- Seagate (U.S.)

- Scality SA (France)

- OVHcloud (France)

- SAP SE (Germany)

- Telefónica S.A. (Spain)

- Fujitsu Limited (Japan)

- NEC Corporation (Japan)

- Hitachi Vantara (Japan)

- Samsung SDS Co., Ltd. (South Korea)

- Zoho Corporation Pvt. Ltd. (India)

- Axiata Group Berhad (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Amazon Web Services is the foundational leader in the market, which is offering highly scalable and secure storage solutions such as Amazon S3, Glacier, and Elastic Block Store. The company’s leadership arises from its extensive global infrastructure, vast service ecosystem, and deep integration with analytics, AI, and machine learning tools.

- Microsoft Corporation is yet another major competitor in the market that benefits through its Azure platform and services such as Azure Blob Storage and OneDrive for Business. Besides, the firm’s strength lies in its enterprise ecosystem integration, especially with Windows Server, Microsoft 365, and Dynamics 365.

- Google LLC has registered itself as a strong player in enterprise cloud storage with services such as Google Cloud Storage and Persistent Disk. The company leverages its knowledge in data analytics, AI, and machine learning with the main goal of offering intelligent storage solutions optimized for performance and scalability.

- IBM Corporation plays a central role in hybrid and enterprise-focused cloud storage solutions. The company is highly focused on secure, compliant, and scalable storage systems, which are suitable for banking, healthcare, and government sectors. IBM’s strategic initiatives focus on data encryption, AI-powered data management through Watson, and enterprise modernization.

- Oracle Corporation is considered to be a significant enterprise cloud storage provider, which is offering Oracle Cloud Infrastructure with high-performance object storage, block storage, and archive solutions. In addition, the company’s strength lies in its deep enterprise database expertise, making it a preferred choice for organizations with mission-critical workloads.

Below is the list of some prominent players operating in the global market:

The global business cloud storage market is being dominated by hyperscalers such as AWS, Microsoft Azure, and Google Cloud, which leverage massive infrastructure scale, AI integration, and global data centers. At the same time, IBM and Oracle are highly focused on hybrid and enterprise-grade security solutions, whereas regional players such as Alibaba Cloud, SAP, and OVHcloud strengthen localized and regulated markets. Apart from these emerging firms, such as Wasabi and Cloudian, that compete in terms of cost efficiency and performance specialization. Key strategies adopted by the leading players in this field include multi-cloud ecosystems, AI-based storage optimization, zero-trust security frameworks, and industry-specific cloud offerings. In April 2026, Wasabi Technologies announced its plans to acquire Seagate’s Lyve Cloud business, making Seagate a shareholder in Wasabi. This particular deal strengthens Wasabi’s position as a leading pure-play cloud storage provider.

Corporate Landscape of the Business Cloud Storage Market:

Recent Developments

- In April 2026, NetApp and Google Cloud together announced the general availability of flex unified service for Google Cloud NetApp Volumes, which enables enterprises to run file and block workloads in the cloud. This collaboration simplifies data migration and unlocks AI innovation by removing complexity.

- In April 2026, Lenovo completed its acquisition of Infinidat to strengthen its enterprise storage portfolio and enhance AI-ready data infrastructure. The deal will expand support for mission-critical workloads and next-generation applications worldwide.

- In April 2026, Tata Steel entered into a partnership with Google Cloud to deploy a unified agentic AI strategy across its global value chain, to scale more than 300 specialized AI agents in nine months. This collaboration enhances efficiency, predictive intelligence, and decision-making.

- In November 2025, GB Labs introduced SPACE NVME and SPACE NVME Plus, which are high-performance all-NVMe storage solutions delivering up to 30 GB/s throughput with exceptional scalability and efficiency. These systems combine NVMe speed with HDD expandability.

- Report ID: 8541

- Published Date: Apr 30, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.