Bulk Container Packaging Market Outlook:

Bulk Container Packaging Market size was valued at USD 22.3 billion in 2025 and is projected to reach USD 40.4 billion by the end of 2035, rising at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of bulk container packaging is estimated at USD 23.7 billion.

The global bulk container packaging market demand is closely aligned with the industrial production, chemical agriculture, food processing, and waste management flows documented by the government agencies. According to the U.S. BEA, August 2023 data, the total exports reached USD 247.5 billion, reflecting the scale of industrial goods requiring intermediate bulk containers, drums, flexitanks, and rigid transport units for storage and distribution. The U.S. chemical production regional index reported continued output expansion across multiple chemical segments, indicating a sustained need for high-capacity industrial packaging for hazardous and non-hazardous materials. On the other hand, the producer price index for plastics product manufacturing reached 203.922 (June 1993 = 100) in December 2025, as per the FRED January 2026 data, reflecting sustained industrial demand despite broader manufacturing sector adjustments.

PPI for Plastics Product Manufacturing: Plastics Packaging

|

Month |

Unit (June 1993=100) |

|

January 2025 |

203.805 |

|

February 2025 |

203.492 |

|

March 2025 |

204.476 |

|

April 2025 |

204.973 |

|

May 2025 |

204.095 |

|

June 2025 |

203.366 |

|

July 2025 |

202.452 |

|

August 2025 |

202.872 |

|

September 2025 |

203.404 |

|

October 2025 |

205.201 |

|

November 2025 |

204.334 |

|

December 2025 |

203.922 |

Source: FRED January 2026

Besides, the regulatory oversight and sustainability mandates are materially influencing the procurement decisions in bulk container packaging. The U.S. Environmental Protection Agency in October 2025 reported that the container and packaging represented 82.2 million tons of the municipal waste generation, accounting for 28.1% of total MSW, indicating regulatory focus on reuse, recycling, and material efficiency. On the other hand, the Eurostat October 2025 data depict that the recycling rates in the EU are above 65%, driving the demand for reusable and recyclable bulk transport formats. Industrial buyers are therefore balancing compliance, reverse logistics efficiency, and lifecycle cost management as production volumes and cross-border trade flows remain structurally elevated across chemicals, food ingredients, agrochemicals, and industrial liquids.

Key Bulk Container Packaging Market Insights Summary:

Regional Highlights:

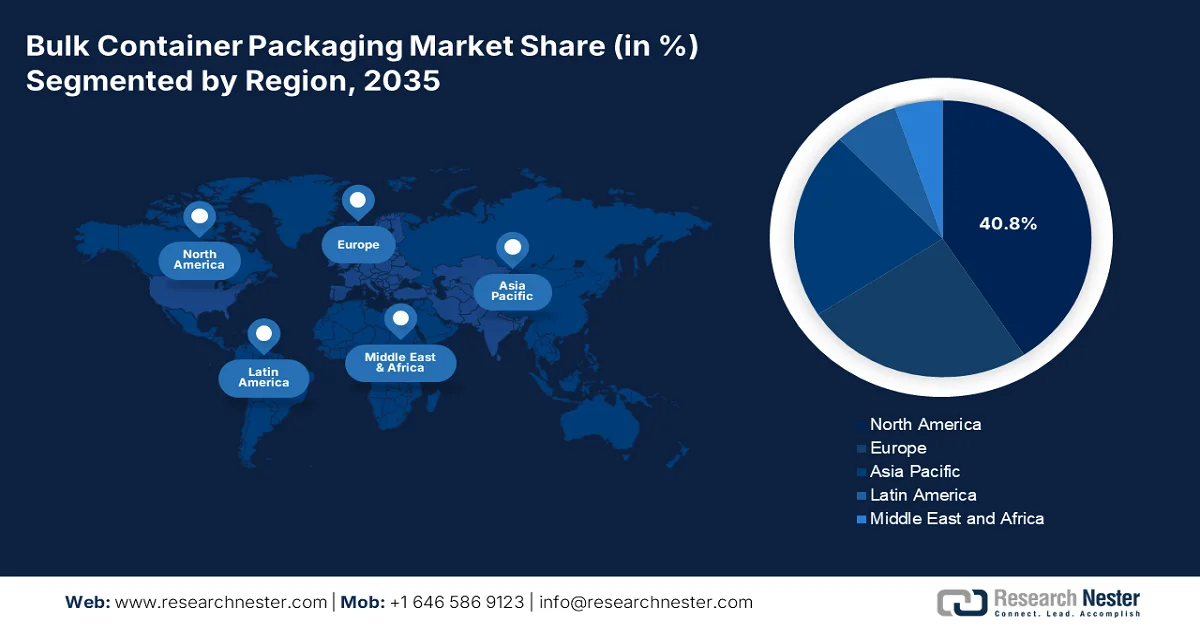

- North America is anticipated to secure a 40.8% revenue share by 2035 in the bulk container packaging market, attributable to its robust chemical manufacturing base, stringent hazardous material transport regulations, and rising adoption of reusable IBCs aligned with circular economy initiatives.

- Asia Pacific is projected to expand at a CAGR of 6.1% during 2026–2035 in the bulk container packaging market, stimulated by rapid industrialization, chemical industry expansion, and export-oriented manufacturing growth across China, India, and Southeast Asia.

Segment Insights:

- The plastics sub-segment is projected to command a 45.5% share by 2035 in the bulk container packaging market, propelled by its durability, lightweight properties, corrosion resistance, and suitability for maintaining product purity in pharmaceutical and specialty chemical applications.

- The large (200–1000 liters) capacity sub-segment is expected to dominate through 2035 in the bulk container packaging market, fueled by its ability to streamline bulk transport efficiency, optimize warehouse utilization, and support automated handling systems across industrial operations.

Key Growth Trends:

- Industrial production and manufacturing output expansion

- Agricultural exports and food ingredient trade flows

Major Challenges:

- Volatile raw material prices and tariffs

- High capital investment for reconditioning infrastructure

Key Players: Schutz GmbH & Co. KGaA (Germany), Mauser Packaging Solutions (U.S.), Greif, Inc. (U.S.), Time Technoplast Ltd (India), Hoover Ferguson Group, Inc. (U.S.), Snyder Industries, Inc. (U.S.), Bulk Handling Australia (Australia), Maschio Pack S.p.A. (Italy), Thielmann US GmbH (U.S.), International Paper Company (U.S.), Sonoco Products Company (U.S.), Sealed Air Corporation (U.S.), Myers Industries, Inc. (U.S.), Sharpsville Container Corporation (U.S.), Jiangsu Fast-Pack Co., Ltd (China), Yontuo Group (China), Braid Logistics (UK), Environmental Packaging Technologies (EPT) (U.S.), Trans Ocean Bulk Logistics (Netherlands), Qingdao LAF Packaging Co., Ltd. (China).

Global Bulk Container Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 22.3 billion

- 2026 Market Size: USD 23.7 billion

- Projected Market Size: USD 40.4 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 23 February, 2026

Bulk Container Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Industrial production and manufacturing output expansion: The government reported manufacturing output remains a primary demand driver for the bulk container packaging market, the chemicals, industrial liquids, and intermediate goods. According to the U.S. Bureau of Economic Analysis, November 2025 data, August exports accounted for USD 280.8 billion, reflecting the sustained industrial freight volumes requiring drums, IBCs, and large format containers for domestic distribution and exports. Additionally, the manufacturing growth trends in chemicals and durable goods are fueling the market growth. These indicators signal steady movement of industrial inputs that depend on compliant bulk transport packaging. Moreover, sustained capital expenditure in the advanced manufacturing facilities under federal industrial support programs is expected to further increase outbound bulk shipments of chemicals, specialty materials, and industrial inputs requiring certified large-capacity packaging solutions.

- Agricultural exports and food ingredient trade flows: Government agriculture trade data indicate strong cross-border commodity flows that depend on bulk storage and transport systems thereby driving the demand for the bulk container packaging market. As per the USDA July 2025, the agricultural exports reported USD 176 billion in 2024, including grains, oilseeds, and processed ingredients transported in bulk formats. Moreover, the News on-Air July 2024 data show that the cereal production globally accounted for 2,854 million tonnes, sustaining the high volume agricultural logistics requirements. These flows require food-grade bulk containers, flexitanks, and reusable intermediate containers. In addition, rising government-supported food security and grain reserve programs across Asia and the Middle East are further strengthening demand for compliant, high-capacity bulk packaging solutions to manage large-scale storage and export operations.

- Chemical sector output and hazardous materials regulation: Chemical production volumes directly influence the demand for the bulk container packaging market designed for hazardous material transport. The U.S. chemical production growth is supported by the industrial activity and export flows. Moreover, the hazardous material shipments account for hundreds of millions of tons annually across the modes. These volumes require un-rated drums and IBCs compliant with the U.S. Department of Transportation Hazardous Materials regulations. Additionally, tightening federal inspection protocols and cross-border transport compliance requirements are encouraging industrial shippers to upgrade to higher-specification reusable bulk containers to mitigate regulatory and liability risks.

Challenges

- Volatile raw material prices and tariffs: Fluctuating costs of the raw materials, such as the HDPE resin, steel, and aluminum, create significant margin pressure for the new entrants. The bulk container packaging market has been severely impacted by the geopolitical trade policies, causing the aluminum premium to surge. Top companies have tackled this by investing in lightweighting technologies to use less material per container, thereby mitigating the impact of raw material volatility on their pricing.

- High capital investment for reconditioning infrastructure: the bulk container packaging market is increasingly driven by the circular economy principles, requiring investment in the reconditioning networks, a significant hurdle for new players. The extended producer responsibility regulations in Europe require producers to finance the entire lifecycle of their packaging, including recovery and recycling. This necessitates costly infrastructure for cleaning, leak testing, and repairing used containers.

Bulk Container Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 22.3 billion |

|

Forecast Year Market Size (2035) |

USD 40.4 billion |

|

Regional Scope |

|

Bulk Container Packaging Market Segmentation:

Material Type Segment Analysis

The plastics sub segments is leading and are poised to hold the share value of 45.5% by 2035 in the bulk container packaging market. The segment is driven by its exceptional durability, lightweight nature, and resistance to corrosion and chemical reactivity. Unlike the metal containers, the high-density polyethylene does not rust or require expensive interior linings, making it the preferred choice for the pharmaceutical and specialty chemical industries where the product purity is paramount. Further, the material’s versatility allows manufacturers to mold complex features such as integrated handles and vents directly into the IBCs and drums. According to the U.S. EPA, October 2025 data, nearly 14.5 million tonnes of plastic containers were generated. This high generation volume shows the sustained industrial reliance on the plastic-based containers.

Capacity Segment Analysis

The large (200-1000 liters) capacity sub-segment is leading in the bulk container packaging market. The segment perfectly balances the efficiency of bulk transport with the manageability of intermediate logistics. These containers, mainly IBCs and reconditioned steel drums, optimize the warehouse space via standardized footprints and reduce the labor costs related to handling multiple smaller units. This capacity range is the workhorse of the chemical and food processing industries, enabling just-in-time manufacturing while minimizing the container disposal frequency. Its compatibility with automated filling, stacking, and palletization systems further enhances throughput efficiency across large-scale distribution and industrial processing facilities.

Closure Type Segment Analysis

The screw caps represent the largest sub-segment within the closure type category of the bulk container packaging market, driven by their reliability, reusability, and ability to form a hermetic seal. Unlike single-use snap-on options, the screw caps provide a mechanical advantage that ensures a tight, leak-proof closure, which is critical for securing hazardous chemicals and volatile organic compounds during transit. Their standardized threading allows for compatibility across various drum and IBC fittings, simplifying the filling and emptying processes for end users. Their robust design also supports multiple opening and resealing cycles without compromising structural integrity, making them suitable for returnable and reconditioned container systems. In addition, compatibility with tamper-evident bands and pressure-relief features enhances safety compliance across chemical, pharmaceutical, and industrial logistics applications.

Our in-depth analysis of the bulk container packaging market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Material Type |

|

|

End use |

|

|

Capacity |

|

|

Closure Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bulk Container Packaging Market - Regional Analysis

North America Market Insights

The North America is dominating and is poised to hold the regional revenue share of 40.8% by 2035. The region’s market is mature and is driven by the robust chemical manufacturing sector and stringent safety regulations enforced by the Pipeline and Hazardous Materials Safety Administration. The demand for the bulk container packaging market in North America is sustained by the need for certified containers for hazardous material transport. A key trend is the increasing adoption of reusable IBCs and reconditioning services driven by corporate sustainability goals and the circular economy principles encouraged by the Environmental Protection Agency. The market is also benefiting from the reshoring of the pharmaceutical manufacturing, which requires high-purity plastic drums and IBCs.

The U.S. market continues to expand in line with the scale and global integration of the domestic chemical industry. According to the Select USA 2025 data, the U.S. has exported over USD 494 billion worth of chemicals in 2022, representing more than 13% of global chemical production, reinforcing sustained demand for UN-rated drums, IBCs, and large capacity transport containers across international supply chains. Strong capital inflows are also evident with USD 766.7 billion in total foreign direct investment in 2023, supporting manufacturing expansion and logistics activity. At the same time, environmental compliance is shaping procurement patterns. The U.S. EPA October 2025 report reports a 53.9% recycling rate for containers and packaging, with 30.5 million tons landfilled and 7.4 million tons combusted with energy recovery. These data reinforce structured growth in durable, reusable bulk container packaging solutions across the bulk container packaging market in the U.S.

Top 6 Exporting States in 2024

|

State or Territory |

Chemical Manufacturing Exports (USD Billions) |

|

Texas |

57.0 |

|

Indiana |

24.7 |

|

Puerto Rico |

20.7 |

|

North Carolina |

16.5 |

|

California |

16.2 |

|

Illinois |

15.7 |

Source: U.S. BLS July 2025

The strong natural resource output, chemical production, and export-oriented industrial activity are shaping the bulk container packaging market in Canada. According to the Government of Canada, May 2024 data, total merchandise exports reached approximately USD 768.2 billion in 2023, reflecting sustained cross-border trade flows requiring compliant bulk transport packaging for chemicals, petroleum products, agricultural commodities, and processed materials. The energy sector remains a major driver, with the Government of Canada data in July 2025 reporting that crude oil production averaged over 4.9 million barrels per day in 2023, reinforcing demand for certified large-capacity containers used in lubricants, specialty chemicals, and related industrial fluids. These data are shaping procurement strategies for durable, reusable, and regulation-compliant bulk container packaging solutions across Canada’s industrial supply chains.

APAC Market Insights

The Asia Pacific is the fastest-growing market and is projected to grow at a CAGR of 6.1% during the forecast period 2026 to 2035. The bulk container packaging market in the Asia Pacific is driven by the rapid industrialization and export-oriented manufacturing. China serves as the production backbone, and India and Southeast Asia emerge as emerging growth markets. The primary driver is the region’s chemical industry expansion. A significant trend is the shift toward sustainable packaging, with Japan and South Korea leading in the adoption of reusable IBCs and lightweight HDPE containers. The region's pharmaceutical manufacturing growth, supported by government initiatives like India's Production Linked Incentive scheme, drives demand for the high-purity single-trip containers for active pharmaceutical ingredient transport.

The large-scale food production, export growth, and circular economy policy implementation are driving the bulk container packaging market in China. According to the People’s Republic of China, December 2023 data, the country’s total grain output reached approximately 695.41 million tonnes in 2023, reinforcing sustained demand for food-grade bulk containers used in edible oils, starches, sweeteners, and processed agricultural ingredients. On the other hand, the General Administration of Customs of China, January 2024 data reported that the total goods exports exceeded RMB 41.76 trillion in 2023, reflecting the significant cross-border movement of food ingredients and industrial products requiring compliant bulk transport solutions. These factors support increasing adoption of food-grade bulk containers and reusable bulk packaging systems across China’s food processing, chemical, and export-oriented manufacturing supply chains.

The expanding chemical production, strong agricultural output, and sustained export growth are propelling the bulk container packaging market in India. According to the PIB April 2025, India’s total merchandise exports reached approximately USD 437.42 billion, reflecting continued cross-border trade flows requiring compliant bulk transport solutions for chemicals, food ingredients, petroleum products, and industrial liquids. Moreover, the Ministry of Agriculture & Farmers Welfare reported record foodgrain production exceeding 357.73 million tonnes, sustaining high-volume storage and logistics requirements for bulk handling systems. Combined with Plastic Waste Management Rules, which promote recycling and extended producer responsibility, regulatory compliance, and export-oriented manufacturing, these are strengthening structured demand for durable, reusable bulk container packaging solutions across India’s industrial supply chains.

Europe Market Insights

The bulk containers packaging market in Europe is growing significantly and is driven by the region’s stringent regulatory framework for chemical transport and its leadership in the circular economy initiatives. Strict compliance with the registration evaluation, authorization, and restriction of chemicals regulations, which mandate the use of certified high-intensity containers for hazardous substance transport. This regulatory pressure ensures a consistent replacement demand for the IBCs and drums. A dominant trend is the shift towards the reusable packaging models propelled by the EU’s packaging and packaging waste regulation, which sets ambitious recycled content targets and waste reduction goals. The market is stable with growth concentrated in Western Europe, where industrial activity and regulatory enforcement are most pronounced.

The bulk container packaging market in Germany is supported by its position as Europe’s largest industrial and chemical producer, with a strong export orientation and strict environmental compliance standards. According to the Umwelt Bundesamt 2025 data, Germany recorded a total export of €132 billion in 2023, reflecting sustained broader movement compliant bulk storage and transport solutions. The German chemical industry remains a key demand contributor, with the Federal Ministry for Economic Affairs and Climate Action reporting chemicals among the country’s leading industrial sectors in terms of output and trade intensity. Export scale industrial production strength and regulatory-driven circular economy targets collectively sustain long-term demand for durable, compliance-certified bulk container packaging solutions across Germany’s B2B supply chains.

The Plastic Packaging Tax (PPT) compliance, pharmaceutical manufacturing strength, and sustained industrial liquid handling requirements are propelling the bulk container packaging market in UK. According to the Plastic Packaging Tax statistics 2024 to 2025 data nearly 1,740 thousand tonnes of plastic packaging were manufactured in the UK and 1,407 thousand tonnes were imported reflecting sustained industrial packaging volumes across chemicals pharmaceuticals food processing and industrial liquids. Of this, 1,591 thousand tonnes were declared as having 30% or more recycled content indicating strong alignment with recycled-content thresholds to mitigate tax exposure. These figures confirm that taxation policy, recycled material integration, and exemption frameworks are influencing procurement decisions, accelerating demand for market growth in UK.

Key Bulk Container Packaging Market Players:

- Schutz GmbH & Co. KGaA (Germany)

- Mauser Packaging Solutions (U.S.)

- Greif, Inc. (U.S.)

- Time Technoplast Ltd (India)

- Hoover Ferguson Group, Inc. (U.S.)

- Snyder Industries, Inc. (U.S.)

- Bulk Handling Australia (Australia)

- Maschio Pack S.p.A. (Italy)

- Thielmann US GmbH (U.S.)

- International Paper Company (U.S.)

- Sonoco Products Company (U.S.)

- Sealed Air Corporation (U.S.)

- Myers Industries, Inc. (U.S.)

- Sharpsville Container Corporation (U.S.)

- Jiangsu Fast-Pack Co., Ltd (China)

- Yontuo Group (China)

- Braid Logistics (UK)

- Environmental Packaging Technologies (EPT) (U.S.)

- Trans Ocean Bulk Logistics (Netherlands)

- Qingdao LAF Packaging Co., Ltd. (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Schutz GmbH & Co. KGaA is a global leader in the bulk container packaging market via relentless innovation and a closed-loop economy approach. The company is renowned for its comprehensive portfolio of intermediate bulk containers, high-quality industrial drums, and advanced packaging systems. The company mainly focuses on sustainability and the circular economy.

- Mauser Packaging Solutions is a powerhouse in the bulk container packaging market, offering a vast array of rigid and industrial packaging, including IBCs, drums, pails, and specialty containers. Following its merger with BWAY, the company has leveraged its combined scale to enhance its manufacturing footprint and service capabilities across Europe and the U.S.

- Greif, Inc is a longstanding industry leader in the bulk container packaging market, distinguished by its comprehensive portfolio of industrial packaging solutions, including steel, plastic, and fiber drums, as well as a wide range of IBCs and closure systems. The company’s strategic direction is based on building a Greif better way initiative, which focuses on customer-centric innovation, operational excellence, and sustainability. According to the 2025 annual report, the company's operational profit was USD 167.6 million.

- Time Technoplast Ltd has emerged as a formidable force in the global bulk container packaging market, leveraging its technological expertise and cost-competitive manufacturing base in India. The company is a leading manufacturer of polymer-based technical products, including a wide array of industrial packaging, such as IBCs, jerry cans, drums, and crates. In 2024, the consolidated net revenue is Rupees 49,925.01 million.

- Hoover Ferguson Group, Inc. is a globally recognized leader in the bulk container packaging market and specializes in the rental, sale, and service of reusable industrial packaging. The company’s extensive portfolio includes IBCs, stainless steel and poly tanks, and portable chemical containers serving diverse sectors from oil and gas to specialty chemicals.

Here is a list of key players operating in the global bulk container packaging market:

The global bulk container packaging market is highly competitive and fragmented, and is defined by the presence of established multinational corporations and specialized regional players. The key strategic initiatives among the market leaders include a strong focus on product innovation, mainly the development of lightweight, sustainable, and reusable intermediate bulk containers and flexitanks to meet stringent environmental regulations. Companies are aggressively expanding their geographic footprint via mergers and acquisitions to enhance production capabilities and enter the high growth Asia market. For example, in April 2022, Novvia Group acquired Southern Container, a distributor of plastic, metal, fiber, and glass packaging products. further the significant investment is being directed towards the advanced manufacturing technologies, such as the automated blow molding for rigid containers, to improve the efficiency and cater to the diverse needs of end-use industries such as chemicals, pharmaceuticals, and food processing.

Corporate Landscape of the Bulk Container Packaging Market:

Recent Developments

- In December 2025, Mauser Packaging Solutions, a leading global supplier of rigid packaging products and services, announced that it has completed the acquisition of substantially all of the assets of Siena Plastics LLC, a manufacturer of small high-performance containers for the industrial packaging industry located in Charlotte, North Carolina.

- In August 2025, Greif, a premier global provider of industrial packaging, delivering legendary customer service has announced the expansion of its sustainable packaging solutions with a new 10L Jerrycan reinforced in Scandinavia.

- In August 2024, Global rigid container and life sciences packaging distributor, Novvia Group has acquired Rhino Container Inc., a distributor of plastic, metal, corrugated, and glass packaging products. Financial terms of the private transaction were not disclosed.

- Report ID: 4512

- Published Date: Feb 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.