Bottled Water Packaging Market Outlook:

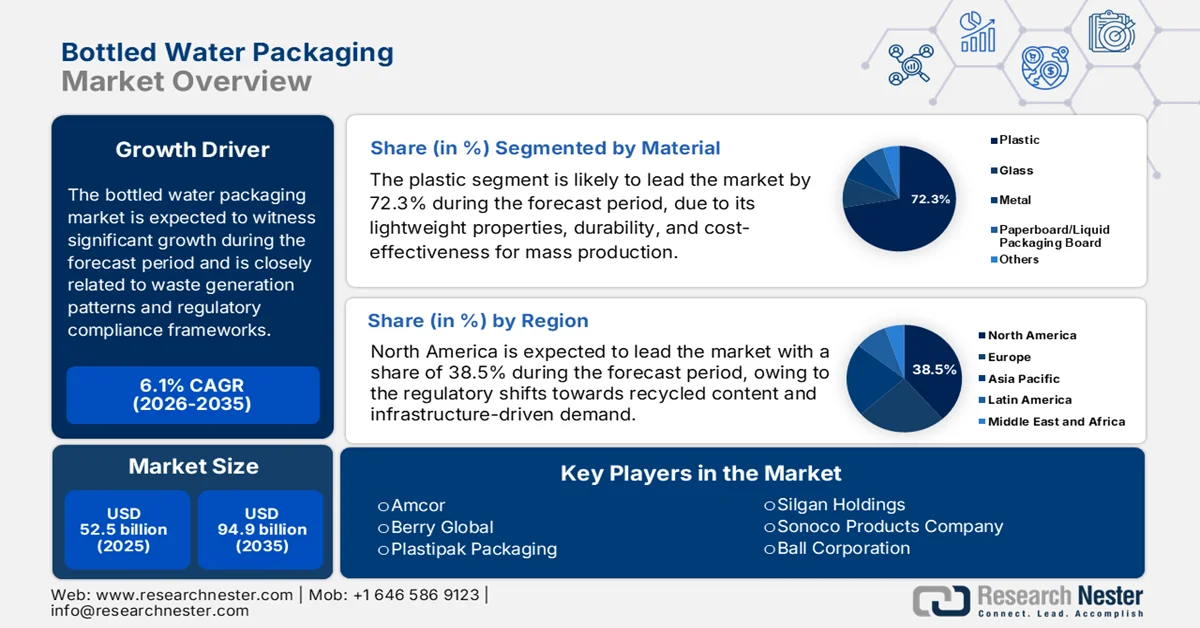

Bottled Water Packaging Market size was valued at USD 52.5 billion in 2025 and is projected to reach USD 94.9 billion by the end of 2035, rising at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of bottled water packaging is assessed at USD 55.7 billion.

The market is closely linked to the consumption volumes, waste generation patterns, and regulatory compliance frameworks. The market is also driven by the process of being hydrated in the day-to-day lifestyle. According to the Bottled Water October 2024 data, nearly 86% of the people in the U.S. consume bottled water, driving the market demand. Moreover, according to the NLM August 2024 study, the global plastic production is nearly 400 million tonnes annually, and the recycling rate is 9%. Additionally, the U.S. Environmental Protection Agency's October 2025 reports that containers and packaging accounted for 28.1% of total municipal solid waste generation, underscoring the scale of the packaging material flow linked to beverage consumption. Further, under the European Union Single Use Plastics Directive, Member States are required to achieve a separate collection rate for plastic beverage bottles, directly influencing recycled content procurement and packaging design strategies.

Besides, beverage bottles are a significant component within this stream. The PET remains the dominant material for the bottled water packaging due to its weight and transport efficiency. however, the recycling performance remains moderate. Regulatory targets are reshaping the procurement and material strategies in the bottled water packaging value chain. According to the European Commission, January 2026 data, the PET beverage bottles are required to contain at least 25% of the recycled plastic by 2025 and 30% by 2030, long 77% separation collection target in 2025. These requirements are prompting the manufacturers and brand owners to reassess supplier partnerships, invest in the recycled resin integration, and align packaging formats with evolving compliance and traceability expectations across the key markets.

Key Bottled Water Packaging Market Insights Summary:

Regional Highlights:

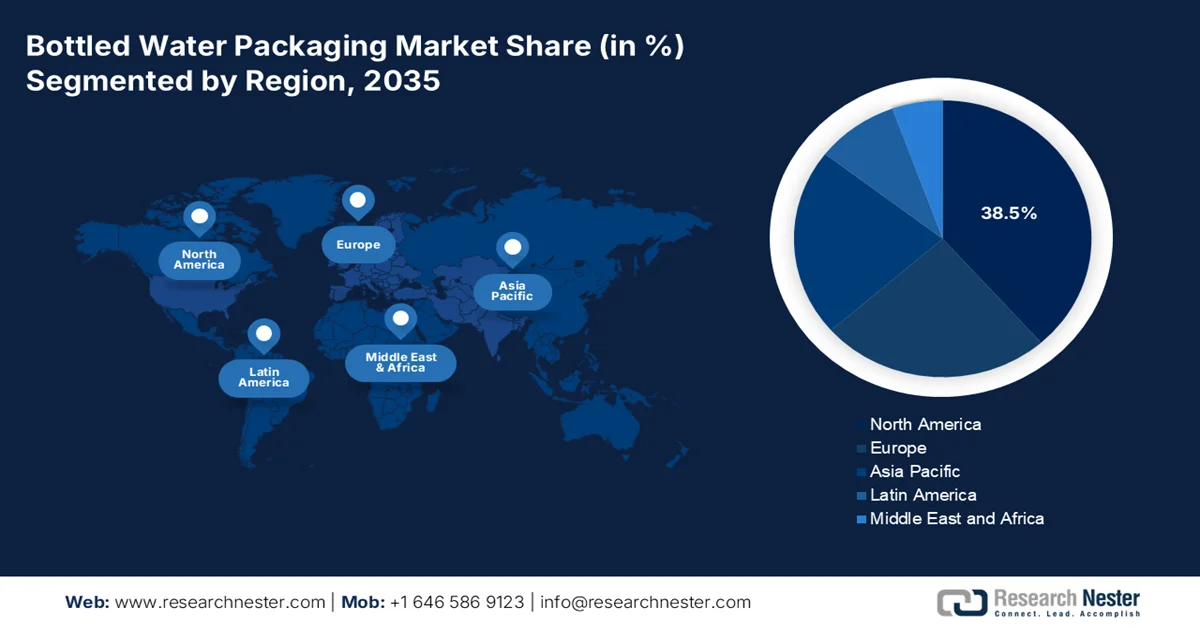

- North America bottled water packaging market is projected to command a 38.5% revenue share by 2035, attributed to regulatory shifts toward recycled content and infrastructure-driven demand.

- Asia Pacific is forecast to expand at a CAGR of 7.1% during 2026–2035, propelled by population density, rapid urbanization, and infrastructure disparities.

Segment Insights:

- Plastic segment in the bottled water packaging market is anticipated to secure a 72.3% share by 2035, driven by its lightweight properties, durability, cost-effectiveness for mass production, and accelerating adoption of recycled packaging.

- Recycled Packaging segment is expected to witness notable expansion through 2026–2035, fueled by supportive government regulations and extended producer responsibility frameworks accelerating closed-loop recycling investments.

Key Growth Trends:

- Expansion of municipal solid waste

- Growth in packaging waste generation

Major Challenges:

- Quality consistency issues in recycled materials

- Declining recycling rates

Key Players: Amcor (Switzerland), Berry Global (U.S.), Plastipak Packaging (U.S.), Silgan Holdings (U.S.), Sonoco Products Company (U.S.), Ball Corporation (U.S.), Alpha Packaging (U.S.), Crown Holdings (U.S.), Sidel International (France), Gerresheimer AG (Germany), Greiner Packaging International (Austria), RPC (UK), SKS Bottle & Packaging (U.S.), Graham Packaging Company (U.S.), Toray Industries (Japan), Amcor Limited (Australia), PET Power (South Korea), Alpack Plastics (India), Ampac (U.S.), Berlin Packaging Company (U.S.)

Global Bottled Water Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 52.5 Billion

- 2026 Market Size: USD 55.7 Billion

- Projected Market Size: USD 94.9 Billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 23 February, 2026

Bottled Water Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of municipal solid waste: Government investment in recycling and waste management infrastructure is directly influencing the packaging material demand and design specifications and driving the market. In the U.S., the EPA's September 2023 report indicates that USD 275 million has been announced in solid waste infrastructure for recycling grants to improve the collection, sorting, and recycling system. These investments strengthen the PET bottle recovery streams and increase the availability of recycled resin, enabling compliance with the recycled content mandates. Similarly, the U.S. Bipartisan Infrastructure Law allocates long-term funding to strengthen the waste and recycling systems, improving the circular material flows. For packaging manufacturers, this creates procurement visibility for recycled feedstock and supports long-term supply agreements.

- Growth in packaging waste generation: The European Commission's October 2023 data reports that EU packaging waste reached 188.7 kg per capita in 2021, the highest recorded level. Packaging remains one of the largest waste streams, placing the beverage bottles under the policy focus. Moreover, the total packaging waste in Europe is reinforcing the scale of regulatory attention on material-intensive sectors such as beverages. Plastic packaging represented a significant share of this volume, with comparatively lower recycling rates than paper and metal streams, increasing the compliance pressure on the PET bottle producers. This sustained rise in per capita packaging waste is surging EPR enforcement and driving the demand for recyclable, lightweight, and high recycled content bottle formats across the EU markets.

- Public health campaigns promoting hydration: Government health agencies are actively promoting water consumption as a public health priority, indirectly supporting the packaged water demand. The nutrition and physical activity program supports water consumption as an alternative to sugar-sweetened beverages. Further, the hydration research projects are actively driving the consumption of water for the betterment of health. Moreover, the water access promotion programs in schools and public facilities are boosting the market growth. These public health investments normalize increased water consumption across demographic groups, expanding the total addressable market for packaged water while positioning bottled products as essential components of healthy living patterns rather than discretionary consumer choices.

Challenges

- Quality consistency issues in recycled materials: The varying quality of post-consumer PET flakes introduces significant processing challenges for manufacturers attempting to meet the recycled content targets in the market. contaminants reduce the yields and increase the production costs, with the color sorting remaining mainly problematic as mixed blue-green and clear flakes degrade the optical properties of recycled material. These quality inconsistencies make it difficult for the new entrants to guarantee product appearance and performance, particularly for premium water brands where visual appeal is paramount.

- Declining recycling rates: Despite the industry's commitments to circularity, recycling infrastructure fails to keep pace with production volumes, creating a critical supply-demand gap in the market. The decline validates stricter regulations while making it nearly impossible for manufacturers to secure adequate food-grade recycled materials. The collection systems also capture fewer PET bottles in most markets, with the dramatic regional variances in parts of Southeast Asia.

Bottled Water Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 52.5 billion |

|

Forecast Year Market Size (2035) |

USD 94.9 billion |

|

Regional Scope |

|

Bottled Water Packaging Market Segmentation:

Material Segment Analysis

Plastic is dominating and is poised to hold the share value of 72.3% by 2035 in the bottled water packaging market. The segment dominance is due to its lightweight properties, durability, and cost-effectiveness for mass production. The leading sub-segment is rapidly shifting due to the stringent global regulations and corporate sustainability pledges aimed at creating a circular economy for plastics. In the U.S., the FDA’s regulatory framework for recycled plastics ensures that the rPET used in food contact applications, such as water bottles, meets rigorous safety standards, thereby enabling its widespread adoption. According to the CEED June 2025 data, nearly 60% of the plastic waste is recycled, compelling the manufacturers to integrate rPET into their supply chains.

Sustainability Initiatives Segment Analysis

The recycled packaging is driving the segment growth in the market. The segment directly addresses the environmental concerns by reducing the reliance on virgin plastic by 79% as per the NLM September 2025 study and lowering the carbon footprint of packaging, indicating a potential reduction in carbon emissions compared to the virgin PET. Major industry players are publicly committing to high rPET inclusion rates to meet both the regulatory demands and consumer expectations. Further, the supportive government regulations and Extended Producer Responsibility frameworks across key markets are accelerating investments in closed-loop recycling infrastructure and boosting the adoption of recycled PET in bottled water packaging.

Bottle Water Type Segment Analysis

Still water is the dominant sub segment in the bottled water packaging market and is driven by the fundamental health and safety concerns worldwide. The consumers consistently choose still water as a healthier alternative to sugary beverages and as a reliable source of clean hydration, mainly in regions where the tap water quality is perceived as unsafe or unreliable. This persistent demand is validated by the public health data. Moreover, many waterborne diseases, such as typhoid and cholera, continue to cause significant morbidity and mortality globally, reinforcing the reliance on safe packaged drinking water. Further, the consumption is immense as a significant percentage of the population consumes bottled water, with the still water constituting the vast majority of that volume.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Material |

|

|

Bottle Water Type |

|

|

End user |

|

|

Distribution Channel |

|

|

Packaging Size |

|

|

Price Range |

|

|

Sustainability Initiatives |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bottled Water Packaging Market - Regional Analysis

North America Market Insights

North America represents a mature market and is expected to hold the regional revenue share of 38.5% by 2035. The market is driven by the regulatory shifts towards recycled content and infrastructure-driven demand. The U.S. emphasis on the water infrastructure replacement cycles sustains consumer reliance on packaged alternatives despite federal investments. Canada provinces increasingly adopt extended producer responsibility frameworks shifting packaging waste management costs to producers. The regional drivers include emergency preparedness, procurement, healthcare facilities, water quality requirements, and tourism industry recovery. The material innovation focuses on recycled PET content compliance with the state-level mandates. The bottled water packaging market in North America demonstrates resilience via institutional contracting cycles.

Strong domestic consumption patterns and measurable economic contributions from the recycling sector are driving the market in the U.S. According to the U.S. EPA’s September 2025 data, recycling and reuse activities accounted for 681,000 jobs, USD 37.8 billion in wages, and USD 5.5 billion in tax revenues. This demonstrates the economic linkage between beverage container recovery and national employment output. On the other hand, the report from the Bottled Water in October 2024 shows that the consumer demand remains strong with bottled water ranking as the No. 1 beverage by volume, surpassing carbonated soft drinks, according to industry-referenced U.S. consumption data. further the packaging preferences also favor plastic formats, with 75% of bottled water consumers preferring plastic bottles, reinforcing a continued PET bottle demand. These structural consumption, recycling, and economic indicators support sustained growth in U.S. bottled water packaging volumes.

Packaging Preference Among Bottled Water Drinkers

|

Packaging Type |

Share (%) |

|

Plastic Bottles |

75% |

|

Glass Bottles |

16% |

|

Metal Cans |

6% |

|

Cartons |

3% |

Source: Bottled Water, October 2024

The Canada market increasingly operates within extended producer responsibility frameworks that reshape packaging economics. According to the Statistics Canada June 2023 report the plastic packaging represents the largest share of plastics used in products for domestic consumption, totaling 6.2 million tonnes. Within packaging, plastic bottles recorded the most consistent growth, increasing by nearly 100,000 tonnes to reach 471,393 tonnes, indicating sustained demand across beverage applications. On the recycling side, the recyclers produced 402,496 tonnes of recycled plastic resin, with packaging accounting for 82.9% of recycled output, demonstrating established recovery channels. These data indicate that the demand for the market in Canada remains volume-driven and is increasingly shaped by circular economy mandates and waste diversion targets.

APAC Market Insights

The Asia Pacific is the fastest growing market and is accelerating at a CAGR of 7.1% during the forecast period 2026 to 2035. The market is driven by population density, urbanization, and infrastructure disparities. Parts of the region lack access to safely managed drinking water in regions with a rising urban population. Moreover, the World Economic Forum data in June 2024 states that USD 800 billion is allocated for water infrastructure investment to meet the sustainable development goals, with the current spending gaps sustaining packaged water demand. The regulatory framework varies significantly from Japan’s mature recycling infrastructure to emerging extended producer responsibility requirements. Moreover, many places in the region lack basic water services, creating an institutional demand for packaged alternatives. Material innovation focuses on lightweighting and recycled content compliance with the divergent national standards across the region.

China maintains regional dominance through population scale and infrastructure investment gaps. The country represents the largest bottled water market globally. According to the IOP Science 2021, the bottled water consumption account for approximately 25%, with total market revenue reaching 166 billion yuan and volume at 48.5 billion litres, reflecting strong structural demand. With a population exceeding 1.38 billion, per capita bottled water consumption stood at 40.97 litres, indicating further headroom for expansion. Market forecasts projected off-trade volume growth of 54.8 billion litres and value growth of 209.6 billion yuan by 2023, signaling sustained packaging requirements, particularly in the still mineral water segment. Consumer behavior trends also reinforce diversified packaging demand, with 51.5% of surveyed urban residents preferring bottled water, while large-format containers and cooler bottles remain widely used, thereby indicating a positive market growth.

Off-trade Bottled Water Sales by Category

|

Category |

2019 |

2020 |

2021 |

2022 |

2023 |

|

Carbonated bottled water |

77.1 |

79.6 |

81.8 |

83.8 |

85.7 |

|

Functional bottled water |

1,289.5 |

1,306.2 |

1,327.1 |

1,352.4 |

1,382.1 |

|

Bottled still water |

42,458.3 |

45,213.2 |

47,930.2 |

50,599.7 |

53,364.7 |

|

Total |

43,824.9 |

46,599.0 |

49,339.1 |

52,035.8 |

54,832.5 |

Source: IOP Science

The bottled water packaging market in India operates within a high-volume and evolving plastic waste ecosystem. According to the CED June 2025 report, India generates 3.90 million tonnes of plastic waste annually, of which only about 60% is recycled, leaving nearly 1.65 million tonnes unmanaged or landfilled. Plastic waste is embedded within India’s broader 160,000 tonnes per day municipal solid waste stream, where limited source segregation constrains high-quality PET recovery. With only 17% of households practicing full waste segregation recycled resin supply remains inconsistent despite strong demand from FMCG and beverage packaging players. For bottled water packaging, the growth is increasingly linked to source segregation reforms, informal sector integration, and stable post-consumer recycled feedstock availability, which will determine cost efficiency and regulatory alignment in the Indian market.

Europe Market Insights

The market in Europe operates in the European Union’s circular economy action plan and single-use plastics directive regulatory framework. The Eurostat October 2025 data depicts that the packaging waste generation reached 79.7 million tonnes in 2023, with plastic representing 19.3% of packaging waste. The regional drivers include extended producer responsibility compliance costs, tourism industry demand, and infrastructure investment gaps in the Eastern European municipal water system. The European Medicines Agency and the European Commission's health initiatives influence the healthcare facility procurement specifications. The market growth reflects steady institutional demand rather than retail expansion, with variation between the Western European maturity and Eastern European development.

Packaging Waste Generated by Material Type

|

Material |

Percentage |

|

Paper and Cardboard |

40.4 |

|

Plastic |

19.8 |

|

Glass |

18.8 |

|

Wood |

15.8 |

|

Metal |

4.9 |

|

Other |

0.2 |

Source: Eurostat October 2025

The bottled water packaging market in Germany is strongly shaped by the country’s Packaging Act, the Single-Use Plastics Ordinances, and the Disposable Plastics Fund Act, which collectively impose structured compliance and cost obligations on producers, fillers, importers, and distributors. According to the CMS March 2024 data, all producers of system-relevant, beverage packaging must register with the LUCID packaging register participate in a dual take-back system, and report packaging volumes and material mass. From 1 January 2025, electronic marketplace operators and fulfilment service providers must verify producer registration before enabling sales, with penalties of up to EUR 100,000 for violations. Moreover, the tethered cap requirements and eco-modulated license fees reward recyclable and recycled-content packaging. These measures position regulatory compliance, recycled resin integration, and lightweight design as central growth determinants in the Germany bottled water packaging market.

The circular economy legislation, deposit return reforms, and the recycled content mandates that are restructuring material demand and the recovery economics are shaping the bottled water packaging market in the UK. According to the Department for Environment, Food & Rural Affairs, January 2023 data, the recycling rates for drinks containers stand at 70%, leaving an estimated 4 billion plastic bottles and 2.7 billion cans unrecycled annually. The planned Deposit Return Scheme (DRS) is designed to increase collection rates to 90% or higher, creating a segregated high-quality recycling stream and improving domestic rPET availability. Moreover, Keep Britain Tidy reported that plastic bottles and non-alcoholic cans account for 43% of total litter volume, reinforcing regulatory urgency to improve recovery systems. These regulatory and infrastructure developments are expected to strengthen recycled content integration, compliance-driven packaging redesign, and stable long-term growth in the UK market.

Key Bottled Water Packaging Market Players:

- Amcor (Switzerland)

- Berry Global (U.S.)

- Plastipak Packaging (U.S.)

- Silgan Holdings (U.S.)

- Sonoco Products Company (U.S.)

- Ball Corporation (U.S.)

- Alpha Packaging (U.S.)

- Crown Holdings (U.S.)

- Sidel International (France)

- Gerresheimer AG (Germany)

- Greiner Packaging International (Austria)

- RPC (UK)

- SKS Bottle & Packaging (U.S.)

- Graham Packaging Company (U.S.)

- Toray Industries (Japan)

- Amcor Limited (Australia)

- PET Power (South Korea)

- Alpack Plastics (India)

- Ampac (U.S.)

- Berlin Packaging Company (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Amcor continues to solidify its leadership in the market by focusing on circular economy principles and regulatory compliance. The company has strategically advanced its portfolio of caps, closures, and reusable caps specifically designed for water and beverage applications. According to the 2024 annual report, the company has made a net sale of USD 3,535 million.

- Berry Global is driving significant advancements in the bottled water packaging market via a dual focus on recycled content and reusable systems. The company has demonstrated its commitment to circularity by producing the bottles for luxury water brands using 100% recycled PET, proving that sustainability does not require compromising on premium aesthetics.

- Plastipak Packaging is an industry leader in the bottled water packaging market and combines technological expertise with deep category knowledge to serve global beverage brands. The company is a recognized specialist in producing packaging for both sparkling and non-carbonated water, utilizing advanced cold fill, hot fill, and aseptic technologies to maintain product integrity and shelf life.

- Silagan Holdings makes a significant impact on the bottled water packaging market via its expertise in rigid packaging solutions and dispensing systems. While serving a broad range of industries, Silgan’s custom container segment provides highly engineered packaging for the beverage sector, including custom-designed closures that enhance the consumer experience for water drinkers. In 2025, the net sales reported were USD 6.5 billion.

- Sonoco Products Company is reinforcing its strategic position in the market by streamlining its focus on high-growth sustainable packaging solutions. As part of a major strategic realignment, the company now emphasizes its consumer packaging segment, which delivers innovative packaging for beverages and other fast-moving consumer goods.

Here is a list of key players operating in the global market:

The global bottled water packaging market is defined by the intense competition among the established multinational corporations and specialized regional players, driven by increasing health consciousness and demand for sustainable solutions. The key industry participants are strategically pivoting towards eco-friendly innovations such as lightweight PET bottles, recycled materials, and biodegradable alternatives to address environmental concerns. The companies are actively focusing on mergers and acquisitions to expand their geographical reach. For example, in October 2025, Coca-Cola collaborates with Tech Partners to create a bottle prototype made from 100% plant-based sources. Further, the companies are investing in advanced packaging technologies and diverse product formats to cater to the growing demand for premium functional and on-the-go hydration products, while also optimizing the supply chains and expanding the distribution networks to strengthen their global footprint.

Corporate Landscape of the Bottled Water Packaging Market:

Recent Developments

- In June 2025, Coca-Cola launched Ratha Yatra-themed packaging for its packaged drinking water brand, Kinley. The company will also foster economic empowerment by supporting local vendors and retailers and driving tangible social and environmental impact.

- In December 2024, The Coca‑Cola Com. pany announced that it has reached an agreement with the Jubilant Bhartia Group, a multi-billion-dollar conglomerate with global presence in diverse sectors, to acquire a 40% stake in Hindustan Coca‑Cola Holdings Pvt. Ltd., the parent company of the largest Coca‑Cola bottler in India, Hindustan Coca‑Cola Beverages Pvt. Ltd.

- In November 2024, Primo Brands announced the successful completion of the merger of Primo Water Corporation and an affiliate of BlueTriton Brands, Inc., creating Primo Brands, a leading branded beverage company in North America focused on healthy hydration.

- Report ID: 4502

- Published Date: Feb 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.