Cast Polypropylene Packaging Films Market Outlook:

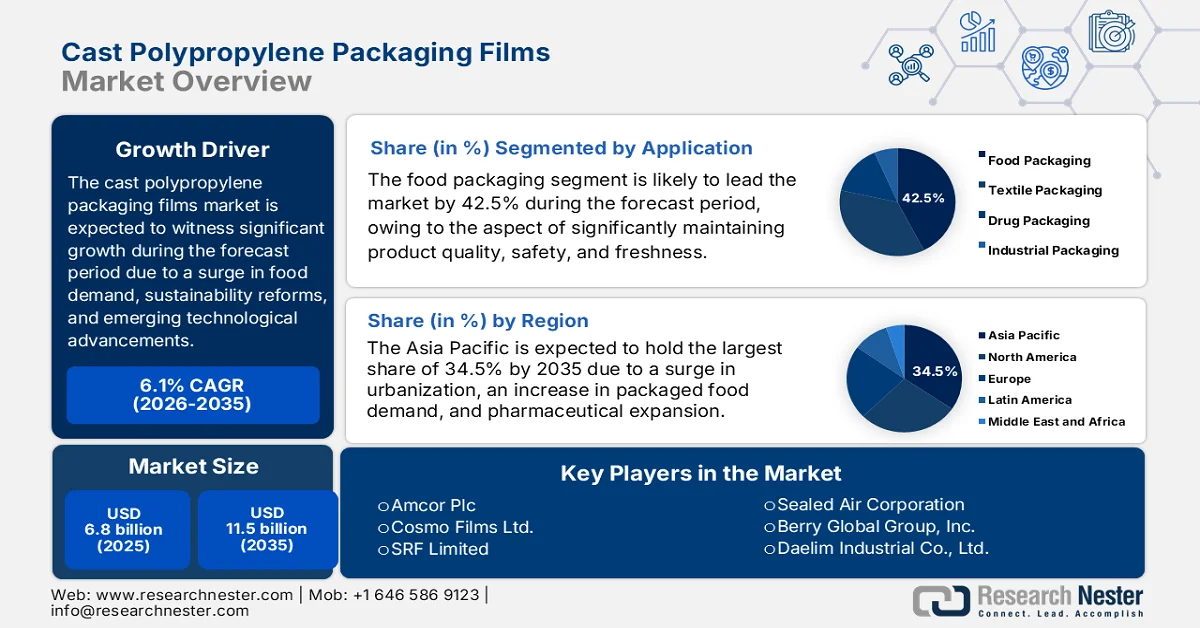

Cast Polypropylene Packaging Films Market size was over USD 6.8 billion in 2025 and is expected to reach USD 11.5 billion by the end of 2035, growing at a CAGR of 6.1% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of cast polypropylene packaging films is estimated at USD 7.2 billion.

The worldwide cast polypropylene packaging films market is rapidly evolving, effectively diversified by factors beyond conventional pharmaceutical and food demand. In addition, a shift towards consumer behaviors, sustainability mandates, and emerging technologies are significantly reshaping the industrial landscape. According to official statistics published by NLM in October 2022, only 2% of plastic packaging materials are recycled as packaging materials globally. Besides, 30% of plastic-based packaging products are either too small or complicated to recycle, such as small sachets and multi-layered materials. Despite this challenge, packaging materials have emerged as a crucial part of regular lives. Moreover, plastic building materials are the most utilized packaging materials, and nearly 26% of the overall utilization of polymers in packaging makes it the largest application.

2024 Plastic Building Materials Export and Import Analysis Internationally

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

3.3 billion |

- |

|

Poland |

2.3 billion |

- |

|

Germany |

1.7 billion |

1.3 billion |

|

U.S. |

- |

2.9 billion |

|

Italy |

- |

1.1 billion |

|

Global Trade Valuation |

16.5 billion |

|

|

Global Trade Share |

0.072% |

|

|

Product Complexity |

0.23 |

|

|

Export Growth |

9.3% |

|

Source: OEC

Furthermore, the smart packaging integration, transition to mono-material packaging, along with branding and customization demand, are certain trends that are responsible for boosting the cast polypropylene packaging films market globally. As per an article published by Future Foods in December 2023, on an international scale, 1/3rd of all food that is produced is wasted or lost, as has been demonstrated by the U.S. Food and Agriculture Organization, along with roughly 600 million people from different nations suffering from foodborne diseases every year. Therefore, by reducing the amount of wasted food, smart packaging is gradually increasing and eventually raising the level of food safety. Besides, as per the April 2024 Journal of Cleaner Production article, the packaging sector readily accounts for nearly 46% of plastic waste, owing to the prevalence of single-use plastics, thereby denoting an optimistic outlook for the overall market.

Key Cast Polypropylene Packaging Films Market Insights Summary:

Regional Highlights:

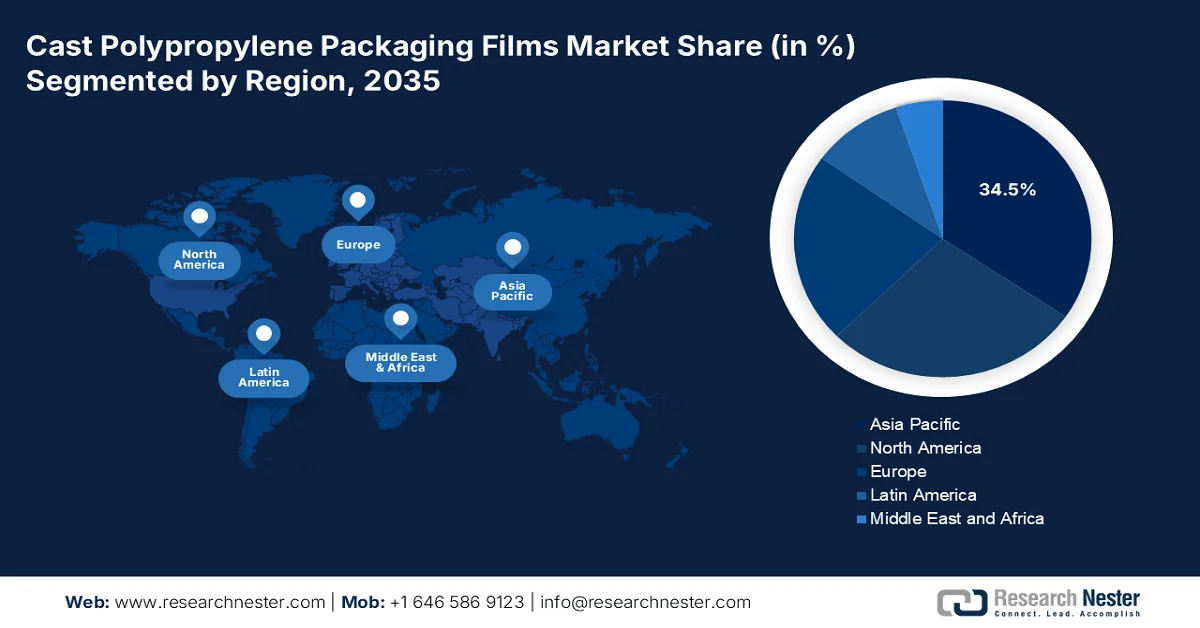

- Asia Pacific is anticipated to command a 34.5% share of the cast polypropylene packaging films market by 2035, impelled by rising urban/actionised urbanization, escalating packaged food demand, pharmaceutical expansion, and supportive government-backed sustainability initiatives.

- Europe is projected to register the fastest growth in the cast polypropylene packaging films market over 2026–2035, catalyzed by strong demand for sustainable pharmaceutical and food packaging solutions alongside progressive circular economy regulations.

Segment Insights:

- The food packaging segment is forecast to capture a 42.5% share by 2035 in the cast polypropylene packaging films market, driven by its criticalexplained role in preserving product quality, freshness, and safety through superior clarity, seal integrity, and moisture barrier performance.

- The retort CPP films sub-segment is expected to secure the second-largest share in the cast polypropylene packaging films market by 2035, fueled by its capability to endure high-temperature sterilization while maintaining structural integrity for safe and shelf-stable packaging.

Key Growth Trends:

- Expansion of cold chain logistics

- Trade liberalization in emerging economies

Major Challenges:

- Environmental regulations and sustainability pressure

- Competition from alternative packaging materials

Key Players: Taghleef Industries (UAE), Jindal Poly Films Limited (India), Polyplex Corporation Limited (India), Oben Holding Group (Peru), Treofan Group (Germany), Mitsui Chemicals Tohcello, Inc. (Japan), Toray Industries, Inc. (Japan), Uflex Ltd. (India), LC Packaging International BV (Netherlands), Innovia Films (UK), Amcor Plc (Australia), Cosmo Films Ltd. (India), SRF Limited (India), Polibak (Turkey), Schur Flexibles Holding GmbH (Austria), Sealed Air Corporation (U.S.), Berry Global Group, Inc. (U.S.), Daelim Industrial Co., Ltd. (South Korea), Scientex Berhad (Malaysia), Toyobo Co., Ltd. (Japan).

Global Cast Polypropylene Packaging Films Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.8 billion

- 2026 Market Size: USD 7.2 Billion

- Projected Market Size: USD 11.5 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (34.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: Chinainspires, United States, Germany, Japan, India

- Emerging Countries: Indonesia, Thailand, Philippines, Malaysia, Vietnam

Last updated on : 3 March, 2026

Cast Polypropylene Packaging Films Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of cold chain logistics: The rise in the demand for chilled and frozen foods worldwide is bolstering the cast polypropylene packaging films market adoption, owing to its durability and moisture resistance in cold storage environments. According to official statistics published by the ASSOCHAM Organization in July 2024, the cold chain logistics industry in India is projected to grow at a 5.6% growth rate, amounting to USD 10.3 billion as of 2024 and further expected to increase to USD 13.5 billion by the end of 2029. This industrial growth is primarily attributed to a rise in the need for perishable products, the growth of e-commerce platforms, and the expansion of the food and pharmaceutical sectors. Therefore, with such growth, there is a huge opportunity for the market to expand globally.

- Trade liberalization in emerging economies: The aspect of free trade deals in Latin America and the Asia Pacific has unleashed the newest opportunities for the cast polypropylene packaging films market exports, thereby fueling market penetration and scale upliftment. As stated in an article published by the UNCTAD Organization in March 2025, global trade facilities reached USD 33 trillion as of 2024, with projections varying across sectors, industries, and regions. Besides, agricultural exports from developing countries have witnessed import duties averaging nearly 20%. Meanwhile, apparel and textiles remain subject to some of the largest tariff rates, with import duties averaging near to 6%. Moreover, trade between South Asia and Latin America has experienced an average tariff of almost 15%, thus driving the market growth.

- Advancements in polymer science: Intense research into nanocomposite cast polypropylene packaging films is significantly enhancing gap properties, expanding shelf life, and developing the latest applications in industrial and healthcare packaging. As per an article published by the Royal Society of Chemistry in 2026, every year, nearly 36 million tons of polymer in liquid formulations are created from fossil sources. The yearly valuation of these materials amounts to USD 125 billion, which is utilized and recovered every year. As stated in an article published by the U.S. National Science Foundation in April 2024, the government organization has unveiled a USD 9.5 million research funding opportunity by partnering with Procter & Gamble Co., PepsiCo Inc., IBM, Dow, and BASF, thereby proliferating the cast polypropylene packaging films market’s exposure.

Challenges

- Environmental regulations and sustainability pressure: One of the most significant challenges facing the cast polypropylene packaging films market is the tightening of environmental regulations worldwide. Governments and regulatory bodies are increasingly restricting single-use plastics, pushing manufacturers to adopt recyclable or biodegradable alternatives. For instance, the Europe’s Single-Use Plastics Directive mandates reductions in plastic waste, directly impacting demand for conventional CPP films. Similarly, the U.S. Environmental Protection Agency (EPA) has expanded its Green Chemistry Program, encouraging sustainable packaging solutions. While these initiatives promote innovation, they also increase compliance costs and require substantial investment in R&D.

- Competition from alternative packaging materials: The cast polypropylene packaging films market faces intense competition from alternative packaging materials such as biaxially oriented polypropylene (BOPP), polyethylene (PE), and polyethylene terephthalate (PET) films. These substitutes often offer superior mechanical strength, barrier properties, or cost advantages, making them attractive to end-users in food and pharmaceutical packaging. For instance, BOPP films are widely used in snack packaging due to their excellent moisture resistance and printability. This competitive landscape forces CPP film manufacturers to continuously innovate to maintain relevance.

Cast Polypropylene Packaging Films Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 6.8 billion |

|

Forecast Year Market Size (2035) |

USD 11.5 billion |

|

Regional Scope |

|

Cast Polypropylene Packaging Films Market Segmentation:

Application Segment Analysis

The food packaging segment, part of the application, is anticipated to garner the largest share of 42.5% in the cast polypropylene packaging films market by the end of 2035. The segment’s upliftment is highly driven by its importance for significantly maintaining product quality, freshness, and safety through excellent clarity, high seal integrity, and superior moisture barriers. According to official statistics published by Invest India in November 2023, the food and beverage packaging sector in India accounts for a yearly growth rate of 14.8%, which is further expected to reach USD 86 billion by the end of 2029. Besides, the Ministry of Food Processing Industries (MoFPI) introduced the Pradhan Mantri Kisan SAMPADA Yojana (PMKSY), which has leveraged USD 1.2 billion that has benefited 2.8 million farmers and also generated 5.4 million direct and indirect job opportunities in the food processing sector, thus boosting the segment’s growth.

Type Segment Analysis

The retort CPP films sub-segment in the cast polypropylene packaging films market is projected to account for the second-largest share during the forecast period. The sub-segment’s growth is highly fueled by its ability to withstand high-temperature sterilization processes. These films are widely used in ready-to-eat meals, soups, sauces, and pharmaceutical packaging, where durability and safety are paramount. Additionally, these maintain structural integrity during retort processing, ensuring that food and drug products remain uncontaminated and shelf-stable. The demand for retort CPP films is driven by the global rise in convenience food consumption, particularly in urban areas where packaged meals are increasingly preferred. Regulatory bodies such as the Europe Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) mandate strict packaging standards for sterilized products, further boosting adoption.

Thickness Segment Analysis

By the end of the stipulated timeline, the 20-30 micron sub-segment, which is part of the thickness segment, is expected to hold the third-largest share in the cast polypropylene packaging films market. The sub-segment’s development is highly attributed to maintaining an optimal balance between strength, flexibility, and cost-effectiveness, making it suitable for diversified applications such as food packaging, textiles, and pharmaceuticals. Films in this particular range provide sufficient barrier properties against moisture and oxygen while maintaining clarity and heat sealability, which are essential for consumer appeal and product safety. Besides, food packaging is the primary driver of demand for 20–30 micron CPP films, particularly in snack foods, bakery items, and frozen products.

Our in-depth analysis of the cast polypropylene packaging films market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Type |

|

|

Thickness |

|

|

End use |

|

|

Functionality |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cast Polypropylene Packaging Films Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the cast polypropylene packaging films market is anticipated to hold the highest share of 34.5% by the end of 2035. The market’s upliftment in the region is highly attributed to an increase in urbanization, a rise in packaged food demand, pharmaceutical extension, and government-funded sustainability strategies. According to official statistics published by NLM in November 2025, there has been a massive growth in the modernized grocery retail industry, particularly in Thailand, Indonesia, the Philippines, and Malaysia, with market sizes amounting to USD 25,747 million, USD 19,684 million, USD 16,876 million, and USD 7,910 million. This growth has resulted in a huge demand for packaged foods in these nations, which is positively uplifting the market’s exposure in the overall region. Besides, the continuous supply of propylene polymers is also bolstering the cast polypropylene packaging films market’s growth in the overall region.

2024 Propylene Polymers Export and Import Analysis in the Asia Pacific

|

Countries |

Export (USD) |

Import (USD) |

|

Saudi Arabia |

5.0 billion |

159 million |

|

South Korea |

4.6 billion |

183 million |

|

China |

2.7 billion |

4.6 billion |

|

Singapore |

2.3 billion |

563 million |

|

Thailand |

1.0 billion |

605 million |

|

Japan |

944 million |

592 million |

|

India |

470 million |

1.8 billion |

|

Vietnam |

722 million |

1.4 billion |

Source: OEC

The cast polypropylene packaging films market in China is growing significantly, owing to the presence of huge pharmaceutical and food industries, government-funded sustainability programs, packaging advancements and technologies, and suitable packaging processes. As per an article published by the International Review of Economics & Finance in November 2023, notably 70% of residents in the country are deliberately willing to initiate a premium payment for green express packaging, with the average premium amounting to USD 0.36, which is 15.8% of the overall expense for green packaging services. Moreover, residents are highly focused on express package recycling, based on the provision of USD 0.13 or 6.9% of the total cost per package. Therefore, with such objectives, the market is gradually expanding in the overall country.

The rise in customer demand, packaging advancements, comprehensive industrial transformation, booming pharmaceutical and food industries, along with expansion in e-commerce services, are responsible for bolstering the cast polypropylene packaging films market in India. According to official statistics published by the IBEF Organization in November 2025, the food processing industry significantly accounted for 8.8% and 8.3% of gross value added (GVA) in agriculture and manufacturing, while effectively contributing 13% of domestic exports and 6% of total industrial investment. Besides, modifications in consumption patterns and rising urbanization are increasingly driving food consumption, leading to an expected growth in the industry to USD 1.2 trillion by the end of 2026, which in turn is proliferating the market’s growth in the overall country.

Food Processing Growth Analysis in India (2023-2047)

|

Year |

Growth (USD Billion) |

|

2023 |

307 |

|

2030 |

700 |

|

2035 |

1,100 |

|

2040 |

1,500 |

|

2045 |

1,900 |

|

2047 |

2,150 |

Source: IBEF Organization

Europe Market Insights

Europe in the cast polypropylene packaging films market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the robust demand for sustainable pharmaceuticals and food packaging. Additionally, the regional Horizon Europe program and Europe Green Deal have also been crucial for ensuring sustainable packaging innovations, leading to increased cast polypropylene packaging films market growth. According to official statistics published by NLM in January 2023, the Europe Strategy for Plastic in a circular economy readily outlined suitable targets for diminishing plastic consumption and enhancing the recycled content, intended to account for 55% of recyclable and reusable plastic packaging by the end of 2030. Therefore, with all these factors, there is a huge growth opportunity for the market in the region.

The cast polypropylene packaging films market in Germany is gaining increased traction, owing to robust industrial capacity, government-funded sustainability programs, innovative packaging technologies, and green packaging solutions. As per an article published by NLM in May 2023, the plastic waste management responsibility is significantly shared between producers and consumers in the overall region, with customers generating 40% of plastic waste and producers responsible for the remaining 60%. Besides, an estimated 26 million tons of post-consumer plastic garbage has been produced in the country, of which 30% has been recycled and 40% burned with electricity extraction. Moreover, the country has utilized Deposit Return Systems (DRS), accounting for a 98% throughput, thus positively impacting the market’s development.

The presence of strong sustainability policies, circular economy strategies, reduction in single-use plastics, and support provision in recyclable packaging are certain factors that are driving the cast polypropylene packaging films market’s demand in France. As stated in an article published by the CMS Law in February 2024, the country’s circular economy law has effectively established a proportion of 5% of reutilized packaging as of 2023, which is further projected to increase to 10% by the end of 2027. Additionally, in 2025, 100% of plastics have been recycled, along with 77% of plastic bottles for beverages collected, which is expected to surge to 90% by the end of 2029. Besides, the French Alternative Energies and Atomic Energy Commission has enabled stringent regional environmental and safety standards, which denotes an optimistic outlook for the market’s development.

North America Market Insights

North America in the cast polypropylene packaging films market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by an increase in the demand for e-commerce logistics, pharmaceuticals, and food packaging, along with the government’s emphasis on advanced manufacturing technologies and sustainable packaging. According to official statistics published by the U.S. Plastic Pact Organization in 2026, 60% to 70% of consumers tend to pay more for sustainable packaging. In addition, 52% of consumers are eager to purchase products with sustainable packaging, while 55% are extremely concerned about the environmental impact of product packaging. Therefore, with the increased focus on sustainability and environmental awareness, there is a huge growth opportunity for the market in the overall region.

The cast polypropylene packaging films market in the U.S. is gaining greater exposure, driven by a surge in demand for food and beverage packaging, government sustainability strategies, and growth in pharmaceutical packaging. As per an article published by the CSIS Organization in September 2025, an estimated 90% of prescriptions are filled in the country, significantly representing 13.1% of overall drug expenditure, owing to low cost. Besides, the biopharmaceutical sector is a crucial pillar of the country’s economy, accounting for roughly 3.4% of the gross domestic product (GDP) as of 2022 and providing millions of high-wage jobs in distribution, production, and research. Moreover, the country almost provided USD 50 billion in yearly National Institutes of Health funding with local and state strategies for creating innovations, thus making it suitable for enhancing the cast polypropylene packaging films market.

The aspects of government funding for clean packaging technologies, expansion of e-commerce packaging, and increased focus on diminishing plastic waste are responsible for bolstering the cast polypropylene packaging films market in Canada. Based on government estimates published by the Government of Canada in October 2025, Environment and Climate Change Canada has generously supported 55 projects with more than USD 10 million through funding for Advancing a Circular Plastics Economy for Canada and the Zero Plastic Waste Initiative. This particular funding opportunity has been leveraged by over USD 7 million in private and public funds, further supported by awareness and education raising, testing of practices and technologies, circular solutions, actions to combat and lower plastic pollution and waste, and community clean-ups. Therefore, based on such funding and objectives, the market is continuously expanding in the overall country.

Key Cast Polypropylene Packaging Films Market Players:

- Taghleef Industries (UAE)

- Jindal Poly Films Limited (India)

- Polyplex Corporation Limited (India)

- Oben Holding Group (Peru)

- Treofan Group (Germany)

- Mitsui Chemicals Tohcello, Inc. (Japan)

- Toray Industries, Inc. (Japan)

- Uflex Ltd. (India)

- LC Packaging International BV (Netherlands)

- Innovia Films (UK)

- Amcor Plc (Australia)

- Cosmo Films Ltd. (India)

- SRF Limited (India)

- Polibak (Turkey)

- Schur Flexibles Holding GmbH (Austria)

- Sealed Air Corporation (U.S.)

- Berry Global Group, Inc. (U.S.)

- Daelim Industrial Co., Ltd. (South Korea)

- Scientex Berhad (Malaysia)

- Toyobo Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Taghleef Industries is one of the largest global producers of CPP films, with a strong presence across Europe, the Middle East, and Asia. The company emphasizes innovation in metalized and retort CPP films, catering to food and pharmaceutical packaging. Its sustainability initiatives, including recyclable film solutions, position it as a leader in eco-friendly packaging.

- Jindal Poly Films Limited is a major Indian manufacturer with a diversified product portfolio, including CPP films for food and textile packaging. The company has expanded globally through acquisitions and capacity enhancements, strengthening its market share. Its focus on cost-efficient production and export competitiveness makes it a key player in the Asia Pacific.

- Polyplex Corporation Limited operates across multiple continents, offering CPP films with strong barrier properties for food and drug packaging. The company invests heavily in R&D for advanced polymer solutions, ensuring compliance with international safety standards. Its global footprint, spanning the U.S., Europe, and Asia, supports steady revenue growth.

- Oben Holding Group is a Latin America-based leader in flexible packaging films, including CPP films. The company has expanded operations into North America and Europe, enhancing its international presence. Its strategy focuses on regional diversification and sustainable packaging innovation, driving growth in emerging markets.

- Treofan Group is a Europe-based pioneer in polypropylene films, with a strong focus on high-performance CPP films. The company is known for its advanced manufacturing technologies and partnerships with major food and pharmaceutical brands. Its emphasis on quality, innovation, and sustainability ensures a competitive edge in the Europe-specific market.

Here is a list of key players operating in the global cast polypropylene packaging films market:

The worldwide cast polypropylene packaging films market is highly competitive, with leading manufacturers pursuing capacity expansion, product innovation, and sustainability initiatives. Companies such as Taghleef Industries, Jindal Poly Films, and Amcor Plc are investing in eco-friendly CPP films to meet regulatory demands and consumer preferences for sustainable packaging. Besides, tactical partnerships, mergers, and acquisitions are common, enabling firms to strengthen their global footprint. For instance, in June 2024, Saica Group and Mondelez successfully joined forces to unveil the latest paper-based product, readily targeted to multipack products for the chocolate, biscuits, and confectionery industries. Additionally, this particular packaging has been designed to be recyclable in the paper waste stream, thereby making it suitable for the boosting the cast polypropylene packaging films industry globally.

Corporate Landscape of the Cast Polypropylene Packaging Films Market:

Recent Developments

- In November 2025, UFlex Ltd planned to develop a 54,000 tons per year biaxially oriented polypropylene line at the Dharwad complex in India’s south Karnataka state by investing USD 79 million to enhance global packaging films capacity to 690,160 tons per year.

- In November 2025, TOPPAN Inc., along with its India-specific subsidiary, TOPPAN Speciality Films Private Limited, successfully installed a hybrid manufacturing line, which is capable of producing both biaxially-oriented polyethylene (BOPE) and biaxially-oriented polypropylene (BOPP) film.

- In July 2025, Stonepeak declared that it has significantly entered into a suitable agreement under which the organization acquired an estimated 50% of a co-controlling stake in IFCO Group from a wholly-owned subsidiary of the Abu Dhabi Investment Authority to utilize more than 400 million reusable packaging containers and enable over 2.5 billion yearly shipments of vegetables, fruits, and other perishables.

- Report ID: 8408

- Published Date: Mar 03, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.