Bio-polylactic Acid (PLA) Market Outlook:

Bio-polylactic Acid (PLA) Market size was valued at USD 2.5 billion in 2025 and is expected to reach USD 5.1 billion by the end of 2035, growing at around 7.4% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of bio-polylactic acid is estimated at USD 2.6 billion.

The growth of the bio-polylactic acid market is the direct outcome of increasing demand for sustainable and bio-based materials across packaging, textiles, consumer goods, agriculture, medical devices, and 3D printing applications. The rising environmental awareness, stricter regulations on certain conventional plastics, and corporate sustainability commitments are encouraging manufacturers to adopt biodegradable and compostable alternatives such as PLA. According to an article published by the National Institute of Health in October 2022, sustainable packaging is highly essential since conventional packaging materials, especially plastics, contribute to environmental pollution due to low recycling rates and slow biodegradation. The report also mentions that the use of bio-based, biodegradable, recyclable, and reusable materials offers a sustainable solution that reduces waste, conserves resources, and supports environmental protection, thus encouraging the use of PLA-based packaging.

Key Bio-polylactic Acid (PLA) Market Insights Summary:

Regional Highlights:

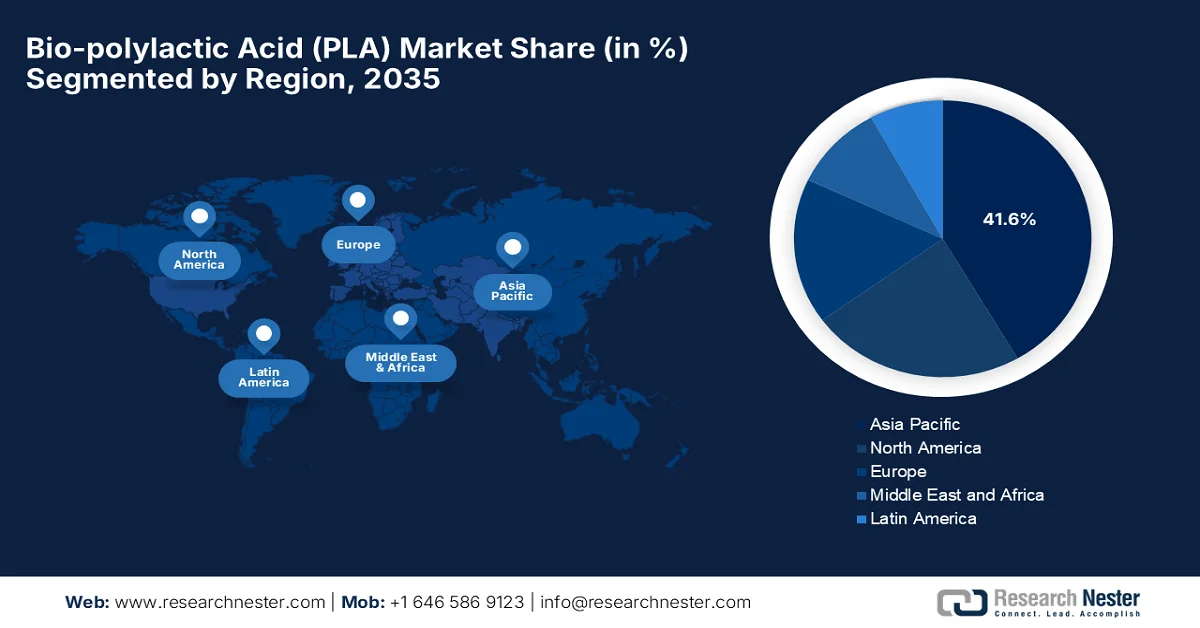

- By 2035, the asia pacific region is projected to capture 41.6% share of the bio-polylactic acid (pla) market, fostered by government mandates and bans on single-use plastics across major growing economies

- During the 2026-2035 period, north america is poised for notable expansion in revenue generation, attributed to rising consumer preference for sustainable products

Segment Insights:

- By 2035, the packaging segment is anticipated to account for 57.4% revenue share in the bio-polylactic acid (pla) market, supported by the expansion of e-commerce and food delivery services

- By 2035, the PLA resins segment is expected to secure a considerable revenue share, reinforced by increasing integration of PLA in advanced manufacturing processes requiring consistent material performance and scalable processing capabilities

Key Growth Trends:

- Expanding use in the food and beverage industry

- Growth of the 3D printing industry

Major Challenges:

- Limited heat resistance and performance constraints

- Insufficient industrial composting infrastructure

Key Players: NatureWorks LLC, TotalEnergies Corbion, Futerro SA, Sulzer Ltd., Zhejiang Hisun Biomaterials Co., Ltd (China).

Global Bio-polylactic Acid (PLA) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.5 billion

- 2026 Market Size: USD 2.6 billion

- Projected Market Size: USD 5.1 billion by 2035

- Growth Forecasts: 7.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, Canada, Germany, Japan, United Kingdom

- Emerging Countries: China, India, Brazil, Mexico, Russia

Last updated on : 16 June, 2026

Bio-polylactic Acid (PLA) Market - Growth Drivers and Challenges

Growth Drivers

- Expanding use in the food and beverage industry: The bio-polylactic acid (PLA) market is being driven by the food and beverage industry, owing to its usage in disposable cups, containers, trays, and food packaging due to its transparency, safety, and compostability. Increasing demand for sustainable packaging solutions among restaurants, retailers, and food delivery services supports the market’s upliftment. In May 2025, the article published by the U.S. Department of Agriculture reported that food and beverage manufacturing converts accounted for 16.8% of U.S. representing 15.4% of total manufacturing employment. The article also mentions that there were more than 42,000 food and beverage processing establishments in the U.S., and hence, the demand for sustainable packaging solutions continues to grow.

- Growth of the 3D printing industry: PLA is commonly used for 3D printing materials due to its ease of use, low warping characteristics, and renewable origin. Therefore, the increasing adoption of additive manufacturing in education, healthcare, and prototyping deliberately supports the bio-polylactic acid market growth. As per an article published by the National Institute of Health (NIH) in January 2023, PLA has become one of the most widely used materials in 3D printing, especially in the case of fused deposition modeling, due to its ease of processing, environmental friendliness, and attractive surface finish. Besides, the report also mentioned that the growing environmental concerns and advances in biopolymer production have increased PLA's industrial significance, wherein the strong market growth is propelled by its renewable origin and reduced carbon footprint when compared to conventional petroleum-based plastics.

- Agricultural feedstock abundance: Expanding production facilities in regions that are rich in corn and sugarcane are propelling a constant supply of raw materials for PLA production. Therefore, this abundant feedstock availability helps reduce supply chain risks and contributes to the long-term growth and exposure of the bio-polylactic acid market. In March 2024, the article published by the USDA released a plan with a main goal to strengthen the U.S. bioeconomy by improving biomass supply chains and expanding markets for biobased products. The strategy supports farmers, rural communities, and industries by increasing the use of agricultural, forest, and waste biomass for fuels, materials, and other sustainable products. In addition, the article underscores that the U.S. biobased products sector contributed a total of USD 489 billion to the economy in a year, demonstrating the scale and maturity of biomass-based industries, hence denoting a lucrative opportunity for the bio-polylactic acid (PLA) market to grow in the next decade.

Challenges

- Limited heat resistance and performance constraints: The bio-polylactic acid (PLA) market is facing severe technical challenges, especially its low heat resistance and brittle mechanical properties when compared to engineering plastics. The standard PLA softens at lower temperatures, which makes it unsuitable for high-heat applications such as hot beverage containers, automotive components, or microwave-safe packaging without modification. There are certain heat-resistant PLA grades and polymer blends that are being developed, but they increase production complexity and cost. The presence of these performance aspects limits the element’s use cases to applications such as cold food packaging, disposable items, and 3D printing filaments. Therefore, there is an urgent need for improvements in durability and thermal stability to be achieved at scale, until this PLA will face barriers in expanding into high-performance industrial applications.

- Insufficient industrial composting infrastructure: Another major burden for the bio-polylactic acid market is the absence of proper industrial composting infrastructure, which is required for proper PLA disposal. The PLA is generally marketed as biodegradable under industrial composting conditions, but most of the regions do not have adequate facilities to process it effectively. As a result, PLA products often end up in landfills or conventional recycling streams, where they do not degrade efficiently and can contaminate plastic recycling systems. Hence, this creates confusion among consumers and weakens the environmental value proposition of PLA. Therefore, the absence of standardized global waste management systems significantly limits the material’s circular economy potential.

Bio-polylactic Acid (PLA) Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.4% |

|

Base Year Market Size (2025) |

USD 2.5 billion |

|

Forecast Year Market Size (2035) |

USD 5.1 billion |

|

Regional Scope |

|

Bio-polylactic Acid (PLA) Market Segmentation:

Application Segment Analysis

Under the application segment, packaging is anticipated to garner the largest revenue share of 57.4% in the bio-polylactic acid market during the forecast period. The segment’s dominance is largely due to the expansion of e-commerce and food delivery services, which have significantly increased the demand for lightweight, durable, and disposable packaging solutions. The rising investments in terms of recyclable and compostable packaging infrastructure by retailers and brand owners are accelerating PLA adoption across the packaging industry. The International Trade Administration, in its 2024 report, disclosed that the global e-commerce market is expanding continuously, wherein B2B sales are projected to reach USD 36 trillion by the end of 2026 at a 14.5% CAGR. It also mentioned that APAC will dominate with 80% of the B2B market share, whereas Latin America and the Middle East show strong growth potential. On the B2C side, revenue is expected to hit USD 5.5 trillion by 2027, denoting a huge opportunity for the segment’s welfare.

Product Segment Analysis

By the end of 2035, the PLA resins segment is expected to grow at a considerable revenue share in the bio-polylactic acid (PLA) market. The increasing integration of PLA in advanced manufacturing processes that require consistent material performance and scalable processing capabilities is the main factor behind the segment’s leadership. The rising utilization of PLA resins in injection molding, thermoforming, and extrusion-based applications is strengthening their demand across diverse industrial sectors. In October 2024, TotalEnergies Corbion, at Fakuma 2024, highlighted the advancement of Luminy® PLA, which is a biobased plastic now engineered for durable, high-performance applications beyond single-use packaging. Luminy® PLA provides improved heat resistance, mechanical strength, and weatherability, and it is being applied to cosmetic jars, electronics, and dishwasher-safe products.

End user Segment Analysis

On the basis of end user food and beverage segment is forecasted to grow with a noteworthy share in the bio-polylactic acid (PLA) market during the discussed timeframe. The segment’s growth is mainly propelled by rising adoption of PLA in ready-to-eat meal solutions and convenience food formats, where manufacturers require materials that maintain product visibility and structural integrity during storage and transport. In addition, the increasing expansion of cold-chain logistics for perishable goods is encouraging the use of PLA-based packaging that supports efficient handling while maintaining product hygiene standards. For instance, in October 2023, SCGP reported that Fest is driving sustainable packaging innovation with solutions that are suitable for ready meals, chilled fresh meat, and vending machines. Its new products, i.e., Fest Fresh Pak and Fest Redi Pak, are made from renewable materials, ensuring durability, freshness, and thus supporting the growth of PLA-based packaging demand in the food and beverage sectors.

Our in-depth analysis of the bio-polylactic acid market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Product Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bio-polylactic Acid (PLA) Market - Regional Analysis

APAC Market Insights

The Asia Pacific bio-polylactic acid (PLA) market is anticipated to garner the highest share of 41.6% during the forecast period. The region’s dominance is mainly propelled by government mandates and bans on single-use plastics across major growing economies. The region's agricultural sector provides an abundant, localized supply of feedstocks such as sugarcane and cassava, which encourages major biopolymer producers to establish completely integrated manufacturing facilities closer to raw material sources. Based on the government data published in October 2025, Japan has set measurable targets under its resource circulation strategy for plastics, which includes reducing single-use plastics by 25% by 2030 and introducing approximately 2 million tons of bio-based plastics by 2030. Therefore, these structured policies and targets collectively encourage the adoption of sustainable materials such as bio-polylactic acid across industries.

The massive domestic investments in industrial-scale manufacturing facilities position the country as a major global production hub for biopolymers. The highly developed infrastructure in the textile, catering, and e-commerce packaging sectors provides a robust ecosystem for commercial adoption in the China bio-polylactic acid market. In June 2023, the article published by the Ministry of Commerce Regulations it require business operators in retail, e-commerce, catering, accommodation, and exhibitions to reduce and report single-use plastic usage. The law deliberately emphasizes compliance with national bans on non-degradable plastics, encourages reusable or recyclable alternatives, and mandates biannual reporting through a national system, thus making it suitable for bolstering the country’s market.

In India, the bio-polylactic acid is entering into a transformative phase of growth mainly due to rising corporate pivot toward eco-friendly materials. As consumer-packaged goods and fast-moving consumer goods companies are looking for compostable alternatives, the domestic packaging and textile industries are transitioning toward biodegradable formats such as plastic films and sheets. This surging demand is shifting the country from an import-reliant market to a localized production hub. As per the article published by Press Information Bureau (PIB) in January 2026, India convened a high-level consultation on using bioplastics for certain sachets, aiming to replace non-degradable plastics with sustainable alternatives. Therefore, stakeholders from MoEFCC, FSSAI, BIS, CIPET, and academia recommended prominent options such as PLA, the need for clear definitions of biodegradable materials, and standardized testing protocols, thus increasing the bio-polylactic acid (PLA) market’s growth potential.

North America Market Insights

The North America bio-polylactic acid (PLA) market is positioned for extensive growth as the consumer preference for sustainable products is on a surge. The region benefits from a robust and highly integrated agricultural infrastructure, utilizing vast domestic corn crops as the primary feedstock to maintain a reliable, large-scale supply chain. The region’s market is also supported by favorable state-level legislation, green procurement policies, and a well-established network of industrial composting facilities. The study by the U.S. Department of Agriculture in 2024 introduced biodegradable and recyclable PLA-CNC laminated films as eco-friendly food packaging materials. By coating cellulose nanocrystals with polyvinyl alcohol or carrageenan onto PLA substrates, researchers achieved multilayer films with dramatically improved oxygen and water vapor barrier properties, hence making it suitable for standard market growth.

The intense corporate focus on carbon reduction and strong consumer demand for eco-friendly packaging alternatives are responsibly driving the U.S. bio-polylactic acid market. The country’s supply chain fuels substantial adoption across the foodservice, medical device, and flexible packaging industries, in which brands are proactively swapping traditional plastics for compostable alternatives. According to the article published by the USDA in May 2026, corn is the dominant U.S. feed grain, which is making up more than 95% of total feed grain production and use, with almost 90 million acres planted annually. Besides, the crop serves as a key energy source in livestock feed, and it contributes nearly 45% of its use to fuel ethanol. Corn is also processed into food and industrial products such as starch, sweeteners, and corn oil. The U.S. is the world’s largest producer and exporter of corn, with major markets including Mexico, China, Japan, and Colombia, thus denoting a positive bio-polylactic acid (PLA) market outlook.

The Canada bio-polylactic acid market represents encouraging growth opportunities for both domestic and foreign players. The federal government’s zero plastic waste agenda and strict regulations targeting single-use conventional plastics are also propelling the country’s market growth. This regulatory environment is pushing the country’s extensive food service, retail packaging, and agricultural sectors to opt for these bio-based alternatives. The country is dependent on integrated supply chains with its North America based neighbors for raw material inputs, domestic interest is growing around utilizing Canada's abundant agricultural byproducts and forestry biomass as alternative feedstocks. Backed by corporate sustainability mandates from major domestic consumer brands and expanding municipal organic waste collection programs, the market is steadily establishing a stronger regional footprint for sustainable biopolymer application and circular economy integration.

Europe Market Insights

The circular economy goals and the presence of key market players are certain visible trends reshaping the growth dynamics of Europe bio-polylactic acid market. It compels consumer brands, automotive manufacturers, and agricultural sectors to make a transition away from fossil-fuel-based plastics. The region's market is highly focused on advanced waste management infrastructure, organic recycling, and industrial composting integration to ensure proper end-of-life processing. In January 2025, the EU Regulation (EU) 2025/40 on packaging and packaging waste established a legal framework under the region’s green deal to ensure that all packaging placed on the regional market is reusable or recyclable by 2030. It introduces stricter requirements on packaging design, waste reduction, recyclability, and recycled content, reinforcing the transition toward a circular economy and reducing dependence on virgin fossil-based plastics.

A heavy focus on advanced industrial engineering, high-tech compounding, and precision polymer modification is fueling the growth of the bio-polylactic acid (PLA) market in Germany. The domestic chemical processors and specialized compounders lead the region in blending PLA with performance-enhancing additives to create durable, flame-retardant, and structurally reinforced materials that are suitable for precision components in automotive interiors and electronic housings. For instance, in June 2024, researchers at the Fraunhofer IAP developed a bio-based plastic film made from PLA, which offers a sustainable alternative to LDPE for shopping and garbage bags. Besides, the team covalently linked polyether plasticizers to PLA chains and created a flexible, recyclable material that avoids the common issue of plasticizer migration. This new PLA film is at least 80% bio-based, cost-efficient to produce, and compatible with conventional processing equipment, thus making it accessible for medium-sized manufacturers.

The UK bio-polylactic acid market is witnessing notable expansion from a niche segment within the broader sustainable packaging and materials ecosystem, supported by strong policy frameworks. In addition, market activity is primarily driven by innovation-focused SMEs and research collaborations that are focused on material development, bio-based polymer applications, and performance enhancement for packaging and consumer goods. At the application level, demand for PLA is very closely associated with food service, retail packaging, and personal care sectors, in which companies are making a shift toward compostable and lower-carbon material alternatives in response to regulatory and brand sustainability commitments. The country’s market also benefits from expanding infrastructure planning for food waste collection and industrial composting, which supports end-of-life treatment pathways for compostable bioplastics under controlled conditions.

Key Bio-polylactic Acid (PLA) Market Players:

- NatureWorks LLC (U.S.)

- TotalEnergies Corbion (Netherlands)

- Futerro SA (Belgium)

- Sulzer Ltd. (Switzerland)

- Zhejiang Hisun Biomaterials Co., Ltd. (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- NatureWorks LLC is one of the leading producers of bio-polylactic acid, which is best known for its Ingeo™ biopolymer platform. The company has established a strong vertically integrated production model covering fermentation, lactic acid production, and PLA polymerization.

- TotalEnergies Corbion is a joint venture combining TotalEnergies’ industrial scale along with Corbion’s biopolymer knowledge. The firm has positioned itself strongly in the circular economy space by focusing extensively on compostable plastics and lifecycle carbon reduction.

- Futerro SA is a company that specializes in lactic acid and PLA production technologies. The company is best known for its integrated sugar-to-PLA model and its focus on fully bio-based and recyclable materials.

- Sulzer Ltd. has registered itself as a key technology provider in the PLA value chain, which is offering engineering solutions, process technologies, and equipment for PLA production. Sulzer plays a remarkable role in enabling efficient and scalable PLA manufacturing with the help of its advanced polymerization and processing technologies.

- Zhejiang Hisun Biomaterials Co., Ltd. is an integrated value chain covering lactic acid, lactide, and PLA resin production, and has achieved full-scale industrialization of PLA through proprietary technologies. The firm is recognized as one of the first listed PLA-focused companies in China and plays a leading role in domestic PLA standard-setting.

Here is a list of key players operating in the global bio-polylactic acid (PLA) market:

The bio-polylactic acid market hosts a few global leaders capturing a significant share of production capacity. The pioneers, such as NatureWorks LLC and TotalEnergies Corbion, dominate in terms of large-scale, vertically integrated manufacturing and strong global distribution networks. Apart from this, Asia-based producers are continuously expanding with certain cost-efficient feedstock access and strong domestic demand. Meanwhile, Europe specific players are highly focused on innovation in circular and compostable materials. Capacity expansions and partnerships with packaging and consumer goods companies to accelerate commercialization are certain strategies opted for by the leading market players. For instance, in December 2024, Emirates Biotech announced that it selected Sulzer’s advanced PLA technology to build the world’s largest polylactic acid production facility in the UAE, with a planned total capacity of 160,000 tons per year.

Corporate Landscape of the Market:

Recent Developments

- In February 2026, TotalEnergies Corbion announced the launch of an embossed PLA water bottle, which is a label-free PLA water bottle in collaboration with Sansu, and it is designed to simplify recycling and support circular packaging systems.

- In December 2025, Futerro S.A. announced that it submitted environmental authorization and building permit applications for its future biorefinery in Port-Jérôme-sur-Seine. This project aims to produce lactic acid, lactide, and PLA, solidifying Europe’s transition to bio-based, recyclable, and compostable plastics.

- Report ID: 8617

- Published Date: Jun 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.