Bearing Market Outlook:

Bearing Market size was valued at USD 59.43 billion in 2025 and is projected to reach USD 130.55 billion by 2036, growing at a CAGR of 7.14% during the forecast period, i.e., 2026-2036. In 2026, the industry size of bearing is evaluated at USD 65.50 billion.

Industrial automation and the rapid adoption of Industry 4.0 technologies have emerged as the primary growth drivers of the global bearing market. As manufacturing facilities evolve into highly connected, machine-intensive environments, the need for precision, speed, reliability, and uninterrupted operations has significantly increased, directly accelerating demand for advanced bearing solutions. Modern automated systems including industrial robots, CNC machinery, automated conveyors, and smart production lines, depend heavily on high-performance bearings to deliver smooth motion, high load capacity, and operational accuracy under continuous usage conditions. As manufacturers increasingly prioritize productivity, efficiency, and reduced downtime, the demand for durable and technologically advanced bearings continues to rise across industries.

In parallel, the integration of IoT and smart manufacturing technologies is transforming conventional bearings into intelligent components equipped with sensors capable of monitoring temperature, vibration, lubrication, and wear conditions in real time. These smart bearings enable predictive maintenance, reduce unexpected equipment failures, and improve overall operational efficiency, further strengthening their value proposition in automated industrial ecosystems. The strong momentum in global industrial robot installations further highlights the accelerating shift toward automation-driven manufacturing. Recent industry data indicates that more than 4.28 million industrial robots are currently operating worldwide, reflecting a 10% increase year-over-year, while annual robot installations have surpassed 500,000 units for three consecutive years. Asia accounts for nearly 70% of new robot deployments, followed by Europe at 17% and the Americas at 10%, underscoring the widespread and sustained adoption of automation technologies globally. Overall, the continued expansion of industrial automation, robotics, and smart manufacturing is positioning Industry 4.0 as the most significant catalyst driving growth in the global bearing market, as industries increasingly require high-performance, reliable, and intelligent bearing systems to support next-generation manufacturing operations.

Key Bearing Market Insights Summary:

Regional Highlights:

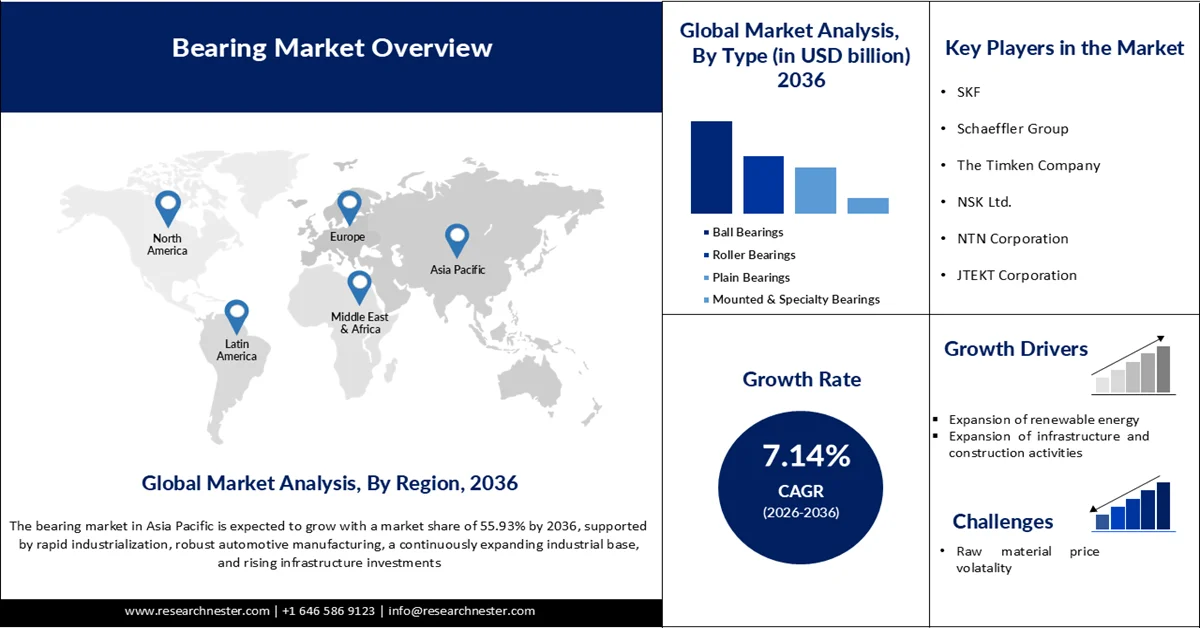

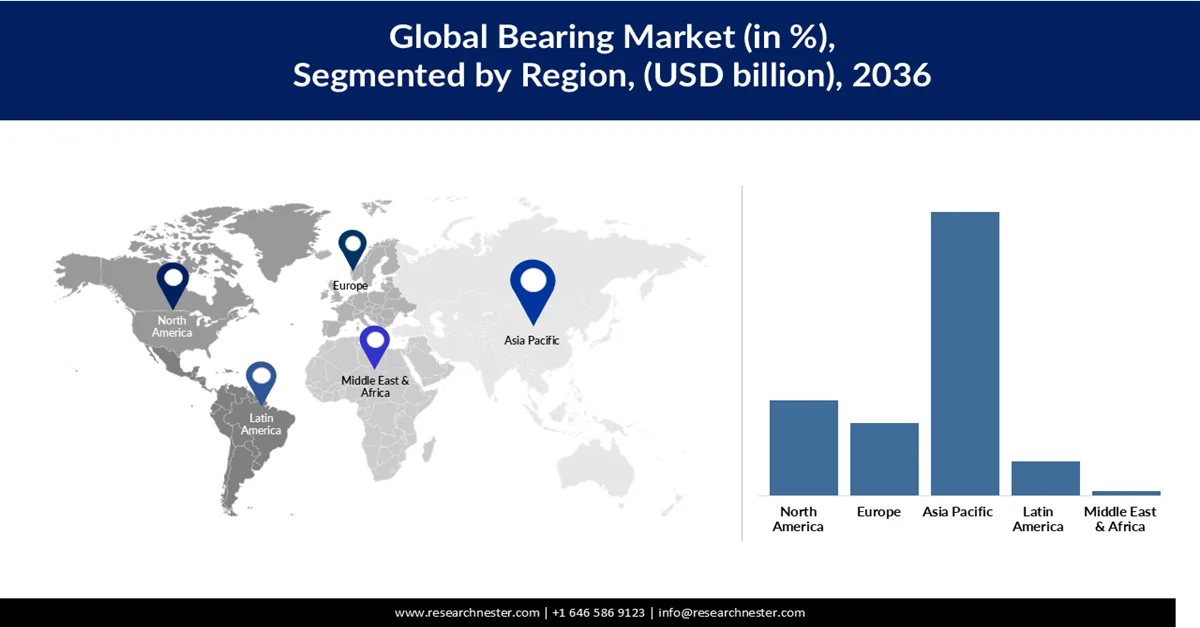

- The Asia Pacific region is anticipated to command 55.93% of the bearing market share by 2036, impelled by rapid industrialization, expanding automotive manufacturing, rising infrastructure investments, and increasing demand for high-performance bearings across industrial machinery, energy, and transportation sectors

- North America is forecast to capture 18.71% share of the market during 2026-2036, stimulated by industrial recovery, accelerating electrification, and the expansion of advanced manufacturing and precision engineering capabilities

Segment Insights:

- The ball bearings segment is projected to secure 43% share of the bearing market by 2036, driven by their ability to reduce friction, ensure smooth motion, and deliver reliable high-speed performance across industrial and automotive applications

- The grease segment is expected to account for around 76% share by 2036 in the market, propelled by increasing demand for effective lubrication, sealing protection, reduced leakage, and extended service intervals in industrial systems

Key Growth Trends:

- Expansion of renewable energy

- Expansion of infrastructure and construction activities

Major Challenges:

- Raw material price volatility

- The availability of low-cost substitutes

Key Players: SKF (Sweden), Schaeffler Group (Germany), The Timken Company (U.S.), NSK Ltd. (Japan), NTN Corporation (Japan), JTEKT Corporation (Japan), Nachi-Fujikoshi Corp. (Japan), RBC Bearings (U.S.), MinebeaMitsumi Inc. (Japan), C&U Group (China).

Global Bearing Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 59.43 billion

- 2026 Market Size: USD 65.50 billion

- Projected Market Size: USD 130.55 billion by 2036

- Growth Forecasts: 7.14% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Asia Pacific (55.93% Share by 2036)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, India

- Emerging Countries: India, South Korea, Vietnam, Brazil, Mexico

Last updated on : 20 May, 2026

Bearing Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of renewable energy: Wind energy, in particular, plays a dominant role, as turbines rely on multiple high-value bearings, including main shaft, gearbox, and generator bearings, to operate under heavy mechanical loads and highly variable conditions. This demand is reinforced by the rapid scale of wind energy deployment. According to the U.S. Department of Energy, global offshore wind capacity alone reached 59,009 MW across 292 operating projects, highlighting the expanding installed base of turbine systems that require precision bearings for reliable operation. In the United States, wind energy is already a well-established sector with over 120 GW of installed capacity, underscoring the large-scale infrastructure driving bearing consumption.

Reliability data from the U.S. Department of Energy further shows that bearing performance is critical to turbine operations, with studies indicating that approximately 76% of wind turbine gearbox failures are caused by bearing-related issues, making them the single most significant failure component in drivetrain systems. With rising global investment in renewable energy projects, demand for bearings is increasing not only in scale but also in technological sophistication. Offshore and remote installations require highly durable, corrosion-resistant, and low-maintenance designs, encouraging manufacturers to develop advanced materials and high-performance engineering solutions.

Furthermore, wind turbines are designed for long operational lifespans, often around 20 years, creating sustained demand for maintenance, repair, and replacement components over time. This strengthens the aftermarket segment and ensures recurring demand even after initial installation cycles. As countries continue to expand clean energy infrastructure, the bearing industry is benefiting from large-scale renewable deployment and an increasing emphasis on efficiency, reliability, and lifecycle performance, driving a shift toward specialized, high-performance bearing technologies. - Expansion of infrastructure and construction activities: According to an Organization for Economic Co-operation and Development study, the global construction sector was valued at approximately USD 14.7 trillion in 2024 and is expected to maintain strong growth momentum, with infrastructure emerging as the fastest-growing segment. In parallel, global infrastructure investment requirements are projected to reach nearly USD 106 trillion by 2040, reflecting the significant scale of upcoming developments in transportation, energy, and urban infrastructure. This rising investment is accelerating the deployment of construction machinery such as excavators, cranes, and loaders, all of which depend on heavy-duty bearings to operate efficiently under high-load and demanding working conditions. As infrastructure projects continue to expand worldwide, the demand for high-performance and durable bearings used in construction equipment and transport systems is increasing substantially. In addition, the growing installed base of machinery is creating long-term aftermarket opportunities through regular maintenance and replacement cycles. Consequently, increasing infrastructure and construction spending is driving both the volume and value demand for bearings, positioning the sector as a key growth driver for the global bearing market.

- Growth of the automotive and electric vehicle (EV) industry: In conventional automobiles, bearings are widely used in key systems such as engines, transmissions, wheels, and steering assemblies to minimize friction, improve durability, and enhance overall vehicle performance. Consequently, rising global vehicle production directly contributes to increased demand for bearings. The rapid transition toward electric vehicles is further accelerating bearing market growth while simultaneously transforming product requirements. EVs require advanced bearing solutions capable of operating at higher speeds, generating lower noise levels, and delivering superior energy efficiency, especially in electric motors and drivetrain systems. In addition, the adoption of electrically insulated and high-precision bearings is increasing to meet the unique operational demands of EV technologies.

Ongoing advancements in automotive engineering, including electrification, lightweight vehicle design, and higher performance standards, are also driving demand for specialized and high-performance bearings. At the same time, the expanding global vehicle parc continues to generate steady aftermarket demand for maintenance and replacement components. Overall, the continued growth of both conventional and electric vehicles is strengthening the bearing market by increasing demand volumes and encouraging technological innovation, making the automotive industry one of the key growth engines for the global bearing sector.

Challenges

- Raw material price volatility: Bearing production depends heavily on steel and specialty alloys. As a result, fluctuations in raw material prices have a direct impact on manufacturing costs and overall profitability. One of the primary concerns is the frequent instability in steel prices across different regions and time periods. Recent industry trends indicate that steel prices in 2025 experienced uneven movements across major markets, with month-on-month increases observed in countries such as India, China, and the United States, while certain markets also recorded year-on-year declines. These inconsistent pricing patterns highlight the unpredictable nature of raw material costs within the industry. Such volatility creates significant operational and financial challenges for bearing manufacturers. Unstable input costs make it difficult to maintain consistent product pricing, safeguard profit margins, and effectively plan long-term investments or expansion strategies. In addition, sudden increases in raw material prices can raise production expenses and disrupt supply chain stability, further affecting bearing market competitiveness.

- The availability of low-cost substitutes: In several industrial and automotive sectors, alternatives such as bushings and plain bearings are increasingly used in place of rolling bearings, especially in applications where high precision, speed, or heavy load capacity is not essential. These substitutes are generally simpler in design, require less complex manufacturing processes, and are easier to install, making them a cost-effective choice for budget-conscious end users. This growing preference for lower-cost alternatives limits the growth potential of standard and low-end bearing segments. As customers shift toward more economical solutions, bearing manufacturers face increasing pricing pressure and reduced profit margins.

Bearing Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2036 |

|

CAGR |

7.14% |

|

Base Year Market Size (2025) |

USD 59.43 billion |

|

Forecast Year Market Size (2036) |

USD 130.55 billion |

|

Regional Scope |

|

Bearing Market Segmentation:

Type Segment Analysis

The ball bearings segment is expected to hold 43% of the bearing market share by 2036 due to their ability to reduce friction, support smooth motion, and deliver reliable high-speed performance across a wide range of industrial and automotive applications. Among them, deep groove ball bearings hold a dominant position owing to their high efficiency, durability, low maintenance requirements, and versatility. Their increasing adoption in advanced machinery, electric vehicles, and automated industrial systems is further accelerating market expansion, making ball bearings a key contributor to the global bearing industry's growth and technological advancement. In June 2025, SKF introduced Energy Efficient DGBB for small industrial motors at the ISEA Tech & Innovation Summit in Delhi, delivering 25%+ lower frictional moment, up to 2x bearing life, and over 25% CO₂ reduction, validated by Indian OEMs. At Agritechnica October 2025 (Hanover), SKF also showcased DuraPro DGBB for tractor drivetrains, offering 2x lifespan and 20% higher load capacity through advanced hardening and surface treatment. These advancements position DGBB to benefit from electrification and sustainability trends, thereby improving energy efficiency and extending operational uptime across industrial and agricultural applications.

Lubrication Type Segment Analysis

The grease segment is expected to account for the largest share of around 76% by 2036 in the bearings application segment market due to its ability to provide effective lubrication, sealing protection, reduced leakage, and longer service intervals. Its semi-solid composition of oil, thickener, and performance additives makes it highly suitable for applications operating under moderate-to-high loads and varying environmental conditions. Widely used in electric motors, wheel hubs, conveyors, and agricultural machinery, grease lubrication enhances bearing reliability, minimizes maintenance requirements, and improves equipment lifespan. The growing demand for low-maintenance and high-performance industrial systems is further increasing the adoption of grease-lubricated bearings across multiple industries. Recent advancements in grease lubrication technologies are further supporting growth in the global bearing market by improving equipment reliability, operational efficiency, and maintenance performance in demanding environments. In October 2025, SKF introduced LGCC 2 grease, specifically engineered for extreme cold conditions to maintain film strength and enhance equipment uptime in sub-zero operations. The company also upgraded its Bearing Grease Selection Tool within its Product Select platform, enabling more accurate and data-driven lubricant selection.

Similarly, at Maintenance Dortmund 2026, Schaeffler AG showcased its Arcanol lubricant portfolio, developed to minimize friction and wear while extending service intervals. These innovations reinforce the importance of grease lubrication in modern bearing applications by enabling reliable, low-maintenance, and cost-efficient performance across challenging industrial operating conditions.

Application Segment Analysis

Automotive applications are playing a major role in driving the global bearing market, as modern vehicles increasingly require compact, high-speed, and low-friction bearings for powertrains, wheel hubs, transmissions, and chassis systems. The rapid growth of electric vehicles (EVs) is further increasing demand for advanced bearing solutions capable of improving e-axle efficiency, handling higher torque, and supporting effective thermal management. On 26 February 2026, SKF announced SKF Vertevo as the future name of its independent automotive business, highlighting its strategic focus on strengthening leadership in EV powertrain technologies, with a planned public listing in Q4 2026. In May 2024, NTN Corporation developed large-diameter deep groove ball bearings for coaxial e-axles that achieved a dmn value of 1.5 million and reduced torque by more than 50%, supporting high-speed and energy-efficient EV performance. These advancements are accelerating innovation and efficiency improvements in automotive bearing systems, reinforcing the critical role of bearings in supporting the global transition toward vehicle electrification and next-generation mobility solutions.

Our in-depth analysis of the bearing market includes the following segments:

|

Segments |

Subsegments |

|

Type |

|

|

Lubrication Type |

|

|

Application |

|

|

Material |

|

|

Motion Type |

|

|

Size |

|

|

Sales Channel |

|

|

Cage |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Bearing Market - Regional Analysis

Asia Pacific Market Insights

Asia Pacific is projected to account for the largest share of the global bearing market, representing 55.93% by 2036. The region’s dominance is supported by rapid industrialization, robust automotive manufacturing, a continuously expanding industrial base, and rising infrastructure investments. Additionally, growing demand for high-performance bearings across sectors such as industrial machinery, energy, and transportation is further contributing to bearing market growth in the region. Countries like China, India, and Japan fuel demand through expanding industries, large-scale construction projects, and increasing adoption of advanced technologies. Government initiatives and cost advantages further strengthen the region’s appeal for local production and partnerships.

The bearing market in China is witnessing steady growth, supported by strong industrial expansion and increasing demand from automotive, machinery, and infrastructure sectors. A key factor shaping this growth is the implementation of the Environmental Protection Law of the People's Republic of China, which enforces strict controls on industrial emissions, waste discharge, and resource utilization. The law requires environmental impact assessments, adherence to pollution limits, and imposes penalties for non-compliance, particularly in energy- and material-intensive industries such as bearing manufacturing. As a result, bearing manufacturers are increasingly required to adopt cleaner production processes, advanced emission control systems, and more efficient resource management practices. While these compliance requirements may raise operational costs in the short term, they are also driving technological upgrades and encouraging the development of high-efficiency, environmentally friendly bearings. This is particularly evident in automotive and industrial applications, where demand is rising for energy-efficient and low-emission components.

Furthermore, stringent regulatory standards are contributing to industry consolidation, as smaller manufacturers face challenges in meeting compliance requirements, while larger, technologically advanced players strengthen their bearing market position. Overall, these regulatory-driven shifts, combined with China’s strong industrial base and growing end-use demand, are supporting the continued expansion of the country’s bearing market.

The bearing market in India is experiencing steady growth, supported by rapid industrialization, expanding automotive production, and increasing infrastructure development. A key factor influencing this growth is the implementation of the Environment (Protection) Act, 1986, which provides a comprehensive framework for controlling industrial pollution, managing hazardous substances, and enforcing environmental compliance across manufacturing sectors. Under this regulation, bearing manufacturers are required to comply with strict norms related to emissions, waste disposal, and chemical handling in processes such as machining, coating, and lubrication. This has encouraged the adoption of cleaner production technologies, sustainable materials, and improved process efficiencies within the industry.

Although compliance with environmental standards increases capital investment and operating costs, it also enhances product quality, operational efficiency, and environmental performance. As a result, organized and technologically advanced manufacturers are strengthening their market position, while smaller players face growing pressure to upgrade capabilities or consolidate. Overall, these regulatory developments, combined with strong end-use demand from automotive and infrastructure sectors, are supporting the sustained expansion of the bearing market in India, with increasing preference for durable, efficient, and environmentally compliant bearing solutions.

North America Market Insights

The North America bearing market is expected to grow with a market share of 18.71% between 2026 and 2036. The bearing market is progressing strongly, supported by a combination of industrial recovery, accelerating electrification, and the growth of advanced manufacturing capabilities. Rather than competing on scale alone, the region is increasingly defined by its focus on precision engineering, reliability, and technological innovation. Demand is continuing to grow steadily, driven by the upgrading of traditional industries alongside the rapid emergence and expansion of new, technology-driven sectors.

The bearing market in the U.S. is experiencing steady growth, driven by strong demand from the automotive, aerospace, and industrial machinery sectors. The rapid expansion of electric vehicles, automation, and advanced manufacturing technologies is increasing the need for high-performance bearings that deliver greater efficiency, durability, and precision. In addition, large-scale investments in infrastructure modernization, renewable energy projects, and industrial automation are further supporting market expansion. The country’s well-established manufacturing base and focus on technological innovation continue to position it as a key contributor to global bearing demand.

At the same time, the U.S. market is benefiting from a shift toward smart manufacturing and energy-efficient systems, where bearings play a critical role in improving equipment performance and reducing operational downtime. The growing emphasis on sustainability and electrification is accelerating the adoption of advanced bearing solutions across industries. Additionally, consistent replacement demand from an aging industrial and automotive fleet is strengthening the aftermarket segment, ensuring stable long-term growth for bearing manufacturers.

The bearing market in Canada is growing steadily, supported by strong activity in natural resource industries such as mining, oil and gas, and forestry. These sectors require durable and heavy-duty bearings capable of performing under extreme operating conditions, driving consistent demand. In addition, increasing investments in renewable energy, transportation infrastructure, and industrial development are contributing to bearing market growth. Canada’s expanding manufacturing base is also supporting demand for precision and application-specific bearing solutions. Alongside this, Canada is witnessing rising adoption of advanced industrial technologies and automation, which is increasing the need for efficient and low-maintenance bearing systems. The shift toward cleaner energy and sustainable industrial practices is further encouraging the use of high-performance bearings designed for energy efficiency and reduced environmental impact. Moreover, steady aftermarket demand from existing industrial equipment ensures continuous replacement and maintenance needs, supporting long-term market stability and growth.

Europe Market Insights

Europe bearing market is expanding through a strategic emphasis on precision engineering, sustainability, and advanced manufacturing capabilities. Rather than competing on volume, the region prioritizes high-value applications where performance, efficiency, and reliability are critical requirements. This focus supports stable demand while continuously elevating the technological sophistication and quality standards of the bearing market.

The bearing market in Germany is experiencing strong growth, supported by its position as a global hub for automotive engineering, industrial machinery, and precision manufacturing. The country’s leadership in high-performance engineering, particularly in premium automotive production and industrial automation, is driving consistent demand for advanced bearing solutions. Growing adoption of electric vehicles and Industry 4.0 technologies is further increasing the need for efficient, low-noise, and high-durability bearings. In addition, strong investments in renewable energy and smart manufacturing systems are reinforcing long-term market expansion. Germany’s focus on quality and innovation continues to strengthen its role as a key European bearing market.

The bearing market in the UK is growing steadily, supported by demand from aerospace, automotive, rail, and industrial manufacturing sectors. The country’s strong aerospace industry, in particular, plays a major role in driving demand for high-precision and high-reliability bearings used in aircraft systems. In addition, ongoing investments in infrastructure modernization, renewable energy, and transportation networks are contributing to market growth. The UK’s shift toward advanced manufacturing and automation is further increasing the adoption of efficient and durable bearing solutions.

Key Bearing Market Players:

- SKF (Sweden)

- Schaeffler Group (Germany)

- The Timken Company (U.S.)

- NSK Ltd. (Japan)

- NTN Corporation (Japan)

- JTEKT Corporation (Japan)

- Nachi-Fujikoshi Corp. (Japan)

- RBC Bearings (U.S.)

- MinebeaMitsumi Inc. (Japan)

- C&U Group (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- SKF is one of the most dominant players in the global bearing market, offering a wide range of bearings, seals, lubrication systems, and condition monitoring solutions. The company focuses heavily on innovation, particularly in reducing friction and improving energy efficiency across industrial applications. It has a strong global manufacturing and service network, enabling it to serve automotive, aerospace, and heavy industry sectors. SKF is also a leader in digitalization through predictive maintenance and IoT-enabled bearing systems

- Schaeffler Group operates through well-known brands like INA, FAG, and LuK, serving automotive and industrial bearing markets globally. It is known for precision engineering and high-performance bearing solutions, especially in drivetrain and mobility systems. The company is actively investing in electrification and e-mobility components, aligning with the shift toward electric vehicles. Its strong R&D focus helps it maintain leadership in advanced motion technology solutions.

- Timken is a major U.S.-based manufacturer specializing in bearings and power transmission products. It is particularly strong in engineered bearings used in heavy industries such as rail, mining, and renewable energy. The company emphasizes durability and reliability in extreme operating conditions. Timken has also expanded through acquisitions to strengthen its global industrial portfolio.

- NSK is a leading Japanese bearing manufacturer known for its high-quality precision bearings used in automotive and industrial machinery. The company focuses on improving motion and control technologies to enhance efficiency and performance. It has a strong presence in automotive OEM supply chains worldwide. NSK is also investing in smart technologies and condition monitoring systems to support predictive maintenance.

- NTN Corporation is one of the largest bearing manufacturers globally, offering products for automotive, industrial, and aerospace applications. It is recognized for its innovation in low-friction and high-durability bearing solutions. The company has a strong focus on sustainability and energy-saving technologies in mechanical systems. NTN continues to expand its global reach through partnerships and localized production facilities.

Below is the list of the key players operating in the global bearing market:

Key players are driving the bearing market through continuous innovation in high-performance, low-friction, and energy-efficient bearing solutions. They are investing heavily in R&D, digitalization, and predictive maintenance technologies to support Industry 4.0 applications. These companies are also expanding their global manufacturing footprints and strengthening supply chains to meet rising demand from automotive, aerospace, and industrial sectors. Additionally, strategic partnerships, acquisitions, and a focus on sustainability are helping them maintain competitiveness and shape bearing market growth.

Corporate Landscape of the Global Bearing Market:

Recent Developments

- In May 2026, NSK Ltd. and NTN Corporation announced that they have reached a basic agreement to establish a joint holding company through a share transfer, aiming to integrate their businesses under a unified structure. The companies stated that they have signed a memorandum of understanding following approvals from their respective boards of directors. This strategic business integration is intended to enhance operational efficiency, strengthen global competitiveness, and accelerate innovation in bearing and motion control technologies. The proposed holding company will serve as a platform for long-term value creation and closer collaboration between the two firms.

- In April 2026, Schaeffler Group has been actively expanding its automotive-focused portfolio through strategic transformation initiatives and partnerships centered on e-mobility and drivetrain technologies. In recent communications, the company highlighted its broad powertrain and electrification portfolio, covering solutions from hybrid systems to fully electric vehicle architectures, including high-efficiency bearings and integrated drive systems. These developments are part of Schaeffler’s strategy to strengthen its position in the global automotive supply chain amid the ongoing shift toward electrification and sustainable mobility. The company continues to emphasize system-level innovation and integration to support next-generation EV platforms and improve overall drivetrain efficiency.

- Report ID: 6082

- Published Date: May 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.