Automotive RFID Tag Market Outlook:

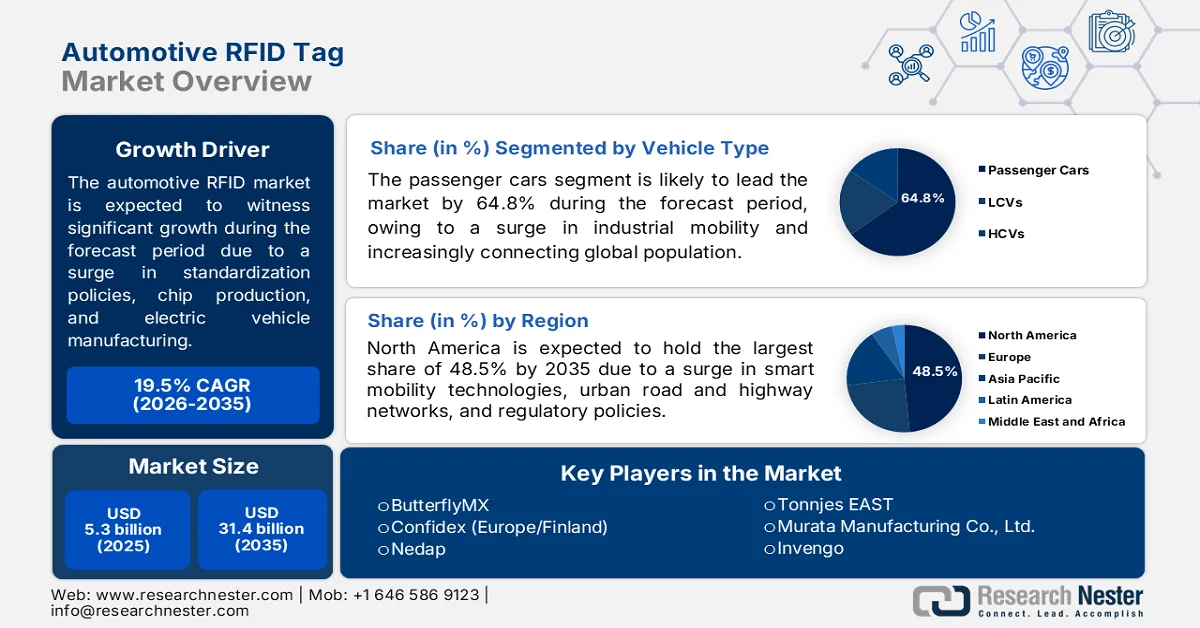

Automotive RFID Tag Market size was valued at USD 5.3 billion in 2025 and is projected to reach USD 31.4 billion by the end of 2035, registering around 19.5% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive RFID tag is estimated at USD 6.3 billion.

The global automotive RFID tag market is being shaped by different foundational factors, such as chip manufacturing, standardization efforts, the growing adoption of cloud-based data management platforms, real-time analytics, an increase in electric vehicle production, and the availability of automotive parts. According to official statistics published by the IEA Organization in 2026, the electric car industry successfully reached new records, accounting for a growth by 20% from 2024 and surpassing 20 million sales. Additionally, the sales share of these vehicles in the overall car sector also surged to 25%, marking the 5th consecutive year with 3.5 million electric cars. Besides, as per the 2026 OEC data report, Germany is considered the top exporter of motor vehicle components, which is valued at USD 64 billion, while the U.S. is considered the largest importer with USD 90.8 billion in valuation, thereby positively impacting the market growth globally.

Global Electric Car Sales Analysis (In Million), 2020-2026e

|

Year |

China |

Europe |

U.S. |

Rest of World |

|

2020 |

1.1 |

1.4 |

0.3 |

0.2 |

|

2021 |

3.3 |

2.3 |

0.6 |

0.3 |

|

2022 |

6.0 |

2.7 |

1.0 |

0.6 |

|

2023 |

8.1 |

3.2 |

1.4 |

1.0 |

|

2024 |

11.2 |

3.2 |

1.5 |

1.4 |

|

2025 |

13.2 |

4.2 |

1.5 |

2.0 |

|

2026e |

14.3 |

5.0 |

1.2 |

2.9 |

Source: IEA Organization

Furthermore, the stringent vehicle safety and security policies, growth in cross-border logistics and trade complexities, a rise in vehicle theft and cargo crime incidences, low-emission zone and urban congestion enforcements, and a sudden shift towards mobility and carsharing models are a few trends that are responsible for boosting the market globally. As stated in an article published by the FBI Organization in August 2024, 14,039 agencies effectively submitted their crime data to NIBRS that covers an overall population of 278,449,430 people as of 2023. Additionally, there was an increase in motor reporting agencies by 79.7%, with total number of incidents accounting for 100,000 people per rates in the same year. Besides, the rate of motor vehicle theft in the U.S. surged from 199.4 incidents per 100,000 people to 283.5 incidents, thereby denoting a huge growing opportunity and demand for the market across different regions.

Key Automotive RFID Tag Market Insights Summary:

Regional Highlights:

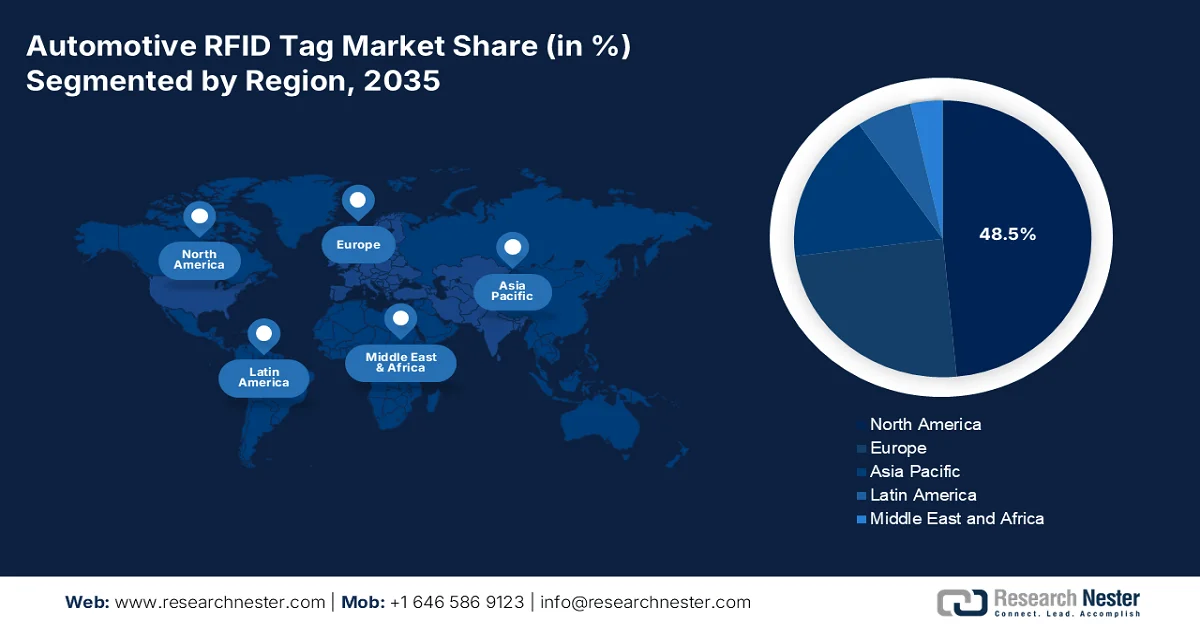

- North America automotive RFID tag market is anticipated to command 48.5% share by 2035, attributed to innovative transportation facilities, rising smart mobility adoption, and strong regulatory strategies

- Asia Pacific is projected to witness the fastest expansion in the market throughout 2026–2035, propelled by rapid digital transformation and increasing adoption of IoT and AI-based vehicle tracking systems

Segment Insights:

- The passenger cars segment is forecast to capture 64.8% of the automotive RFID tag market by 2035, reinforced by the continuous production and registration of passenger vehicles across Europe

- The passive RFID tags segment is expected to secure a considerable share in the market during 2026–2035, stimulated by their lightweight structure, durability, and battery-free operational capability for harsh automotive environments

Key Growth Trends:

- Increase in automotive manufacturing

- Focus on crowdsourced vehicle data networks

Major Challenges:

- Interference from metal and liquids in automotive environments

- Lack of standardization across global tolling and identification systems

Key Players: HID Global (U.S.), Zebra Technologies (U.S.), Impinj (U.S.), Honeywell International (U.S.), Alien Technology (U.S.), Avery Dennison (U.S.), OTI PetroSmart (Nayax) (U.S.), SkyRFID (U.S.), Xminnov (U.S.), ButterflyMX (U.S.), Confidex (Europe/Finland), Nedap (Europe/Netherlands), TagMaster (Europe/Sweden), Smartrac (Europe/Netherlands), HARTING Technology Group (Europe/Germany), Tonnjes EAST (Europe/Germany), Murata Manufacturing Co., Ltd. (Japan), Invengo (China), Xerafy (China), DMATEK (South Korea), NXP (Netherlands), Infineon Technologies AG (Germany), Seuic (China).

Global Automotive RFID Tag Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.3 billion

- 2026 Market Size: USD 6.3 billion

- Projected Market Size: USD 31.4 billion by 2035

- Growth Forecasts: 19.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (48.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, China, Japan, South Korea

- Emerging Countries: India, Vietnam, Thailand, Indonesia, Mexico

Last updated on : 26 May, 2026

Automotive RFID Tag Market - Growth Drivers and Challenges

Growth Drivers

- Increase in automotive manufacturing: The majority of Tier-1 automotive suppliers commenced in-house RFID tag production for reducing expenses and ensuring supply chain security, which is significantly driving the automotive RFID tag market globally. For instance, as per the April 2025 PIB Government article, India generously contributes 7.1% of the global gross domestic product (GDP) through its automotive industry and ranks 4th in worldwide vehicle manufacturing and production. Based on this, the country’s Vision 2030 approach has effectively aimed to upscale automotive production to USD 145 billion, along with exports to USD 60 billion, and also generate 2 million to 2.5 million employment opportunities, thereby making it suitable for enhancing the market’s upliftment.

- Focus on crowdsourced vehicle data networks: The presence of car rental fleets and logistics organizations has resulted in the increased pooling of RFID read data for creating real-time traffic and parking availability maps, which is also fueling the market globally. As per a data report published by OECD in January 2023, the increased penetration of smartphone devices are considered machine-to-machine (M2M) connections as of 2023, demonstrating a surge from 33% from the past years. In addition, these M2M-embedded mobile data subscriptions, which are crucial to ensure communications for a subset of the Internet of Things (IoT), further upsurged by more than 16% in different countries, which denotes suitable data availability, thereby denoting a huge growth opportunity for the market.

Challenges

- Interference from metal and liquids in automotive environments: Vehicles are readily composed predominantly of metal body panels, engine blocks, transmission casings, and chassis components, all of which reflect and absorb radio frequency signals. Besides, liquid-containing elements such as fuel tanks, coolant reservoirs, windshield washer fluid, and even humidity within vehicle cabins further attenuate RFID signals, particularly at ultra-high frequencies. When an RFID tag is attached to a metal surface such as a door panel, hood, or chassis rail, the metal detunes the tag's antenna, drastically reducing read range or rendering the tag completely unreadable. Similarly, tags placed near fuel tanks or coolant lines experience signal degradation due to liquid absorption of RF energy, thus negatively impacting the automotive RFID tag market growth.

- Lack of standardization across global tolling and identification systems: Different countries and regions within the same country operate incompatible RFID-based toll collection, vehicle registration, and access control systems using varying frequency bands, data protocols, and encryption methods. For instance, Europe primarily deploys dedicated short-range communications, while North America relies heavily on UHF RFID for systems, such as E-ZPass. Likewise, Japan utilizes its own proprietary active RFID standard for electronic toll collection, incompatible with foreign tag technologies. A single commercial fleet operating vehicles across multiple jurisdictions cannot use one RFID tag for all purposes, thus resulting in limiting the market expansion.

Automotive RFID Tag Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

19.5% |

|

Base Year Market Size (2025) |

USD 5.3 billion |

|

Forecast Year Market Size (2035) |

USD 31.4 billion |

|

Regional Scope |

|

Automotive RFID Tag Market Segmentation:

Vehicle Type Segment Analysis

The passenger cars segment in the vehicle type is anticipated to capture the highest share of 64.8% in the automotive RFID tag market by the end of 2035. The segment’s upliftment is primarily attributed to its vital provision of industrial mobility and readily connecting people to social activities, healthcare, and jobs. Besides, according to official statistics published by the German Trade and Invest (GTAI) in May 2025, Germany significantly accounts for more than 32% of overall manufactured passenger cars, along with nearly 22% of new registrations in Europe. In addition, the country is considered the leader in the regional car production, with about 4.1 million passenger cars. Besides, domestic passenger car OEMs usually generated automotive industrial revenue of USD 431.8 billion as of 2024, demonstrating a 5% decrease from 2023. Moreover, the continuous production and registration of passenger cars in Europe is also creating a huge growth opportunity for the segment.

Passenger Cars Production and Registration in Europe, 2024

|

Countries |

Production (Million Units) |

Registration (Million Units) |

|

Germany |

4.1 |

2.8 |

|

Spain |

1.9 |

1.0 |

|

Czech Republic |

1.5 |

- |

|

Slovakia |

1.0 |

- |

|

France |

0.9 |

1.7 |

|

UK |

0.8 |

1.9 |

|

Italy |

- |

1.5 |

|

Poland |

- |

0.5 |

Source: GTAI

Tag Type Segment Analysis

Based on the tag type, the passive RFID tags segment is projected to register a considerable share in the automotive RFID tag market during the forecast period. The segment’s growth is effectively fueled by its operational capability without an internal battery, drawing power from the reader's electromagnetic field. This design makes them lightweight, thin, and extremely durable, which is ideal for harsh automotive environments, including engine compartments, tire assemblies, and undercarriage exposure. In vehicle manufacturing, passive tags enable real-time work-in-progress tracking along assembly lines, allowing OEMs to monitor each car's exact build status without manual scanning. For supply chain logistics, these tags are affixed to pallets, containers, and reusable automotive racks, automatically recording movement through warehouse gates and loading docks.

Frequency Band Segment Analysis

By the end of the stipulated timeline, the low frequency sub-segment in the frequency band segment is expected to account for suitable growth in the market. The sub-segment’s development is highly propelled by its usefulness, which is uniquely suited for applications requiring reliable performance near metal or liquids, where higher frequencies often fail due to signal interference. Besides, vehicle immobilizer systems represent the largest low frequency deployment, with the transponder embedded in a car key fob that communicates with the ignition reader, preventing engine start unless a valid low frequency signal is detected. This anti-theft application has been mandated by automotive insurance standards in multiple regions. Moreover, this sub-segment is also utilized in tire pressure monitoring systems and tire identification, where rubber compounds and steel belts do not degrade low frequency performance.

Our in-depth analysis of the automotive RFID tag market includes the following segments:

|

Segment |

Subsegments |

|

Vehicle Type |

|

|

Tag Type |

|

|

Frequency Band |

|

|

Application |

|

|

Material Substrate |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive RFID Tag Market - Regional Analysis

North America Market Insights

North America in the automotive RFID tag market is anticipated to garner the highest share of 48.5% by the end of 2035. The market’s upliftment in the region is primarily driven by innovative transportation facilities, an increase in the adoption of smart mobility technologies, robust adoption across logistics corridors, urban road networks, and highways, along with an expanded highway network and strong regulatory strategies. According to official statistics published by the ASCE’s 2025 Infrastructure Report Card, there has been an investment of more than USD 591 billion from the Infrastructure Investment and Jobs Act (IIJA) for roadways in the U.S. Besides, the share of pavement on roads, in terms of federal funding for quality ride, has increased from 40.7% to 47.2%, thereby making it suitable for uplifting the market and its expansion in the overall region.

The market is growing significantly in the U.S., owing to an expansion in the electronic toll collection network, suitable government mandates for vehicle security and emission standards, the presence of state and federal smart infrastructure programs for generous investments, a surge in vehicle ownership, and logistics volume. As stated in an article published by the Institute for Transportation and Development Policy in January 2024, the U.S. Department of Transportation noted that transportation is considered the highest yearly consumer spending, amounting to a total of USD 12,295 as of 2023. Besides, 90% of the regional population had one car, and nearly a quarter of the domestic population owned more than 3 vehicles. Moreover, in terms of overall national household expenditure, transportation catered to an overall USD 1.6 trillion. Simultaneously, the car accessibility in terms of different community types is also driving the market growth in the country.

Car Accessibility in the U.S., Based on Communities, 2022

|

Community Type |

Number of Cars (Million) |

Car Access % |

|

All |

10.5 |

8 |

|

Asia-America |

708,000 |

11 |

|

Black |

2.5 |

17 |

|

Latino |

1.7 |

10 |

|

Mixed/Other |

379,000 |

10 |

|

Native America |

76,700 |

13 |

|

Pacific Islander |

12,800 |

8 |

|

People of Color |

5.5 |

13 |

|

White |

4.9 |

6 |

Source: National Equity Atlas

The demand for durable tracking in severe conditions, robust dependency on rail, mining, and logistics, modernization in smart cities and facilities, an increase in the requirement for cross-border and domestic cargo visibility, along with the integration with innovative technologies, are certain factors that are proliferating the automotive RFID tag market in Canada. As per an article published by Elsevier in May 2026, a study analysis was conducted on smart cities of 200 communities, of which 130 were selected, and a further 20 communities received an overall USD 250,000 to significantly develop their respective proposals. In addition, the funding opportunity was distributed across three categories, including USD 50 million for a community with more than 500,000 inhabitants, USD 10 million for 300,000 and 500,000 inhabitants, and USD 5 million with less than 300,000 inhabitants, thus positively impacting the market growth.

APAC Market Insights

The Asia Pacific in the automotive RFID tag market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by rapid digital transformation, an increase in the adoption of IoT and AI-based vehicle tracking systems, cloud-specific fleet management, and a rise in the demand for secure transport of vehicles and high-value goods. According to official statistics published by the ADB Organization in January 2022, there has been an increase in vehicle ownership by 7.4%, which is proportionate to 7.7% GDP growth. In addition, there has also been a surge in road vehicle stock from almost 310 million to nearly 1.2 billion vehicles, which is about half of motorized two and three-wheelers, thereby making it suitable for expanding the market exposure in the region.

The automotive RFID tag market is gaining increased traction in China, owing to an expansion in toll collection systems across major cities, such as Guangzhou, Shenzhen, Shanghai, and Beijing, dominant leadership in automotive manufacturing, and readily prioritizing intelligent transportation systems and smart city infrastructure. As stated in an article published by the State Council Information Office in May 2026, new-energy vehicles (NEVs) successfully made up 53.2% of overall new car sales in April, indicating a 47.3% rise from 2024. Additionally, in the first 4 months of 2026, NEV sales significantly reached 4.3 million units, and meanwhile, overall exports upsurged by 61.5% to 3.1 million units. Likewise, NEV exports also doubled to 1.3 million units, based on which there is a huge growth and expansion opportunity for the market in the overall country.

The aspects of an upsurge in the demand for intelligent logistics systems for ensuring real-time tracking and inventory management of the automotive industry, an increase in domestic logistics, the expansion of automobile production, and the innovation of digitalization in manufacturing processes are a few trends that are responsible for proliferating the automotive RFID tag market in Japan. The market’s upliftment in the country accounts for USD 115.9 million as of 2025, which is predicted to expand to USD 133.9 million by 2026, and further reach USD 494.9 million, along with a 15.6% growth by the end of 2035. Besides, in terms of manufacturing, the April 2025 ITA article noted that the value-added manufacturing business in the country accounted for over 20% of domestic GDP, and organizations are projected to have spent USD 12.9 billion on software, thereby denoting an optimistic outlook for the market’s development.

Europe Market Insights

Europe in the automotive RFID tag market is projected to witness considerable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively attributed to a rise in electric vehicles, smart city projects, suitable logistics and transportation solutions, and real-time tracking and monitoring of automotive assets. According to official statistics published by E-Mobility Europe in January 2025, passenger cars were readily responsible for 16% of the region’s carbon emissions as of 2022, demonstrating a rise from 13%. Besides, based on government approaches, a grant scheme offered electric car purchasers a USD 7,828.4 in grants towards an electric car expense. Moreover, the French government spent USD 1.1 billion on electric vehicle subsidies as of 2025, thereby creating a huge growth opportunity for the market in the region.

The market is gaining increased exposure in Germany, owing to supply chain management, vehicle identification, asset tracking, climate neutrality goals, generous spending on automotive chemical innovations, and an increased focus on creating recyclable substrates and low-carbon semiconductor materials for automotive applications. As stated in an article published by the EV TCP Organization in 2026, almost 2.8 million electric vehicles were registered in the country as of 2024, of which 1 million were plug-in hybrid vehicles and the remaining 1.8 million were battery electric vehicles (BEVs). In addition, BEVs readily accounted for 14% of the overall automotive industry, with 380,609 new registrations. Therefore, with this ongoing growth in electric vehicle adoption, there is a huge demand for the market in the country.

Different Types of Electric Vehicle Registration in Germany, 2014-2023

|

Year |

Battery Electric Vehicle |

Plug-in Hybrid Electric Vehicle |

Hybrid Electric Vehicle |

|

2014 |

18,948 |

- |

107,754 |

|

2015 |

37,306 |

10,810 |

120,232 |

|

2016 |

40,785 |

20,979 |

167,552 |

|

2017 |

75,162 |

44,431 |

193,034 |

|

2018 |

101,001 |

67,011 |

275,099 |

|

2019 |

173,545 |

102,220 |

438,776 |

|

2020 |

313,020 |

280,046 |

727,313 |

|

2021 |

682,355 |

566,416 |

1,106,917 |

|

2022 |

683,958 |

566,553 |

1,110,065 |

|

2023 |

1,555,265 |

922,869 |

2,002,021 |

Source: EV TCP Organization

The supply chain management, vehicle identification, asset tracking of the automotive industry, authorization demands, sustainable innovation in vehicle materials, generous investment plan, growth in logistics and manufacturing industries, and a surge in export and domestic consumption are certain trends that are bolstering the market in Turkey. As per an article published by the ITA in January 2026, the manufacturing industry in the country accounts for the highest share in the GDP with 16.8% share as of 2024. Based on this, 40.3% of manufacturing exports comprise medium-based products and 5.1% comprised high-technological products. Moreover, in the upcoming decade, the country is projected to generously invest between USD 1 and USD 1.5 billion yearly for integrating Industry 4.0 solutions into the overall manufacturing process, thereby denoting an optimistic outlook for the market.

Key Automotive RFID Tag Market Players:

- HID Global (U.S.)

- Zebra Technologies (U.S.)

- Impinj (U.S.)

- Honeywell International (U.S.)

- Alien Technology (U.S.)

- Avery Dennison (U.S.)

- OTI PetroSmart (Nayax) (U.S.)

- SkyRFID (U.S.)

- Xminnov (U.S.)

- ButterflyMX (U.S.)

- Confidex (Europe/Finland)

- Nedap (Europe/Netherlands)

- TagMaster (Europe/Sweden)

- Smartrac (Europe/Netherlands)

- HARTING Technology Group (Europe/Germany)

- Tonnjes EAST (Europe/Germany)

- Murata Manufacturing Co., Ltd. (Japan)

- Invengo (China)

- Xerafy (China)

- DMATEK (South Korea)

- NXP (Netherlands)

- Infineon Technologies AG (Germany)

- Seuic (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- HID Global offers a range of rugged RFID tags designed for vehicle identification, asset tracking, and supply chain visibility in automotive manufacturing. The company focuses on high-frequency and ultra-high-frequency solutions that integrate with existing transportation and access control systems.

- Zebra Technologies provides durable RFID tags and readers tailored for automotive assembly lines, parts traceability, and finished vehicle logistics. Its solutions are widely adopted for real-time location tracking across large manufacturing and distribution facilities.

- Impinj specializes in RAIN RFID tag chips and readers that enable item-level tracking of automotive components throughout the production and delivery cycle. The company’s technology powers many third-party tag designs used by tier-one suppliers and OEMs.

- Honeywell International supplies RFID-enabled scanning and data capture hardware for automotive warehouses, service centers, and assembly plants. Its ruggedized mobile computers and fixed readers support high-speed identification of tagged vehicles and parts.

- Alien Technology manufactures UHF RFID tags and readers frequently embedded into reusable automotive containers, pallets, and component bins. The company’s tag chips are engineered for high-volume, cost-sensitive applications in complex supply chain environments.

Here is a list of key players operating in the global market:

The global automotive RFID tag market is highly competitive, featuring a mix of specialized RFID innovators and large-scale industrial automation providers. Key players are strengthening their market position through innovation, strategic collaborations, and geographic expansion. Likewise, companies are generously investing in advanced product development to enhance tag durability and data accuracy. Moreover, a significant trend is the formation of partnerships with transportation authorities and logistics operators to accelerate large-scale deployment. Besides, in October 2025, Infineon Technologies AG launched two of the latest secured prepaid tag solutions by effectively focusing on open-loop and closed-loop gift cards to protect merchants, issuers, and consumers from increased fraud rates, thereby making it suitable for boosting the automotive RFID tag industry globally.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, NXP introduced NXP’s newest UCODE X for delivering industry-specific RAIN RFID performance for high-volume applications to ensure reading and writing customizable and sensitivity configurations.

- In April 2025, Avery Dennison Corporation unveiled its very first RFID inlays and labels production facilities, particularly in India, which is a crucial step in supporting RFID technological growth in overall South Asia under the Make in India approach.

- In April 2025, Seuic launched 5 latest products, such as an AI-based RFID reader, based on which more than 100 industrial partners collaborated to explore these technologies for future innovations and industry applications.

- Report ID: 8580

- Published Date: May 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.