Automotive Navigation System Market Outlook:

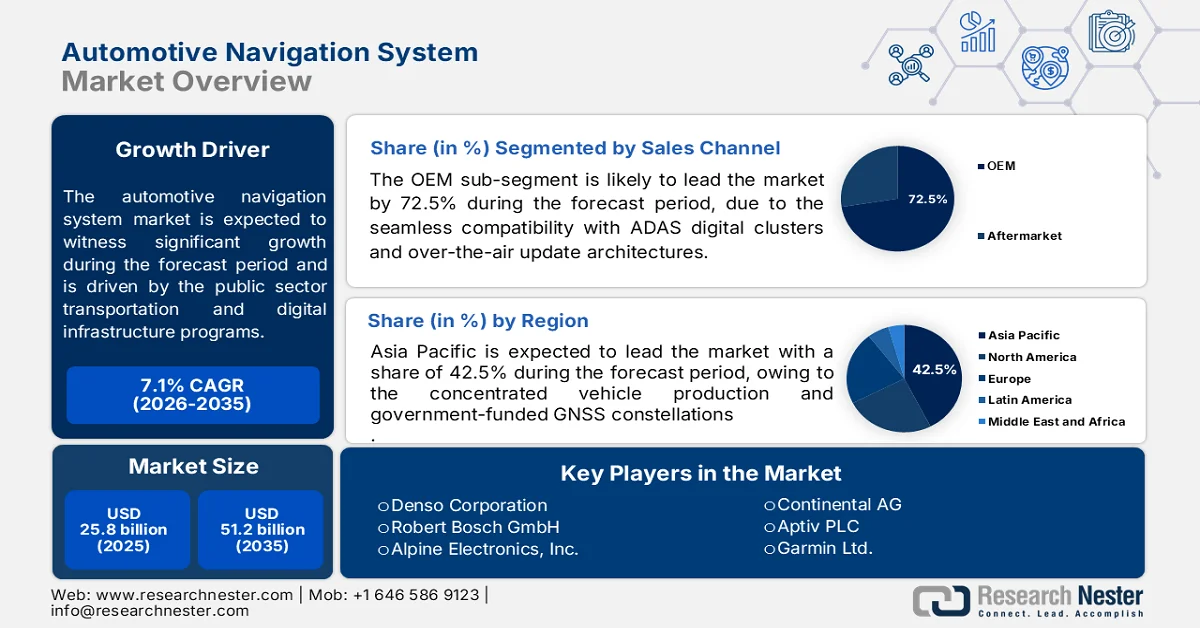

Automotive Navigation System Market size was valued at USD 25.8 billion in 2025 and is projected to reach USD 51.2 billion by 2035, rising at a CAGR of 7.1% during the forecast period, 2026-2035. In 2026, the industry size of automotive navigation system is estimated at USD 27.6 billion.

Public sector transportation and digital infrastructure programs are materially shaping the demand for automotive navigation systems via sustained investment in intelligent transport systems and connected vehicle ecosystems. According to the U.S. Department of Transport, March 2024 data, the Bipartisan Infrastructure Law allocates USD 110 billion for roads, bridges, and major projects with dedicated funding for ITS deployments and real-time traffic data integration that directly supports in-vehicle navigation accuracy and routing efficiency. On the other hand, the European Commission's July 2023 data has indicated that the European Union’s Connecting Europe Facility has earmarked more than USD 27.9 billion for transport infrastructure, with a strong emphasis on digitalization and cross-border traffic management systems that require high precision navigation integration.

Besides, the national smart mobility policies, satellite navigation investments are stimulating the adoption of the automotive navigation system market. According to the State Council Information Office of the People’s Republic of China, November 2022 data, China’s BeiDou Navigation Satellite System has surpassed 1 billion active terminals with extensive integration into commercial and passenger vehicles for fleet management and route optimization. NITI Aayog May 2023 data indicates that the commercial vehicle tracking which overseas more than 283 million registered vehicles nationwide. These public investments are complemented by regulatory frameworks promoting road safety and traffic efficiency, such as the European Commission’s ITS Directive and the U.S. Federal Highway Administration’s congestion mitigation programs, both of which rely on accurate navigation data inputs. These government-led initiatives demand that OEMs and fleet operators seek compliance, operational efficiency, and integration with national transport systems.

Key Automotive Navigation System Market Insights Summary:

Regional Highlights:

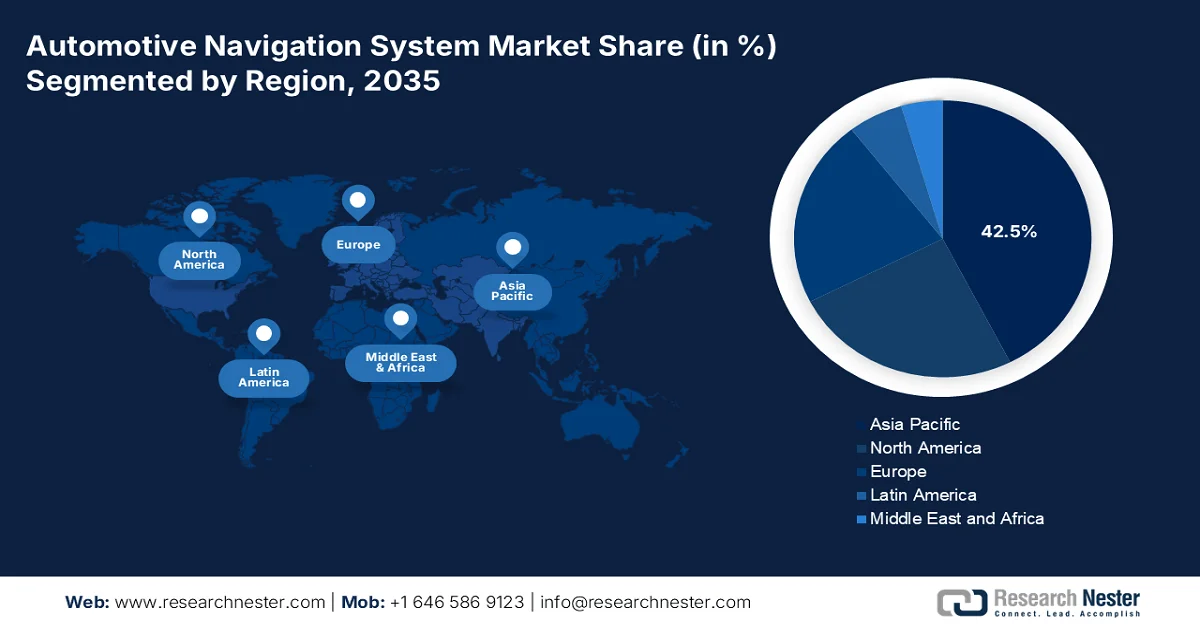

- Asia Pacific automotive navigation system market is projected to secure 42.5% revenue share by 2035, reinforced by concentrated vehicle production and government-backed GNSS constellations across China, Japan, South Korea, and India

- North America market is anticipated to witness the fastest growth at a CAGR of 10.1% during 2026–2035, fueled by federal investments in GPS modernization and vehicle safety programs

Segment Insights:

- The OEM segment is expected to account for 72.5% of the automotive navigation system market by 2035, propelled by rising integration of factory-installed navigation systems with ADAS, infotainment platforms, and over-the-air update architectures

- The individual consumer segment is anticipated to maintain its leading position in the market through 2035, attributed to increasing dependence on real-time traffic updates, predictive routing, and digitally connected in-car navigation experiences

Key Growth Trends:

- Road safety and accident reduction initiatives

- Expansion of satellite navigation infrastructure

Major Challenges:

- High system development and integration costs

- Complex integration with ADAS and autonomous driving platforms

Key Players: Denso Corporation (Japan), Robert Bosch GmbH (Germany), Alpine Electronics, Inc. (Japan), Continental AG (Germany), Aptiv PLC (U.S.), Garmin Ltd. (U.S.), Clarion Co., Ltd. (Japan), Hyundai Mobis (South Korea), Pioneer Corporation (Japan), TomTom International BV (Netherlands), Mitsubishi Electric Corporation (Japan), Visteon Corporation (U.S.), Panasonic Automotive Systems (Japan), Harman International Industries (U.S.), Fujitsu Ten Limited (now Densoten) (Japan), LG Electronics (South Korea), NNG Kft. (Hungary), MapmyIndia (India), Hexagon (Sweden), ECARX Holdings Inc (China).

Global Automotive Navigation System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 25.8 billion

- 2026 Market Size: USD 27.6 billion

- Projected Market Size: USD 51.2 billion by 2035

- Growth Forecasts: 7.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: India, Malaysia, Brazil, Mexico, Indonesia

Last updated on : 7 May, 2026

Automotive Navigation System Market - Growth Drivers and Challenges

Growth Drivers

- Road safety and accident reduction initiatives: Government road safety programs are pushing the adoption of navigation systems that provide hazard alerts, speed guidance, and safer route planning. According to the World Health Organization, December 2023 data, nearly 1.19 million road traffic deaths are annually registered, prompting governments to invest in safer mobility systems. The U.S. Federal Highway Administration’s safety programs and the EU’s Vision Zero strategy emphasize technologies that improve driver awareness and reduce accidents. Beyond regulatory mandates, insurers are beginning to offer premium reductions for vehicles equipped with safety-oriented navigation features. Fleet operators are also adopting these systems to lower accident-related downtime and liability costs, creating commercial pull beyond government requirements.

- Expansion of satellite navigation infrastructure: Global navigation satellite systems funded by the government are significantly improving positioning accuracy, directly strengthening automotive navigation demand. According to the EUSpace 2024 data, Europe’s Galileo system has exceeded 4 billion enabled devices, providing dual-frequency accuracy critical for urban navigation. These systems reduce dependency on single constellation positioning and enable lane-level navigation capabilities. These infrastructure investments support autonomous vehicle testing corridors and commercial logistics fleets requiring high-integrity positioning. The interoperability between GPS, Galileo, and BeiDou systems allows navigation suppliers to offer true global coverage without deploying proprietary ground infrastructure.

- Growth of connected and autonomous vehicle programs: Government funding for connected and autonomous vehicle programs is increasing the reliance on high-precision navigation systems. The U.S. DOT and state governments are investing in CAV pilot corridors, and Japan’s government supports autonomous driving via its strategic innovation promotion program. These initiatives require lane-level accuracy and continuous connectivity, driving the demand for advanced navigation solutions. These programs are further supported by public investments in vehicle-to-everything (V2X) infrastructure, enabling real-time communication between vehicles and road systems to enhance navigation accuracy and safety. As a result, OEMs and technology providers are prioritizing multi-sensor fusion and high-definition mapping to meet government-backed performance standards for automated driving systems.

Challenges

- High system development and integration costs: Developing automotive-grade navigation systems requires substantial investment in hardware, software, and integration with vehicles' ADAS platforms. The global in-dash navigation system market is set to grow, yet high system costs remain a significant barrier for new players lacking economies of scale in the automotive navigation system market. Top companies address this challenge by developing cost-optimized single-camera ADAS solutions mainly for price-sensitive markets with a strong R&D team to co-develop affordable technologies with local OEMs. This modular approach allows companies to offer entry-level navigation integration while maintaining profitability.

- Complex integration with ADAS and autonomous driving platforms: Modern navigation systems must seamlessly integrate with the ADAS features and autonomous driving stacks, requiring a centimeter-level accuracy and sub-second latency. Though there is an active expansion in the automotive navigation system market growth, the growth is concentrated among the established players with proven ADAS integration capabilities. Top companies have strategically positioned themselves by developing navigation platforms that share sensor data between navigation and ADAS functions, reducing component redundancy and cost.

Automotive Navigation System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.1% |

|

Base Year Market Size (2025) |

USD 25.8 billion |

|

Forecast Year Market Size (2035) |

USD 51.2 billion |

|

Regional Scope |

|

Automotive Navigation System Market Segmentation:

Sales Channel Segment Analysis

Under the sales channel segment, the OEM is dominating the automotive navigation system market and is poised to capture 72.5% of the market value by 2035. The segment is driven as the automakers increasingly integrate navigation as a standard or subscription-based feature directly into vehicle infotainment systems. The OEM integration ensures seamless compatibility with ADAS digital clusters and over-the-air update architectures, which aftermarket solutions cannot fully replicate. According to the SIAM August 2023 data, the new passenger vehicles sold in 2023 were 3,34,247 units, which came with factory-installed connected navigation systems. This rapid OEM penetration reflects consumer preference for built-in navigation that requires no smartphone tethering and offers deep vehicle integration, such as EV route planning with battery preconditioning. Automakers also use OEM navigation as a recurring revenue stream via monthly or annual subscriptions for real-time traffic and map updates.

End user Segment Analysis

Within the end user segment, the individual consumer represents the largest end user segment in the automotive navigation system market, driven by rising daily reliance on real-time traffic point of interest discovery and predictive routing for personal travel. While fleet operators contribute significantly to the sheer volume of privately-owned vehicles, mainly in North America, Europe, and China, ensures consumer dominance. Consumers increasingly expect navigation to integrate with their digital lifestyles, including calendar syncing, EV charger routing, and voice assistants. Automakers and aftermarket brands alike target individual buyers with features like augmented reality, turn-by-turn directions, and offline map storage. As navigation becomes a standard amenity even in entry-level cars, individual consumers will continue driving volume, while fleet operators adopt more specialized, telematics-heavy navigation solutions.

Navigation Type Segment Analysis

Hybrid navigation sub-segment is driving the navigation type segment in the automotive navigation system market, as it introduces an industry-first solution combining traditional 2D maps with augmented reality guidance across web, mobile, and kiosks. While the orginally targeted at indoor spatial computing and events, the underlying technology seamlessly switches between 2D and AR modes, paralleling the hybrid navigation principles used in automotive offline base maps plus real-time immersive overlays. According to the July 2025 press release, ARway’s Interactive Map Navigation enables point-to-point wayfinding that unifies conventional navigation with cutting-edge AR, allowing users to transition from a standard 2D route to an AR-driven camera-based overlay without losing context. ARway’s solution demonstrates how hybrid architectures are expanding beyond vehicles into cross-platform spatial experiences, reinforcing hybrid navigation as the dominant paradigm for seamless, fail-safe guidance in both automotive and adjacent markets.

Our in-depth analysis of the automotive navigation system market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Navigation Type |

|

|

Vehicle Type |

|

|

Technology |

|

|

Sales Channel |

|

|

Functionality |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Navigation System Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the automotive navigation system market and is poised to hold the regional revenue share of 42.5% by the end of 2035. The region is driven by the concentrated vehicle production in China, Japan, and South Korea, alongside emerging demand in India and Malaysia. The region benefits from government-funded GNSS constellations, including China’s BeiDou, Japan’s QZSS, and India’s NavIC. The region also benefits from dense urban environments where real-time traffic and lane-level guidance are essential, pushing both the OEMs and aftermarket suppliers to integrate advanced navigation as a standalone feature. Government policies across multiple APAC countries increasingly link navigation systems to broader smart city initiatives, creating sustained demand for connected and continuously updated mapping platforms. Further, the rapid expansion of electric vehicle adoption in the region requires navigation systems that can route the drivers to compatible charging stations, further embedding navigation as a core vehicle function rather than an optional convenience.

The rapid EV adoption and expanding internet penetration are shaping the automotive navigation system market in India. According to the NITI Aayog August 2025 data, EV sales in India increased from 50,000 units to 2.08 million, aligned with the government’s target of achieving a 30% EV share in total vehicle sales by 2030, which is accelerating demand for navigation systems with charging station mapping and route optimization. Moreover, the IBEF January 2025 data digital readiness is strengthening with 886 million active internet users in 2024, growing 8% YoY, and rural users accounting for 55% of the total base (488 million users). This widespread connectivity supports real-time navigation, cloud-based updates, and smartphone integration. These trends are promoting the OEMs and technology providers to scale both embedded and hybrid navigation solutions across urban and rural mobility ecosystems.

The increasing localization of advanced in vehicle technologies and OEM investments are supporting the growth of the automotive navigation system market in China. The push in China for China strategies is evident as global manufacturers such as Volkswagen introduce locally developed ADAS platforms in April 2025, designed to integrate seamlessly with navigation systems for enhanced driving precision and safety. On the other hand, suppliers are scaling production of connected vehicle technologies, with Magna reporting its first full year of global Driver Monitoring System (DMS) production initiated in China in October 2025, reflecting growing deployment of intelligent cockpit and safety solutions. These developments indicate a broader shift toward integrated platforms where navigation, ADAS, and real-time data systems operate together. Further, the OEMs and Tier-1 suppliers are increasingly prioritizing high-definition mapping, localized software development, and system integration to meet China’s rapidly evolving smart mobility and connected vehicle ecosystem.

North America Market Insights

The North America is projected to emerge as the fastest-growing region in the automotive navigation system market and is expected to expand at a CAGR of 10.1% during the assessed period, 2026 to 2035. The region is driven by the federal investments in GPS modernization and vehicle safety programs. The region is driven by the federal investments in GPS modernization and vehicle safety programs. Key drivers include NEVI program mandates requiring EV charging station data integration into navigation systems and UNECE safety regulations adopted by both countries. Trends show an increase in the adoption of hybrid navigation and lane-level positioning using GPS III and Galileo dual-frequency signals. Automotive navigation system market growth is tempered by smartphone navigation competition and aftermarket saturation.

Rising electrification and digital connectivity are reinforcing the demand for advanced automotive navigation system market in the U.S. According to the EIA February 2026 data, about 22% of light-duty vehicle sales were hybrid battery electric or plug-in hybrid, up from 20% in 2024, indicating a growing requirement for navigation platforms capable of supporting EV-specific functionalities such as charging station mapping and range optimization. Similarly, widespread digital adoption is strengthening the ecosystem for connected navigation, with 95% of U.S. adults using the internet, 90% owning smartphones, and 80% having home broadband access in 2023, according to the Pew Research Center's January 2024 data. This high level of connectivity enables seamless integration between in-vehicle systems and cloud-based navigation services. Together, these trends are driving OEMs to prioritize hybrid and connected navigation architectures that can support real-time data exchange and evolving vehicle technologies.

The increased electrification, connectivity, and digital infrastructure support are shaping the automotive navigation system market in Canada. According to the Government of Canada, March 2024 data, zero-emission vehicles accounted for 11.7% of new light-duty vehicle sales, reflecting growing demand for navigation systems with charging station integration and range optimization. The November 2023 data reports that over 26.3 million registered road motor vehicles were recorded, creating a large installed base for navigation-enabled upgrades and services. Additionally, the Government of Canada's December 2023 data indicates that 93.6% of households had access to high-speed internet, enabling real-time navigation, cloud-based updates, and connected vehicle services. These factors are encouraging OEMs and technology providers to expand embedded and hybrid navigation solutions aligned with national electrification and digital connectivity goals.

Canada Vehicle Registrations by Type and Province, 2022

|

Category |

Key Data |

|

Light-Duty Vehicles (LDVs) |

24.1 million vehicles; 91.7% of total registrations; up 0.1% from 2021 |

|

Medium-Duty Vehicles |

Increased by 4.0% from 2021; growth driven primarily by pickup trucks |

|

Heavy-Duty Vehicles |

Increased by 2.0% from 2021 |

|

Bus Registrations |

Recovered to 2020 levels after decline in 2021 |

|

Ontario |

9.4 million vehicles; 35.9% share; decreased by 0.3% from 2021 |

|

Alberta |

Declined by 1.0% from 2021 |

|

Saskatchewan |

Declined by 1.5% from 2021 |

|

Prince Edward Island |

Declined by 2.3% from 2021 |

|

British Columbia |

Increased by 2.9% from 2021 |

Source: Government of Canada November 2023

Europe Market Insights

The automotive navigation system market in Europe is expanding rapidly and is shaped by the strong regulatory frameworks and cross-border infrastructure cooperation among the member states. The European Commission has established mandates for emergency call systems that rely on positioning technology, creating a consistent requirement across all new vehicles sold in the region. National governments and the EU collectively fund the Galileo satellite constellation, which provides open service positioning signals specifically designed for civilian applications, including automotive use. Member states are also deploying cooperative intelligent transport systems along major transport corridors, allowing navigation platforms to receive real-time road hazard, traffic signal, and speed advisory information directly from roadside infrastructure. This regulatory harmonization reduces development costs for manufacturers and accelerates deployment of advanced navigation features such as lane-level guidance and speed adaptation.

The rising electrification and sustained public investment are driving the automotive navigation system market in Germany. According to the VDIK May 2025 data, nearly 242,728 new passenger cars were registered with a calendar-adjusted growth of 4.8%, indicating stable OEM activity despite short-term fluctuations. A key demand driver is the rapid expansion of electric vehicles, with 45,535 battery electric vehicles registered in April 2025, marking a 53.5% YoY increase and capturing 18.8% market share, significantly higher than the previous year. This trend is reinforcing the need for navigation systems with EV route optimization and charging integration. Additionally, Germany’s allocation of USD 36.2 billion for transport infrastructure in 2025 is strengthening digital traffic systems and road networks, further supporting advanced navigation deployment as per the Business Sweden August 2025 data. Together, these factors are supporting OEMs to enhance embedded and connected navigation capabilities aligned with evolving mobility requirements.

Germany Vehicle Registrations and Market Share Breakdown, 2025

|

Category |

April Volume |

April YoY (%) |

April Market Share (%) |

|

Passenger Cars |

242,728 |

-0.2 |

— |

|

International Brands |

102,607 |

2.8 |

42.3 |

|

German Brands |

137,108 |

-1.9 |

56.5 |

|

Electric Vehicles (Total) |

69,852 |

55.9 |

28.8 |

|

Battery Electric Vehicles |

45,535 |

53.5 |

18.8 |

|

International Brands |

18,412 |

91.3 |

40.4 |

|

German Brands |

25,503 |

42.2 |

56.0 |

|

Plug-in Hybrid Vehicles |

24,317 |

60.7 |

10.0 |

|

International Brands |

9,636 |

77.1 |

39.6 |

|

German Brands |

14,441 |

51.1 |

59.4 |

|

Commercial Vehicles |

27,545 |

-16.9 |

— |

Source: VDIK May 2025

The rising vehicle connectivity, EV adoption, and public digital mobility investments are driving the automotive navigation system market in the UK. According to the RAC Foundation, in August 2025, 1.95 million new cars were registered in 2023, reflecting a stable OEM production and the opportunities for embedded navigation integration. The Global Ardour Recycling Limited February 2026 reported that battery electric vehicles accounted for 16.5% of total new car registrations in 2024, driving demand for navigation systems with charging station mapping and range management. Additionally, the TechUK November 2025 Ofcom reported that 97% of UK premises had access to superfast broadband by 2024, enabling stronger real-time connectivity for the cloud-based navigation services and over-the-air updates. These developments are supporting the automotive suppliers to invest in connected and hybrid navigation solutions aligned with the UK’s electrification strategy and smart transport infrastructure modernization initiatives.

Key Automotive Navigation System Market Players:

- Denso Corporation (Japan)

- Robert Bosch GmbH (Germany)

- Alpine Electronics, Inc. (Japan)

- Continental AG (Germany)

- Aptiv PLC (U.S.)

- Garmin Ltd. (U.S.)

- Clarion Co., Ltd. (Japan)

- Hyundai Mobis (South Korea)

- Pioneer Corporation (Japan)

- TomTom International BV (Netherlands)

- Mitsubishi Electric Corporation (Japan)

- Visteon Corporation (U.S.)

- Panasonic Automotive Systems (Japan)

- Harman International Industries (U.S.)

- Fujitsu Ten Limited (now Densoten) (Japan)

- LG Electronics (South Korea)

- NNG Kft. (Hungary)

- MapmyIndia (India)

- Hexagon (Sweden)

- ECARX Holdings Inc (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Denso Corporation is a dominant player in the automotive navigation system market, leveraging its expertise in hardware and software integration. The company has advanced navigation solutions by combining high precision GPS with vehicle sensor data, enabling accurate real-time positioning even in GPS-denied environments such as tunnels or urban canyons.

- Robert Bosch GmbH stands out for its end-to-end navigation ecosystem in the automotive navigation system market, combining GNSS receivers, inertial sensors, and high-definition maps. Bosch has strategically invested in the satellite-based localization technologies that achieve lane-level accuracy critical for semi-autonomous and autonomous vehicles. Its open collaboration model with the automakers and mapping firms reinforces its leadership.

- Alpine Electronics has carved a niche in the automotive navigation system market by emphasizing premium user experience and aftermarket navigation solutions. The company’s strategic initiatives revolve around integrating smartphone connectivity with dedicated onboard navigation to offer redundancy and choice. Alpine has pioneered split-screen navigation displays that show the 2D maps and 3D landmarks, enhancing driver situational awareness.

- Continental AG is a technological leader in the automotive navigation system market, known for its scalable eHorizon platform that combines navigation data with predictive vehicle control. This strategic initiative uses digital map data and GPS positioning to anticipate road gradients, speed limits, and traffic signs, enabling fuel-efficient driving and ADAS functionality. In 2024, the company made sales of USD 42.9 billion.

- Aptiv PLC has redefined its role in the automotive navigation system market by focusing on software-defined navigation architectures for electric and autonomous vehicles. The company’s strategic initiative includes the development of a centralized navigation compute platform that integrates GNSS, inertial measurement, and vision-based localization. In 2025, the company made a percentage of net sales of 19.1%.

Here is a list of key players operating in the global automotive navigation system market:

The automotive navigation system market is highly competitive and is driven by the shift from portable devices to fully integrated connected and autonomous driving solutions. The key players are aggressively adopting strategies such as autonomous driving solutions. The key players are aggressively adopting strategies such as partnerships with cloud service providers for real-time traffic data integration of augmented reality dashboards and development of electric vehicle optimized routing. Mergers and acquisitions are common to consolidate mapping data and software capabilities, while investments in over-the-air updates and AI-based predictive navigation are central to retaining automotive navigation system market share. For example, in March 2025, Hexagon completes the acquisition of Septentrio, expanding the reach of mission-critical navigation and autonomy applications. Companies are also focusing on hardware and software integration to offer seamless infotainment experiences.

Corporate Landscape of the Automotive Navigation System Market:

Recent Developments

- In January 2026, TomTom announced the successful integration of its Automotive Navigation Application with the cognitoAI™ platform from Visteon, a global automotive technology leader in cockpit electronics. This collaboration delivers an onboard AI voice experience deeply integrated with an automotive navigation solution, highlighting a shared commitment to bringing a high-performance, secure, reliable, and intuitive driver experience to automotive navigation system market.

- In July 2025, HERE Technologies, the global leader in digital mapping and location data, and Genesys International, a leading Indian geospatial solutions company, have joined forces to radically improve the in-car navigation experience and strengthen road safety efforts across India.

- In April 2025, ECARX Holdings Inc., a global mobility tech provider, announced a strategic partnership with HERE Technologies, the leading location data and technology platform, to co-develop a next-generation, AI-powered in-vehicle navigation system for global automakers. The new system will make its production-ready debut, alongside a live demonstration, at Auto Shanghai 2025.

- Report ID: 8556

- Published Date: May 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.