Automotive Repair Software Market Outlook:

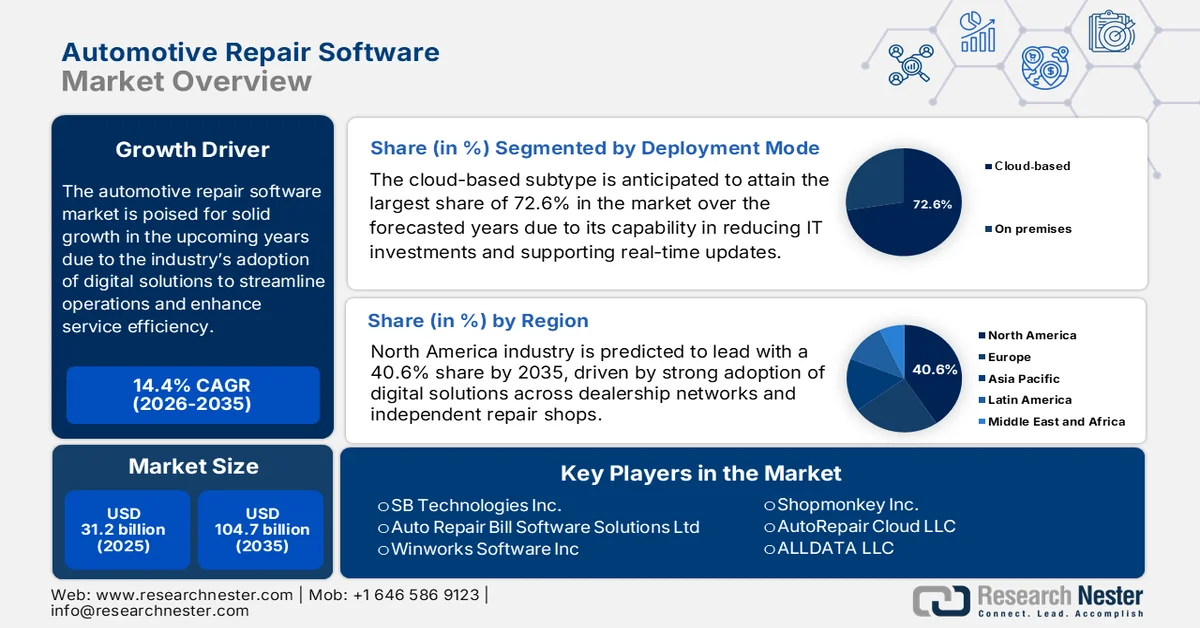

Automotive Repair Software Market size was valued at USD 31.2 billion in 2025 and is expected to grow to USD 104.7 billion by 2035, registering a CAGR of 14.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive repair software is evaluated at USD 35.6 billion.

The automotive repair software market is poised for solid growth in the upcoming years due to the industry’s adoption of digital solutions to streamline operations and enhance service efficiency. The market growth is also carried forward by the rising demand for improved diagnostic tools, cloud-based solutions, and integrated management systems. In this context Congress Government in July 2024 revealed that modern motor vehicles rely on software and telematics to manage operations, deliver proper driver-assistance features, and transmit data to OEM-hosted cloud platforms. This growing integration of cloud-based systems has made access to vehicle data a central issue in the right-to-repair debate. Federal and state policies, including Massachusetts and Maine laws, and proposed federal legislation share the collective goal of ensuring independent repair shops and consumers can access critical vehicle data.

Furthermore, the complexity associated with modern vehicles, national security risks, and the need for proper repair information are encouraging workshops to adopt software solutions that reduce manual errors. As per the September 2024 article published by the Bureau of Industry and Security (BIS), it has proposed a 2024 rule to mitigate national security risks from foreign-controlled information and communications technology that is integral to connected vehicles, particularly from China and Russia. The rule, which is under Executive Order 13873 and IEEPA, mainly focuses on the prohibition of transactions posing undue or unacceptable risks to U.S. critical infrastructure, cybersecurity, or vehicle connectivity systems. Hence, this reflects the intersection of automotive cloud technologies, telematics, and administrative guidelines, benefiting the overall automotive repair software market.

Key Automotive Repair Software Market Insights Summary:

Regional Highlights:

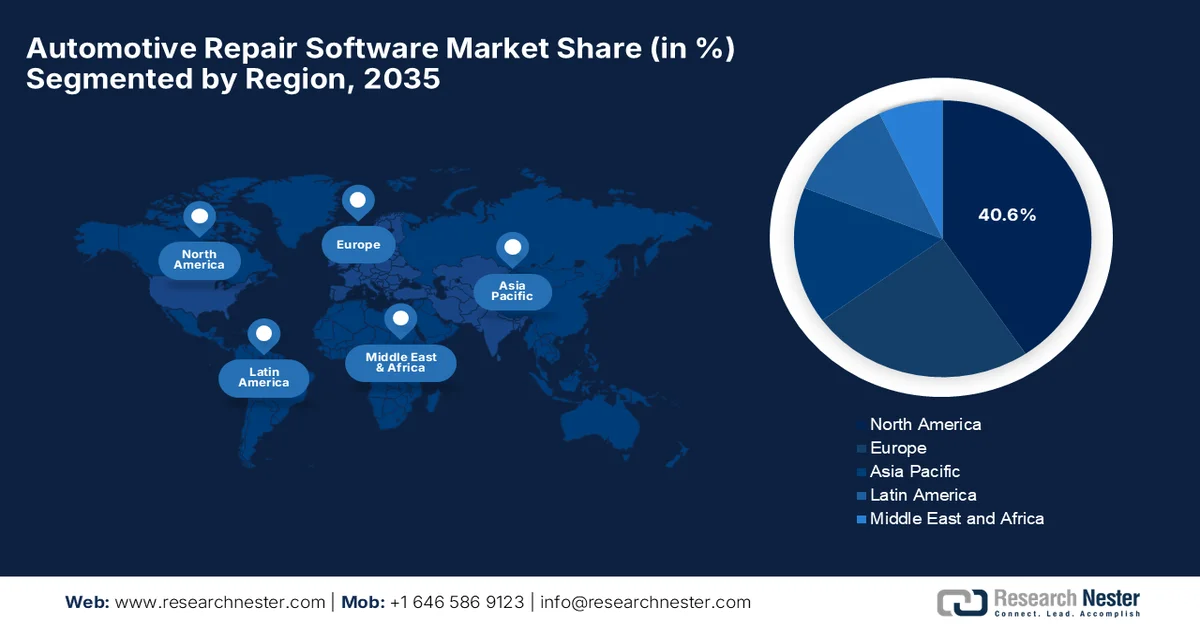

- The automotive repair software market in North America is projected to command a 40.6% share by 2035, underpinned by high digital adoption across dealership networks and independent repair shops.

- Asia Pacific is poised to record the fastest expansion in the forecast period 2026–2035, attributed to rising urbanization and increasing vehicle ownership accelerating workshop digitalization.

Segment Insights:

- In the automotive repair software market, the Cloud-based Deployment segment is projected to account for a 72.6% share by 2035, propelled by its ability to reduce IT investments while enabling real-time updates and remote diagnostics.

- Garage Management Software is anticipated to secure a considerable share by 2035, supported by the increasing shift toward digital workflow automation across automotive service centers.

Key Growth Trends:

- Digital transformation across repair shops

- Integration of AI, IoT & predictive analytics

Major Challenges:

- Data security and privacy concerns

- Resistance to change

Key Players: SB Technologies Inc. (U.S.), Auto Repair Bill Software Solutions Ltd. (UK), Winworks Software Inc. (U.S.), Shopmonkey Inc. (U.S.), AutoRepair Cloud LLC (U.S.), ALLDATA LLC (U.S.), Mitchell Repair Information Company LLC (U.S.), Palmer Products Inc. (U.S.), Fullbay Inc. (U.S.), Identifix Inc. (U.S.), AutoLeap Inc. (U.S.), Workshop Software Pty Ltd. (Australia), GaragePlug Inc. (India), Roadzen Inc. (U.S.), RAMP Software Solutions (Global), Nexsyis Collision Inc. (U.S.), Torque360 Inc. (U.S.), Orderry (Europe), HARMAN Automotive (U.S.), Motosync.ae (UAE), Autorox AI (India), Syncron AB (Sweden).

Global Automotive Repair Software Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 31.2 billion

- 2026 Market Size: USD 35.6 billion

- Projected Market Size: USD 104.7 billion by 2035

- Growth Forecasts: 14.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 9 March, 2026

Automotive Repair Software Market - Growth Drivers and Challenges

Growth Drivers

- Digital transformation across repair shops: Auto repair businesses across most nations are making a shift from manual and paper-based workflows to digital platforms to automate their crucial operations. This shift towards digitalization accelerates service delivery, boosting growth in the automotive repair software market. According to the U.S. Government Accountability Office (GAO) article published in March 2024, the industry associations and automakers reaffirmed a national commitment in 2023 with a collective goal to ensure independent repair shops have access to vehicle telematics and diagnostic data, including for electric and hybrid vehicles, and established stakeholder panels to address technology changes affecting repairs. It also stated that over the recent years, independent repair shops have grown along with the overall vehicle aftercare industry, earning about 70% of post-sale revenues and expanding both in total revenue and number of locations, hence positively impacting automotive repair software market growth.

- Integration of AI, IoT & predictive analytics: This factor in repair software enables predictive diagnostics, parts forecasting, along with certain automated workflow suggestions. Also, the understanding helps to reduce downtime and optimize resource use, which are attractive features for competitive service providers. As of the October 2025 data from the U.S. Department of Transportation (DOT), it makes use of artificial intelligence to enhance safety, innovation, and operational efficiency across transportation systems, which also includes automated driving, unmanned aircraft, and traffic management. Besides, DOT applies AI tools internally and in citizen-facing services, utilizing generative AI, natural language processing, computer vision, and predictive analytics with the main goal to improve processes and research, hence suitable for bolstering the automotive repair software market.

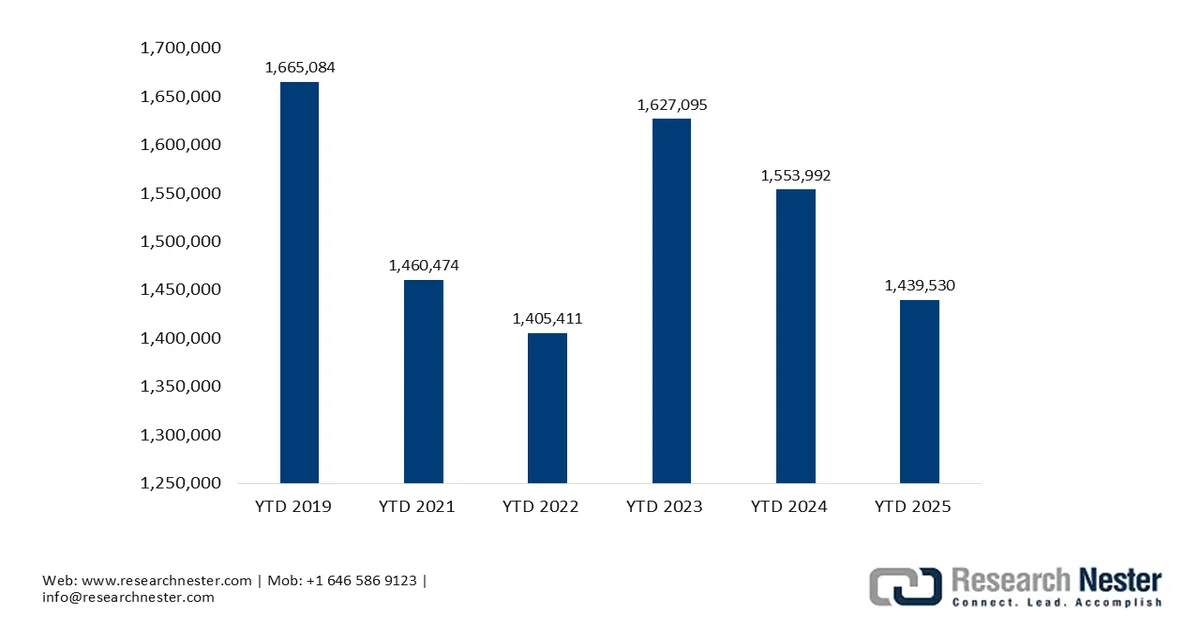

- Growth in vehicle ownership & aftermarket services: The surge in vehicle ownership increases the demand for maintenance and repair services, prompting a profitable business environment for players in the automotive repair software market. Also, this leads to a greater need for systems that manage high service volumes efficiently, from appointment booking to inventory and customer records. According to the official statistics, which were published by the International Organization of Motor Vehicle Manufacturers (OICA) in 2025, that is, quarter 1 to quarter 3, global vehicle production reached 68,755,124 units, out of which 28,549,120 were in developed countries/regions and 40,206,004 in emerging countries/regions. This increase in the total number of vehicles denotes a huge growth opportunity for the market’s expansion and exposure.

Global Motor Vehicle Production Trends (2022-2024) by Developed and Emerging Regions

|

Units |

Year to Date (YTD) 2022 (Q1-Q3) |

YTD 2023 (Q1-Q3) |

YTD 2024 (Q1-Q3) |

|

Developed Countries/Region |

26,376,009 |

30,112,073 |

28,874,456 |

|

Emerging Countries/Regions |

34,523,711 |

36,939,025 |

37,364,940 |

|

Total |

60,899,720 |

67,051,098 |

66,239,396 |

Source: OICA

Challenges

- Data security and privacy concerns: Most of the automotive repair software stores customer information such as contact details, vehicle history, and payment data. In this context, cybersecurity concerns as ransomware or data breaches, can compromise this information, which can lead to legal liabilities. A large portion of small repair shops lack the expertise or resources to implement proper security measures. On the other hand, compliance with data protection regulations is also complex, particularly for cloud-based solutions. Therefore, vendors in the automotive repair software market need to focus on encryption, secure access controls, and regular audits, whereas businesses must maintain proper measures for password management and backup protocols.

- Resistance to change: Numerous automotive repair shops are dependent on manual processes and the traditional way of record-keeping. Also, employees and management in certain emerging nations might not opt for software due to fear of complexity and disruption. Resistance may appear as a hesitation to enter data accurately, ignoring software features, or rejecting digital tools entirely. Therefore, addressing these cultural obstacles in the automotive repair software market in turn necessitates clear communication, training, and demonstration of the software’s benefits, such as reduced paperwork and faster diagnostics. Change management is highly essential, especially in family-owned or long-established workshops where habits are deeply entrenched, whereas failure to address resistance can lead to underutilization of the digital solutions.

Automotive Repair Software Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.4% |

|

Base Year Market Size (2025) |

USD 31.2 billion |

|

Forecast Year Market Size (2035) |

USD 104.7 billion |

|

Regional Scope |

|

Automotive Repair Software Market Segmentation:

Deployment Mode Segment Analysis

The cloud-based sub-segment is anticipated to attain the largest share of 72.6% in the automotive repair software market over the forecasted years. The dominance is highly attributable to its capability in reducing IT investments, supporting real-time updates across shop locations, and enabling remote analytics & mobile diagnostics. In February 2025, CCC Intelligent Solutions reported that it integrated its CCC repair workflow with Tekion’s cloud-native automotive retail cloud platform to enable dealer-owned collision centers to manage repairs from start to finish through a unified cloud system. This integration reduces manual data entry, synchronizes repair orders, vehicle information, and accounting details, and supports real-time updates across locations. Hence, such developments from the global players will position the subtype as the gold standard to generate revenue in this sector.

Type of Software Segment Analysis

Garage management software is expected to hold a considerable share in the automotive repair software market by 2035. The structural shift towards digital workflow automation, wherein most of the service centers are implementing integrated platforms to oversee their operations from start to finish are certain driver uplifting the subtype’s growth in this field. In this context, autoGMS in June 2025, notified that it has launched the technician management feature, which enables the garages to assign jobs, track progress, and communicate with customers directly from the platform. The company also notes that technicians can log updates, attach photos, notes, and warranty documents, improving record-keeping and workflow visibility. This update exemplifies the prominence of the segment in streamlining operations, hence denoting a positive automotive repair software market outlook.

End user Segment Analysis

By the conclusion of the forecast period, the independent auto repair shops, which are a part of the end user segment is predicted to grow at a significant rate in the automotive repair software market. The sheer number of local, independent garages worldwide that are adopting digital solutions to stay competitive against larger franchise and dealership networks is the main factor driving the subtype’s leadership. Regulatory drivers also strengthened this segment by guaranteeing access to OEM diagnostic data, enabling independent shops to perform advanced repairs. Moreover, investments in terms of mobile diagnostics and integrated customer communication tools are enhancing operational efficiency. In addition, the aspect of partnerships with parts suppliers and cloud-based analytics platforms is enabling better inventory management, hence denoting a wider segment scope.

Our in-depth analysis of the automotive repair software market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Mode |

|

|

Type of Software |

|

|

End user |

|

|

Vehicle Type |

|

|

Organization Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Repair Software Market - Regional Analysis

North America Market Insights

The North America automotive repair software market is expected to register its dominance by capturing 40.6% of the revenue share by 2035. The region’s leadership is majorly driven by high digital adoption across dealership networks and independent repair shops. Forecast growth is also supported by strong SaaS penetration, cloud-based diagnostics, and integrated workflow platforms. For instance, in July 2023, independent auto repair organizations and leading automakers signed a right-to-repair agreement to make sure that independent repair shops have access to the same diagnostic and repair information as authorized dealer networks for all vehicle types and powertrains, including gasoline, diesel, electric, hybrid, and fuel cell. The pact also guarantees access to telematics data and includes commitments to education and training through automaker portals and platforms such as OEM1Stop.com, hence making it suitable for standard market growth.

Shortage of technicians is forcing shops to use software to optimize workflows, driving growth of the U.S. automotive repair software market. The utilization is deeply embedded in the maintenance ecosystem of independent garages and dealership networks. The country’s workshops incorporate cloud-based and mobile platforms to meet evolving service demands. In this regard, Way.com in January 2026 announced that it had launched the AI-based repair & maintenance platform, which is a shop management system especially designed for independent auto repair shops across the U.S. This particular cloud-based solution consists of AI voice agents, instant estimates, digital invoicing, inventory synchronization, and analytics tools to streamline daily operations and improve efficiency. Hence, with constant efforts from domestic pioneers, the country is all set to witness unprecedented growth in the upcoming years.

The fleet service providers and multi-location auto care networks are identified as the leading adopters of digital solutions, which is the main factor driving growth in the Canada automotive repair software market. The growing demand for fleet analytics and service management tools supports software deployment beyond major urban centers. In October 2025, Fleetio reported that it is expanding the maintenance shop network into Canada by extending its cloud-based fleet maintenance platform to operators in the country. The expansion enables fleets to access trusted repair partners, repair tracking, automated approvals, consolidated billing, and centralized service history for improved visibility as well as cost control. Hence, this denotes that there is a shift toward cloud-based, data-driven repair management across fleets in the country, denoting a lucrative growth opportunity for the automotive repair software market.

APAC Market Insights

The Asia Pacific automotive repair software market is likely to exhibit the fastest growth from 2026 to 2035. The region benefits from rising urbanization and an increase in vehicle ownership. The region’s development of organized automotive service chains and government initiatives encouraging workshop digitalization accelerate software uptake. In June 2025, Japan’s Ministry of Economy, Trade and Industry (METI) and Ministry of Land, Infrastructure, Transport and Tourism (MLIT) released an updated mobility digital transformation strategy with a primary focus on strengthening the global competitiveness of the country’s automotive industry. The strategy is mainly focused on accelerating investment in terms of the software-defined vehicles, improving AI-based autonomous driving technologies, promoting data integration, and building collaborative industry platforms, hence supporting the adoption of automotive repair platforms.

The fast growth of urban garages and an expanding aftermarket service sector is responsible for uplifting the automotive repair software market in China. The government's efforts to digitalize the automotive industry are fueling increased adoption of this sector. The rapid adoption of new energy vehicles, and a massive, maturing car parc vehicles also propels growth in the market. Based on government data, which was published in January 2026, China’s Ministry of Industry and Information Technology, together with the Ministry of Education, State Administration for Market Regulation, and National Data Administration, issued the implementation plan for the digital transformation of the automotive industry. The initiatives include improving diagnostic assessment systems, promoting digital transformation for small and medium-sized auto parts enterprises, demonstrating AI applications, and enabling collaborative digital supply chains. This supports the adoption of automotive repair and service platforms nationwide.

The automotive repair software market in India is making a transition towards scalable and affordable software, making it suitable for smaller independent garages and SMEs. Government backing and mobile platforms that reduce infrastructure burdens and offer localized language support are gaining traction as repair businesses modernize operations and improve customer service efficiency. The eTransport Mission Mode Project, which is led by the country’s Ministry of Road Transport and Highways, is a nationwide eGovernance initiative that digitizes RTO operations and citizen services through applications such as Vahan, Sarathi, eChallan, PUCC, and NextGen mParivahan. By June 2025, this platform will have enabled more than 40,000,000 vehicle registrations, 22,000,000 driving licenses, and 35,000,000 challans, while also supporting 27,000 digitized driving schools and 48,000 PUC centers. It has generated approximately USD 9,600,000,000 in Vahan revenue, USD 2,160,000,000 in Sarathi revenue, and USD 2,400,000,000 from challan penalties.

Europe Market Insights

With the presence of structured after-sales ecosystems, rising vehicle production regulatory compliance requirements, and a focus on maintenance precision, the automotive repair software market in Europe is expected to witness exceptional growth during the stipulated timeframe. Besides the aspect of strict regulations regarding vehicle emissions, safety increases demand for software that ensures compliance and transparent data reporting. In September, 2025, the European Commission published certain guidelines on vehicle data accompanying the Data Act to clarify the obligations for access and use of vehicle-generated information under Chapter II of the regulation. It is mainly focused on the automotive sector, which includes OEMs, suppliers, aftermarket service providers, and insurers, highlighting the rules for fair and secure data access. Furthermore, it emphasizes that the content is strictly applicable to the automotive industry and cannot be directly applied to other sectors or public services, hence, by ensuring standardized access to vehicle data for independent operators.

Europe Light Commercial Vehicle Production Trends (2019-2025 Q1-Q3)

Source: OICA

The combination of premium service centers and small to medium workshops that are adopting software solutions for maintenance recording and repair efficiency fuels the strong growth of the automotive repair software market in Germany. Competitive pressures and the need for workflow tools that support multi-brand servicing contribute to substantial software investment and innovation in the country. In May 2023, Bosch notified that it is restructuring its automotive-supply business into a dedicated Bosch Mobility sector with the main goal of strengthening its focus on software-driven mobility and accelerating growth. The reorganization is mainly focused on cross-divisional collaboration and aims to generate more than USD 84 billion in sales by 2029. Such tactical steps from the leading pioneers reflect the country’s investment in this sector, thereby enabling both premium service centers and smaller workshops to adopt advanced digital tools for repair efficiency.

The UK automotive repair software market is a representation of a balance between traditional on-site systems and cloud native software, with upgrades mostly focusing on accessibility and centralized customer service data. The rising vehicle ownership in the country is encouraging automotive repair shops to integrate digital platforms to automate invoicing, parts procurement, and workshop scheduling. Based on the government data, which was published in June 2025, the Department for Transport in the UK reported 2,605,000 vehicles were registered in 2024, for the first time, which is a 3% increase from 2023, including 410,000 new zero-emission vehicles, up 20% from the previous year. By the end of 2024, there were 41.7 million licensed vehicles on the country’s roads, marking a 1% rise, with 1,394,000 zero-emission vehicles, up 37%. Therefore, from a strategic perspective, these statistics highlight the growing adoption of cleaner vehicles and support the automotive repair software for managing and servicing an evolving vehicle fleet.

Key Automotive Repair Software Market Players:

- SB Technologies Inc. (U.S.)

- Auto Repair Bill Software Solutions Ltd. (UK)

- Winworks Software Inc. (U.S.)

- Shopmonkey Inc. (U.S.)

- AutoRepair Cloud LLC (U.S.)

- ALLDATA LLC (U.S.)

- Mitchell Repair Information Company LLC (U.S.)

- Palmer Products Inc. (U.S.)

- Fullbay Inc. (U.S.)

- Identifix Inc. (U.S.)

- AutoLeap Inc. (U.S.)

- Workshop Software Pty Ltd. (Australia)

- GaragePlug Inc. (India)

- Roadzen Inc. (U.S.)

- RAMP Software Solutions (Global)

- Nexsyis Collision Inc. (U.S.)

- Torque360 Inc. (U.S.)

- Orderry (Europe)

- HARMAN Automotive (U.S.)

- Motosync.ae (UAE)

- Autorox AI (India)

- Syncron AB (Sweden)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ALLDATA LLC is identified as one of the longest-standing providers of automotive repair information and software. The firm offers a broad suite of products, such as OEM diagnostic data, collision repair databases, and shop management tools, and has expanded its digital toolkit with mobile apps and community platforms.

- Mitchell is a specialist player, and it provides aftermarket software solutions that help repair facilities with collision and mechanical workflows, parts and labor estimation, and customer service optimization. The company benefits from an extensive adoption across North America, and its platforms merge repair information with operational management tools.

- GaragePlug Inc. is yet another prominent player in this field that benefits from a global-oriented auto repair and workshop management platform. This platform is mostly focused on cloud-based digital transformation of service operations, inventory tracking, customer communication, and AI-powered analytics.

- Orderry offers a web-based work order and garage management system that combines job scheduling, repair updates, customer communications, inventory control, and invoicing within a single platform. The company is mainly focused on real-time transparency for customers and operational efficiency for shops makes it well-suited for independent garages and multi-location service providers.

- Syncron is a major provider of cloud-based aftermarket and service operations software for OEMs and distributors with strong capabilities in parts pricing, warranty management, centralized repair operations, and field service support. The firm has a global presence, and its services help large dealers and repair networks optimize spare parts inventory and technician enablement.

Below is the list of some prominent players operating in the global automotive repair software market:

The automotive repair software market is extremely competitive. Established U.S. based pioneers such as Shopmonkey, Mitchell, and Fullbay are dominating this field with deep integration and extensive features, whereas the newer SaaS platforms are focused on cloud‑native solutions, mobile accessibility, and AI capabilities. Europe-specific players mostly adapt to regional compliance and multilingual requirements. AI-driven diagnostics, real-time workflow automation, mergers & acquisitions, and integrations with parts, CRM, and insurer systems are the tactical strategies adopted by the leading players in this sector. For instance, in September 2024, Vehlo acquired Shop-Ware, which is a leading cloud-based shop management platform, to strengthen its aftermarket suite with automation and customer communication tools hence suitable for bolstering the industry growth.

Corporate Landscape of the Automotive Repair Software Market:

Recent Developments

- In January 2026, Roadzen Inc. announced that it had acquired VehicleCare, which is an AI-based vehicle repair and workshop aggregation platform, at CES 2026, valuing its India business at a total of USD 277 million. The acquisition integrates VehicleCare’s software-enabled national network by enabling end-to-end claims execution and AI-based optimization for insurers.

- In December, 2024, HARMAN Automotive reported that it has launched Ready CQuence Loop and Ready Link Marketplace to speed automotive software development and enhance in-vehicle experiences. Ready CQuence Loop virtualizes testing for faster feature delivery, whereas Ready Link Marketplace offers apps and services with monetization capabilities.

- Report ID: 8422

- Published Date: Mar 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.