Automotive Glass Market Outlook:

Automotive Glass Market size was valued at USD 34.3 billion in 2025 and is projected to reach USD 55.5 billion by the end of 2035, rising at a CAGR of 5.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of automotive glass is evaluated at USD 36.1 billion.

The automotive glass market is entering into a new phase of growth, positively impacted by the rising global production and sales of passenger cars and commercial vehicles, which creates constant demand for both original equipment and replacement components. As per an article published by the International Energy Agency (IEA) in November 2025, the global car industry is undergoing a structural shift, wherein electric and hybrid vehicles are driving surging growth, representing around 30% of total sales in 2024. Besides, China has become the largest car producer and exporter, accounting for almost 40% of global manufacturing capacity, whereas Europe and North America each hold 15%. New entrants, especially China-based EV makers and Tesla, captured 45% of global electric car sales, supported by government policies, manufacturing capacity, and competitive pricing, thereby driving upstream materials and component supply chains.

Furthermore, the automotive glass market is stimulated by the expanding adoption of electric vehicles and the rising demand for premium sunroofs. Meanwhile, the government subsidies have been a persistent feature of the global car industry, with new pure-play electric vehicle entrants generally receiving larger support when compared to the legacy carmakers. In this context, the Organization for Economic Co-operation and Development (OECD) in February 2025 revealed that China-based carmakers, including both state-owned and private EV firms, receive higher subsidies when compared to those in OECD countries. This is attributed to the large scale of domestic production and international expansion. In addition, the growing share of China-based EV sales denotes intensifying competition with established OECD carmakers, highlighting the trade and policy implications of subsidies in the global EV category. Hence, this accelerates higher demand for specialized windshields, laminated glass, and component integration across global assembly lines.

Key Automotive Glass Market Insights Summary:

Regional Highlights:

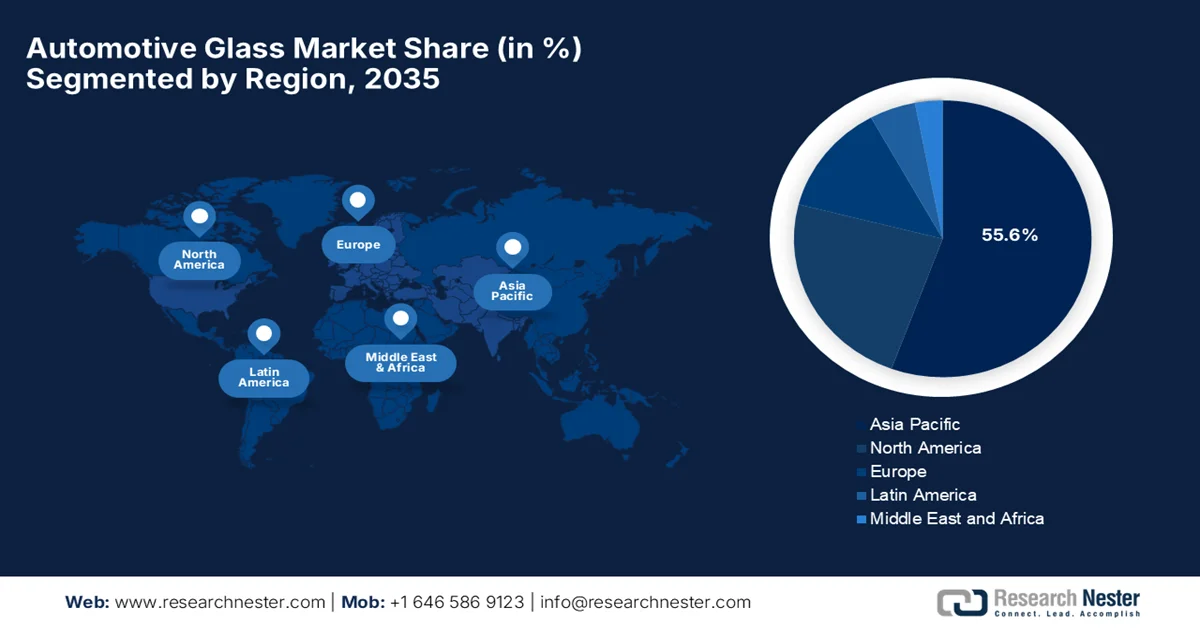

- Asia Pacific is projected to dominate the automotive glass market with a 55.6% share by 2035, bolstered by rapid automotive sector expansion and rising vehicle demand across diverse segments

- North America Market is expected to witness notable growth through 2026-2035, attributed to increasing adoption of lightweight and eco-friendly glass materials for improved fuel efficiency

Segment Insights:

- Original Equipment Manufacturer segment in the automotive glass market is estimated to command a 90.4% share by 2035, propelled by strong collaboration between OEM suppliers and automakers to deliver customized glass solutions

- Laminated Glass Type segment is poised for considerable expansion during 2026-2035, fueled by stringent safety regulations and increasing investments in production capacity expansion

Key Growth Trends:

- Advanced technology & smart glass

- Safety standards & regulations

Major Challenges:

- Supply chain disruptions

- Environmental and sustainability pressures

Key Players: AGC Inc., Saint-Gobain, Nippon Sheet Glass Company, Fuyao Glass Industry Group, Guardian Industries, Corning Incorporated, Xinyi Glass Holdings Limited, Central Glass Co., Ltd., Şişecam Group, Vitro S.A.B. de C.V., Magna International Inc., Gentex Corporation, Webasto SE, PGW Auto Glass, Apollo Funds, Canatu.

Global Automotive Glass Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 34.3 billion

- 2026 Market Size: USD 36.1 billion

- Projected Market Size: USD 55.5 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (55.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Brazil, Mexico, Indonesia

Last updated on : 6 April, 2026

Automotive Glass Market - Growth Drivers and Challenges

Growth Drivers

- Advanced technology & smart glass: The innovations in terms of advanced driver assistance systems and heads-up displays require high‑optical‑clarity glass to support sensors and displays. This factor propels the continued growth of the automotive glass market since smart glass technologies, such as electrochromic and PDLC, adjust transparency and improve comfort and safety. In April 2025, Gauzy Ltd. announced that its dual smart glass technologies combining SPD and PDLC were implemented in 75% of the glazing of the Mercedes-Benz Vision V show car. This configuration enables dynamic transitions between transparent, shaded, and private states, supporting comfort, privacy, and digital projection applications. In addition, such a kind of technology addresses glare, reduces cabin temperature, and maintains optical clarity for passengers.

- Safety standards & regulations: The implementation of stricter regulations, i.e., mandatory laminated windscreens and tempered glass requirements, encourages the use of high-performance glass to protect passengers and meet design mandates. The Safety Glass Amendment Order was issued by the Ministry of Commerce and Industry, Government of India, in March 2023, under the powers of the Bureau of Indian Standards Act. In this context, it amends the safety glass order and imposes mandatory compliance with safety glass standards for automotive use in India. This particular order provides exemptions for manufacturers importing safety glass for producing up to 10,000 vehicles per year and for importing up to 5,000 safety glass units annually for repairs or after-sales service. Hence, such regulations drive the growth of the automotive glass market by ensuring that automotive glazing meets safety standards to protect passengers.

- Massive boom in consumer demand: The automotive glass market is seeing an incremental demand for attributes such as panoramic roofs, UV, IR protection, and reduced noise, which is driving premium glass adoption across different vehicle segments. In November 2025, the article published by Windshield Advisor reported that modern laminated automotive glass is a carefully prepared blend of two glass layers bonded with a PVB interlayer that provides both safety and comfort. Moreover, it blocks almost 99% of harmful UV radiation, reduces cabin noise through acoustic dampening, and maintains structural integrity, thereby supporting roof strength and proper airbag deployment in crashes. Therefore, the presence of these features enhances occupant protection and comfort, driving demand for premium glass in vehicles, hence benefiting the overall automotive glass market growth.

Challenges

- Supply chain disruptions: Interruptions in the logistical network of raw materials directly impact the growth of the automotive glass market. The industry is majorly relying on a supply chain for raw materials, components, and logistics. Any interruptions caused by geopolitical issues or transportation issues can ultimately cause delays to production and, hence, increased expenses. The just-in-time manufacturing model used by many automakers leaves little room for delays, adding additional pressure on glass suppliers to deliver on tight schedules. On the other hand, the aspect of shortages of critical materials or components can halt production lines entirely. In this context, building resilient supply chains requires diversification, inventory management, and strategic partnerships, all of which add complexity and cost, thus negatively impacting the market’s exposure.

- Environmental and sustainability pressures: There has been a growing concentration on environmental degradation, which encourages investments in sustainable practices. The aspect of glass production needs higher energy, and it also contributes to carbon emissions, making it a main target for decarbonization efforts. Therefore, this factor adds pressure on companies to reduce their carbon emissions and improve recycling rates. Transitioning to greener technologies necessitates burgeoning investments and process changes, making it challenging for small-scale players in the automotive glass market. Recycling automotive glass is complex, which is influenced by lamination and coatings, complicating material recovery, hence a major hurdle for industry players.

Automotive Glass Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 34.3 billion |

|

Forecast Year Market Size (2035) |

USD 55.5 billion |

|

Regional Scope |

|

Automotive Glass Market Segmentation:

End use Segment Analysis

The original equipment manufacturer is forecasted to garner a dominant 90.4% share of the automotive glass market by the end of the projected time period. This segment consists of the production and supply of glass directly to vehicle manufacturers for factory installation. At the same time, OEM suppliers work closely with automakers with the main goal of delivering customized glass solutions designed for specific vehicle models. In January 2025, FORVIA HELLA and Fuyao Group jointly won the 2025 automotive industry sustaining power award for their switchable intelligent glass. Besides, this innovation allows adjustment of transparency for sunroofs and windows, combining Fuyao’s glass expertise with HELLA’s electronic control technologies. Therefore, the collaborative efforts reflect cross-disciplinary innovation, allowing players to gain a competitive edge in the evolving automotive glass market category.

Glass Type Segment Analysis

The laminated glass type segment is anticipated to grow considerably in the automotive glass market during the assessment period. The segment’s growth is largely ascribed to the stringent safety regulations requiring laminated windshields and rising emphasis on production capacity expansion to meet the swelling end user demand. In March 2025, Thaco Industries announced the launch of a premium automotive glass plant in Vietnam, which has an annual capacity of up to 450,000 sets, producing windshields, back glass, and door glass for passenger cars using advanced automated technologies from Italy, Germany, and Japan. The plant consists of automated cutting, grinding, drilling, and tempering lines, including laminated glass production with vacuum chambers, ensuring high precision, durability, and compliance with Vietnam and Europe-based safety standards, hence denoting a huge exposure for the segment’s growth.

Vehicle Type Segment Analysis

The passenger cars segment is predicted to account for a significant share of the automotive glass market over the forecasted years. This segment consists of glass products specifically designed for vehicles intended for personal transportation, including windshields, side windows, and rear windows for sedans, hatchbacks, and SUVs. Exemplifying this, the official statistics published by Invest India observed that India’s automobile sector recorded a turnover of USD 240 billion in FY 2024-25, wherein the exports crossed 5.3 million units, including 770,000 passenger vehicles. Besides, it also stated that leading companies such as Skoda Auto Volkswagen India export about 30% of their production, whereas Maruti Suzuki exports nearly 280,000 units annually, which reflects the segment’s growing global footprint. Hence, passenger cars play a pivotal role in both export growth and domestic consumption, solidifying their position in the global automotive industry.

Our in-depth analysis of the automotive glass market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Glass Type |

|

|

Vehicle Type |

|

|

Technology |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Glass Market - Regional Analysis

APAC Market Insights

The Asia Pacific automotive glass market is anticipated to garner the largest share of 55.6% by the end of the forecast period. The region’s dominance is effectively fueled by strong growth in the automotive sector and high vehicle demand across multiple segments. Factors such as rapid urbanization, rising disposable incomes, and a growing population are fueling increased automobile sales. According to the article published by the International Trade Administration in November 2025, Japan registered itself as the world’s fourth-largest automotive industry, selling over 4.4 million new passenger vehicles in 2024. Domestic brands have consolidated market share, with Toyota, Honda, Nissan, and others holding 95% of the automotive glass market, whereas imports account for 5%. On the other hand, hybrid vehicles are also highly popular, with adoption surpassing two million units in 2024 and now representing 54.8% of new passenger car sales, thus driving extensive demand for automotive glass.

Japan New Vehicle Sales Breakdown 2021-2024: Passenger Cars, Trucks, Buses, Kei, Hybrid, and Electric Vehicles

|

Vehicle Type |

2021 |

2022 |

2023 |

2024 |

|

Total New Vehicle Sales |

4,448,340 |

4,201,320 |

4,779,086 |

4,421,494 |

|

Passenger Cars |

3,675,698 |

3,448,297 |

3,992,727 |

3,725,200 |

|

Trucks |

765,762 |

747,543 |

777,949 |

686,197 |

|

Buses |

6,880 |

5,480 |

8,410 |

10,097 |

|

Kei Car Sales |

1,652,522 |

1,638,136 |

1,744,919 |

1,557,868 |

|

Hybrid Vehicle (HV) Sales |

1,441,487 |

1,467,683 |

1,868,625 |

2,040,181 |

|

Electric Vehicle (EV) Sales |

21,693 |

58,813 |

88,535 |

59,736 |

Source: ITA

With drivers and passengers seeking safety and comfort, coupled with the integration of advanced optical and mechanical technologies, the China automotive glass market is becoming more popular in the region. As a critical element of advanced automotive technology, smart glass is progressively enhancing the in-vehicle experience. In July 2024, the Information Technology & Innovation Foundation (ITIF) reported that China has become the global leader in EVs and batteries, producing almost 62% of the world’s EVs and 77% of EV batteries as of 2022, with exports rising 851% between 2020 and 2023. On the other hand, patent activity has surged too, with China’s share in electric propulsion rising significantly in a span of ten years. Moreover, China-based EVs showcase innovations such as multiple display screens, karaoke microphones, and USD 350 price point augmented reality glasses offered by Nio for passengers, highlighting both technological ambition and consumer-focused creativity.

In India, the automotive glass market is supported by surging vehicle production and a shift toward premium attributes such as panoramic sunroofs and acoustic glazing. The industry is transitioning toward advanced safety standards, with a heavy reliance on laminated windshields and tempered side glass. Based on government data, the Production Linked Incentive Scheme for automobile and auto components has a total budget of USD 3.1 billion for five years, i.e., FY 2022-23 to FY 2026-27, to boost the manufacturing of over 50 advanced automotive technology products. This scheme highly targets deep localization, creation of domestic and global supply chains, and focuses on zero-emission vehicle deployment. Meanwhile, incentives are disbursed annually from FY 2023-24 to FY 2027-28, thereby covering more than 200 auto and component manufacturers. This is bolstering market growth in the country.

North America Market Insights

The North America automotive glass market is set for significant growth, fueled by the primary demand for lightweight materials to improve fuel efficiency. This creates strong demand for eco-friendly glass solutions. Moreover, the push for aerodynamic vehicle designs has encouraged the use of nanotechnology to develop self-cleaning, anti-glare, and high-clarity glass products. As of May 2025, data from the U.S. Environmental Protection Agency (EPA) show that the glass manufacturing effluent guidelines regulate wastewater discharges from both direct and indirect glass manufacturers, which include automotive glass, plate glass, fiberglass, and containers. It notes the imposed limits on pollutants such as ammonia, BOD, COD, fluoride, lead, oil, phenol, phosphorus, pH, and TSS, with some waste streams requiring zero discharge. Besides, these regulations are applied through NPDES permits for direct dischargers and pretreatment or other control mechanisms for indirect dischargers, hence encouraging the use of sustainable manufacturing processes.

The advanced technological integration and a high concentration of premium vehicle features are reshaping the growth dynamics of the automotive glass market in the U.S. The country benefits from a resilient aftermarket segment, driven by a massive existing vehicle fleet and specialized service networks. In August 2025, the U.S. International Trade Commission reported that total investment in U.S. automotive manufacturing reached a significant value of USD 87.8 billion in 2023, largely driven by electrification, with parts manufacturing investments more closely tied to rules of origin. In addition, the country’s market shares of vehicle sales and parts consumption have remained relatively stable, whereas light-vehicle and parts production have increased, reflecting improved competitiveness, denoting a lucrative growth opportunity for the automotive glass industry.

The automotive glass market in Canada is supported by increasing integration of specialized technologies, including heated glass, to address the country's cold climate. Moreover, the mutually profitable collaborations between glass manufacturers and original equipment manufacturers ensure a steady supply of specialized glass for both domestic and imported vehicles. Based on the government data published in February 2026, Canada launched consultations to strengthen its automotive remission framework, with a collective goal to attract more investment and protect domestic jobs in a rapidly evolving global industry. The initiative is part of a new auto strategy that focuses on building made-in-Canada vehicles and positioning the country as a leader in EV production. The article notes that with more than 500,000 workers supported by the sector and 90% of vehicles exported to the U.S., the framework seeks to counter U.S. tariffs and ensure long-term competitiveness for the country’s manufacturers.

Europe Market Insights

There is a huge opportunity for Europe automotive glass market due to a primary focus on eco-friendly automotive products and high-tech integration. Manufacturers in the region are utilizing ultra-thin, lightweight glazing and solar-control glass to extend battery range and reduce the load on climate control systems. In July 2025, Cary Group announced that its subsidiary ExpressGlass acquired Newcar to expand its automotive glass repair and replacement footprint in Portugal. The acquisition adds 32 workshops to ExpressGlass’s network, increasing its total presence to 120 locations. Therefore, this particular move reflects ongoing consolidation in Europe’s fragmented automotive glass repair and replacement category, which is strengthening regional service coverage and operational scale. Furthermore, the growing investment in automotive glass aftermarket services supports maintenance and calibration needs across modern vehicles.

A rapid shift toward smart glass technologies, including head-up display integration and switchable transparency for panoramic roofs, is responsible for uplifting the automotive glass market in Germany. A strong focus on vehicle engineering and OEM-led innovation is accelerating the use of multi-functional glass with embedded antennas, heating layers, and display capabilities. In October 2024, the article published by the International Council on Clean Transportation revealed that Germany’s passenger car fleet faces a major decarbonization challenge, aimed at achieving zero emissions by 2035. Current policies will cut emissions, but a gap of 34 Mt CO2e remains for 2030, requiring additional measures. The article notes that a scrappage program targeting older diesel and gasoline cars could close about one-third of this gap, delivering cost-effective reductions denoting a lucrative growth opportunity for sustainable automotive glass.

In the UK, the automotive glass market is growing, backed by the evolution of the vehicle aftermarket and service ecosystem, where demand is increasingly influenced by repair, replacement, and recalibration needs rather than only in terms of new vehicle production. In February 2026, the country’s government announced the launch of a consultation proposing to mandate the fitment of up to 18 advanced vehicle safety technologies that are also under the GB type approval scheme for mass-produced vehicles. Besides these measures, which aim to enhance road safety, reduce collisions, and align GB safety standards. The proposal covers both active systems, such as emergency braking, lane-keeping, and intelligent speed assistance, and passive measures, such as strengthened structures and pedestrian protection. Hence, such an initiative reflects the country’s focus on integrating advanced safety technologies into vehicles, driving demand for compatible automotive components, including high-performance windshields and sensor-ready glazing.

Key Automotive Glass Market Players:

- AGC Inc. (Japan)

- Saint-Gobain (France)

- Nippon Sheet Glass Company (Japan)

- Fuyao Glass Industry Group (China)

- Guardian Industries (U.S.)

- Corning Incorporated (U.S.)

- Xinyi Glass Holdings Limited (China)

- Central Glass Co., Ltd. (Japan)

- Şişecam Group (Turkey)

- Vitro S.A.B. de C.V. (México)

- Magna International Inc. (Canada)

- Gentex Corporation (U.S.)

- Webasto SE (Germany)

- PGW Auto Glass (U.S.)

- Apollo Funds (U.S.)

- Canatu (Finland)

- Schott AG (Germany)

- Automotive Glass Experts (Netherlands)

- Wallglass (Belgium)

- Asahi India Glass Limited (India)

- Tata AutoComp Systems Limited (India)

- Samvardhana Motherson Group (India)

- Taiwan Glass Industry Corporation (Taiwan)

- Shanghai Yaohua Pilkington Glass Group (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- AGC Inc. is a global leader in automotive glass, which is best known for its strong OEM relationships and advanced glazing technologies. Besides, the company is highly focused on innovation in smart glass, head-up display integration, and solar control glass, positioning itself at the forefront of next-generation mobility solutions.

- Saint-Gobain, through its automotive glazing division, is identified as the leading player in this sector. The company is readily advancing lightweight glazing, acoustic glass, and smart glazing technologies, making it suitable for premium and EV segments.

- Nippon Sheet Glass Company is a major global supplier with a broader portfolio of glass products spanning automotive, architectural, and specialty glass. NSG highly concentrates on improved automotive glazing and ADAS-compatible windshields, aiming to enhance competitiveness as well as profitability.

- Fuyao Glass Industry Group is one of the largest automotive glass manufacturers globally. In addition, the firm has built its competitive edge through cost efficiency, large-scale production, and close partnerships with global automakers, allowing it to maintain a strong position in this field.

- Guardian Industries is a subsidiary of Koch Industries and plays a significant role in automotive and specialty glass categories. The firm’s primary emphasis on energy-efficient products and sustainable manufacturing aligns with evolving automotive industry requirements, particularly in terms of EVs and environmentally conscious markets.

Below is the list of some prominent players operating in the global automotive glass market:

The automotive glass market is dominated by prominent companies such as AGC Inc., Saint-Gobain, and Nippon Sheet Glass Company, which benefit from strong R&D and global OEM relationships. Leading pioneers are highly focused on strategic initiatives such as mergers, partnerships, and capacity expansion to strengthen regional presence. In addition, collaborations with EV manufacturers and technology firms are enabling innovation in solar glass and sensor-integrated windshields, thereby intensifying competition amongst the established and newly entering players. For instance, in February 2026, Automotive Glass Experts announced Wallglass, which is an automotive glass manufacturer, as its new partner supplier. This partnership strengthens AGE’s supplier ecosystem in Europe, ensuring reliability and consistent product quality for members.

Corporate Landscape of the Automotive Glass Market:

Recent Developments

- In March 2026, Apollo Funds announced the acquisition of Nippon Sheet Glass Company, Limited, with a total private equity investment of USD 3.7 billion to support long-term growth in terms of automotive, architectural, and solar glass segments.

- In March 2026, Canatu signed a two-year joint development agreement with an automotive technology supplier to develop a carbon nanotube film heater concept to incorporate it into the automotive glass. The collaboration is focused on improving material compatibility within laminated glass, enabling more cost-efficient integration.

- Report ID: 4500

- Published Date: Apr 06, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.