Automotive Night Vision Systems Market Outlook:

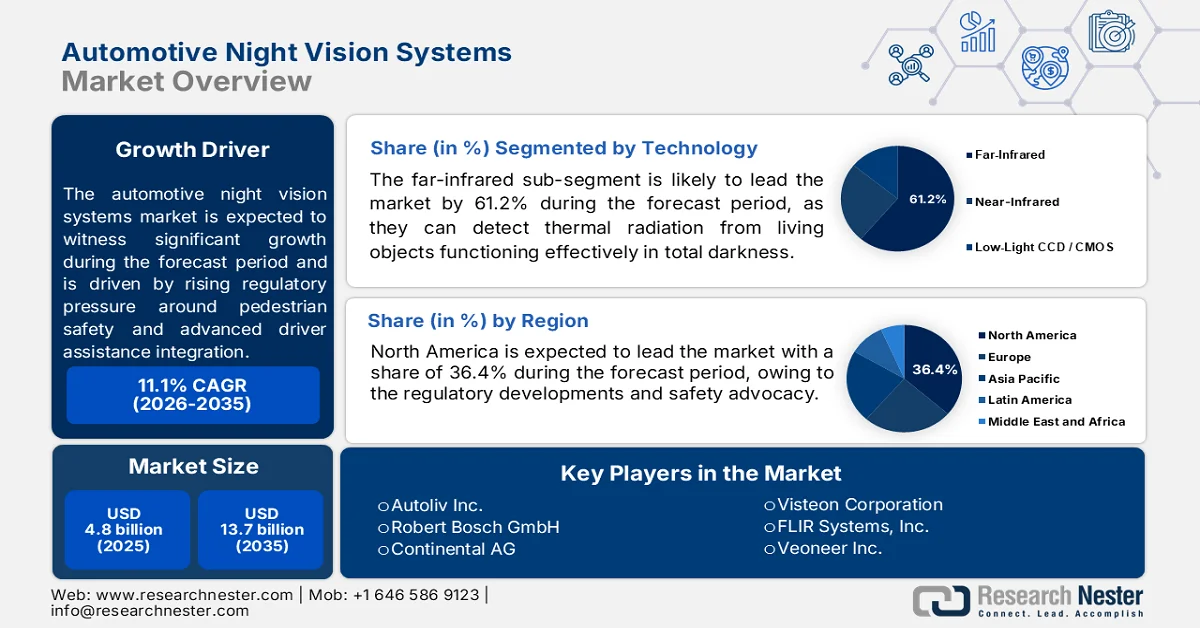

Automotive Night Vision Systems Market size was valued at USD 4.8 billion in 2025 and is expected to reach USD 13.7 billion by the end of 2035, rising at a CAGR of 11.1% during the forecast period, 2026-2035. In 2026, the industry size of automotive night vision systems is assessed at USD 5.3 billion.

The automotive night vision systems market is gaining commercial traction as vehicle manufacturers respond to the rising regulatory pressure around pedestrian safety, nighttime collision reduction, and advanced driver assistance integration. The GHSA July 2025 data reported that pedestrian deaths in the U.S. increased by more than 80%, reaching levels not recorded in four decades. These trends are influencing OEM investment toward infrared sensing thermal imaging integration and sensor fusion platforms capable of improving driver response time in adverse visibility conditions. Moreover, the European Road Safety Observatory 2022 report nearly 40% of all fatal road accidents in Europe. These statistical realities have prompted safety assessment bodies to revise testing protocols.

Besides, the automotive night vision systems market outlook is also being shaped by broader transportation safety and intelligent mobility investment programs across North America, Europe, and the Asia Pacific. According to the World Health Organization's May 2026 report, nearly 1.19 million people die annually in road traffic crashes worldwide. The PIARC May 2025 data pedestrians and cyclists account for more than 25% of fatalities. Public-sector focus on reducing these deaths is accelerating the adoption of sensor-enabled vehicle safety technologies that operate effectively during nighttime and low-contrast conditions. Commercial fleet operators are also emerging as an important demand segment due to rising liability costs associated with nighttime accidents and driver fatigue. Heavy commercial vehicles, logistics fleets, and long-haul transport operators are increasingly evaluating night vision-enabled safety packages to reduce operational risk and insurance exposure. As regulatory agencies continue tightening vehicle safety expectations automotive night vision systems are expected to become more closely integrated with predictive safety and autonomous driving architectures.

Ranking of Death Due to Road Traffic Injury Compared with all Other Causes for Children, 2025

|

Region |

1–4 years |

5–9 years |

10–14 years |

|

North America |

1 |

1 |

1 |

|

Central Europe |

3 |

1 |

1 |

|

Australasia |

2 |

1 |

1 |

|

Western Europe |

2 |

2 |

1 |

|

North Africa and Middle East |

4 |

1 |

1 |

|

Latin America |

4 |

1 |

1 |

Source: PIARC May 2025

Key Automotive Night Vision Systems Market Insights Summary:

Regional Highlights:

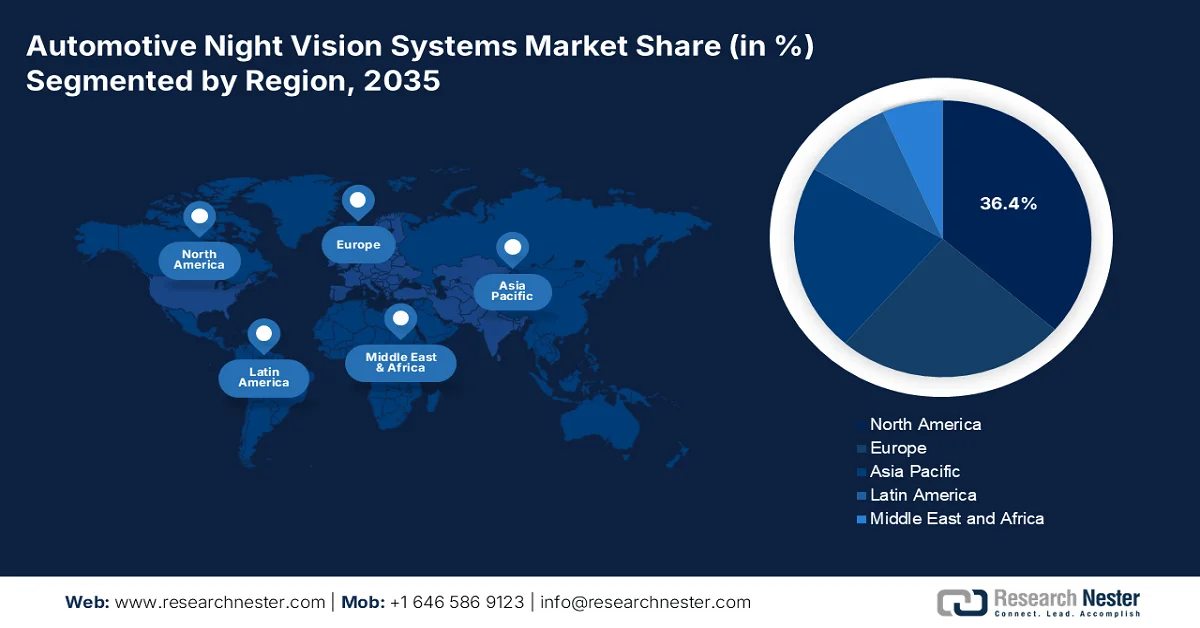

- North America automotive night vision systems market is anticipated to command 36.4% revenue share by 2035, propelled by regulatory developments from the National Highway Traffic Safety Administration and safety advocacy from the Insurance Institute for Highway Safety

- Asia Pacific is poised to witness rapid expansion in the market throughout 2026-2035, fueled by dense urban traffic, diverse driving conditions, and increasing integration of night vision systems by regional OEMs

Segment Insights:

- The far-infrared sub-segment in the automotive night vision systems market is projected to secure 61.2% market share by 2035, driven by rising demand for thermal-based detection systems capable of operating effectively in darkness, fog, and glare conditions

- Passenger cars remain the dominant vehicle type segment in the market during 2026-2035, owing to rising global passenger vehicle sales and declining thermal sensor costs enabling wider integration across mid-range models

Key Growth Trends:

- Rising government road safety spending

- Expansion of smart mobility and intelligent transport infrastructure

Major Challenges:

- Lack of standardization across OEM platforms

- Technical Integration Complexity

Key Players: Autoliv Inc. (U.S.), Robert Bosch GmbH (Germany), Continental AG (Germany), Visteon Corporation (U.S.), FLIR Systems, Inc. (U.S.), Veoneer Inc. (U.S.), Magna International Inc. (Canada), OmniVision Technologies, Inc. (U.S.), Denso Corporation (Japan), Panasonic Corporation (Japan), Samsung Electro-Mechanics (South Korea), LG Innotek (South Korea), ZF Friedrichshafen AG (Germany), Valeo SA (France), Melexis NV (Belgium), Protruly Electronics (China), Adasky, Ltd. (Israel), Pro-Vision (Netherlands), Ajax (Ukraine), Indra (Spain).

Global Automotive Night Vision Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.8 billion

- 2026 Market Size: USD 5.3 billion

- Projected Market Size: USD 13.7 billion by 2035

- Growth Forecasts: 11.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (36.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, South Korea

- Emerging Countries: India, Brazil, Mexico, Thailand, Indonesia

Last updated on : 19 May, 2026

Automotive Night Vision Systems Market - Growth Drivers and Challenges

Growth Drivers

- Rising government road safety spending: Government expenditure on road safety infrastructure is becoming a major demand driver for the automotive night vision systems. In the U.S., the Department of Transportation's April 2026 data indicated that nearly USD 5 billion is under the Safe Streets and Roads for All initiative to reduce roadway fatalities and improve vehicle safety technologies. Low-visibility crashes remain a priority area, particularly pedestrian fatalities occurring at night. In Europe, the European Commission’s Vision Zero framework aims to reduce road deaths to near zero, promoting the OEMs to deploy advanced nighttime sensing technologies. These investments are accelerating procurement opportunities for suppliers focused on ADAS-integrated night vision platforms.

- Expansion of smart mobility and intelligent transport infrastructure: The completion of 177 smart mobility projects during is supporting the long-term growth outlook for the automotive night vision systems market, as per the PIB June 2025 data, by accelerating the deployment of the intelligent transport infrastructure and connected traffic ecosystems. The implementation of Intelligent Transport Management Systems monitored via Integrated Command and Control Centers is improving the traffic flow management, reducing congestion, and strengthening enforcement of traffic violations. These developments increase the operational importance of advanced in-vehicle sensing technologies capable of supporting safer navigation during nighttime and low-visibility conditions. The expansion of digitally connected mobility infrastructure also creates favorable conditions for the adoption of advanced driver assistance technologies linked to nighttime safety and predictive traffic management.

Challenges

- Lack of standardization across OEM platforms: Different automakers employ varying system architectures, imaging algorithms, and display methods, creating fragmentation that increases supply chain complexity and aftermarket maintenance difficulty. New entrants must develop multiple product variants to serve different OEMs, raising R&D costs and time to market. The automotive night vision systems market lacks uniform technical standards for night vision system performance metrics, testing protocols, and integration interfaces. This fragmentation particularly challenges smaller manufacturers who cannot afford to customize solutions for each automotive platform.

- Technical Integration Complexity: Integrating night vision with existing ADAS architectures requires sophisticated sensor fusion capabilities. Traditional late fusion approaches process each sensor independently before combining data, which increases computational burden and limits information extraction. New entrants lacking AI and machine learning expertise struggle to implement efficient early fusion techniques. Top players have pioneered early fusion of thermal and imaging radar sensors, combining raw data streams before object classification. This approach improves nighttime pedestrian detection but requires centralized computing architectures and high-bandwidth connections that many manufacturers do not yet support.

Automotive Night Vision Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.1% |

|

Base Year Market Size (2025) |

USD 4.8 billion |

|

Forecast Year Market Size (2035) |

USD 13.7 billion |

|

Regional Scope |

|

Automotive Night Vision Systems Market Segmentation:

Technology Segment Analysis

Under the technology segment, the far‑infrared is the leading sub‑segment in the automotive night vision systems market, projected to capture 61.2% of the market share by 2035. FIR passively detects thermal radiation from living objects functioning effectively in total darkness, fog, and glare conditions where visible cameras and Near‑Infrared fail. Falling microbolometer costs have accelerated FIR adoption beyond luxury vehicles. According to a 2024 report by the Federal Highway Administration, March 2026 data show that nearly 76% of pedestrian fatalities occur at night, underscoring the urgent need for thermal-based detection. This statistical reality, combined with Euro NCAP’s upcoming low-light testing protocols, positions FIR as the dominant technology for reducing nighttime collisions.

Vehicle Type Segment Analysis

Under the vehicle type segment, the passenger cars sub-segment is dominating in the automotive night vision systems market. Premium automakers have long offered night vision as an option, while declining sensor costs are now enabling integration into mid‑range passenger vehicles from Toyota, Hyundai, Ford, and Tata Motors. Regulatory pressure and growing vehicle volumes drive this expansion. According to the DD News May 2026 report, domestic passenger vehicle dispatches to dealers in India rose 25.4% YoY to 4,37,312 units in a single month. As passenger car sales surge globally, particularly in emerging economies, the addressable market for factory‑fitted night vision systems grows proportionally. This volume growth, combined with falling thermal sensor prices, solidifies passenger cars as the dominant vehicle type segment for night vision adoption.

Sales Channel Segment Analysis

The OEM factory fit channel is the dominant sales segment in the automotive night vision systems market. Automakers prefer integrating night vision directly into vehicles during assembly to ensure seamless calibration, warranty control, and optimal placement of infrared cameras and displays. Factory integration also enables the direct fusion with an Advanced Driver Assistance System, allowing night vision data to trigger the automatic emergency braking or dashboard alerts without driver intervention. This deep integration is difficult to achieve with the aftermarket retrofits, which often face compatibility and installation challenges. Further, OEMs benefit from the volume pricing when sourcing components from Tier-1 suppliers, reducing per-unit costs. As safety regulations increasingly mandate pedestrian detection in low-light conditions, automakers are making night vision a factory-installed option or standard feature, cementing OEMs as the primary sales channel for the foreseeable future.

Our in-depth analysis of the automotive night vision systems market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Component |

|

|

Vehicle Type |

|

|

Sales Channel |

|

|

Application |

|

|

Sensor Fusion Integration |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Night Vision Systems Market - Regional Analysis

North America Market Insights

The North America automotive night vision systems market is dominating and is expected to hold the regional revenue share of 36.4% by 2035. The market is primarily driven by regulatory developments from the National Highway Traffic Safety Administration and safety advocacy from the Insurance Institute for Highway Safety. Proposed rulemaking for nighttime pedestrian automatic emergency braking is pushing original equipment manufacturers to evaluate and integrate thermal and near-infrared detection systems into passenger vehicles and light trucks. The region's diverse driving conditions, including poor rural highways and suburban streets, further support the adoption. Suppliers are actively developing fusion architectures that combine the infrared cameras with existing radar and camera-based ADAS platforms. Cost reduction remains a central focus as the automakers seek to transition the night vision from an exclusive luxury option to a broadly available safety feature across mainstream vehicle segments.

The increasing demand for vehicle perception technologies capable of operating effectively in low light and adverse weather conditions is shaping the automotive night vision systems market in the U.S. RGB cameras used in conventional ADAS platforms face operational limitations during nighttime driving, direct sunlight exposure, fog, and glare from oncoming vehicles, increasing industry focus on thermal imaging and long-wave infrared sensing systems. Demand is mainly strong in rural transportation networks where roadway fatality rates remain significantly higher than in urban areas. According to the U.S. Department of Transportation, April 2025 data, more than 83,000 people died on rural roadways by 2021, accounting for 43% of roadway deaths despite only 20% of the population residing in rural regions. In 2022, 17,283 rural traffic fatalities were recorded, reinforcing the OEM investment in the advanced nighttime detection and driver assistance technologies.

The rising roadway fatalities and increasing government focus on collision prevention strengthen the demand for the automotive night vision systems market in Canada. According to the Government of Canada, May 2024 data, nearly 1,931 motor vehicle fatalities represented a 6% increase from 2021 serious injuries increased 8.1% to 8,851 cases, and total injuries rose 9.5% to 118,853. These trends are pushing the adoption of infrared-based safety systems capable of improving pedestrian and animal detection during nighttime driving. Government of Canada August 2021 data also highlights that night vision systems can detect pedestrians or animals at distances between 150 and 300 meters using infrared sensors and real-time dashboard displays. Growing awareness of rural road safety, wildlife collision risks, and low visibility driving conditions is supporting the integration of thermal imaging technologies across the premium passenger vehicles and advanced driver-assistance system platforms.

Collisions and Casualties, 2011 to 2022

|

Year |

Fatal |

Personal Injury |

Fatalities |

Serious Injuries |

Injuries (Total) |

|

2011 |

1,849 |

122,350 |

2,023 |

10,940 |

167,741 |

|

2012 |

1,848 |

122,834 |

2,075 |

11,104 |

166,727 |

|

2013 |

1,772 |

120,371 |

1,951 |

10,662 |

164,525 |

|

2014 |

1,675 |

114,617 |

1,841 |

10,445 |

156,557 |

|

2015 |

1,693 |

117,857 |

1,887 |

10,835 |

160,806 |

|

2016 |

1,738 |

116,583 |

1,900 |

10,573 |

158,854 |

|

2017 |

1,698 |

112,714 |

1,861 |

10,104 |

152,773 |

|

2018 |

1,754 |

109,580 |

1,930 |

9,463 |

149,065 |

|

2019 |

1,620 |

103,020 |

1,761 |

8,917 |

139,084 |

|

2020 |

1,602 |

78,388 |

1,711 |

7,868 |

104,286 |

|

2021 |

1,628 |

81,962 |

1,821 |

8,185 |

108,552 |

|

2022 |

1,746 |

89,787 |

1,931 |

8,851 |

118,853 |

Source: Government of Canada, May 2024

APAC Market Insights

The Asia Pacific is projected to grow rapidly in the automotive night vision systems market during the assessed period, 2026 to 2035. The region is shaped by the dense urban traffic, diverse driving conditions, and varying regulatory frameworks across the major automotive hubs. Japan and South Korea lead in technology adoption, driven by domestic OEMs integrating night vision into premium and mid-range passenger vehicles. Moreover, China's rapidly expanding vehicle fleet and focus on advanced driver assistance systems create a substantial demand for commercial vehicle night vision solutions. India presents a unique growth with its unlit highways and high incidence of nighttime animal and pedestrian encounters. Regional suppliers are increasingly partnering with the thermal sensor manufacturers to develop cost-effective solutions suited for high-volume production.

The rising investments in infrared imaging technologies, increasing road fatalities, and expanding domestic manufacturing capabilities are driving the automotive night vision systems market in India. The PIB October 2025 data indicated that the Government of India inaugurated an advanced night vision facility established by Bharat Electronics Limited in Andhra Pradesh, with an investment of nearly Rs 360 crore to manufacture advanced night vision devices, infrared seekers, and drone detection systems. The expansion of indigenous infrared and electro-optical manufacturing is expected to strengthen the domestic supply chain for automotive thermal imaging applications. Demand is also supported by India’s high accident burden, with ORF September 2024 indicating 168,491 road fatalities and 461,312 accidents in 2022. Increasing focus on nighttime visibility, pedestrian safety, and smart mobility infrastructure is encouraging OEMs to adopt advanced infrared sensing and driver assistance technologies.

The Japan automotive night vision systems market is expanding rapidly and is projected to grow from USD 189.52 million in 2025 to USD 909.84 million by 2035 at a CAGR of 9.8% during the assessed period. In 2026, the market is expected to reach USD 223.20 million. The nation is driven by government incentives supporting advanced vehicle safety technologies and a rising focus on nighttime collision prevention. Japan introduced environmental performance-based tax reductions and tonnage tax incentives for vehicles equipped with eligible Advanced Safety Vehicle (ASV) systems, including automatic emergency braking with pedestrian collision avoidance functions. These incentives are pushing OEMs to integrate infrared sensing and nighttime pedestrian detection technologies into passenger and commercial vehicles. Demand is further supported by road safety concerns, as CAO June 2024 data recorded 2,678 traffic fatalities in 2024, with nighttime accidents thus driving the automotive night vision systems market expansion and growth.

Europe Market Insights

The automotive night vision systems market in Europe grows steadily and is driven by stringent safety regulations and advanced driver assistance system mandates enforced across the region. Euro NCAP's evolving testing protocols reward vehicles capable of detecting pedestrians, cyclists, and animals during low-light or dark conditions, pushing automakers to integrate thermal and near-infrared sensors. Germany, France, and the UK lead adoption with domestic OEMs incorporating night vision into mid-range and premium passenger cars as either standard or optional equipment. The growing emphasis on Vision Zero initiatives across Nordic countries further accelerates demand, particularly for animal detection systems on rural and forested roads.

The strong adoption of advanced driver assistance technologies, increasing road safety initiatives, and growth in premium vehicle manufacturing are driving the automotive night vision systems market in Germany. According to the ZIV August 2025, nearly 2,839 people were killed in road traffic accidents in 2023, reinforcing demand for enhanced nighttime detection and collision prevention systems. GTAI 2026 data indicated that more than USD 575 million is allocated for connected mobility and digital transport infrastructure modernization projects supporting intelligent vehicle technologies. Additionally, the European Commission's May 2025 data reported that 45,535 new BEVs were registered, increasing the deployment potential for software-defined vehicle architectures compatible with infrared sensing and thermal imaging systems. These developments are strengthening the OEM investment in integrated night vision and predictive safety technologies across passenger and luxury vehicle segments.

The increasing investments in road safety, connected mobility infrastructure, and electric vehicle adoption are shaping the automotive night vision systems market in the UK. According to the UK Government, September 2024 data, nearly 1,624 road fatalities were recorded in Great Britain, sustaining demand for advanced nighttime collision prevention technologies. The OECD June 2025 data indicated that the UK government committed more than USD 199 million through the Connected and Automated Mobility programme to support the deployment of self-driving and intelligent vehicle technologies across public roads. Additionally, the Global Ardour Recycling Limited February 2026 data reported that the battery electric vehicle registrations accounted for 16.5% of all new car registrations, expanding the automotive night vision systems market for sensor-integrated vehicle platforms. These developments are promoting the automakers to deploy infrared sensing, thermal imaging, and advanced night detection systems in next-generation vehicles.

UK Road Safety Statistics, 2023

|

Road Safety Indicator |

Statistics |

|

Total Road Fatalities |

1,624 fatalities (5% decline vs 2022) |

|

Killed or Seriously Injured (KSI) Casualties |

29,711 cases |

|

Total Road Casualties |

132,977 casualties (2% decline vs 2022) |

|

Vehicle Miles Travelled |

334 billion vehicle miles travelled |

|

Fatalities per Billion Vehicle Miles |

5 fatalities per billion miles (7% decline vs 2022) |

|

Motorcyclist Fatality Change |

10% decline compared to 2022 |

|

Male Casualty Share |

75% of fatalities and 61% of casualties were male |

Source: Government of UK September 2024

Key Automotive Night Vision Systems Market Players:

- Autoliv Inc. (U.S.)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Visteon Corporation (U.S.)

- FLIR Systems, Inc. (U.S.)

- Veoneer Inc. (U.S.)

- Magna International Inc. (Canada)

- OmniVision Technologies, Inc. (U.S.)

- Denso Corporation (Japan)

- Panasonic Corporation (Japan)

- Samsung Electro-Mechanics (South Korea)

- LG Innotek (South Korea)

- ZF Friedrichshafen AG (Germany)

- Valeo SA (France)

- Melexis NV (Belgium)

- Protruly Electronics (China)

- Adasky, Ltd. (Israel)

- Pro-Vision (Netherlands)

- Ajax (Ukraine)

- Indra (Spain)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Autoliv Inc. is a key player in the automotive night vision systems market, leveraging its expertise in automotive safety electronics. The company integrates far infrared (FIR) cameras with active safety systems to detect pedestrians, cyclists, and animals in darkness or poor weather. Autoliv’s strategic initiatives include developing fusion-based night vision solutions that combine thermal imaging with radar and lidar data, enhancing predictive crash avoidance.

- Robert Bosch GmbH remains a dominant player in the automotive night vision systems market, offering near-infrared active illumination and thermal imaging solutions. Bosch’s strategic initiatives include embedding night vision into its broader ADAS portfolio, enabling head-up display projections of the detected hazards. In 2024, the company has made revenue sales of USD 98.48 billion.

- Continental AG is a major innovator in the automotive night vision systems market, specializing in multi-spectral sensor fusion. The company combines infrared cameras with long-wave infrared (LWIR) technology and its proprietary ContiGuard safety architecture. Strategic initiatives include developing night vision systems that can detect the heat signatures and interface with adaptive headlights.

- Visteon Corporation is a top player in the automotive night vision systems market by focusing on display and cockpit integration. Visteon provides digital instrument clusters and the augmented reality head-up displays that render night vision camera data seamlessly for drivers. Strategic initiatives include collaboration with thermal sensor suppliers to offer low-latency video processing and overlay of highlighted pedestrians. In 2024, the company has reported a net sales of USD 3,866 million.

- FLIR Systems, Inc. is a technology leader in the automotive night vision systems market, known for its high-performance thermal imaging cores. FLIR’s PathFindIR and Thermal by FLIR automotive modules detect heat signatures from living objects beyond headlight range, even in total darkness, smoke, or fog. Strategic initiatives include reducing module size and cost for production vehicles, integrating with ADAS ECUs and developing pedestrian/animal detection algorithms.

Here is a list of key players operating in the global automotive night vision systems market:

The automotive night vision systems market is consolidated, with the key players from Europe, Japan, and North America dominating due to the high R&D investments in sensor fusion and AI-driven object detection. Strategic initiatives include partnerships with LiDAR suppliers, integration with autonomous driving suites, and cost reduction through solid-state technologies. Europe firms lead in the high-end infrared cameras Japan and America companies focus on the augmented reality overlays. Emerging players from South Korea and India are targeting the aftermarket and commercial vehicle segments, leveraging thermal imaging and deep learning to enhance pedestrian and animal detection in low visibility conditions. Companies are actively focusing on mergers and acquisitions for market expansion. For example, in May 2026, Pro-Vision announced the acquisition of Convoy Technologies to expand fleet safety and video solutions.

Corporate Landscape of the Automotive Night Vision Systems Market:

Recent Developments

- In August 2025, Ajax introduced three cameras featuring hybrid light illumination, such as BulletCam HL, TurretCam HL, and DomeCam Mini HL. These cameras combine white light illumination and IR to deliver color footage even in low-light conditions.

- In May 2024, Indra introduced a 360-vision system, which is based on AI that endows armored vehicles with increased effectiveness and situational awareness when it comes to fulfilling their mission.

- In January 2024, Valeo and Teledyne FLIR announced a strategic collaboration to bring thermal imaging technology to the automotive industry to improve the safety of road users. The team delivers their new thermal imaging cameras as part of a new gen of advanced driver-assist systems (ADAS) driver-aide technology to improve vehicle and road safety

- Report ID: 5942

- Published Date: May 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.