Automated Fiber Placement Market Outlook:

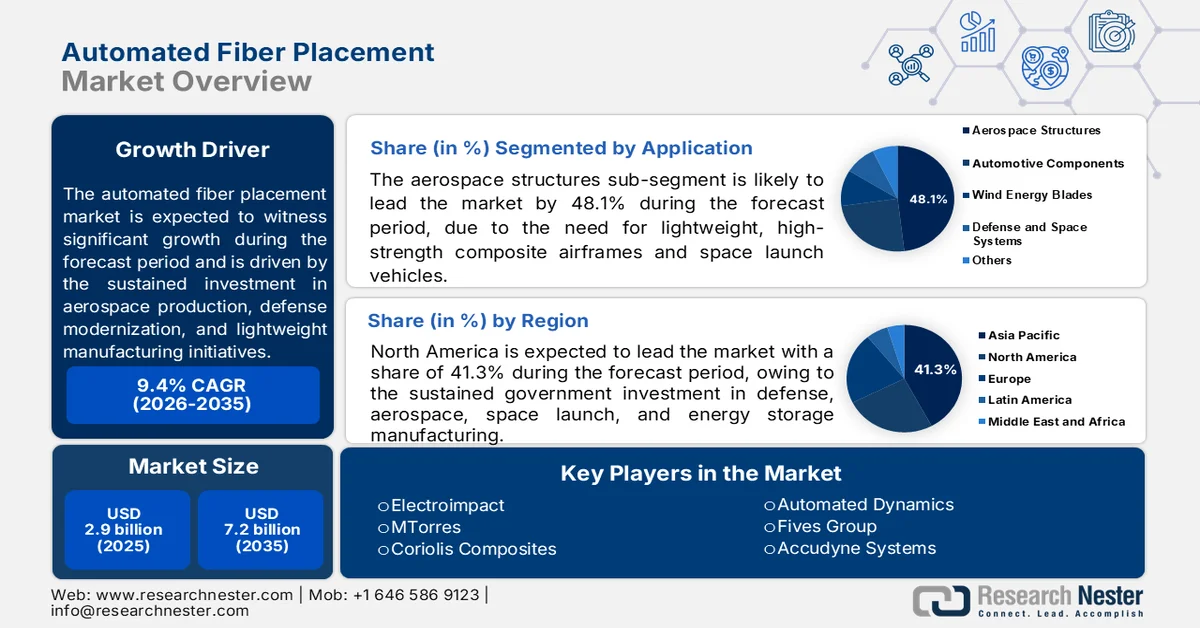

Automated Fiber Placement Market size was valued at USD 2.9 billion in 2025 and is projected to account for USD 7.2 billion by 2035, rising at a CAGR of 9.4% during the forecast period 2026 to 2035. In 2026, the industry size of automated fiber placement is evaluated at USD 3.2 billion.

The automated fiber placement market is shaped by sustained investment in aerospace production, defense modernization, and lightweight manufacturing initiatives across North America, Europe, and the Asia Pacific. The U.S. Bureau of Transportation Statistics March 2023 data reported that global commercial aircraft fleet activity continues to expand alongside long-term air traffic growth, with U.S. carriers alone transporting more than 853 million passengers annually before recent fleet renewal programs accelerated demand for fuel-efficient airframes incorporating high-volume composite structures. The National Aeronautics and Space Administration has continued to fund advanced composite manufacturing programs aimed at reducing aircraft weight and improving structural efficiency, including large-scale thermoplastic composite research for next-generation aviation systems.

Besides, the government-backed renewable energy deployment is also contributing to broader industrial demand for automated composite manufacturing systems. The U.S. Department of Energy's August 2024 data reported that wind turbine blades continue to increase in size, with average utility-scale turbine rotor diameters in the U.S. exceeding 133.8 meters in recent installations, creating additional requirements for high-throughput composite production capacity. The International Energy Agency projected that global renewable electricity capacity additions will continue rising through the decade, led by wind and solar infrastructure expansion. Composite intensive manufacturing is additionally receiving policy support through initiatives such as the U.S. Manufacturing USA program and the European Union’s Horizon Europe framework, both of which fund digital manufacturing and advanced materials research. These data are strengthening long-term capital investment in automated composite fabrication infrastructure across aerospace, energy, transportation, and defense supply chains.

Key Automated Fiber Placement Market Insights Summary:

Regional Highlights:

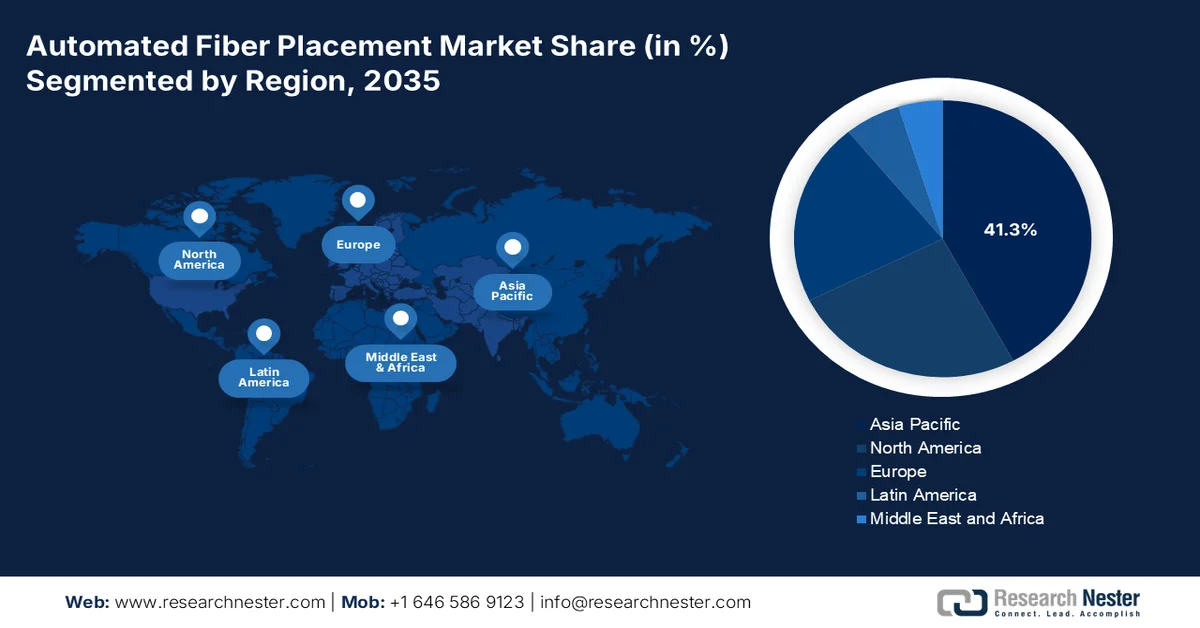

- North America in the automated fiber placement market is anticipated to secure a 41.3% revenue share by 2035, reinforced by sustained government investments across defense, aerospace, space launch, and energy storage manufacturing initiatives

- Asia Pacific is expected to witness accelerated expansion in the 2026–2035 period, fueled by government-backed programs to strengthen indigenous aerospace and defense manufacturing capabilities

Segment Insights:

- The aerospace structures segment in the automated fiber placement market is projected to account for a 48.1% share by 2035, supported by the rising requirement for lightweight and high-strength composite airframes and space launch vehicles

- Robotic automated fiber placement is anticipated to gain strong momentum during 2026–2035, stimulated by increasing investments in robotics automation and advanced manufacturing technologies

Key Growth Trends:

- Defense aircraft modernization programs

- Expanding civil infrastructure modernization

Major Challenges:

- Technological complexity and required expertise

- Global supply chain vulnerabilities and material costs

Key Players: Electroimpact (U.S.), MTorres (Spain), Coriolis Composites (France), Automated Dynamics (U.S.), Fives Group (France), Accudyne Systems (U.S.), Mikrosam (North Macedonia), Cevotec GmbH (Germany), Addcomposites (Finland), Ingersoll Machine Tools (U.S.), Broetje-Automation (Germany), Composite Automation (U.S.), Langzauner (Austria), KUKA Systems (Germany), Mitsubishi Heavy Industries (Japan), Kawasaki Heavy Industries (Japan), SAMTECH (South Korea), Hanyang Advanced Manufacturing Systems (South Korea), Rocket Lab, Inc. (U.S.), Firefly Aerospace (U.S.).

Global Automated Fiber Placement Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.9 billion

- 2026 Market Size: USD 3.2 billion

- Projected Market Size: USD 7.2 billion by 2035

- Growth Forecasts: 9.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: South Korea, Vietnam, Brazil, Mexico, Indonesia

Last updated on : 27 May, 2026

Automated Fiber Placement Market - Growth Drivers and Challenges

Growth Drivers

- Defense aircraft modernization programs: The rising defense aircraft procurement is strengthening the demand for automated composite production systems in the military aerospace supply chains. The Defense Budget Overview 2024 data reported that the government allocated USD 61.1 billion for air power programs, including the investments in Next Generation Air Dominance and advanced rotorcraft platforms. These programs rely on large composite-intensive structures requiring high-precision automated manufacturing to maintain production consistency and reduce assembly timelines. NATO members are increasing defense expenditure commitments, creating long-term procurement pipelines for composite aerostructures. Further, the aerospace production demand is expected to rise further as military fleet replacement programs expand across North America and Europe, increasing the requirement for scalable automated layup operations.

- Expanding civil infrastructure modernization: Public infrastructure modernization programs are increasing the use of advanced composites in bridges, seismic retrofits, and corrosion-resistant structures. According to the GFOA 2026 data, the U.S. Infrastructure Investment and Jobs Act allocates more than USD 1.2 trillion toward transportation and infrastructure modernization, including bridge rehabilitation programs, where lightweight composite materials are increasingly evaluated for durability improvement. The Asian Development Bank and World Bank are also supporting climate-resilient infrastructure initiatives across developing economies. Automated composite manufacturing technologies are gaining attention because they improve production consistency for structural reinforcement components and prefabricated systems. Moreover, the rising public infrastructure investment in coastal protection, rail modernization, and resilient transportation networks is expected to support broader industrial demand for automated composite production technologies in civil engineering supply chains.

Challenges

- Technological complexity and required expertise: Operating AFP machinery requires a highly specialized skillset that blends robotics, material science, and software programming. New entrants struggle to recruit and train personnel capable of programming complex robotic paths, managing process parameters for different fiber types, and performing maintenance on sophisticated placement heads. This shortage of skilled labor can lead to production inefficiencies, high scrap rates, and extended ramp-up periods. The integration of Industry 4.0 principles, such as real-time sensor feedback and AI-driven process control, further intensifies the need for cross-disciplinary expertise.

- Global supply chain vulnerabilities and material costs: Entering the automated fiber placement market requires securing a reliable, high-quality supply of raw materials, primarily carbon fiber, glass fiber, and aramid fiber tows. These advanced materials have their own concentrated supply chains, often dependent on a few global producers. New entrants are vulnerable to price volatility, geopolitical trade restrictions, and logistics disruptions. A lack of established relationships with tier-1 material suppliers can lead to inconsistent quality, higher costs, and production delays that erode already thin profit margins.

Automated Fiber Placement Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.4% |

|

Base Year Market Size (2025) |

USD 2.9 billion |

|

Forecast Year Market Size (2035) |

USD 7.2 billion |

|

Regional Scope |

|

Automated Fiber Placement Market Segmentation:

Application Segment Analysis

The aerospace structures sub-segment is the largest application segment in the automated fiber placement market and is poised to hold the share value of 48.1% by the end of 2035. The segment is driven by the need for lightweight, high-strength composite airframes and space launch vehicles. AFP enables precise placement of carbon fiber tows over complex contoured geometries such as fuselage barrels, wing skins, and rocket motor cases, eliminating thousands of mechanical fasteners. According to the NCCUK January 2026 data, composite materials now account for over 50% of the structural weight in next-generation commercial aircraft, with AFP being the primary manufacturing method for these components. As major programs like the Boeing 787, Airbus A350, and new narrow-body replacements ramp up production, the demand for high speed AFP cells continues to grow.

Technology Segment Analysis

Robotic automated fiber placement has revolutionized composite manufacturing by offering flexible, reconfigurable, and cost-effective solutions compared to traditional gantry systems. According to the Public Spend Forum 2026 data, the U.S. federal government's substantial investment in advanced manufacturing has directly surged the robotic automated fiber placement technology. With over USD 6 billion spent on robotics automation and advanced manufacturing-related R&D, signifying 222% growth, agencies like NASA and the Department of Energy have prioritized composite manufacturing automation. This funding has enabled the development of next-generation robotic AFP systems featuring real-time adaptive process control, enhanced end effector precision, and collaborative dual-arm architectures.

Process Segment Analysis

The thermoplastic placement is leading the process segment in the automated fiber placement market, eliminating the need for separate autoclave curing. During this process, a high-energy heat source, typically a laser or infrared emitter, melts the incoming thermoplastic composite tow precisely at the nip point while a compaction roller applies immediate pressure to fuse the material to the underlying substrate. This simultaneous melting and consolidation achieve full part density directly on the machine, producing ready-to-use components immediately after layup. By removing the autoclave step, manufacturers drastically reduce cycle times, energy consumption, and capital equipment costs. Furthermore, thermoplastic parts created via in-situ consolidation can be welded or reformed, enabling novel joining methods and repair strategies for complex aerospace and defense structures.

Our in-depth analysis of the automated fiber placement market includes the following segments:

|

Segment |

Subsegments |

|

Fiber Material |

|

|

Application |

|

|

Technology |

|

|

Process |

|

|

End user |

|

|

Curing Method |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automated Fiber Placement Market - Regional Analysis

North America Market Insights

North America is dominating the global automated fiber placement market and is expected to capture a regional revenue share of 41.3% by the end of 2035. The market is driven primarily by sustained government investment in defense, aerospace, space launch, and energy storage manufacturing. The U.S dominates regional demand with federal agencies funding AFP development for next-generation fighter aircraft, hypersonic systems, and reusable launch vehicle structures. Canada contributes via specialized programs focused on composite repair technologies and landing gear components for regional aircraft programs. Across the region, government procurement mandates and R&D grants act as the primary demand anchors rather than purely commercial forces. Suppliers entering this market must align their product roadmaps with multi-year defense space and energy program timelines to secure consistent revenue streams.

The rising defense export partnerships and military aviation modernization programs supported by allied nations are shaping the market in the U.S. According to the ITA November 2024 data, Croatia increased its 2024 defense budget to USD 1.39 billion and continues expanding procurement of composite-intensive aircraft platforms, including Dassault Rafale F-3R fighter jets and UH-60M Black Hawk helicopters supported by the U.S. government. These aircraft programs require advanced composite aerostructures manufactured through automated production technologies to improve precision and structural performance. Further, the U.S. Department of State reported that total U.S. defense exports and arms transfers reached over USD 238 billion in 2024, reflecting the sustained international demand for aerospace systems. Growing allied procurement activity is strengthening long-term demand for automated composite manufacturing capacity across U.S. aerospace supply chains.

The market in Canada is gaining momentum as aerospace export agreements and composite manufacturing partnerships expand across international markets. The proposed Canada-Indonesia Comprehensive Economic Partnership Agreement is expected to strengthen aerospace trade by locking in duty-free access for aircraft simulators, helicopters, and aerospace components, supporting higher production activity among Canadian manufacturers. According to the Government of Canada, September 2024 data, Canada’s aerospace sector contributed nearly USD 29 billion to national GDP, with more than 75% of industry revenue generated through exports. Provinces, including Quebec and Manitoba, are expanding capabilities in aircraft assembly, composite manufacturing, and flight simulation systems. Growing export-oriented aerospace production is increasing demand for automated composite fabrication technologies to improve manufacturing efficiency, precision, and large-scale aerostructure output across Canada's supply chains.

APAC Market Insights

The Asia Pacific is projected to emerge during the assessed period, 2026 to 2035, in the automated fiber placement market. The region is driven by the government-backed initiatives to develop indigenous aerospace and defense manufacturing capabilities. Japan leads in precision AFP applications for next-generation aircraft structures while South Korea focuses on domestic fighter program components. China continues expanding its composite production capacity for commercial and military airframes. India and Malaysia are emerging as the lower-cost manufacturing hubs for global aerostructure suppliers leveraging AFP to meet export quality standards. Australia contributes via research partnerships with defense primes. Across the region, government production-linked incentives and technology localization mandates shape demand with a preference for mid-sized robotic AFP systems over large gantry configurations.

Rising aerospace manufacturing investments, defense modernization, and domestic aircraft production initiatives are driving the market in India. According to the Sansad March 2025 data, India handled more than 376 million passengers across the domestic and international traffic, increasing demand for the next generation aircraft and aviation infrastructure. The Government of India allocated USD 81 billion to the Ministry of Defence Union Budget as per the PIB February 2025 report, supporting the military aviation procurement and indigenous aerospace manufacturing programs. In addition, the Indian Space Research Organization completed multiple launch missions, strengthening demand for lightweight composite structures in launch vehicles and satellites. These developments are accelerating investment in automated composite manufacturing technologies across aerospace and defense supply chains.

The Japan market is projected to grow from USD 18.90 million in 2025 to USD 38.2 million by the end of 2035 at a CAGR of 7.5%. In 2026, the market is projected to reach USD 20.01 million. The market is driven by the defense modernization and advanced manufacturing investments, which increase nationwide demand for high-performance composite structures. As per the Japan Wire by Kyodo News, August 2025 data, the Ministry of Defense plans to allocate nearly 2% of GDP toward defense spending by 2025 to strengthen military capabilities. Rising procurement of fighter aircraft, aerospace systems, and advanced mobility platforms is increasing the use of lightweight composite materials across domestic manufacturing operations. Automated fiber placement technologies are gaining adoption because they improve precision and production efficiency for the aerospace-grade composite components used in defense and aviation applications.

Europe Market Insights

Europe maintains a mature automated fiber placement market anchored by commercial aerospace programs and a strong supplier base of AFP machine builders. Spain, France, Germany, and Italy host the region’s primary manufacturing activity, with local builders supplying both European and export customers. The European Union’s clean aviation initiatives fund AFP development for next-generation narrow-body aircraft fuselages and wings, emphasizing reduced energy consumption and lower assembly costs. Thermoplastic AFP with in situ consolidation receives focused attention as a means to eliminate autoclave processing. The UK contributes through defense and space applications, including missile airframes and satellite structures.

Increasing aerospace production, defense modernization, and industrial decarbonization investments are shaping the market in Germany. According to the Hydrogen Europe August 2023 data, the federal government allocated nearly EUR 212 billion for the Climate and Transformation Fund to support industrial modernization and advanced manufacturing technologies. The ITA 2021 data reported that the country’s aerospace sector generated over EUR 41 billion in industry turnover, strengthening demand for precision composite manufacturing systems. In addition, Germany’s defense budget is supporting military aircraft procurement and aerospace innovation programs. These investments are accelerating the adoption of automated composite production technologies across aerospace, energy, and transportation manufacturing supply chains.

The rising aerospace manufacturing output and defense aviation investments are driving the market in the UK. According to the Government of the UK, June 2025 data, the aerospace sector supported more than 100,000 direct jobs and generated over GBP 34 billion in turnover, reinforcing demand for advanced composite manufacturing technologies. The Government of the UK's April 2024 report announced defense spending plans exceeding GBP 87 billion, including investments in combat air systems, military aircraft upgrades, and submarine programs that require lightweight composite structures. Increased focus on sustainable aviation and domestic aerospace supply chain resilience is encouraging manufacturers to adopt automated composite fabrication systems to improve production efficiency, precision, and scalability across commercial aviation and defense-related manufacturing operations.

Key Automated Fiber Placement Market Players:

- Electroimpact (U.S.)

- MTorres (Spain)

- Coriolis Composites (France)

- Automated Dynamics (U.S.)

- Fives Group (France)

- Accudyne Systems (U.S.)

- Mikrosam (North Macedonia)

- Cevotec GmbH (Germany)

- Addcomposites (Finland)

- Ingersoll Machine Tools (U.S.)

- Broetje-Automation (Germany)

- Composite Automation (U.S.)

- Langzauner (Austria)

- KUKA Systems (Germany)

- Mitsubishi Heavy Industries (Japan)

- Kawasaki Heavy Industries (Japan)

- SAMTECH (South Korea)

- Hanyang Advanced Manufacturing Systems (South Korea)

- Rocket Lab, Inc. (U.S.)

- Firefly Aerospace (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Electimpact is a dominant player in the market, specializing in the ultra-high-speed AFP systems for aerospace primary structures. The company has significantly advanced the market by developing large-scale multi-tow placement machines capable of processing both thermoset and thermoplastic composites at rates exceeding 200 kg per hour.

- MTorres is a leading innovator in the market, renowned for its high-precision multi-gantry AFP systems. The company has advanced the market by integrating in situ consolidation capabilities for thermoplastic composites, eliminating the need for autoclave post-processing.

- Coriolis Composites is a disruptive force in the market, pioneering compact 6-axis robotic AFP solutions. The company has advanced the market by adopting open architecture robotic arms for complex contoured geometries such as engine nacelles, fuselage sections, and helicopter rotor blades.

- Automated Dynamics is a specialized leader in the market, focusing on high-temperature thermoplastic composite winding and AFP processes. The company has significantly advanced the market by developing radiation-resistant and cryogenic-capable structures for space and defense applications.

- Fives Group is a diversified industrial engineering player in the market, offering the Cincinnati brand of large-scale AFP systems. The company has significantly advanced the market by integrating robotic fiber placement with automated tape laying and laser-assisted heating for thermoplastics.

Here is a list of key players operating in the global automated fiber placement market:

The global automated fiber placement market is highly consolidated, dominated by a few specialized aerospace and industrial automation leaders from North America and Europe, with emerging players in Asia. Key strategic initiatives include developing a hybrid AFP system integrating in situ consolidation for out-of-autoclave manufacturing and expanding into the non-aerospace sectors, such as the automotive and hydrogen storage. Major players like Electroimpact and MTorres focus on the ultra-high speed placement for the large composite structures, while companies such as Coriolis Composites pioneer robotic AFP for the complex geometries. Players in Asia are leveraging government-backed R&D to reduce import reliance.

Corporate Landscape of the Market:

Recent Developments

- In June 2025, Mikrosam has commissioned a Robotic Automated Fiber Placement (AFP) Work Cell at Qarbon Aerospace, Inc. (Qarbon). This system is designed to enhance the Qarbon Aerospace’s R&T capabilities, enabling the production of high-performance thermoplastic composite parts with exceptional precision and efficiency.

- In August 2024, Rocket Lab, Inc. announced that it has installed the largest automated fiber placement machine into the Company’s Neutron rocket production line in Middle River, MD. The AFP machine enables the Rocket Lab to automate the production of the largest carbon composite rocket structures in history.

- In February 2024, Firefly Aerospace increases the facilities in Briggs, Texas, to support the medium launch vehicle. Firefly’s expanded manufacturing space from 92,000 to 207,000 square feet which includes two new large-scale buildings for the rocket production, assembly, and integration.

- Report ID: 8585

- Published Date: May 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.