Commercial Pumps Market Outlook:

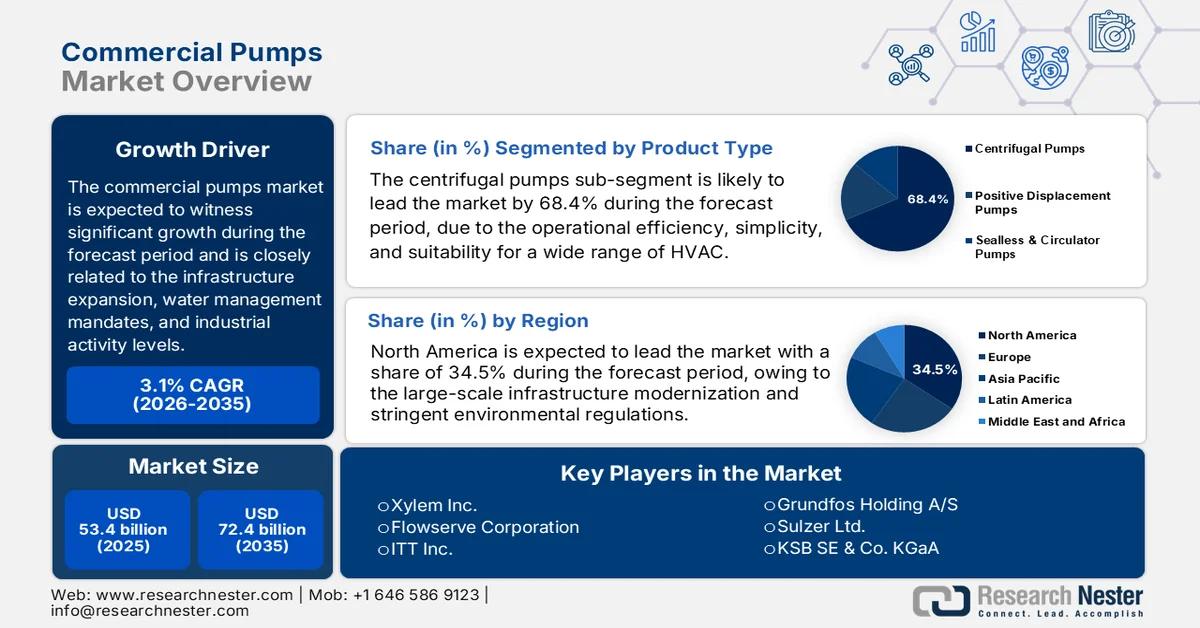

Commercial Pumps Market size was valued at USD 53.4 billion in 2025 and is projected to reach USD 72.4 billion by the end of 2035, rising at a CAGR of 3.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of commercial pumps is assessed at USD 55.1 billion.

The demand for the commercial pumps market is closely related to the infrastructure expansion, water management mandates, and industrial activity levels. The public sector investment remains a primary driver. According to the Infrastructure USA June 2024 data, the U.S. alone requires over USD 744 billion in water infrastructure investment in the next 20 years, covering drinking water, wastewater, and stormwater systems, all of which depend heavily on large-scale pumping equipment for distribution and treatment processes. Similarly, the European Environment Agency's October 2024 data depicts that over 20% of Europe’s water distribution systems experience leakage losses necessitating pump upgrades and replacements to improve system efficiency and pressure management. These government-led programs create consistent long-term demand from municipalities, utilities, and EPC contractors.

Moreover, the industrial and energy sector requirements further reinforce procurement volumes for commercial pumps, mainly in process industries, thermal power, and building services. As per the Modern Building Services data in May 2023, the pumping system accounts for 20% of the world's electricity demand, indicating a substantial installed base requiring both new installations and retrofits for efficiency compliance. On the other hand, the global electricity demand is expected to grow, increasing the need for pumps in cooling systems, boiler feed applications, and auxiliary plant operations. Further, the urban construction trends also contribute significantly, driving the demand across the commercial buildings. These factors collectively sustain steady procurement cycles, with replacement demand, regulatory upgrades and capacity expansions shaping purchasing decisions across end-user industries.

Key Commercial Pumps Market Insights Summary:

Regional Highlights:

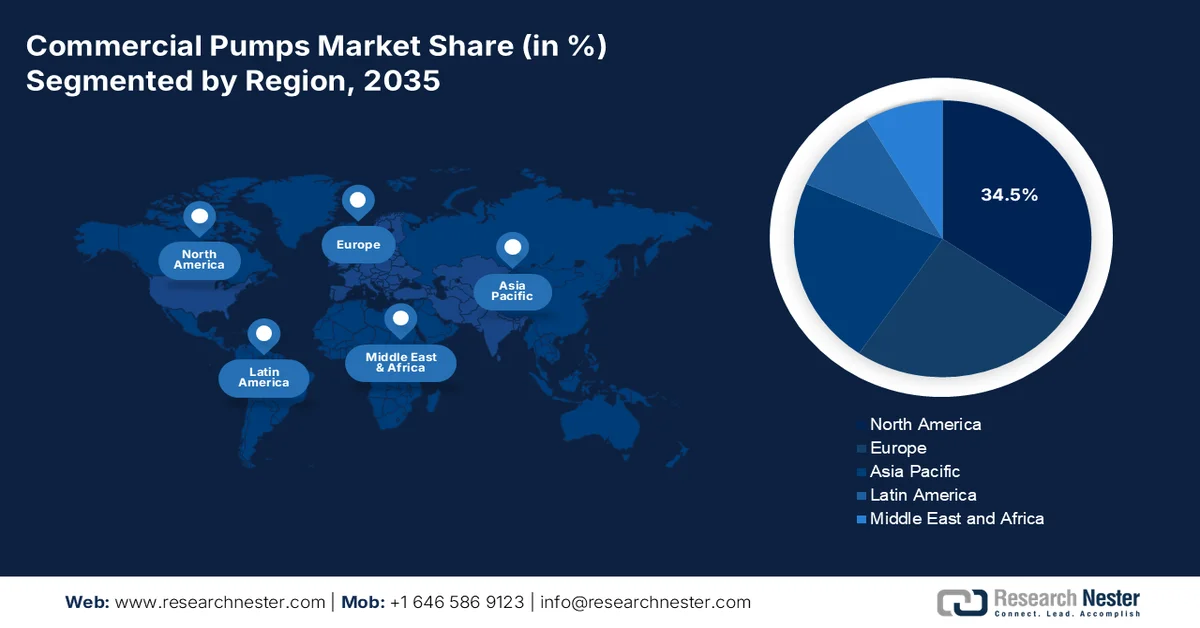

- North America commercial pumps market is anticipated to capture a 34.5% revenue share by 2035, bolstered by large-scale infrastructure modernization and stringent environmental regulations.

- Asia Pacific is forecast to expand at a CAGR of 7.5% during 2026–2035, accelerated by rapid urbanization, massive infrastructure investment, and industrial expansion.

Segment Insights:

- The centrifugal pumps sub-segment in the commercial pumps market is projected to account for a 68.4% share by 2035, propelled by their operational efficiency, simplicity, and suitability for a wide range of HVAC, water supply, and building services applications.

- The smart pumps segment is expected to witness notable growth during 2026–2035, fueled by increasing focus on energy optimization, predictive maintenance, and compliance with stringent green building codes.

Key Growth Trends:

- Wastewater treatment spending

- Agricultural and irrigation modernization programs

Major Challenges:

- High upfront costs and capital constraints

- Customer preference for after-sales support

Key Players: Xylem Inc. (U.S.), Flowserve Corporation (U.S.), ITT Inc. (U.S.), Grundfos Holding A/S (Denmark), Sulzer Ltd. (Switzerland), KSB SE & Co. KGaA (Germany), Atlas Copco AB (Sweden), Wilo SE (Germany), Ebara Corporation (Japan), Torishima Pump Mfg. Co., Ltd. (Japan), Weir Group PLC (UK), SPX Flow, Inc. (U.S.), Dover Corporation (U.S.), IDEX Corporation (U.S.), Danfoss A/S (Denmark), Concentric Group (UK), Officine Mazzocco Pagnoni (Italy), Kirloskar Brothers Limited (India), Setco Automotive Limited (India), Honda India Power Products Limited (India).

Global Commercial Pumps Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 53.4 billion

- 2026 Market Size: USD 55.1 billion

- Projected Market Size: USD 72.4 billion by 2035

- Growth Forecasts: 3.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (34.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Netherlands, China, Japan

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 30 March, 2026

Commercial Pumps Market - Growth Drivers and Challenges

Growth Drivers

- Wastewater treatment spending: Stricter discharge regulations and sustainability mandates are pushing governments to increase the funding for wastewater treatment infrastructure, directly influencing the commercial pumps market demand. The European Commission reports that member states collectively invest a billion annually in the wastewater management systems with upgrades targeting nutrient removal and energy efficiency operations. Pumps are critical in sludge handling, aeration processes, and water recirculation. According to Governor Kathy Hochul's August 2025 data, the Clean Water State Revolving Fund has provided over USD 153 billion for wastewater infrastructure projects, sustaining the continuous replacement and upgrade cycles. This regulatory push ensures recurring demand for high-efficiency and corrosion-resistant pumping systems.

- Agricultural and irrigation modernization programs: Government spending on irrigation and water efficiency in agriculture significantly contributes to the commercial pumps market. According to the UNESCO February 2024 data the agriculture accounts for nearly 70% of the global freshwater withdrawals, necessitating efficient irrigation systems supported by pumps. Moreover, in India, the schemes such as Pradhan Mantri Srishi Sinchayee Yojana focus on expanding irrigation coverage and improving water use efficiency, driving the pump installations in rural and semi-urban areas. These initiatives often include subsidies for pump procurement, mainly energy-efficient and solar-powered systems. Further, manufacturers targeting government-backed agricultural programs with cost-effective and energy-efficient pump solutions can access high-volume demand, especially in emerging economies, prioritizing food security and water conservation.

- Climate resilience and flood control investments: Rising climate risks are pushing governments to invest in flood control, stormwater management, and drainage infrastructure, all of which depend heavily on commercial pumps. Moreover, the global investments in flood protection infrastructure are increasing significantly, mainly in Asia and coastal regions where the urban flooding risks are high. Pumps are essential for dewatering stormwater evacuation and flood migration systems. Large-scale urban flood management projects include the installation of high-capacity pumping stations. Further, the high-capacity pumps with rapid deployment capabilities can benefit from emergency and resilience-focused government contracts, which are expected to grow as climate adaptation becomes a policy priority.

Challenges

- High upfront costs and capital constraints: The high initial capital expenditure required for advanced energy-efficient pumping systems poses a significant barrier, mainly in developing regions where customers lack capital. Users with smaller systems often opt for cheaper, less efficient pumps rather than investing in premium solutions. Rising material costs further pressure OEMs, forcing them to either absorb marginal losses or pass costs to buyers, which dampens sales volumes during economic uncertainty. Further, manufacturers must develop flexible financing models, leasing arrangements, or energy-performance contracting structures to lower the barrier to entry and accelerate the adoption of high-efficiency systems in price-sensitive markets.

- Customer preference for after-sales support: Commercial pump buyers mainly in critical applications such as HVAC, water treatment, and fire protection prioritize reliable after-sales service, spare parts availability, and rapid response times. The new players without established local distribution networks and service infrastructure struggle to gain customer trust, as end users are reluctant to risk the downtime with unproven suppliers. To overcome this barrier, new entrants in the market must partner with established local distributors, invest in regional service hubs, or offer extended warranty and guaranteed response-time commitments to build credibility and demonstrate reliability from the outset.

Commercial Pumps Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

3.1% |

|

Base Year Market Size (2025) |

USD 53.4 billion |

|

Forecast Year Market Size (2035) |

USD 72.4 billion |

|

Regional Scope |

|

Commercial Pumps Market Segmentation:

Product Type Segment Analysis

Under the product type segment, the centrifugal pumps sub-segment is dominating and is poised to hold the share value of 68.4% by the end of 2035 in the commercial pumps market. The segment is driven by their operational efficiency, simplicity, and suitability for a wide range of HVAC, water supply, and building services applications. These pumps utilize rotational kinetic energy to move fluids, making them ideal for continuous low viscosity applications prevalent in commercial buildings and municipal infrastructure. According to the OEC February 2026 data, the centrifugal pumps world trade reached USD 18.3 billion in 2024, highlighting the extensive installed base and significant opportunity to drive innovation and replacement demand.

Trade Flow of Centrifugal Pumps (2024)

|

Country |

Trade Flow |

Value (USD Billion) |

|

China |

Export |

4.76 |

|

Germany |

Export |

1.88 |

|

Italy |

Export |

1.37 |

|

U.S. |

Import |

2.02 |

|

Germany |

Import |

1 |

Source: OEC February 2026

Technology Segment Analysis

Within the technology segment, the smart pumps equipped with the integrated variable frequency drives, IoT, and cloud-based monitoring are leading in the commercial pumps market. This growth is fueled by the commercial sector’s increasing focus on energy optimization, predictive maintenance, and compliance with stringent green building codes. Smart pumps autonomously adjust speed and flow based on real-time system demand, delivering substantial energy savings compared to the traditional constant speed pumps while enabling facility managers to remotely monitor performance and detect anomalies before failure occurs. Additionally, the integration of advanced analytics and AI-driven insights in smart pump systems is further enhancing operational efficiency and extending equipment lifespan across commercial applications.

Sales Channel Segment Analysis

Distributors and wholesalers are leading the sales channel segment in the commercial pumps market, owing to their extensive networks, localized inventory, and ability to provide the technical support and aftermarket services that commercial end users and contractors require. This channel remains preferred because commercial pump systems often involve complex specifications, urgent replacement needs for critical applications such as HVAC and fire protection, and the requirement for on-site expertise that digital platforms cannot fully replicate. Distributors serve as vital intermediaries offering value-added services such as system design assistance, installation, and rapid spare parts availability. According to the Pumps Hydraulic Institute, February 2021 data, the U.S. pump sales are estimated at USD 10 billion annually, ensuring recurring revenue streams and high customer retention in the market.

Our in-depth analysis of the commercial pumps market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Application |

|

|

End user |

|

|

Technology |

|

|

Power Rating |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Commercial Pumps Market - Regional Analysis

North America Market Insights

North America is the largest and dominating region in the commercial pumps market and is expected to hold the regional revenue share of 34.5% by the end of 2035. The region is driven by large-scale infrastructure modernization and stringent environmental regulations. The U.S. leads the regional demand and is fueled by the Bipartisan Infrastructure Law, which allocates substantial funding for water and wastewater infrastructure upgrades. A key driver is the increasing adoption of smart pumping solutions integrated with IoT sensors and variable frequency drives, enabling predictive maintenance and energy optimization. Sustainability initiatives are pushing the manufacturers to develop high efficiency low emission pumps to meet the EPA standards and corporate ESG goals. The commercial pumps market is also seeing a growth in specialized applications such as hydrogen pumps for the emerging clean energy sector, supported by federal investments such as DOE’s Hydrogen Shot initiative.

The commercial pumps market in the U.S. is significantly shaped by federal energy efficiency regulations, particularly the DOE’s adopted standards for circulator pumps, which are set to take effect from 2028. According to the Federal Register May 2024 report, these standards are projected to deliver the lifetime energy savings of 0.55 quadrillion Btu, representing a 32.6% reduction in energy use compared to a no new standards scenario. Moreover, this creates a strong push toward high efficiency and smart pump systems across HVAC and building applications. The manufacturers are expected to incur conversion costs of USD 81.2 million. The long-term economic outlook remains favorable, with consumer net benefits ranging between USD 0.95 billion and USD 2.34 billion, driven by reduced operating costs. Furthermore, the environmental gains, including 10.04 million metric tons of CO₂ emission reductions, align with broader federal decarbonization goals, further driving the demand for commercial pumps market expansion.

U.S. DOE Circulator Pump Standards - Economic, Energy, and Environmental Impact (2024)

|

Category |

Metric |

Value / Range |

|

Manufacturer Impact |

Industry Net Present Value (INPV) new standards |

USD 347.1 million |

|

Change in INPV with standards |

-19.9% to +3.2% |

|

|

INPV Value Impact |

-USD 69.2 million to +USD 11.1 million |

|

|

Total Conversion Costs |

USD 81.2 million |

|

|

Energy Savings |

Lifetime Energy Savings (2028–2057) |

0.55 Quadrillion Btu |

|

Reduction vs No-Standards Case |

32.6% |

|

|

Consumer Benefits |

Net Present Value (7% discount rate) |

USD 0.95 billion |

|

Net Present Value (3% discount rate) |

USD 2.34 billion |

|

|

Environmental Impact |

CO₂ Emissions Reduction |

10.04 million metric tons |

|

SO₂ Emissions Reduction |

2.95 thousand tons |

|

|

NOx Emissions Reduction |

18.65 thousand tons |

|

|

Methane (CH₄) Reduction |

83.84 thousand tons |

|

|

Nitrous Oxide (N₂O) Reduction |

0.10 thousand tons |

|

|

Mercury (Hg) Reduction |

0.02 tons |

Source: Federal Register May 2024

The combination of agricultural demand and import dependence for key pump categories such as centrifugal systems is shaping the commercial pumps market in Canada. According to the OEC 2024 data country imported USD 588 million worth of centrifugal pumps, indicating a strong reliance on external supply to meet demand across irrigation, municipal, and industrial applications. On the other hand, there is a gradual shift toward alternative fuel-powered pumping systems, particularly propane-based irrigation pumps, which offer 20% to 40% lower acquisition costs compared to diesel engines and up to 50% operational savings, as reported in the Canadian Propane Association 2026 data. These systems also align with Canada’s environmental priorities by reducing particulate emissions and greenhouse gases, supporting cleaner farm operations. These data show a growing adoption of cost-efficient and low-emission pump technologies, particularly in agriculture-driven provinces.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the commercial pumps market and is expected to expand at a CAGR of 7.5% during the assessed period, 2026 to 2035. The region is driven by unprecedented urbanization, massive infrastructure investment, and industrial expansion across the region. The region invests significant billions to maintain growth, with water and urban development representing a substantial portion of this demand. Moreover, the initiatives in China that manage stormwater and improve urban drainage continue to drive the market adoption of advanced pumping systems. Further, other nations are investing heavily in water treatment infrastructure and data center development. Energy efficiency regulations are tightening across the region with the adoption of IE4 and IE5 motor standards for commercial pump applications.

The rapid progress of the Jal Jeevan Mission, which has expanded rural water infrastructure at an unprecedented scale, is driving the commercial pumps market in India. According to the PIB February 2025 data, over 15.44 crore rural households have been provided with tap water connections, a sharp increase from just 3.23 crore households since past decade. This expansion has required extensive deployment of pumps across groundwater extraction, bulk water transfer, treatment plants, and village-level distribution networks. The program’s infrastructure components, including piped water systems, greywater management, and source sustainability initiatives such as rainwater harvesting, further reinforce the sustained demand for both new pump installations and replacement systems. Moreover, the scale of implementation is reflected in coverage across 9.32 lakh schools and 9.69 lakh Anganwadi centers, indicating deep penetration of water supply systems into public infrastructure. These data show a positive impact on the market growth.

The large-scale government investment in water infrastructure and industrial capacity expansion is fueling the commercial pumps market in China. According to the People’s Republic of China, January 2026 data, the country invested over USD 810 billion in water conservancy projects supporting flood control, irrigation, and water supply systems that require extensive pump deployment. On the other hand, the February 2025 People’s Republic of China data depicted that China’s industrial sector generated over USD 5,676 billion in value-added in 2024, sustaining strong demand for pumps across chemical processing, manufacturing, and energy applications. These data show an increased adoption of energy-efficient pumping systems to meet regulatory and sustainability targets.

Europe Market Insights

The commercial pumps market in Europe is anticipated to account for a significant share, owing to the strong position, aggressive decarbonization targets, infrastructure modernization, and stringent environmental regulations. The European Green Deal, which aims for climate neutrality, serves as the overarching policy framework with the Renovation Wave strategy targeting the doubling of annual building renovation. This directly fuels the demand for the high efficiency HVAC circulatory pumps in commercial buildings. Moreover, the implementation of the Water Framework Directive and the Urban Wastewater Treatment Directive compels member states to upgrade the aging water and wastewater infrastructure, creating a sustained demand for centrifugal and submersible pumps. The market is also benefiting from increased investment in industrial automation and data center expansion across the region.

The industrial base energy transition and water infrastructure investments are driving the commercial pumps market in Germany. According to the GTAI 2025 data, the country’s manufacturing sector generated 29% of the total EU turnover, sustaining strong demand for industrial process and fluid handling systems, including pumps. Moreover, the Federal Government's August 2023 data reported that Germany allocated over USD 62.2 billion in energy transition and climate-related funding supporting applications such as district heating, hydrogen systems, and cooling infrastructure, where advanced pumping solutions are required. Further, over 96% of the population was connected to the public wastewater treatment systems based on the Bundesumweltministerium's February 2026 data, driving replacement demand for efficient pumps. These factors indicate a market has steady replacement cycles, high specification industrial demand, and therefore increasing adoption.

The sustained public investment in water infrastructure, building services, and energy systems is shaping the commercial pumps market in the UK. According to the Water UK October 2023 data, the water sector has committed over USD 121.9 billion in investment covering upgrades to water supply, wastewater treatment, and leakage reduction areas that require extensive deployment of pumping systems. Moreover, the UK Government's April 2023 data reports that the UK allocated over USD 38.1 billion toward energy efficiency and low-carbon infrastructure, supporting applications such as district heating, HVAC upgrades, and industrial decarbonization, where pumps play a critical role. These data reflect a market driven by regulatory investment cycles, infrastructure modernization, and increasing adoption of energy-efficient pumping technologies.

Key Commercial Pumps Market Players:

- Xylem Inc. (U.S.)

- Flowserve Corporation (U.S.)

- ITT Inc. (U.S.)

- Grundfos Holding A/S (Denmark)

- Sulzer Ltd. (Switzerland)

- KSB SE & Co. KGaA (Germany)

- Atlas Copco AB (Sweden)

- Wilo SE (Germany)

- Ebara Corporation (Japan)

- Torishima Pump Mfg. Co., Ltd. (Japan)

- Weir Group PLC (UK)

- SPX Flow, Inc. (U.S.)

- Dover Corporation (U.S.)

- IDEX Corporation (U.S.)

- Danfoss A/S (Denmark)

- Concentric Group (UK)

- Officine Mazzocco Pagnoni (Italy)

- Kirloskar Brothers Limited (India)

- Setco Automotive Limited (India)

- Honda India Power Products Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Xylem Inc. uses commercial pumps market data to drive its digital transformation strategy, integrating the smart pumping solutions with the advanced analytics and real-time monitoring capabilities. By utilizing market insights on energy efficiency and infrastructure resilience, Xylem develops intelligent pump systems that optimize water and wastewater management for commercial buildings and industrial facilities. In 2024, the company made a revenue of USD 1,498 million in water infrastructure.

- Flowserve Corporation harnesses commercial pumps market data to enhance its aftermarket services and the predictive maintenance offerings under its Flowserve 2.0 initiative. By analyzing performance data from thousands of installed pumps across commercial and industrial application the company delivers optimized reliability solutions that extend equipment life and improve energy efficiency. According to the 2024 annual report, the company has made sales of USD 3,158.6 million.

- ITT Inc utilizes commercial pumps market data to drive innovation in its industrial process and commercial pump portfolios, mainly via its Goulds Pump brand. By integrating data analytics into pump design and system monitoring, ITT delivers solutions that address growing market demands for energy efficiency and remote asset management in commercial HVAC building services.

- Grundfos Holding A/S leverages commercial pumps market data extensively to advance its digital ecosystem, including the Grundfos iSolutions platform, which integrates the pump controllers and cloud-based monitoring. By analyzing market trends toward sustainability and carbon neutrality, the company develops intelligent energy-optimized pumping solutions, commercial building HVAC systems, and water utilities.

- Sulzer Ltd applies commercial pumps market data to enhance its service network and develop high-efficiency pumping solutions for commercial and industrial applications, including building services, water transport, and district heating. Through its digital service platform, the company utilizes operational data to optimize pump performance and offer condition-based maintenance, reducing the unplanned downtime for commercial facility operators.

Here is a list of key players operating in the global commercial pumps market:

The global commercial pumps market is highly competitive and is defined by a mix of diversified industrial players and specialized fluid management firms. The key players are actively focusing on the digitalization offering smart pumps with IoT capabilities for predictive maintenance. Strategic initiatives include mergers and acquisitions to expand the technological portfolios and geographic reach, alongside a strong push toward energy-efficient and sustainable pumping solutions to meet the stringent environmental regulations and reduce the operational cost for end users. For example, in July 2025, Concentric Group announced the strategic acquisition of the leading pump manufacturer, Officine Mazzocco Pagnoni.

Corporate Landscape of the Commercial Pumps Market:

Recent Developments

- In November 2025, the Hydraulic Institute introduced member company Kirloskar Brothers Limited (KBL), as the latest company to have its pump test laboratory, located at Kirloskarvadi, Maharashtra, approved through the HI Pump Test Lab Approval Program.

- In June 2025, Setco Automotive Limited has launched its Automotive Water Pump, expanding its product portfolio into engine cooling solutions for Light Commercial Vehicles (LCVs) and Medium & Heavy Commercial Vehicles (MHCVs).

- In August 2024, Honda India Power Products Limited (HIPP) announced the launch of a 4-inch self-priming petrol water pump model, WB40XD. This innovative product aims to address the irrigation challenges faced by farmers growing water-intensive crops by providing portability, high-discharge, efficient, and eco-friendly solution.

- Report ID: 8479

- Published Date: Mar 30, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Commercial Pumps Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.