Application Container Market Outlook:

Application Container Market size was valued at USD 3.5 billion in 2025 and is projected to reach USD 39.1 billion by the end of 2035, rising at a CAGR of 27.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of application container is evaluated at USD 4.5 billion.

The application container market represents a fundamental shift in how enterprises deploy and manage software, which is centered on the adoption of containerization and orchestration platforms. This paradigm is critical for modernizing legacy infrastructure and scalable, portable workloads across hybrid and multi-cloud environments. According to the VMware white paper data in December 2022, nearly 96% of organizations are using or evaluating Kubernetes, which is the actual standard for container orchestration. This reflects a move beyond experimentation to production-grade deployment for core business applications. The expansion is further supported by increased investment in cloud-native technologies, with the CNCF landscape documenting a maturation of the ecosystem around security, networking, and management tools essential for operational stability at scale.

Application Container Market evolution is highly focused on addressing the operational and security complexities that are introduced by the widespread container adoption. The key driver is the urgent requirement to manage the entire application lifecycle securely from development to runtime. Reports from the National Institute of Standards and Technology state that the importance of software supply chain security is the heightened focus following increased scrutiny of vulnerabilities in open source components. Furthermore, the U.S. government's push for adopting zero-trust architectures, as outlined in federal strategy documents, is compelling suppliers to integrate robust security controls directly into their container platforms. This further includes the automated compliance checks and cryptographic software attestation to address the requirements of the government and financial sector, which is shaping the product development and enterprise procurement criteria.

Key Application Container Market Insights Summary:

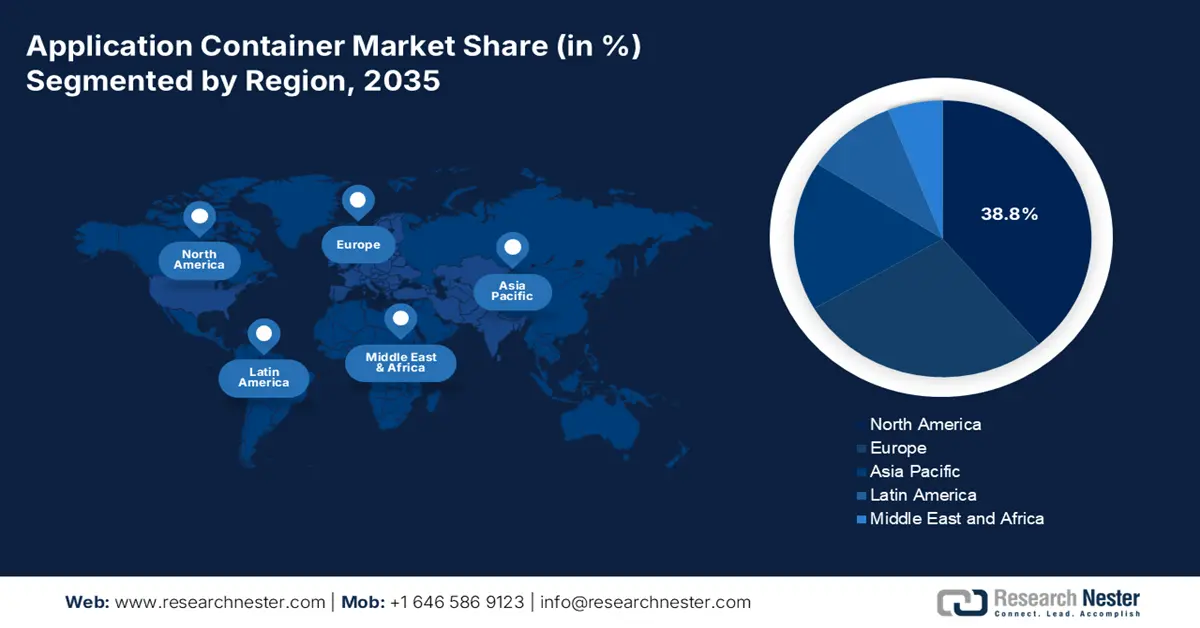

Regional Insights:

- Across 2026–2035, North America is anticipated to secure a 38.8% share of the application container market, underpinned by early cloud adoption and stringent federal modernization mandates.

- By 2035, Asia Pacific is set to expand rapidly at a 12.5% CAGR, propelled by extensive digital-infrastructure programs and accelerating cloud-native adoption across public and private sectors.

Segment Insights:

- By 2035, the cloud deployment mode in the application container market is expected to capture a 75.5% share, supported by the rising enterprise shift toward agile, scalable, and cost-efficient infrastructure models.

- By 2035, the IT & Telecommunications segment is projected to command a notable share, energized by its escalating need for ultra-reliable, scalable, and agile systems to power modern digital services and next-generation networks.

Key Growth Trends:

- Federal mandates for cloud first and modernization

- Accelerated software delivery and DevOps integration

Major Challenges:

- High initial investment and total cost of ownership

- Navigating the open source business model

Key Players: Docker Inc. (USA), VMware (Broadcom) (USA), Google LLC (USA), Amazon Web Services, Inc. (USA), Microsoft Corporation (USA),SUSE (Germany),Canonical Ltd. (UK),HashiCorp (USA), Mirantis Inc. (USA), Rancher Labs (SUSE) (USA),D2iQ Inc. (USA), Platform9 Systems, Inc. (USA), IBM Corporation (USA), Oracle Corporation (USA), Samsung SDS (South Korea),Tata Consultancy Services (India), Infosys Limited (India), NEC Corporation (Japan), Weaveworks (UK).

Global Application Container Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.5 billion

- 2026 Market Size: USD 4.7 billion

- Projected Market Size: USD 7 billion by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, Singapore, South Korea, Brazil, United Arab Emirates

Last updated on : 24 November, 2025

Application Container Market - Growth Drivers and Challenges

Growth Drivers

- Federal mandates for cloud first and modernization: Government expenditures on cloud are the main factors behind the change that is being driven by policies such as the U.S. Cloud Smart strategy, which is leading to a move to cloud native technologies for new IT investments. This, in turn, raises the need for application containers as the basic architecture for portable and modern applications. The U.S. Federal Cloud Computing Strategy details the need to use services that make the organization more efficient and secure, which is the main reason why containerized environments are attractive. This is resulting in a large, regulated application container market for vendors who are able to comply with federal standards for security, and thus procurement is directed to container-based platforms.

- Accelerated software delivery and DevOps integration: The adoption of DevOps and agile methodology is the key driver for the application container market. The reason of this dominance is due to the delivery of the necessary technical foundation for continuous integration and deployment. Develops and agile practices rely on containers to provide consistent environments across development and production, enabling continuous integration and rapid release cycles. This momentum is reinforced by the expansion of the availability of pre-hardened container images. For example, the report from the U.S. Department of Defense in April 2025, the Iron Bank container repository hosts more than 1,200 hardened images, which includes 400 commercial and 800 open-source containers, hence supporting a secure and efficient deployment within DevSecOps workflows.

- Increased focus on application portability: Application portability is another driver that is fueling the growth of the application container market. As companies try to prevent being locked into a single vendor and improve their adaptability, containers support and enable applications to operate in the same way in different environments. This movement is in line with the findings that indicate a large number of enterprises consider portability as the main factor in their cloud strategies. The move from on-premises to the cloud is a very important step for businesses. Further, the application container market is likely to expand as the investment by the firms in the latest technologies facilitates application portability, ensuring to have a flexible adoption in the changing business needs.

Challenges

- High initial investment and total cost of ownership: Building a competitive container platform requires a massive R&D investment. Apart from the development, the TCO includes ongoing support, cloud infrastructure, and maintenance costs are unpredictable. HashiCorp minimizes this for its users by providing a single commercial solution for securing, provisioning, and connecting containers across any cloud. This minimizes the TCO of multi-cloud container management, a significant pain point that they turn into a competitive advantage, justifying their commercial licensing against purely open source alternatives.

- Navigating the open source business model: Many container technologies are open source, making it difficult to monetize. Companies must strategically decide their features and check for the free and paid features. Docker Inc. has transformed this challenge by turning its business model away from its Docker Desktop software for large enterprises and towards a focus on developer security and supply chain management via Docker Scout, demonstrating the constant evolution which is required to find a sustainable revenue stream in an open source centric market.

Application Container Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

27.1% |

|

Base Year Market Size (2025) |

USD 3.5 billion |

|

Forecast Year Market Size (2035) |

USD 39.1 billion |

|

Regional Scope |

|

Application Container Market Segmentation:

Deployment Mode Segment Analysis

By 2035, the cloud is expected to dominate the deployment mode and is expected to hold the revenue share of 75.5% in the application container market. The dominance is due to the agility, scalability, and cost efficiency. The enterprise is rapidly shifting from capital-intensive on-premises infrastructure to operational expenditure models that are offered by the cloud providers. The U.S. Department of the Treasury in March 2022 reported that the public cloud services spending in technological research and consulting companies surged from USD 220 billion to USD 411 billion from 2016 to 2021. Major cloud providers such as AWS, Microsoft, and Google continuously innovate their managed container services, making them the most powerful deployment choice. This tendency is directly supported by government sources like the National Institute of Standards and Technology (NIST), which has long promoted the cloud model for its capacity for innovation and cost savings.

Application Segment Analysis

Under the application segment, the IT & Telecommunications sector is leading and is expected to hold a considerable share value by 2035. The key drivers of this segment are the vital need for ultra-reliable, scalable, and agile infrastructure to aid the modern digital services, VoIP platforms, and 5G core networks. The U.S. Department of State data in 2025 depicts that the government partners around the world to aid countries in enhancing the benefits of the digital ecosystem with secure and trusted ICT infrastructure and services. In order to advance this, USD 40.7 million is funded during the fiscal year 2023. Further, the containers enable telecom operators to build a resilient, distributed network and rapidly deploy new services. This transformation is essential for the rollout of next-generation telecommunications infrastructure.

Component Size Segment Analysis

The container platform is leading the component segment as it represents the foundational, integrated solutions that organizations require. The orchestration tools, such as Kubernetes, are vital as enterprises are highly seeking a comprehensive platform that bundles orchestration, monitoring, security, and developer tools into a single supported product. This reduces the operational overhead and complexity, hence accelerating the application modernization. The shift towards platforms is the upgradation of the market, moving from DIY assembly to managed enterprise-grade solutions. Large-scale landscapes of these technologies are created by industry consortia like the Cloud Native Computing Foundation (CNCF), emphasizing the ecosystem's expansion and the crucial role of integrated platforms.

Our in-depth analysis of the application container market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Mode |

|

|

Component |

|

|

Application |

|

|

Organization Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Application Container Market - Regional Analysis

North America Market Insights

North America is dominating the application container market and is expected to hold share of 38.8% during the forecast period, 2026 to 2035. The market is fueled by early cloud adoption and stringent federal mandates. Enterprise priorities include faster release cycles, resilient hybrid cloud, and cost optimization via container density and automation. Further, the organization is actively adopting a hybrid cloud, fueling the container demand. The key drivers include the modernization of legacy federal IT systems and the requirement for secure, scalable infrastructure to comply with zero-trust architecture directives from CISA and NIST. A primary trend is the integration of advanced security scanning and software supply chain governance into container pipelines, as outlined in NIST SP 800-218 on secure software development.

The government modernization standards and the shift towards cloud native architectures are driving up demand for the application container market in the U.S. Data from the Center for Strategic & International Studies in July 2023 shows that U.S. spending on cloud services across agencies was more than 12 billion, which is a clear indication of the rapid adoption of container orchestration and DevSecOps workflows. Such an investment is, therefore, the main factor behind the accelerated adoption of Kubernetes-based platforms in order to comply with these mandates. Moreover, the binding directives from CISA regarding the implementation of zero-trust security architectures are forcing agencies to adopt the micro-segmentation that is inherent in containerized environments. These forces ensure that application containers continue to be a primary and expanding federal IT landscape.

Canada’s application container market is driven by the government initiatives aimed at digital service modernization, strengthening data sovereignty, and improving cloud infrastructure. The Canadian Digital Government Strategy highlights containerization for scalable, secure public service delivery, which is supported by investments from Innovation, Science, and Economic Development Canada. The healthcare and financial services lead the adoption by prioritizing compliance and secure data handling. Further, companies leverage container orchestration to shorten the innovation cycles and reduce the operational costs. The government supports a framework for interoperability and multi-cloud portability, aligning with privacy and security standards. The collaboration among the federal and provincial organizations enhances cloud readiness and container service deployment. The presence of established cloud providers and a growing start-up ecosystem in Toronto and Vancouver bolsters market expansion.

APAC Market Insights

Asia Pacific is the fastest-growing application container market and is expected to grow at a CAGR of 12.5%. The market is driven by the rapid digital transformation. The key drivers of the market include massive government-led digital infrastructure initiatives such as India’s MeghRaj cloud policy and China’s Digital China initiative, which mandates the adoption of cloud native for public sector modernization. With a booming startup ecosystem and the expansion of hyperscale cloud data centers, the demand will further expand the market. The primary trend is the strategic focus on sovereign cloud capabilities and data residency, leading to investments in regional Kubernetes platforms. The push for IT self-reliance in countries such as China and India also stimulates the local container platform development. According to a NASSCOM report in August 2022,, cloud market in India is expected to reach USD 13.5 billion by 2026, a growth that is directly tied to container adoption for a scalable application deployment.

By 2035, the application container market in China will be driven by the top-down national strategies that mandate the deep integration of digital technology into the real economy. This state-driven initiative prioritizes the technological self-sufficiency and the development of sovereign digital infrastructure, which directly stimulates the demand for domestic cloud native and container technologies. The People’s Republic of China data in November 2023 indicated that the cloud computing market in China increased by over 40.91% in 2023. This highlights the massive scale of infrastructure investment upon which container adoption depends. Further, the growth is channeled towards modernizing key sectors like finance, manufacturing, and government services, where the containers are the foundational component for building scalable and resilient applications.

Japan is expected to hold a maximum share in the application container market in APAC during the forecast period. The country is driven by the corporate digital transformation and government pressure to enhance productivity and address a shrinking workforce. The key government policy is the Digital Garden City Nation Vision that aims to revitalize the regional economies via digital technology, therefore creating a demand for modern, scalable software platforms. A significant trend is the updating of old systems in manufacturing and finance through the use of containers for the development of agile and data-driven applications. his push is quantified by official investment data from Japan Wire Kyodo News in September 2024, indicating that the Japan firms' April-June pretax profits hit a record, investment up 7.4%. According to this information, cloud-native technologies become the main instrument for a company to stay competitive in industries with high added value and to address societal problems through technological innovation.

Europe Market Insights

The Europe application container market is defined by a strong growth driven by the robust data sovereignty regulations, thriving financial sector, and digital government initiatives. The EU’s coordinated push for digital autonomy via programs such as the Digital Europe Programme and the binding Cybersecurity Act pushes both public and private entities to adopt secure, portable, and resilient cloud architectures. A key driver is the GDPR compliance that makes the isolated, manageable nature of containers advantageous for data processing. Furthermore, the initiatives such as GAIA-X focus on creating a federated sovereign data infrastructure, inherently promoting container-based application development for portability across certified cloud providers. The region is also witnessing a surge in healthcare and life sciences adoption, accelerated by EU-level health data spaces.

UK is holding the largest revenue share in Europe during the forecast period 2026 to 2035. The country is driven by the dominance financial services sector and a proactive regulatory approach. The UK’s Financial Conduct Authority promotes technology innovation via its Sandbox initiative, promoting fintech to adopt cloud native technologies such as containers for scalability and resilience. The Cloud Industry Forum data in 2023 depicts that cloud continues to offer a variety of advantages, from greater agility (48%), flexibility in IT spend (32%), scalability (40%), and cost savings (31%). This data highlights the growth in the cloud native workloads, DevOps adoption, and enterprise migration to microservices. A key trend is the modernization of legacy public sector IT through the G-Cloud framework, which consistently awards contracts to providers offering Kubernetes-based solutions, ensuring sustained public investment.

Germany will maintain its position as a leader in the Europe application container market with the growth fundamentally tied to its manufacturing sector transformation and stringent data sovereignty laws. The government's Sovereign Cloud and participation in GAIA-X are establishing a secure market for Germany container platform providers that comply with the Federal Office for Information Security (BSI) standards. The major trend is the use of containers at the industrial edge, which enables real-time data processing for smart factories. The Plattform Industrie 4.0 initiative, financed by the Federal Ministry for Economic Affairs and Climate Action, is very active in the promotion of standardized, containerized software components for the purpose of interoperability in manufacturing thus it is becoming a huge and quite specific demand driver.

Key Application Container Market Players:

- Docker Inc. (USA)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Red Hat, Inc. (IBM) (USA)

- VMware (Broadcom) (USA)

- Google LLC (USA)

- Amazon Web Services, Inc. (USA)

- Microsoft Corporation (USA)

- SUSE (Germany)

- Canonical Ltd. (UK)

- HashiCorp (USA)

- Mirantis Inc. (USA)

- Rancher Labs (SUSE) (USA)

- D2iQ Inc. (USA)

- Platform9 Systems, Inc. (USA)

- IBM Corporation (USA)

- Oracle Corporation (USA)

- Samsung SDS (South Korea)

- Tata Consultancy Services (India)

- Infosys Limited (India)

- NEC Corporation (Japan)

- Weaveworks (UK)

- Docker Inc. is a key player in the application container market, which was largely influenced by the container revolution built around the developer-friendly Docker Engine. With changes in the market, the firm made a smart decision to change its focus to securing the software supply chain for developers and enterprises. Basically, their solutions aim at enabling development teams to easily access trusted content, accelerate their development workflows, and leverage in-depth security scanning with Docker Scout and Docker Hub.

- Red Hat Inc. exerts immense influence on the application container market mainly via its industry-standard Kubernetes platform, OpenShift. The strategic initiative of the company is to provide a comprehensive, enterprise-grade container application platform that spans hybrid and multi-cloud environments. Integrating developer tools, operational management, and security enforcement into a single platform, the company enables large organizations to modernize their traditional applications.

- VMware is positioned to be the strongest player in the application container market with its Tanzu portfolio to bring modern containerized applications and Kubernetes to its vast enterprise customer base already using vSphere and VMware Cloud. The annual revenue for the second quarter in 2024 was USD 3.41 billion, highlighting the increased demand in the container-based services.

- Google is an architectural pillar in the application container market and originally developed the Kubernetes orchestrator that became the industry standard. The primary strategic initiative is to use Google Kubernetes Engine, which is a fully managed, secure, and scalable service. The company actively focuses on advancing the application container market with innovations in multi-cluster management, tight integration, and serverless containers.

- Amazon Web Services is a dominant leader that significantly influences the direction of the application container market with its various intertwined and scalable services. Amazon aims to give customers freedom of choice through Amazon ECS and a Kubernetes-certified service, Amazon EKS, as its main strategy. The annual revenue increased by 11% year-over-year from USD 575 billion to USD 638 billion.

Here is a list of key players operating in the global application container market:

The application container market is very competitive and is dominated by the cloud native innovators and tech giants. The key players of the market are setting foundational standards, while hyperscalers AWS, Microsoft Azure, and Google Cloud use containers to drive the consumption of cloud. Further, ecosystem control through strong managed services, simplified developer tooling, and all-encompassing security solutions are the main strategic priorities. Major acquisitions such as Cloudera purchased Taikun to deliver a cloud experience to data anywhere for AI everywhere in August 2025, highlighting the consolidation trends to provide full-stack platforms. The competition is highly shifting towards the orchestration layers and integrated DevOps toolchains, pushing traditional IT firms and system integrators to build specialized containerization services to remain relevant.

Corporate Landscape of the Application Container Market:

Recent Developments

- In November 2025, ActiveState has announced the launch of Secure Container Image Catalog, which is a new web-based resource designed to help developers, DevOps, and security professionals easily browse, evaluate, and pull the latest secure container images, without the need for third-party registries.

- In August 2025, F5 has announced the acquisition of MantisNet to enhance cloud-native observability in the F5 Application Delivery and Security Platform. This acquisition offers a comprehensive platform to deploy, observe, and secure the applications and networks across various domains.

- In February 2025, Akamai introduced a managed container service for enterprises to accelerate application development and deployment. The service is aimed at delivering better experiences by running workloads closer to users, devices, and sources of data.

- Report ID: 8266

- Published Date: Nov 24, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Application Container Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.