Anti-corrosion Coating Market Outlook:

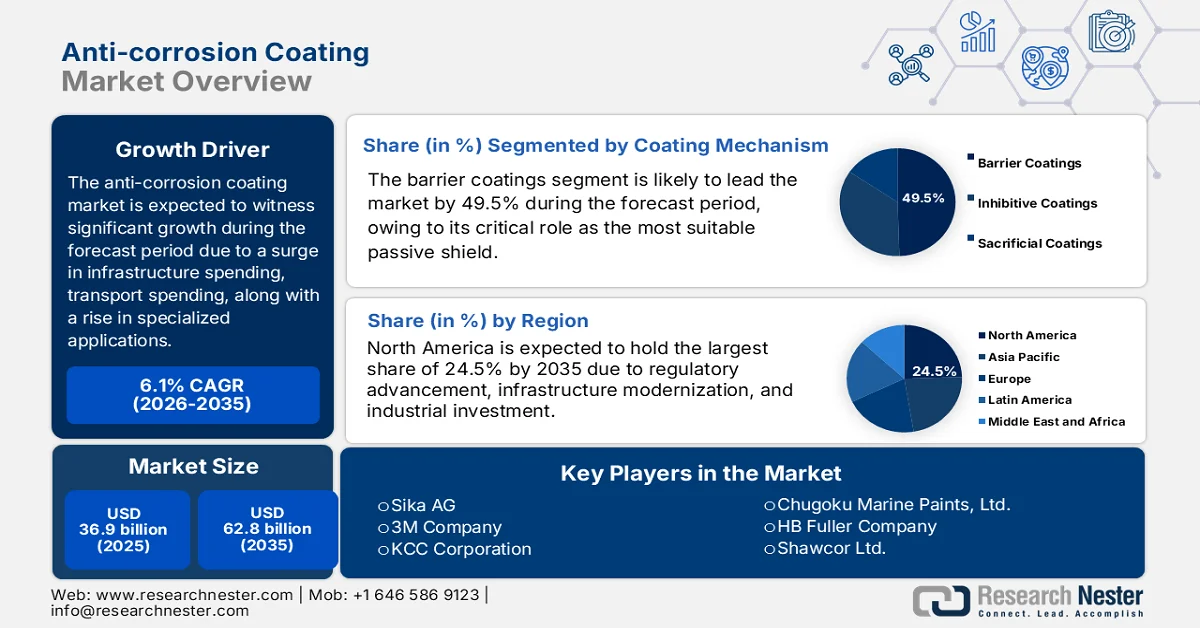

Anti-corrosion Coating Market size was valued at over USD 36.9 billion in 2025 and is expected to reach USD 62.8 billion by the end of 2035, growing at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of anti-corrosion coating is estimated at USD 39.1 billion.

The worldwide anti-corrosion coating market is being reshaped by a convergence of factors beyond foundational factors of energy production and infrastructure expenditure. These factors include the rise of specialized applications, the transformative impact of digitalization on asset management, the economic imperative of lifecycle cost optimization, and raw material price volatility. According to official statistics published by OECD in June 2025, nearly one-quarter of nations with available information, which is 8 out of 33 countries or 24%, demand asset management plans under regulation or law. Moreover, advanced funding instruments tend to provide investment for infrastructure maintenance, with grants and subsidies, which is 29% or 88%, along with long-lasting revenue generation from current assets, thereby making it suitable for uplifting the market growth.

Furthermore, the integration of self-healing and smart coating technologies, the proliferation of nanotechnology-based formulations, the development of multi-functional coating systems, and a sudden shift towards application-specific engineered solutions are certain trends that are fueling the anti-corrosion coating market globally. According to an article published by the America Coatings Association in 2026, the worldwide smart coatings industry, which comprises self-cleaning, self-healing, and self-stratifying, was worth USD 885.5 million, further reaching an estimated USD 1 billion as of 2024. Besides, conventional blocked catalysts effectively require high temperatures, ranging between 120 degrees and 150 degrees Celsius. Besides, by readily encapsulating unblocked catalysts in a thermoplastic, the polymeric matrix melts a lower temperature ranging from 60 degrees to 75 degrees Celsius, thus proliferating the market expansion.

Key Anti-corrosion Coating Market Insights Summary:

Regional Highlights:

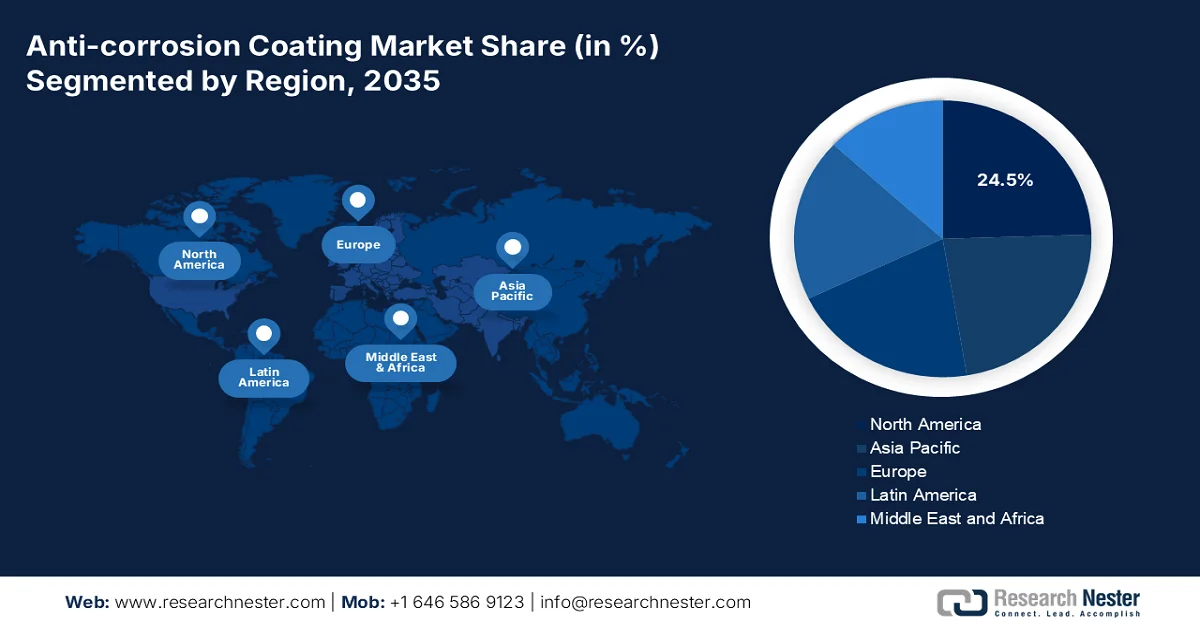

- North America in the anti-corrosion coating market is projected to hold a 24.5% share by 2035, impelled by large-scale infrastructure modernization, rising industrial reinvestment, and expanding clean energy and rehabilitation investments.

- Europe is expected to emerge as the fastest-growing region during 2026-2035, attributed to stringent environmental regulations and accelerating transition toward sustainable high-solids and water-borne coating technologies.

Segment Insights:

- The barrier coatings sub-segment of the anti-corrosion coating market is projected to capture a 49.5% share by 2035, propelled by its ability to act as a passive shield protecting substrates from oxygen, moisture, and electrolytes.

- Solvent-borne coatings are poised to secure the second-largest share across 2026-2035, buoyed by superior adhesion, durability, and high performance in harsh and moisture-intensive environments.

Key Growth Trends:

- Expansion of the offshore energy

- Increased electrification of transport

Major Challenges:

- Stringent environmental regulations and compliance costs

- Raw material price volatility and supply chain disruptions

Key Players: PPG Industries (U.S.), AkzoNobel (Netherlands), The Sherwin-Williams Company (U.S.), BASF SE (Germany), RPM International Inc. (U.S.), Nippon Paint Holdings Co., Ltd. (Japan), Jotun (Norway), Axalta Coating Systems (U.S.), Hempel A/S (Denmark), Kansai Paint Co., Ltd. (Japan), Sika AG (Switzerland), 3M Company (U.S.), KCC Corporation (South Korea), Chugoku Marine Paints, Ltd. (Japan), HB Fuller Company (U.S.), Shawcor Ltd. (Canada), DAW SE (Germany), Cromology (France), Carpoly Chemical Group Co., Ltd. (China), Berger Paints India Limited (India), BirlaNu (India), RuggON (Taiwan).

Global Anti-corrosion Coating Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 36.9 billion

- 2026 Market Size: USD 39.1 billion

- Projected Market Size: USD 62.8 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (24.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Indonesia, Vietnam, Mexico

Last updated on : 12 March, 2026

Anti-corrosion Coating Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of the offshore energy: The worldwide transition toward the latest forms of energy production is one of the sustained and massive drivers of the anti-corrosion coating market demand. According to official statistics published by the Ember Energy Organization in October 2025, the offshore wind deployment is projected to surge and nearly triple by the end of 2030, significantly increasing from 83 GW to 238 GW. Moreover, 88 nations have identified offshore wind potential, along with 11 proactive developing plans. Besides, in the U.S., nearly 5.8 GW of offshore wind is currently projected to be developed between 2205 and 2029, which is further based on the present 5 projects under construction, thus denoting a positive impact on the anti-corrosion coating market’s growth and expansion.

- Increased electrification of transport: The international shift toward electric vehicles is creating demanding and new requirements for corrosion protection, which is positively impacting the anti-corrosion coating market. As per an article published by the UNECE Organization in May 2025, the transport industry is one of the major contributors to global greenhouse gas emissions, accounting for 23% of energy-based carbon dioxide emissions. Besides, there has been an increase in electric car sales, surpassing 10 million as of 2022, and this further surged to an additional 35% in 2023, reaching 14 million units. Moreover, the substantial growth in electric cars has positively impacted the industrial share within the total automotive sector, rising from roughly 4% of overall car sales to 14% in 2022, thus fueling the market development.

- Focus on infrastructure renewal super-cycle across developed economies: The aspect of infrastructure development across emerging economies is a well-known driver, as well as a powerful and distinct driver, focusing on the renewal super-cycle. As per data published by OECD, as of 2023, the infrastructure investment amounted to USD 14.7 billion in Germany, which is followed by USD 14.4 billion in France, USD 13.2 billion in Japan, and USD 10.7 billion in Australia. Besides, based on government estimates published by the PIB Government in February 2025, the overall infrastructure investment in India has significantly enhanced, with private and public sector contributions deliberately shaping the growth trajectory based on a generous budget allocation of USD 120.5 billion, thus fueling the anti-corrosion coating market exposure.

Challenges

- Stringent environmental regulations and compliance costs: The single most significant challenge confronting the anti-corrosion coating market is the intensifying regulatory pressure regarding volatile organic compound (VOC) emissions. Regulatory bodies worldwide, including the Environmental Protection Agency (EPA) in the U.S. and Europe through its Industrial Emissions Directive and REACH framework, are implementing increasingly stringent emission standards that directly impact coating formulations. These regulations have led to compliance costs that are deliberately increasing for manufacturers over the past five years, with many regions banning certain solvents entirely. This financial burden extends far beyond simple reformulation costs, thereby negatively impacting market growth.

- Raw material price volatility and supply chain disruptions: The anti-corrosion coating market faces persistent and intensifying challenges from fluctuating raw material prices and supply chain disruptions that threaten profitability and operational stability. Key components essential to coating formulations, including epoxy resins, polyurethanes, titanium dioxide, specialty solvents, pigments, and zinc-based materials, have experienced price increases in recent years, squeezing manufacturer margins across the value chain. This volatility stems from multiple interconnected factors. Geopolitical tensions, particularly the Russia-Ukraine conflict, have disrupted energy markets and chemical supply chains globally. Moreover, trade policies and tariff regimes add another layer of complexity, thus causing a hindrance to market expansion.

Anti-corrosion Coating Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 36.9 billion |

|

Forecast Year Market Size (2035) |

USD 62.8 billion |

|

Regional Scope |

|

Anti-corrosion Coating Market Segmentation:

Coating Mechanism Segment Analysis

The barrier coatings sub-segment, which is part of the coating mechanism segment, is anticipated to garner the highest share of 49.5% in the anti-corrosion coating market by the end of 2035. The sub-segment’s upliftment is highly propelled by its role acting as a passive shield that deliberately substrates from oxygen, electrolytes, and moisture to combat oxidation. According to official statistics published by NLM in September 2022, there has been an increase in the packaging paper consumption by 2.1%, as well as household and sanitary paper by 3.1%, especially in Europe. Therefore, this denotes eco-friendly utilization of petroleum-based polymeric packaging materials and coatings. Besides, barrier coatings made of natural, renewable biopolymers can be readily applied to paper packing materials, thereby making it suitable for boosting the sub-segment’s growth.

Technology Segment Analysis

Based on technology, the solvent-borne coatings segment in the anti-corrosion coating market is projected to account for the second-largest share during the forecast period. The segment’s growth is highly fueled by its performance in high-moisture and harsh environments, durability, and superior adhesion. Additionally, this segment's enduring market leadership stems from its superior performance characteristics in demanding environments, offering unparalleled adhesion, film formation, and chemical resistance that alternative technologies have yet to fully replicate. Moreover, the growth is reinforced by advanced formulation flexibility that allows manufacturers to engineer coatings for specific performance requirements through sophisticated resin chemistry and cross-linking technologies, thereby positively impacting the segment globally.

Type Segment Analysis

By the end of the stipulated timeline, the epoxy coatings sub-segment, part of the type segment, is expected to hold the third-largest share in the anti-corrosion coating market. The sub-segment’s development is highly attributed to durable barrier protection, high chemical resistance, and exceptional adhesion against electrolytes, oxygen, and water. As per an article published by the America Coatings Association in 2026, an estimated 16% of the overall demand for binders is utilized in coatings that are supplied by epoxy resins. Besides, liquid epoxy resin is also utilized for 100% solids epoxy formulas that are applied as tank linings, concrete surfacers, and other select applications. Additionally, this is augmented with novolac and phenoxy resins that tend to enhance performance features, thus denoting an optimistic outlook for the sub-segment expansion.

Our in-depth analysis of the anti-corrosion coating market includes the following segments:

|

Segment |

Subsegments |

|

Coating Mechanism |

|

|

Technology |

|

|

Type |

|

|

Material |

|

|

End use Industry |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Anti-corrosion Coating Market - Regional Analysis

North America Market Insights

North America is anticipated to account for the largest share of 24.5% in the anti-corrosion coating market by the end of 2035. The market’s upliftment in the region is highly propelled by infrastructure modernization, industrial reinvestment, and regulatory evolution, along with the presence of massive rehabilitation programs. According to official statistics published by the RMI Organization in February 2025, between January 2023 and December 2024, the private sector invested approximately USD 150 billion in operating, under-construction, and under-construction infrastructure projects across 10 sectors. Moreover, as per the 2026 Clean Investment Monitor Organization article, USD 278 billion has been generously invested across the U.S. for deployment and manufacture of clean energy, carbon management technology, clean vehicles, and building electrification, thus denoting a 5% increase from 2024, which is positively impacting the anti-corrosion coating market growth.

Quarter-Wise Clean Investment Analysis in the U.S. (2018-2025)

|

Year |

Quarter 1 (USD Billion) |

Quarter 2 (USD Billion) |

Quarter 3 (USD Billion) |

Quarter 4 (USD Billion) |

|

2018 |

15 |

18 |

22 |

22 |

|

2019 |

17 |

21 |

24 |

23 |

|

2020 |

25 |

25 |

30 |

33 |

|

2021 |

31 |

35 |

36 |

37 |

|

2022 |

39 |

42 |

44 |

47 |

|

2023 |

48 |

56 |

61 |

64 |

|

2024 |

61 |

67 |

70 |

68 |

|

2025 |

67 |

71 |

79 |

60 |

Source: Clean Investment Monitor Organization

The anti-corrosion coating market in the U.S. is growing significantly, owing to the infrastructure renewal super-cycle, expansion in the oil and gas industry, and the offshore wind energy build-out. As per an article published by the U.S. Department of Energy in January 2026, the crude oil production in the country has effectively set an all-time high output record of 13.6 million b/d as of 2025, which is projected to continue throughout 2026. Moreover, gas prices are at a 4-year low, averaging almost USD 2.9 per gal and are deliberately continuing to plummet, while gas is currently found under USD 3 per gallon across 43 states in the country. Besides, natural gas is predicted to reach 109 billion cubic feet per day by the end of 2026, which is a new all-time high. Therefore, with all such expansions, the market in the country is gradually gaining increased exposure.

The aspects of asset production, harsh climatic conditions, the sudden shift towards sustainable coatings and eco-friendliness, and the presence of offshore and maritime energy activities are certain factors that are bolstering the anti-corrosion coating market in Canada. As per an article published by the Government of Canada in July 2025, the Minister of Energy and Natural Resources declared nearly USD 16 million in federal funding for energy projects across maritime provinces that assist in delivering affordable and reliable clean energy in New Brunswick, Nova Scotia, and Prince Edward Island. In addition, this particular funding readily drives innovation that powers economic advancement and creates suitable employment opportunities throughout the country. Besides, as per the November 2023 ITA article, the country’s overall installed electricity generation capacity accounted for an estimated 149 GW, which is further expected to reach 170 GW by the end of 2035, thus proliferating the anti-corrosion coating market expansion.

Europe Market Insights

Europe in the anti-corrosion coating market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly fueled by the existence of stringent environmental regulations, robust emphasis on sustainable innovation, and escalation in the transition to high-solids and water-borne coating technologies. Besides, the market in the overall region is also propelled by technological dominance in nanotechnology and smart coatings, with Nordic and German-based manufacturers readily pioneering self-healing and sensor-based protective systems. Moreover, the region significantly reflects balanced growth across established industrial economies and emerging East Europe industries, thus making it suitable for driving the market.

The anti-corrosion coating market in Germany is gaining increased traction, owing to the presence of a powerful presence of industrial base and suitable leadership in automotive manufacturing, chemical production, and mechanical engineering. According to official statistics published by the Germany Trade and Invest (GTAI) in 2025, the automotive industry in the country accounted for 1.3 million passenger electric vehicles that were produced in 2024, thus making the country the second-biggest producer. This caters to 24% of the overall domestic industry revenue generated by the automotive industry, with more than 60% growth in research and development in the region, which is readily created by domestic automotive industries. Moreover, the industry comprises 158,000 highly skilled research and development personnel, thus fueling the market expansion.

The alignment with regional chemical regulations, development of independent enforcement mechanisms, and innovation budget for sustainable chemical initiatives are certain factors that are responsible for driving the anti-corrosion coating market in the UK. As per a data report published by the UK Business in August 2024, the chemicals industry in the country is expected to double the economic output and significantly reduce its greenhouse gas emissions by sourcing 80% of its carbon requirement by the end of 2050. Moreover, the UK CHEM 2050 Ambition demands 14.7% of all domestic theoretical sustainable carbon readily available from biomass, carbon dioxide, and recycled carbon from CCU. This is equivalent to 22.4% of theoretical carbon, 11.5% from carbon dioxide, and 101.7% from recycled carbon, thereby making it suitable for bolstering the market growth.

APAC Market Insights

The Asia Pacific in the anti-corrosion coating market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by unprecedented industrialization, infrastructure investment, urbanization, and generous spending across Southeast Asia, India, and China. According to official statistics published by Market Genics in August 2025, the region is significantly leading the protective coatings market with an industrial share accounting for 56.3% with USD 7.7 billion in revenue. In addition, the industrial opportunities amounted to an estimated USD 6 billion, which is positively impacting the market growth in the overall region. Besides, China accounts for 42% of the regional share of protective coatings, thereby creating an optimistic outlook for the overall market’s expansion in the region.

The anti-corrosion coating market in China is gaining increased exposure, owing to industrial output, infrastructure construction, unparalleled scale in manufacturing, investment in the chemical industry, and a huge demand for marine-based coatings. As stated in an article published by the China Organization in March 2026, the country’s gross domestic product growth target accounts for between 4.5% and 5%, which is further projected to increase by more than USD 869.6 billion. Besides, the country is poised to earmark USD 36.3 billion in long-lasting manufactured consumer goods trade-in programs, further generating USD 605 billion in sales, readily driving 531 million customer transactions. Therefore, with such growth opportunities in the domestic manufacturing industry, the market is continuously expanding in the overall country.

The aspects of governmental investments for encompassing roads, railways, ports, and urban infrastructure, attracting international manufacturing funding, administrative production-based incentive schemes, and the presence of port modernization programs are certain trends that are boosting the anti-corrosion coating market in India. Based on government estimates published by the PIB Government in October 2025, almost 95% of the country’s trade by volume and nearly 70% by valuation move through maritime routes. Moreover, the Maritime India Vision 2030 approach has focused on more than 150 initiatives with expected investments amounting to USD 35.5 billion to USD 41.5 billion, which is deliberately supported by a USD 7.5 million package for shipbuilding. Therefore, with such developments, there is a huge growth opportunity for the market in the country.

Key Anti-corrosion Coating Market Players:

- PPG Industries (U.S.)

- AkzoNobel (Netherlands)

- The Sherwin-Williams Company (U.S.)

- BASF SE (Germany)

- RPM International Inc. (U.S.)

- Nippon Paint Holdings Co., Ltd. (Japan)

- Jotun (Norway)

- Axalta Coating Systems (U.S.)

- Hempel A/S (Denmark)

- Kansai Paint Co., Ltd. (Japan)

- Sika AG (Switzerland)

- 3M Company (U.S.)

- KCC Corporation (South Korea)

- Chugoku Marine Paints, Ltd. (Japan)

- HB Fuller Company (U.S.)

- Shawcor Ltd. (Canada)

- DAW SE (Germany)

- Cromology (France)

- Carpoly Chemical Group Co., Ltd. (China)

- Berger Paints India Limited (India)

- BirlaNu (India)

- RuggON (Taiwan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- PPG Industries is continuing to lead through innovation, having launched PPG PRIMERON Optimal in August 2024, a patent-pending zinc epoxy powder primer formulated with an optimized zinc content that provides superior corrosion protection meeting rigorous ISO standards while offering transfer efficiency and reducing greenhouse gas emissions. The company's commitment to sustainably advantaged solutions positions it strongly in the high-performance industrial and automotive coating segments.

- AkzoNobel leverages its international brand to strengthen partnerships in the marine sector, recently extending its agreement with China's Winning Shipping to supply biocide-free Intersleek 1100SR fouling control coatings that deliver fuel savings and reduced GHG emissions. The company's focus on sustainable innovation through advanced slime-release technology demonstrates its strategic emphasis on environmental performance and operational efficiency for deep-sea vessels.

- The Sherwin-Williams Company has introduced Heat-Flex ACE, a high-performance primer specifically engineered to combat corrosion under insulation (CUI) in the oil and gas industry, tested to ISO 19277:2018 standards, and effective across a wide temperature range. This launch addresses the never-ending battle against CUI with functional chemical enhancements that surpass traditional solvent-based epoxy phenolic coatings.

- BASF SE leverages its construction chemicals division to provide advanced admixtures offering maximum corrosion protection for infrastructure applications, targeting regional markets with technically superior solutions. The company's extensive R&D capabilities in material science enable it to maintain a strong position in heavy-duty industrial and chemical processing environments where corrosion resistance is critical.

- RPM International Inc. owns subsidiaries, including Carboline, that are world leaders in corrosion control coatings, serving industrial markets globally with specialty chemicals, flooring coatings, and protective systems for demanding applications. With suitable manufacturing facilities across 119 locations, especially in Argentina, RPM's diversified portfolio under brands such as Stonhard and Tremco provides comprehensive asset protection solutions to the industrial sector.

Here is a list of key players operating in the global market:

The global anti-corrosion coating market is characterized by a consolidated competitive landscape, where the top 10 players led by PPG, AkzoNobel, and Sherwin-Williams account for the majority of the market share. These industry leaders are pursuing aggressive growth through strategic acquisitions and geographic expansion into high-potential markets, such as the Asia Pacific and the Middle East. A dominant trend is the industry-wide pivot toward sustainable innovation, with major investments in water-borne, high-solids, and powder coating technologies to comply with stringent environmental regulations such as Europe REACH and EPA VOC limits. Besides, in November 2025, Akzo Nobel N.V. and Axalta Coating Systems Ltd. entered into a definitive deal to combine in an all-stock-based merger, developing an international coatings organization with an enterprise valuation of an estimated USD 25 billion, thus driving the anti-corrosion coating industry.

Corporate Landscape of the Anti-corrosion Coating Market:

Recent Developments

- In November 2025, BirlaNu has significantly signed a standard deal for acquiring Clean Coats Private Limited. This particular tactical move has underscored the company’s commitment to upscaling its construction-based chemical business.

- In November 2025, RuggON unveiled VULCAB 10A, which is an AI-specific enhanced and rugged vehicle-mounted computer built for always-on industrial mobility and readily deliver uninterrupted performance across demanding industrial applications.

- In March 2025, Sherwin-Williams Protective & Marine unveiled superior coating system consistency and specification efficiency, along with an expanded line of global core products that are effectively available at the same performance and quality standards across different nations.

- Report ID: 8432

- Published Date: Mar 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.