Agricultural Micronutrients Market Outlook:

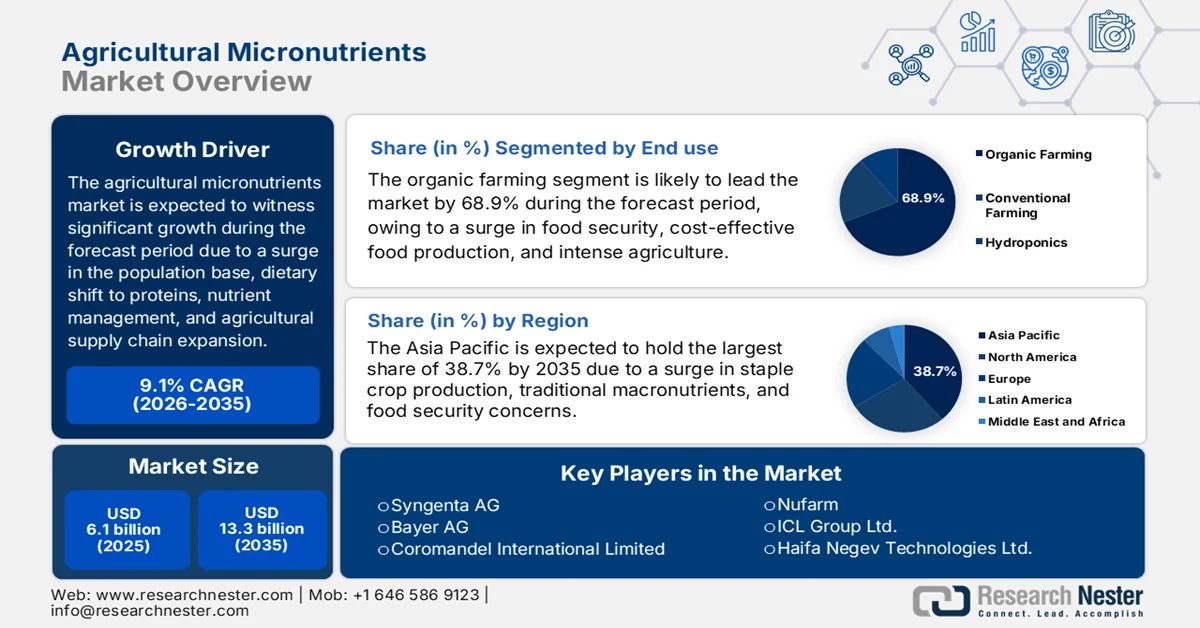

Agricultural Micronutrients Market size was valued at over USD 6.1 billion in 2025 and is expected to reach USD 13.3 billion by the end of 2035, growing at a CAGR of 9.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of agricultural micronutrients is estimated at USD 6.6 billion.

The global agricultural micronutrients market is gradually shaping based on a rise in the worldwide middle-class population, the dietary transition towards protein-based and horticultural production, the demand for nutrient management, and the expansion of the corporate agricultural supply chain and contract farming. According to official statistics published by Project Drawdown in December 2025, the U.S., India, and China, together, account for 52% of global excess nitrogen application. Besides, nitrous oxide emissions usually peak when nitrogen availability is extremely high, and the soil moisture ranges from 70% to 90%. Based on this, water management is essential to overcome long-lasting periods of soil moisture, which is extremely crucial to cater to nutrient management, especially in irrigated croplands and wet climates, thus bolstering the market growth.

Furthermore, the biological chelation and next-generation formulations, data-based application and digitalized integration, the regenerative agriculture alignment, as well as controlled and urban environment agriculture are a few trends that are responsible for uplifting the agricultural micronutrients market globally. As per an article published by Smart Agricultural Technology in December 2022, by the end of 2050, the population is anticipated to increase from 7.7 billion to 9.2 billion, along with a rise in the urban population by 66%, leading to a decline in arable land by an estimated 5 million hectares. Besides, the worldwide greenhouse gas emissions is also expected to increase by 50%, as well as a reduction in agri-food production by 20%, and an increase in food demand from 59% to 98%. Therefore, based on all these reductions and decline, there is a huge demand for digitalization in the agriculture industry.

Key Agricultural Micronutrients Market Insights Summary:

Regional Highlights:

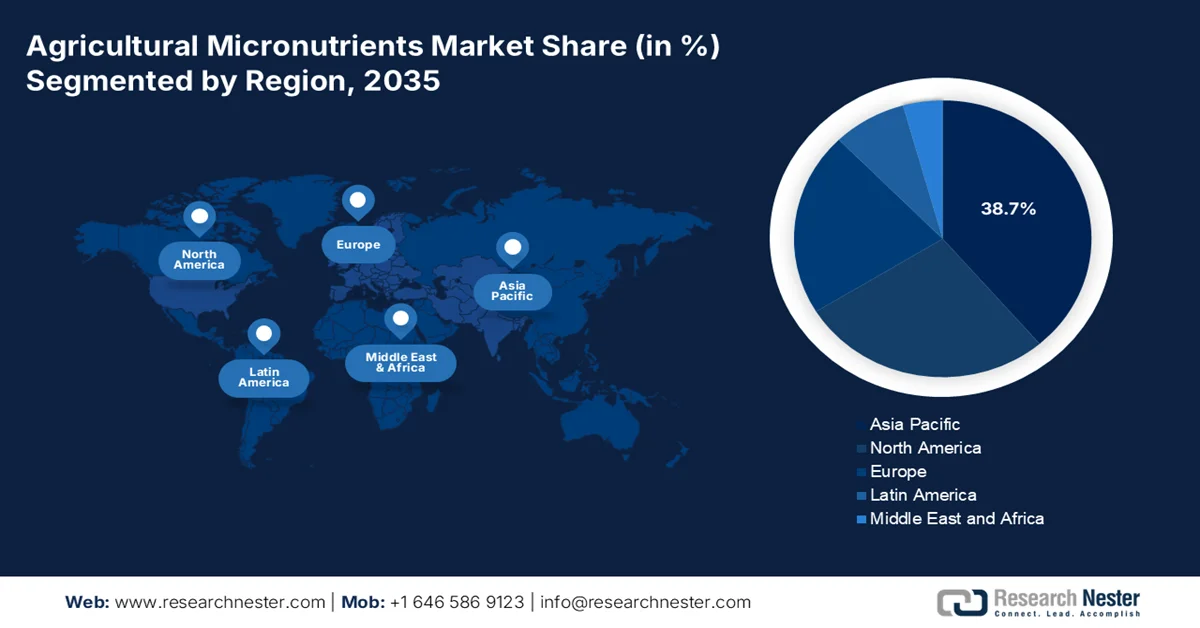

- Asia Pacific is projected to capture a 38.7% share of the agricultural micronutrients market by 2035, driven by rising soil nutrient depletion and increasing focus on balanced crop nutrition

- Europe is expected to register the fastest growth during 2026-2035, fueled by the growing emphasis on sustainable farming practices and adoption of climate-smart agriculture

Segment Insights:

- In the agricultural micronutrients market, the organic farming segment is anticipated to account for a 68.9% share by 2035, propelled by increasing demand for chemical-free cultivation and sustainable food production

- The chelated sub-segment is projected to secure the second-largest share by 2035, owing to its enhanced nutrient stability and improved plant uptake efficiency

Key Growth Trends:

- Increase of biofortification for nutritional security

- Expansion in plant genetic and breeding

Major Challenges:

- Distribution fragmentation and counterfeit products

- Regulatory gaps and policy inconsistencies

Key Players: BASF SE (Germany), Yara International ASA (Norway), The Mosaic Company (U.S.), Nutrien Ltd. (Canada), Nouryon (Netherlands), Syngenta AG (Switzerland), Bayer AG (Germany), Coromandel International Limited (India), Nufarm (Australia), ICL Group Ltd. (Israel), Haifa Negev Technologies Ltd. (Israel), FMC Corporation (U.S.), Stoller Enterprises, Inc. (U.S.), Valagro (Italy), JR Simplot Company (U.S.), Zuari Agrochemicals Ltd. (India).

Global Agricultural Micronutrients Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.1 billion

- 2026 Market Size: USD 6.6 billion

- Projected Market Size: USD 13.3 billion by 2035

- Growth Forecasts: 9.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.7% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, India, Germany, Brazil

- Emerging Countries: Mexico, Indonesia, Vietnam, Thailand, Philippines

Last updated on : 7 April, 2026

Agricultural Micronutrients Market - Growth Drivers and Challenges

Growth Drivers

- Increase of biofortification for nutritional security: This is one of the distinct drivers for the agricultural micronutrients market for enhancing the nutritional content of staple crops through fertilization. According to official statistics published by NLM in September 2023, more than 2 billion people globally suffer from micronutrient deficiency, constituting a negative impact on socio-economic and health conditions. In this regard, over 21.9% of the population in India resides in extreme poverty with restricted accessibility nutrition resources. Besides, iodine, selenium, and zinc deficiencies are increasingly common, accounting for nearly 15% of selenium, 30% of zinc, and 60% of iron deficiencies. Therefore, biofortification has the suitable capability to eradicate these deficiencies and malnutrition, thus boosting the agricultural micronutrients market exposure.

- Expansion in plant genetic and breeding: The unveiling of stress-tolerant and high-yielding crop varieties has effectively created a parallel need for enhanced nutrition programs, which is uplifting the agricultural micronutrients market globally. As stated in an article published by the World Health Organization (WHO) in February 2025, over 75% of international food crops depend on pollinators, significantly contributing USD 237 billion to USD 577 billion yearly to worldwide agricultural output. Besides, more than 50% of modernized medicines originate from natural sources, including antibiotics from painkillers and fungi from plant compounds. Moreover, forests have the capacity to store 80% of terrestrial biodiversity, which absorbs an estimated 2.6 billion tons of carbon dioxide yearly, thus positively impacting the market expansion.

- Modernization in water irrigation and scarcity: The extension of micro-irrigation systems, including sprinkler and drip networks, is eventually altering application patterns in the agricultural micronutrients market. As per a data report published by the International Commission on Irrigation and Drainage in September 2025, the integration of drip irrigation has led to suitable optimization in water utilization efficiency, along with a significant 2 to 5-fold increase in farm yields. Besides, agriculture effectively consumes a huge portion of available water resources, with India majorly utilizing an estimated 78% for irrigation. Furthermore, conventional open canal systems frequently have resulted to substantial water losses, ranging from 30% to 35%, owing to evaporation and seepage. This has diminished overall water utilization efficiency, which positively contributes to the market upliftment.

Challenges

- Distribution fragmentation and counterfeit products: The agricultural inputs distribution network, particularly in emerging economies, remains highly fragmented and inadequately regulated, creating significant challenges for established manufacturers and farmers in the agricultural micronutrients market. The market is characterized by a long tail of unorganized retailers, many of whom lack formal agronomic training and stock products based on margins rather than scientific merit. This environment fosters the proliferation of counterfeit, substandard, or mislabeled products that claim micronutrient content but deliver little agronomic value. Such products not only defraud farmers but also damage the credibility of the broader micronutrient category when perceived failures occur.

- Regulatory gaps and policy inconsistencies: The regulatory landscape governing the agricultural micronutrients market is often fragmented, inconsistent, and misaligned with the sector’s scientific and commercial realities. In many jurisdictions, micronutrient fertilizers are subject to the same regulatory frameworks as pesticides or macronutrient fertilizers, despite having fundamentally different application profiles, environmental impacts, and safety considerations. This misclassification leads to protracted registration timelines, redundant testing requirements, and disproportionately high compliance costs that stifle innovation and deter new entrants. Moreover, the absence of harmonized standards for product quality, particularly for chelated and complexed formulations, creates ambiguity in the marketplace, allowing inferior products to claim equivalence to advanced technologies.

Agricultural Micronutrients Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.1% |

|

Base Year Market Size (2025) |

USD 6.1 billion |

|

Forecast Year Market Size (2035) |

USD 13.3 billion |

|

Regional Scope |

|

Agricultural Micronutrients Market Segmentation:

End use Segment Analysis

Based on end use, the organic farming segment in the agricultural micronutrients market is expected to account for the largest share of 68.9% by the end of 2035. The segment’s upliftment is highly driven by its importance to international food security, as it enables large-scale, cost-efficient, high-yielding food production. According to official statistics published by NLM in June 2022, the agricultural area usually covers nearly 38% of the worldwide land surface, wherein 1/3rd of this is highly utilized as cropland, and the remaining pastures and meadows readily serve as grazing land. Moreover, agricultural intensification is predicted to increase, owing to the expected surge in the worldwide food production by almost 70% by the end of 2050. Therefore, based on all these developments, there is a huge growth opportunity for organic farming, since it does not use any pesticides or fertilizers.

Form Segment Analysis

The chelated sub-segment, part of the form segment, is anticipated to grab the second-largest share in the agricultural micronutrients market. The sub-segment’s growth is effectively fueled by the aspect of protecting micronutrient ions from being either fixed or rendered insoluble by soil components such as high pH, carbonates, or antagonistic elements. This ensures that nutrients, such as zinc, iron, and manganese, remain stable and readily available for plant uptake, resulting in lower required application rates compared to non-chelated alternatives. The increasing adoption of precision agriculture and fertigation systems, which demand highly soluble and compatible formulations, further accelerates the shift toward chelated products. As farmers seek higher efficiency and return on investment, particularly in high-value horticulture and intensive cereal cultivation, the chelated sub-segment is positioned to maintain its revenue leadership throughout the forecast period.

Type Segment Analysis

By the end of the stipulated timeline, the zinc segment, which is part of the type, is expected to grab the third-largest share in the agricultural micronutrients market. The segment’s development is primarily attributed to its increased requirement for ion transport, enzyme function, and metabolism of plants. As per an article published by Advances in Nutrition in March 2024, approximately 17% of the worldwide population is presently at risk of inadequate zinc consumption, with an increased prevalence of 24% in Africa and 19% in Asia, respectively. Besides, as per the October 2022 NLM article, zinc plays a crucial role as a standard constituent of more than 300 enzymes from all these 6 enzymes, including ligases, oxidoreductases, isomerases, hydrolases, transferases, and lyases, thereby making it suitable for boosting its growth.

Our in-depth analysis of the agricultural micronutrients market includes the following segments:

|

Segment |

Subsegments |

|

End use |

|

|

Form |

|

|

Type |

|

|

Application Method |

|

|

Crop Type |

|

|

Mode of Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Agricultural Micronutrients Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the agricultural micronutrients market is anticipated to grab the highest share of 38.7% by the end of 2035. The market’s upliftment in the region is primarily attributed to critical soil nutrient depletion from intensive farming, focus on staple crop production, a rise in food security concerns, the transition from conventional macronutrient to balanced crop nutrition, and the availability of different soil types. According to official statistics published by the Food and Agriculture Organization in January 2025, 25 million people in the region overcame hunger in 2024 and reduced undernourishment to 6.4% from 7% as of 2023. Besides, the payer’s pricing of healthy diets in the region is expensive, amounting to an average of USD 4.7 in terms of purchasing power parity (PPP) as of 2024, which is extremely higher than USD 4.4 PPP globally. Likewise, East Asia constitutes the highest payer’s pricing, amounting to USD 5.9 PPP every day, thus proliferating the agricultural micronutrients market growth.

The agricultural micronutrients market in China is growing significantly, owing to the upscaling of the massive agricultural base, increased production of grains, a surge in the demand for yield-enhancing inputs, the existence of advanced nutrient management strategies, and generous funding opportunities for soil remediation projects. As per an article published by the State Council Information Office in April 2025, the country witnessed an increase in its grain output, hitting 709 million tons as of 2025, depending on its previous year’s record-high of 706.5 million tons. This particular increase is owing to enhanced efforts for bolstering per unit crop yield on growing enthusiasm and large-scale grain production and planting. Based on this growth, the soybean output in the country grew by 2.5% year on year (YoY) in 2025 to 21.1 million tons, thereby making it suitable for uplifting the market.

The aspects of combining acute soil deficiencies and robust government policy support, along with the widespread deficiencies of iron and boron across cereal-growing states, the promotion of balanced nutrition strategies, and innovation in nano-fertilizers are factors driving the agricultural micronutrients market in India. Based on the government estimates published by the PIB Government in July 2024, the presence of food security programs in the country resulted in accounting for 60.8 million metric tons of food grains, which effectively exceeded the stocking norm of 41.1 million metric tons. Moreover, the National Food Security Act legally entitled almost 75% of the rural population, along with 50% of the urban population, to achieve subsidized food grains through the Targeted Public Distribution System, thereby positively impacting the market growth in the overall nation.

Europe Market Insights

Europe in the agricultural micronutrients market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the intensified focus on balanced crop nutrition, sustainable farming practices, yield optimization, awareness regarding micronutrient deficiencies, and the presence of intensive cultivation. According to official statistics published by the World Economic Forum in April 2022, the aspect of more than 20% farmers adopting climate-smart agriculture can lead to the region diminishing its agricultural greenhouse gas emissions by approximately 6% and optimizing soil health over an area, which is equal to 14% of agricultural land by the end of 2030. In addition, this adoption can also result in improving the livelihoods of farmers by between USD 2.2 billion and USD 10.7 billion every year by the end of the same year, thereby enhancing the agricultural micronutrients market development.

The agricultural micronutrients market in France is gaining increased traction, owing to the presence of the massive agricultural base, diversified cropping systems spanning high-value horticulture, grapes, oilseeds, and cereals, robust awareness of soil nutrient management, and governmental investment programs. Based on government estimates published by the ITA in August 2024, the agri-food sector has generated over USD 07.9 billion in yearly sales, and significantly employed almost 459,803 people. Additionally, the industry comprises nearly 17,372 organizations, with small and medium-sized enterprises (SMEs) constituting about 98% of the sector, while the agricultural sector comprises 759,000 workers. Besides, both industries are readily composed of SMEs, which make up the majority of the industry, thereby denoting an optimistic outlook for the agricultural micronutrients market expansion.

French Industrial Share Analysis of Agri-Food and Agriculture Industry (2022)

|

Sub-Sectors |

Industry Share |

|

Viticulture and Wine |

18.1% |

|

Poultry and Livestock |

10.7% |

|

Dairy Farming |

8.1% |

|

Cereal |

6.9% |

Source: ITA

The convergence of severe soil conditions, intensified horticultural production, robust policy support for sustainable nutrient management, the presence of critical vegetable-producing regions, the expansion of protected cultivation, and the increased focus on high-value crops export are factors driving the agricultural micronutrients market in Spain. As stated in an article published by OEC in March 2026, the country is regarded as the largest exporter of citrus, with a valuation amounting to USD 3.6 billion as of 2024. In addition, the import valuation amounts to USD 229 million, which is deliberately enhancing the market exposure in the overall country. Besides, in terms of grapes, the country’s import valuation is worth USD 217 million and export valuation is USD 537 million. Meanwhile, the country is also considered the top exporter of olives, with a valuation of USD 47.7 million and an import of USD 27.8 million, thereby fueling the market development.

North America Market Insights

North America in the agricultural micronutrients market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by an increase in adopting precision agriculture, a focus on sustainable farming practices, a rise in awareness among farmers regarding deficiencies in soil nutrients, and the shift towards chelated micronutrients. According to official statistics published by the USDA Government in December 2024, there has been an increase in the utilization of harvesters, guidance autosteering systems on tractors, and other equipment by 52% of midsized farms, as well as 70% of large-scale crop-producing farms, as of 2023. Besides, the implementation rates of precision agriculture technologies have significantly increased, with small-scale family farms with gross income less than USD 350,000 being the main users.

Precision Agriculture Technology Utilization Across U.S.-based Farms (2023)

|

Technology Type |

Small-Scale Family Farms |

Midsized Family Farms |

Large-Scale Family Farms |

Nonfamily Farms |

|

Yield Monitors, Maps, or Soil Maps |

13% |

55% |

68% |

55% |

|

Guidance Autosteering |

9% |

52% |

70% |

40% |

|

Variable Rate Technologies |

5% |

32% |

45% |

35% |

|

Drones |

2% |

9% |

12% |

13% |

|

Robotic Milking |

Less than 1% |

6% |

19% |

10% |

|

Wearable Livestock Technologies |

1% |

3% |

12% |

1% |

Source: USDA Government

The agricultural micronutrients market in the U.S. is gaining increased exposure, owing to the adoption of GPS-based variable-rate application systems, drone-driven imagery, and soil sensors to improve input efficiency and enhance yields in wheat, soybean, and corn production, a focus on high-yield row crops, and pressures associated with sustainability and soil depletion. As stated in an article published by NLM in September 2024, the utilization of an agricultural sensor network system with the utilization of optical camera communication (OCC) and drones tends to diminish the overall flight duration by 30%. In addition, with this system, a total of 5,178 images of LED panels have been collected, especially by installing a drone-based camera to provide suitable training to YOLOv5 for detecting objects, thus denoting a huge growth opportunity for the market.

The expansion of pulse and canola crop acreage, suitable governmental support for sustainable agriculture, along with the presence of a short growing season and cold climate, are a few factors that are responsible for bolstering the agricultural micronutrients market in Canada. Based on government estimates published by the Agricultural and Agri-Food Canada in June 2023, the Sustainable Canada Agricultural Partnership is considered the newest USD 3.5 billion and a 5-year deal that has been formed between the territorial, provincial, and federal governments. The purpose was to effectively strengthen the resiliency, innovation, and competitiveness of the agri-based, agri-food, and agricultural products industry. Additionally, the deal also comprises USD 1 billion in federal activities and programs, along with USD 2.5 billion in cost-shared programs, thus fueling the market demand in the country.

Key Agricultural Micronutrients Market Players:

- BASF SE (Germany)

- Yara International ASA (Norway)

- The Mosaic Company (U.S.)

- Nutrien Ltd. (Canada)

- Nouryon (Netherlands)

- Syngenta AG (Switzerland)

- Bayer AG (Germany)

- Coromandel International Limited (India)

- Nufarm (Australia)

- ICL Group Ltd. (Israel)

- Haifa Negev Technologies Ltd. (Israel)

- FMC Corporation (U.S.)

- Stoller Enterprises, Inc. (U.S.)

- Valagro (Italy)

- JR Simplot Company (U.S.)

- Zuari Agrochemicals Ltd. (India)

- ATP Nutrition (Canada)

- Dayal Group (India)

- Kronos Micronutrients (Belgium)

- QC Corporation (U.S.)

- British International Investment plc (BII) (UK)

- Akshayakalpa Organic (India)

- Samunnati Financial Intermediation & Services Private Limited (India)

- Unilever (UK)

- FrieslandCampina (Netherlands)

- IFOAM Organics Europe (Belgium)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF SE has established itself as a leader in the micronutrients space through its advanced chelation technologies and comprehensive crop protection portfolio. The company focuses on integrating micronutrient solutions within its broader sustainable agriculture platform, emphasizing precision application and biological crop enhancement.

- Yara International ASA leverages its deep expertise in crop nutrition to offer a complete range of micronutrient products, often bundled with its signature nitrogen-based fertilizers. The company emphasizes agronomic knowledge transfer and digital farming tools to optimize micronutrient application efficiency across diverse cropping systems.

- The Mosaic Company capitalizes on its extensive phosphate and potash mining operations to incorporate micronutrients into its core fertilizer offerings. The company focuses on developing fortified and coated products that address micronutrient deficiencies while enhancing nutrient use efficiency for large-scale row crop agriculture.

- Nutrien Ltd. operates as an integrated agricultural inputs provider, utilizing its vast retail distribution network to deliver customized micronutrient solutions directly to growers. The company emphasizes crop-specific advisory services and precision agronomy to tailor micronutrient applications to localized soil conditions.

- Nouryon is a key player in the chelated micronutrients segment, supplying high-performance formulations that ensure nutrient stability and bioavailability across varying soil conditions. The company focuses on innovation in biodegradable chelation technologies to align with the growing demand for sustainable and environmentally compatible agricultural inputs.

Here is a list of key players operating in the global market:

The agricultural micronutrients market is moderately consolidated, with a mix of global agrochemical giants and specialized regional players. Besides, BASF, Nutrien, Yara, and Mosaic collectively hold a significant share of the global market, leveraging their extensive distribution networks and integrated crop solution portfolios. The competitive landscape is characterized by a strong shift toward high-value, technologically advanced products. Additionally, to differentiate themselves, market leaders are heavily investing in the development of chelated and controlled-release formulations that offer superior bioavailability and efficiency compared to traditional salts. For instance, in February 2024, British International Investment plc (BII), Akshayakalpa Organic, and Samunnati Financial Intermediation & Services Private Limited signed a MoU to offer financing for almost 1,500 small-scale dairy farmers in India, with BII significantly committing USD 65. Million Climate Innovation Facility, thus driving the agricultural micronutrients industry.

Corporate Landscape of the Agricultural Micronutrients Market:

Recent Developments

- In June 2025, Unilever made expansions in its regenerative agricultural practices across 1 million hectares of agricultural land, which is projected to be achieved by the end of 2030, while implementing this practice across 130,000 hectares globally, and further displayed progress across America, Asia, and Europe.

- In September 2024, FrieslandCampina increased its guaranteed payer’s pricing for organic farm milk to USD 70.1 per 100 kgs, denoting a surge of USD 1.7 in comparison to previous months, based on demonstrating a continuous rise, owing to the growth in market demand.

- In March 2023, IFOAM Organics Europe and Diversified Communications significantly renewed their partnership to make advancements in sustainable growth and innovation in the organic industry, and ensuring collaboration on a wide range of trade events across Europe.

- Report ID: 8504

- Published Date: Apr 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.