5G Infrastructure Market Outlook:

5G Infrastructure Market size was valued at USD 41.6 billion in 2025 and is projected to reach USD 146.2 billion by the end of 2035, rising at a CAGR of 13.4% during the forecast period, 2026-2035. In 2026, the industry size of 5G infrastructure is evaluated at USD 47.1 billion.

The 5G infrastructure market is supported by sustained public-sector investment, spectrum allocation programs, and nationwide connectivity initiatives across major economies. According to the 5G Americas December 2025 data, more than 99% of the U.S. population is covered by at least one 5G provider, reflecting extensive deployment of radio access and backhaul infrastructure across urban and rural regions. Federal support for broadband and advanced wireless networks has also accelerated infrastructure expansion. The National Telecommunications and Information Administration (NTIA) is administering the USD 42.45 billion Broadband Equity, Access, and Deployment (BEAD) Program, which is encouraging network upgrades and fiber deployment that support mobile transport requirements, as per the Congress.gov August 2025 data. In addition, the FCC’s spectrum management initiatives have expanded access to mid-band frequencies that improve network capacity and coverage. These developments are increasing demand for macro cell sites, small cells, fiber backhaul, and network modernization projects.

According to the European Commission's June 2026 data, 5G coverage reached 94% of populated areas in the EU in 2024, up from previous years, demonstrating continued investment in network infrastructure and spectrum utilization. The International Telecommunication Union 2024 data reported that global internet usage exceeded 5.5 billion people in 2024, representing nearly 68% of the world’s population, increasing pressure on operators to expand network capacity and reliability. Government-backed smart manufacturing, transportation modernization, healthcare digitization, and public safety communication programs are contributing to infrastructure spending. As governments pursue connectivity targets and support advanced digital services, demand remains strong for radio equipment, transport networks, edge infrastructure, and network management systems, positioning the market for continued investment across developed and emerging economies.

Key 5G Infrastructure Market Insights Summary:

Regional Highlights:

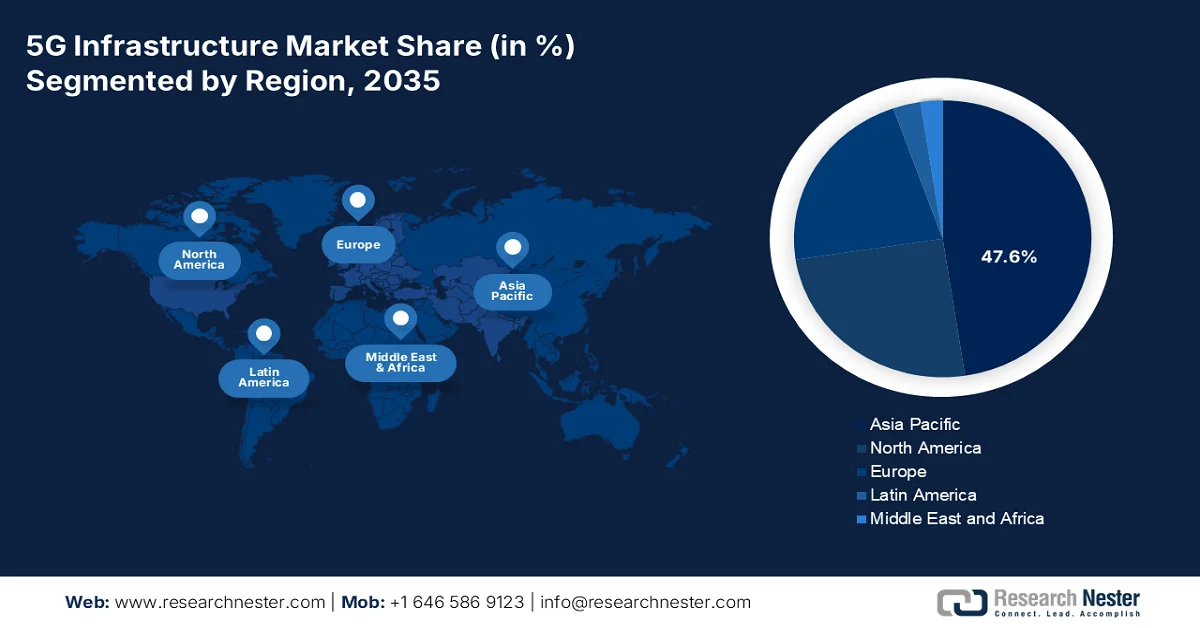

- Asia Pacific is anticipated to capture 47.6% of the 5G infrastructure market revenue by 2035, reinforced by diverse deployment maturity levels, advanced spectrum allocation strategies, and supportive government industrial policies

- North America is set to witness rapid expansion throughout 2026–2035, fueled by aggressive mid-band network densification, strengthened supply chain security initiatives, and accelerating private 5G adoption across industrial sectors

Segment Insights:

- The hardware sub-segment is projected to account for 78.3% of the 5G infrastructure market by 2035, underpinned by extensive investments in new site builds, tower upgrades, and network densification required for 5G coverage

- The mid-band (1–6 GHz) spectrum segment is expected to maintain its leading position through 2035, attributed to its essential role in balancing network coverage and capacity

Key Growth Trends:

- Expansion of public broadband infrastructure programs

- Rising government investment in smart manufacturing

Major Challenges:

- Spectrum licensing and regulatory hurdles

- Interoperability and open RAN standards complexity

Key Players: Huawei (China),Ericsson (Sweden),Nokia (Finland),ZTE (China),Samsung Electronics (South Korea),Cisco Systems (U.S.),Ciena (U.S.),Fujitsu (Japan),NEC Corporation (Japan),Qualcomm (U.S.),Intel (U.S.),Marvell Technology (U.S.),Broadcom (U.S.),Juniper Networks (U.S.),Mavenir (U.S.),Rakuten Symphony (Japan) ,Tech Mahindra (India),Time dotCom (Malaysia) ,Sterlite Technologies (India),D-Link Corporation (Taiwan).

Global 5G Infrastructure Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 41.6 billion

- 2026 Market Size: USD 47.1 billion

- Projected Market Size: USD 146.2 billion by 2035

- Growth Forecasts: 13.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (47.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, South Korea, Japan, Germany

- Emerging Countries: India, Canada, Australia, Saudi Arabia, United Arab Emirates

Last updated on : 10 June, 2026

5G Infrastructure Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of public broadband infrastructure programs: Government-funded broadband expansion initiatives are creating sustained demand for 5G transport networks, fiber backhaul, towers, and edge infrastructure. Public authorities increasingly view high-capacity communications networks as critical economic infrastructure, leading to long-term capital allocation programs that support mobile network deployment. Similarly, Canada’s Universal Broadband Fund has committed over USD 3.225 billion to improve connectivity nationwide, as per the Government of Canada August 2025 data. These investments indirectly stimulate demand for fiber deployment, network densification, and radio access infrastructure required for advanced wireless services. Operators are leveraging publicly funded transport networks to accelerate 5G rollout while reducing deployment costs. As governments prioritize nationwide connectivity, infrastructure vendors, tower companies, and network equipment providers are positioned to benefit from increased procurement activity.

- Rising government investment in smart manufacturing: Industrial digitization programs are increasing demand for private and public 5G infrastructure capable of supporting connected manufacturing facilities. Governments are investing heavily in advanced manufacturing initiatives that require low-latency communications and high-capacity industrial networks. The European Commission allocated approximately USD 8.8 billion under the Digital Europe Programme to accelerate deployment of digital infrastructure, advanced computing, and industrial digital transformation. As manufacturers adopt automation, robotics, predictive maintenance, and industrial IoT applications, demand rises for private 5G networks, edge computing infrastructure, and localized radio deployments. Infrastructure suppliers are increasingly targeting industrial campuses, logistics centers, and production facilities where connectivity requirements exceed the capabilities of legacy wireless systems.

Challenges

- Spectrum licensing and regulatory hurdles: Manufacturers must design equipment that aligns with fragmented global spectrum bands. In India, 5G spectrum auctions saw high reserve prices, delaying entry for local suppliers. Companies had to retune radios for multiple bands. This has become a top barrier for new entrants to cite spectrum.

- Interoperability and open RAN standards complexity: Open RAN promises multi-vendor integration but creates interface mismatches. Top companies faced months of integration delays pairing Fujitsu radios with Nokia cores. Open RAN trials fail initial interoperability tests. Moreover, new suppliers spend some percentage of R&D on compliance testing alone.

5G Infrastructure Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.4% |

|

Base Year Market Size (2025) |

USD 41.6 billion |

|

Forecast Year Market Size (2035) |

USD 146.2 billion |

|

Regional Scope |

|

5G Infrastructure Market Segmentation:

Component Segment Analysis

Within the component segment, the hardware sub segment is leading and is poised to hold the share value of 78.3% by the end of 2035. Hardware encompasses base stations, antennas, small cells, macro cells, routers, switches, and fiber optic cabling. Despite the industry's gradual shift toward software-defined and virtualized networks, hardware remains indispensable because radio signals must be transmitted, received, and amplified through tangible equipment. Massive MIMO antennas, radio units, and fronthaul modules require significant capital investment and physical installation at cell sites. Hardware dominates the component segment due to the sheer volume of new site builds, tower upgrades, and densification required for 5G coverage.

Spectrum Bandwidth Segment Analysis

Under the spectrum bandwidth segment, the mid-band (1–6 GHz) spectrum is the leading sub-segment in the market. the segment is due to its critical role in balancing coverage and capacity. However, a widening gap exists between regional allocations. According to NITA April 2023 data, China wireless operators already have greater mid-band access than the U.S., and China is considering dedicating up to 1,660 megahertz of licensed mid-band spectrum—nearly four times the 450 megahertz available in the U.S. If China allocates the upper half or the entire 6 GHz band for licensed use, it could command either 1,060 or 1,660 MHz of licensed mid-band spectrum. This disparity will drive differential infrastructure investment, with China’s operators deploying dense, high-capacity 5G networks faster.

End user Segment Analysis

In the market, the industrial manufacturing sub-segment leads the end user segment, driven by national rollouts and use case promotion. According to the PIB March 2026 data, 5G services now cover 99.9% of Indian districts, with 5.23 lakh 5G Base Transceiver Stations (BTSs) installed across all States/UTs. The government is undertaking initiatives to promote 5G adoption in smart manufacturing, telemedicine, precision agriculture, and education, while fostering an indigenous 5G ecosystem and strengthening 6G preparedness. This extensive infrastructure enables factories to deploy private 5G networks for real-time automation and predictive maintenance.

Our in-depth analysis of the 5G infrastructure includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Spectrum Brand |

|

|

Architecture |

|

|

Network Type |

|

|

End user |

|

|

Infrastructure Deployment |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

5G Infrastructure Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating and is poised to hold the regional revenue share of 47.6% by the end of 2035. The region is characterized by extreme diversity in deployment maturity, spectrum allocation strategies, and government industrial policies. China leads in mid-band density and standalone 5G adoption, while Japan and South Korea focus on mmWave and 5G-advanced features for urban entertainment and robotics. India has completed a rapid nationwide rollout covering nearly all districts, with emphasis on indigenous manufacturing and telemedicine use cases. Australia and Singapore prioritize Open RAN and supply chain diversification, whereas Indonesia, Malaysia, and the Philippines are in expansion phases targeting metropolitan coverage. Government-backed private 5G networks are growing in manufacturing, ports, and precision agriculture. The region also houses the world's largest 5G equipment manufacturing base. Cross-border spectrum harmonization remains limited.

The extensive network deployment and increasing subscriber adoption are driving the 5G infrastructure market in India. According to the PIB March 2025 data, Government of India, 5G services were available in 99.6% of districts nationwide as of February 2025, demonstrating one of the fastest network rollouts globally. Telecom service providers had installed approximately 469,000 5G Base Transceiver Stations (BTSs) across the country by February 2025, significantly expanding network capacity and coverage. The government’s spectrum auction framework established phased rollout obligations over five years, encouraging continued infrastructure deployment. Additionally, around 250 million mobiles subscribers had adopted 5G services since its launch in October 2022, supporting sustained demand for radio access equipment, fiber backhaul, towers, and network modernization investments.

The large-scale network deployment and rising digital connectivity demand in the 5G infrastructure market in China. According to the People’s Republic of China January 2026 data, China achieved 5G coverage across all towns and more than 95% of administrative villages by the end of 2025, reflecting significant investment in nationwide communications infrastructure. The country also reported 1.204 billion 5G subscriptions out of 1.827 billion mobile subscriptions, making it the world’s largest 5G user base. Furthermore, 5G-Advanced (5G-A) services had expanded to more than 330 cities by 2025, supporting next-generation network capabilities. Growing adoption across industrial, transportation, and public-service applications is driving continued demand for base stations, fiber networks, data centers, and advanced wireless infrastructure.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the market. The region is characterized by aggressive mid-band network densification, strong government focus on supply chain security, and accelerating private 5G adoption across industrial sectors. The United States leads in commercial deployment scale, while Canada emphasizes rural and Indigenous coverage mandates alongside spectrum auction buildout obligations. Both nations have implemented vendor restriction policies excluding high-risk equipment suppliers, creating opportunities for Open RAN alternatives. Government funding programs support defense-based 5G trials, smart manufacturing, and edge computing node deployment. The market is transitioning from non-standalone to standalone 5G architectures, enabling network slicing for enterprise customers. Private 5G licenses are increasingly sought by logistics, port, and manufacturing operators seeking deterministic low-latency connectivity.

The rapid subscriber adoption and increasing network capacity requirements is shaping the 5G infrastructure market in the U.S. According to 5G Americas April 2023 data, U.S. recorded approximately 108 million 5G connections by Q3 2022, with 5G penetration approaching 30% of the region’s population, reflecting strong demand for advanced wireless services. The region added nearly 14 million new 5G connections in a single quarter, demonstrating continued network expansion. Globally, mobile data traffic reached 90 exabytes per month in 2022 and was growing by about 40% annually, increasing pressure on operators to expand spectrum utilization, deploy additional base stations, and enhance backhaul infrastructure. This growth is supporting sustained investment in U.S. radio access networks, fiber connectivity, and mid-band spectrum deployments.

The large-scale government investment in nationwide broadband expansion, which is strengthening the foundation for advanced wireless network deployment is driving the market in Canada. According to the Government of Canada March 2023 data, approximately 93.5% of Canadian households had access to high-speed Internet services by 2024, up from 79%, reflecting substantial progress in connectivity infrastructure. The federal government has made USD 7.6 billion available for connectivity improvements, supported by the Universal Broadband Fund and other federal and provincial programs. These investments have helped extend high-speed internet access to roughly 2.2 million additional homes, creating opportunities for further deployment of fiber backhaul, network densification, and 5G infrastructure across both urban and rural regions.

Europe Market Insights

The market in Europe is characterized by fragmented spectrum harmonization efforts across member states, strong government backing for Open RAN deployment to reduce vendor concentration, and significant funding for cross-border 5G corridors. The European Commission promotes multi-vendor interoperability through its RISE initiative and 5G for Smart Communities program. National regulators in Germany, France, Italy, and Spain have conducted mid-band auctions with coverage obligations for rural and transport routes. Private 5G networks are rapidly expanding in automotive manufacturing, ports, and logistics hubs, often co-funded by national recovery plans. Security-related vendor restrictions vary by country, creating a non-uniform procurement landscape. Edge computing node deployment is concentrated in industrial clusters.

The rapid network expansion and continued investment in standalone 5G capabilities is shaping the 5G infrastructure market in Germany. According to the Bundesnetzagentur June 2024 data, 92% of Germany’s population received 5G coverage from at least one network operator as of April 2024, demonstrating substantial progress in nationwide deployment. In addition, 5G Standalone (5G SA) coverage reached 90%, a significant milestone considering that no 5G SA coverage was reported when measurements began in October 2021. During the same period, overall 5G coverage increased from 53% to 92%, reflecting an expansion of nearly 40 percentage points. These developments are driving demand for advanced radio access networks, fiber backhaul infrastructure, cloud-based network architecture, and standalone core network investments across Germany.

The targeted government initiatives aimed at expanding advanced wireless connectivity nationwide is shaping the 5G infrastructure market in the UK. The UK Government's April 2023 data, under the UK Wireless Infrastructure Strategy, the government has established an ambition to achieve nationwide standalone 5G coverage across all populated areas by 2030, creating long-term opportunities for network deployment and modernization. To accelerate adoption, the government has also committed £40 million for 5G Innovation Regions, supporting the implementation of 5G-enabled applications across public-sector services and industrial environments. The strategy further promotes advanced connectivity in healthcare facilities and regional digital projects, encouraging additional investment in network infrastructure. These initiatives are driving demand for radio access equipment, fiber backhaul networks, standalone 5G core systems, and edge computing capabilities across the UK.

Key 5G Infrastructure Market Players:

- Huawei (China)

- Ericsson (Sweden)

- Nokia (Finland)

- ZTE (China)

- Samsung Electronics (South Korea)

- Cisco Systems (U.S.)

- Ciena (U.S.)

- Fujitsu (Japan)

- NEC Corporation (Japan)

- Qualcomm (U.S.)

- Intel (U.S.)

- Marvell Technology (U.S.)

- Broadcom (U.S.)

- Juniper Networks (U.S.)

- Mavenir (U.S.)

- Rakuten Symphony (Japan)

- Tech Mahindra (India)

- Time dotCom (Malaysia)

- Sterlite Technologies (India)

- D-Link Corporation (Taiwan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Huawei is the leading player in the 5G infrastructure market and has leveraged ultra-low latency and high-bandwidth networks to enable real-time transmission of high-resolution ECG data from wearable patches to cloud-based AI diagnostic platforms. In 2024, the company has made a revenue of USD 118,162 million.

- Ericsson is the top player in the market and has deployed 5G radio access and edge computing technologies that facilitate seamless, low-power mobile cardiac telemetry. Its Ericsson Connected Health framework uses 5G standalone architecture to prioritize uplink traffic from ambulatory cardiac monitors, ensuring drop-free transmission during patient movement.

- Nokia’s contribution in the market includes its 5G Fixed Wireless Access and Edge Cloud platforms, which support continuous remote cardiac monitoring with sub-10ms latency. Nokia’s industrial-grade 5G small cells, deployed in community health centers, securely aggregate data from multiple wireless ECG sensors.

- ZTE is the leading player in the 5G infrastructure market and has introduced ultra-reliable low-latency communication (URLLC) features in its 5G base stations to support mobile cardiac telemetry. ZTE’s 5G network-in-a-box solutions enable pop-up cardiac monitoring units in remote or disaster-prone areas. In 2024, the company has made a revenue of USD 4.25 billion

- Samsung Electronics, active in the market through its 5G vRAN and chipset solutions, enables low-power, miniaturized cardiac telemetry devices. Its Exynos-modem-integrated 5G modules are embedded in wearable ECG patches, offering continuous ambulatory monitoring with beamforming-enhanced connectivity.

Here is a list of key players operating in the global market:

The global 5G infrastructure market is highly concentrated, led by Chinese giants Huawei and ZTE, though Western security concerns have opened doors for Ericsson and Nokia. Key players are pursuing strategic initiatives such as Open RAN (O-RAN) deployments to reduce vendor lock-in, massive MIMO advancements, and private 5G networks for industrial automation. For example, in April 2026, Amazon’s announced the acquisition of Globalstar. U.S. and Europe vendors focus on cybersecurity and interoperability, while South Korea and Japan firms excel in components and small cells. Manufacturers in India and Malaysia are emerging in network software and radio units. Mergers, patent cross-licensing, and government-backed 5G rollouts remain critical competitive levers.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, Broadcom Inc. announced its collaboration with Samsung Electronics Co., Ltd. on a new, broadband-optimized reference platform for the global fixed wireless access (FWA) market, integrating Broadcom's BCM6776 Wi-Fi 8 System-on-Chip (SoC) with Samsung's B1320 5G Modem.

- In April 2026, Ericsson and Freshwave announced the launch of the next evolution of indoor 5G in the UK. UK organizations expecting assured indoor 5G connectivity from all the mobile network operators, a more energy-efficient choice with 5G on Omni.

- In April 2026, Siemens has expanded its industrial-grade private 5G infrastructure to the U.S. and seven additional countries. The expansion is enabled by two new radio units covering the 3.8–4.2 GHz band and the US-specific CBRS band, bringing the solution to a total of 15 countries across Europe and the Americas.

- Report ID: 8130

- Published Date: Jun 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.