Urinary Tract Infection Testing Market Outlook:

Urinary Tract Infection Testing Market size was over USD 1.4 billion in 2025 and is estimated to reach USD 2.4 billion by the end of 2035, expanding at a CAGR of 6.5% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of urinary tract infection testing is evaluated at USD 1.4 billion.

The growing occurrence and severity of urinary tract infections (UTIs) are creating a surge in efficient diagnostic services and products. According to a 2025 NLM study, the number of people visiting health services for this condition every year reached 3 million. It also predicted the global incidence rate, prevalence, and disability-adjusted life year (DALY) rates per 100 thousand population to be 6,486.3, 127.5, and 93.3, respectively, by 2050. Besides, the study concluded the count of incident and prevalent cases of UTIs worldwide to be 652.8 million and 12.4 million by the end of 2050, showcasing a 43.5% and 43.7% rise from 2022. The demography of the market is further expanding with the rapid aging and increasing incidence of chronic ailments.

The equal distribution and wide accessibility in the market highly depend on the reliability of the supply chain and production capacity of detection tools and their key component. However, the intense concentration of manufacturing essential reagents and instruments within a concise region often creates volatility in payers’ pricing in this sector due to its reliance on imports. This further translates to financial exhaustion among both patients and service providers. Testifying to such an economic burden, in 2023, the NLM conducted a study on urine testing for emergency hospital admissions, which unveiled that the total annual expense on urinalysis accounted for $8,490.6 and $49,701.0 direct and total costs. Thus, companies are now engaged in developing affordable and value-based testing models.

Key Urinary Tract Infection Testing Market Insights Summary:

Regional Highlights:

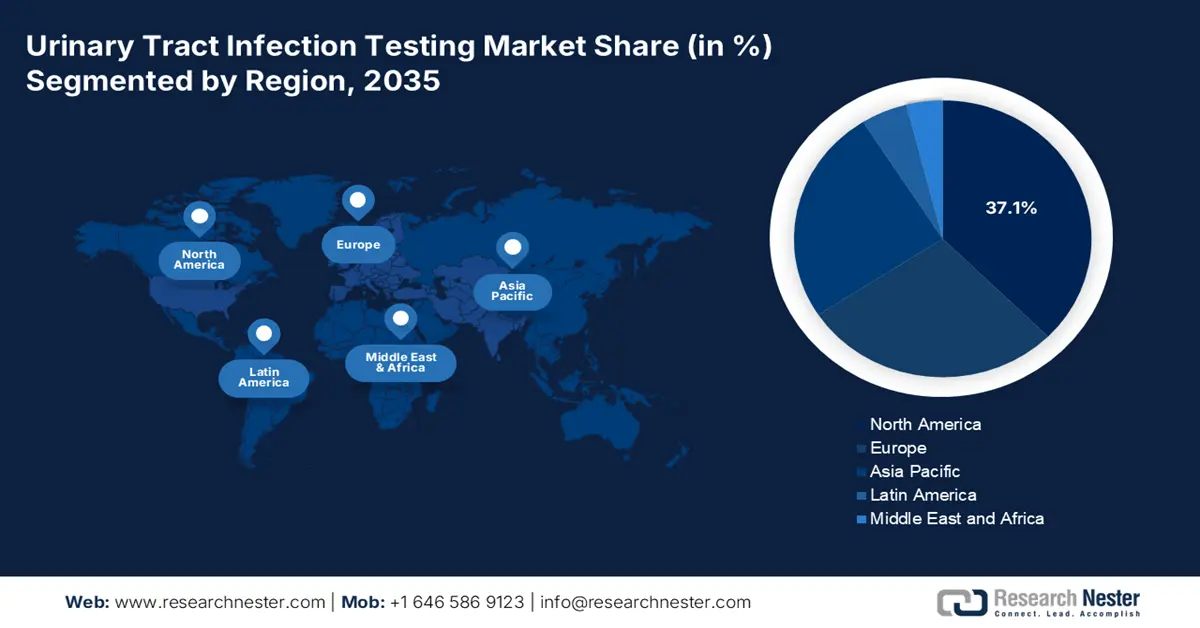

- By 2035, North America in the urinary tract infection testing market is anticipated to secure a 37.1% share, upheld by a robust healthcare system.

- Asia Pacific is projected to be the fastest-growing region during 2026-2035, bolstered by rapid development in healthcare infrastructure.

Segment Insights:

- By 2035, the hospitals segment in the urinary tract infection testing market is set to hold a 52.6% share, propelled by high patient volume.

- The laboratory-based devices segment is projected to capture a 42.8% share by 2035, impelled by the need for sophisticated analysis.

Key Growth Trends:

- Growing trend of early detection and prevention

- Advancements in diagnostic technologies

Major Challenges:

- Prolonged and expensive compliance process

- Strict reimbursement and price control policies

Key Players: Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers, Danaher Corp. (Beckman Coulter, Cepheid), BD (Becton, Dickinson and Company), bioMérieux SA, Thermo Fisher Scientific Inc., QuidelOrtho Corporation, Cardinal Health, McKesson Corporation, Trivitron Healthcare, 77 Elektronika Kft., ACON Laboratories, Inc., RENALYS, SD BIOSENSOR, Inc., Lupin Limited, PathogenDx, Mankind Pharma.

Global Urinary Tract Infection Testing Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.4 billion

- 2026 Market Size: USD 1.4 billion

- Projected Market Size: USD 2.4 billion by 2035

- Growth Forecasts: 6.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (37.1% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Canada, Germany, United Kingdom, China

- Emerging Countries: India, Brazil, South Korea, Singapore, Australia

Last updated on : 29 August, 2025

Urinary Tract Infection Testing Market - Growth Drivers and Challenges

Growth Drivers

- Growing trend of early detection and prevention: As patients become more informed about symptoms, such as frequent urination, burning sensation, and pelvic pain, the volume of doctor visits and proactive testing for UTIs is amplifying. Early-stage diagnosis not only helps prevent complicated kidney infections but also minimizes antibiotic misuse. Testifying to the need, a 2025 NLM study revealed that even 1 day of delay in diagnosis and prescription filling added over $1.6 thousand in health plan spending to treat UTI. It also mentioned that on the day of testing can reduce treatment costs by 40%. This is pushing both healthcare providers and afflicted individuals to invest in the market.

- Advancements in diagnostic technologies: Recent advances in associated tools, such as molecular testing, PCR-based assays, and point-of-care devices, are revolutionizing the market. These technologies are gaining traction in this field through their faster turnaround times, higher sensitivity, and better accuracy compared to traditional urine cultures, which is influencing companies to invest more in innovation. Following the same pathway, in December 2023, Siemens Healthineers launched its compact Analyzer for urine sediment assessments, the Atellica UAS 60. It can automate the workflow in labs by enabling full-field-of-view digital imaging, allowing professionals to analyze results rapidly and accurately.

- Government and institutional backing and activity: Government and academic institutions are increasingly showing interest in R&D for the market to control and combat the widespread UTI epidemiology more effectively. Particularly, the enlarging vulnerable populations are pushing them to cultivate sufficient supplies for early detection, which is ultimately helping the sector expand its pipelines with stable capital influx. For instance, till 2025, Astek Diagnostics garnered a total of $2.3 million in non-dilutive grant funding from public investors, including NSF, FDA, and NIH, for developing a one-hour point-of-care UTI detection and antibiotic sensitivity indication system.

Historic Trends in the Primary Patient Pool of the Urinary Tract Infection Testing Market

Analysis of Global Burden Shifts in the UTI Patient Pool (1990-2021)

|

Indicator |

2021 Statistics |

Change / Notes |

|

Total Number of Cases |

4,491,022,288 |

66.4% increase |

|

ASIR (per 100,000 population) |

5,531.8 |

EAPC: 0.1 |

|

ASPR (per 100,000 population) |

105.3 |

EAPC: 0.1 |

|

Deaths (No. of Cases) |

300,112 |

190% increase from 1990 |

|

ASDR (per 100,000 population) |

3.7 |

EAPC: 1.0 |

|

ASDAR (per 100,000 population) |

83.7 |

EAPC: 0.4 |

Source: NLM

Legend:

- ASIR: Age-Standardized Incidence Rate

- ASPR: Age-Standardized Prevalence Rate

- ASDR: Age-Standardized Death Rate

- DALYs: Disability-Adjusted Life Years

- ASDAR: Age-Standardized DALY Rate

- EAPC: Estimated Annual Percentage Change

Cost Distribution/Cost Analysis Related to Specified Testing Methods from the market

Direct Costs Associated with Urine Testing (2023)

|

Supplies |

Direct cost/unit |

|

Urinalysis cup |

$0.24 |

|

Urinalysis with micro supplies |

$1.00 (estimate) |

|

Culture plate and single-use inoculating loop |

$0.71 |

|

Organism identification via mass spectroscopy supplies |

$0.95 |

|

Organism susceptibility via VITEK-2 |

$3.78 |

Source: NLM

Challenges

- Prolonged and expensive compliance process: The procedure of obtaining an allowance from certification authorities often becomes a major hurdle for widespread commercialization in the market. Particularly, for novel Class II and III IVD devices, different standardization criteria of various regulatory bodies cause delays in product launch. This ultimately translates to notable financial and brand reputation losses by creating uncertainty in submission processes and increasing upfront compliance costs.

- Strict reimbursement and price control policies: With the growing trend of value-based healthcare models, the threshold of cost-effectiveness for financial backing is shrinking. This may restrict the product’s ability to enable public reimbursement in the urinary tract infection testing market. Additionally, such pricing controls make hospitals and labs reluctant to adopt new testing technologies, regardless of their clinical utility, limiting the scope of securing greater profit margins. This consequently discourages manufacturers from participating in this sector.

Urinary Tract Infection Testing Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.5% |

|

Base Year Market Size (2025) |

USD 1.4 billion |

|

Forecast Year Market Size (2035) |

USD 2.4 billion |

|

Regional Scope |

|

Urinary Tract Infection Testing Market Segmentation:

End user Segment Analysis

Hospitals are expected to maintain their position as the primary end-user in the market with a share of 52.6% over the assessed period. High patient volume of these facilities is propelling demand for comprehensive laboratory capabilities and rapid, accurate diagnostics to guide antibiotic stewardship programs. Besides, the increasing number of complex and postoperative UTI cases amplifies the demographic volume in hospitals. According to a 2025 Journal of European Urology Focus, more than 40% of the hospital-associated infections are UTIs. This underscores the importance of diagnosis as a fundamental action to improve patient care and combat resistance in hospitals, cementing the segment’s leadership in this sector.

Product Type Segment Analysis

The laboratory-based devices segment is poised to show dominance over the urinary tract infection testing market by capturing a share of 42.8% by the end of 2035. The proprietorship is empowered by the essentiality of these components in fetching high accuracy and sensitivity to perform antimicrobial susceptibility testing (AST). Besides, the ongoing trend of automating laboratory instruments and molecular platforms is accounting for a greater revenue generation in this sector. Moreover, the need for sophisticated analysis, definitive diagnosis, and guidance for targeted therapy positions laboratory-based devices at the forefront of the list of expenditures for UTI testing.

Test Type Segment Analysis

Urinalysis is predicted to remain the dominant method used in the market till the end of the analyzed tenure. Widespread availability, cost-effectiveness, and ease of use are the major growth factors behind the segment’s notable augmentation in this sector. On the other hand, urinalysis is considered to be the most suitable option for initial UTI screening, which directs to majority of cash inflow in this category. Furthermore, the effective characteristics of this method make urinalysis the gold standard for hospitals, clinics, and even home care settings.

Our in-depth analysis of the global market includes the following segments:

|

Segment |

Subsegment |

|

Product Type |

|

|

Test Type |

|

|

Application |

|

|

End user |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Urinary Tract Infection Testing Market - Regional Analysis

North America Market Insights

North America is anticipated to secure the highest share of 37.1% in the global urinary tract infection testing market during the discussed timeframe. The robust healthcare system, high disease awareness, and robust diagnostic capabilities are the foundational pillars of this landscape. The region has a large patient pool of UTI, majorly containing women, the elderly, and catheterized patients, contributing to steady demand for accurate and rapid testing solutions. As evidence, in a 2022 article, the NLM unveiled that UTI had a 2.3% mortality rate for hospitalized patients in the U.S., where the medical cost of this condition ranged between $340 million and 450 million every year. Further, strict regulations for HAIs, the presence of global MedTech leaders, and ongoing R&D activities fuel the landscape.

The U.S. is the leading contributor to the North America market, owing to intense disease occurrence, advanced diagnostic infrastructure, and strong focus on preventative healthcare. The country is also home to globally leading medical research institutions, which makes the U.S. an epitome of innovation in this category. Exemplifying the same, in May 2023, Researchers at The University of Texas at Dallas introduced a new prototype diagnostic sensor that shortens the result time in UTI detection. The component is capable of delivering 85% accuracy, without having to wait 24 to 48 hours for lab test results.

Canada also plays a prominent role in the regional expansion of the market. It is augmenting the sector in support of the rising awareness about urinary health and a growing geriatric population. Complementing the demographic enlargement, government initiatives aimed at improving infection control and elderly care are further driving adoption in this field. Evidencing the same, the 2021 healthcare budget of Canada allocated $3 billion over the next five years to deploy adequate preventive measures and healthcare standards for long-term care to combat infectious epidemics.

APAC Market Insights

Asia Pacific is expected to be recognized as the fastest-growing region in the global urinary tract infection testing market over the analyzed tenure. Rapid development in healthcare infrastructure and an increasing volume of afflicted patients are cumulatively establishing a sustainable consumer base for UTI diagnosis and management. The increasing occurrence, particularly among densely populated countries such as India and China, is fueling demand for reliable and affordable diagnostic solutions. Furthermore, the notable expansion in the network of diagnostic laboratories, increasing adoption of point-of-care testing, and government efforts to improve infection control standards are major growth factors in this field.

China is a key driver in the Asia Pacific urinary tract infection testing market, which is primarily fueled by its large population, increasing healthcare investments, and excellence in medical device manufacturing. On the other hand, rapid centralization of the national medical system and innovation in affordable UTI testing solutions expanded patient access in this sector. Government efforts to enhance infection prevention and control, along with growing public awareness about urinary health, are further encouraging early diagnosis and treatment for this condition. As a result, China presents lucrative opportunities for both domestic and international diagnostic companies operating in this field.

India is emerging as the epicenter of growth in the APAC urinary tract infection testing market. High occurrence and mortality rates of UTIs, coupled with public awareness initiatives, are enlarging the consumer base in this sector. Besides, the robust expansion of the home-healthcare industry, which is exhibiting a remarkable CAGR of 19%, is propelling demand for point-of-care medical devices. Besides, in 2022, the government of India proposed INR 2.05 trillion budget for smart city developments and technological advancements, benefiting this merchandise with a progressive atmosphere.

Country-wise UTI Patient Pool Trends

|

Analyzed Region |

Metric |

Numbers/Notes |

Year |

|

China |

Age-standardised incidence rate (ASIR) |

1,184.1 |

2021 |

|

North India |

Culture-positive rate for UTI in symptomatic patients |

77.9% |

2022 |

|

Australia |

Proportion of UTI afflicted residents |

10% of women and 5% of men aged >65 years |

2021-2022 |

Source: NLM, Frontiers, and AJGP

Europe Market Insights

Europe is estimated to augment steadily in the global urinary tract infection testing market during the timeline between 2026 and 2035. The rapidly aging populations and strict infection control protocols are collectively widening the consumer base. It is also progressing with the amplified scale of R&D and commercialization of cutting-edge testing technologies, including molecular diagnostics and automated urinalysis systems. This cohort is empowered by the presence of global MedTech pioneers, focusing on product pipeline expansion. Furthermore, government initiatives focused on antimicrobial resistance and infection control are promoting innovation in this category.

The UK is strongly propagating the Europe market, which is backed by a high UTI incidence rate and government efforts to combat such widespread. The National Health Service (NHS) plays a vital role in promoting routine diagnostic practices, particularly among vulnerable groups such as elderly citizens and patients in long-term care. In this regard, the UK Health Security Agency (UKHSA) unveiled that hospital stays, with UTI being the primary diagnosis, across the nation accounted for more than £604 million expenditure from 2023 to 2024. Moreover, with the amplifying capital influx in diagnostic technologies and digital health infrastructure, the UK continues to support the expansion of this sector.

Germany leads the regional urinary tract infection testing market, which is accomplished through its state-of-the-art healthcare system, high diagnostic standards, and strict regulations on infection control measures. The country experiences a substantial number of UTI cases every year, particularly among women and elderly patients. Thus, with a projected geriatric population (aged 65 and over) of 24 million by 2050, the country presents a great potential to garner profitable revenue in this sector. Additionally, ongoing investments in diagnostic innovation and the presence of key medical technology firms are boosting capabilities of Germany in this landscape.

Country-wise UTI Patient Pool Dynamics

|

Country |

Metric |

Numbers/Notes |

Year |

|

UK |

Hospital Admissions |

189,756 |

2023-2024 |

|

Germany |

Proportion of UTI in total HAI |

19.0% |

2022 |

|

Switzerland |

Incidence rate of catheter-associated UTI |

Increased from 0.9 to 1.5 per 1,000 catheter days |

2021-2023 |

Source: GOV.UK, NLM, and FOPH

Key Urinary Tract Infection Testing Market Players:

- Abbott Laboratories

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers

- Danaher Corp. (Beckman Coulter, Cepheid)

- BD (Becton, Dickinson and Company)

- bioMérieux SA

- Thermo Fisher Scientific Inc.

- QuidelOrtho Corporation

- Cardinal Health

- McKesson Corporation

- Trivitron Healthcare

- 77 Elektronika Kft.

- ACON Laboratories, Inc.

- RENALYS

- SD BIOSENSOR, Inc.

- Lupin Limited

- PathogenDx

- Mankind Pharma

The commercial dynamics of the market are becoming intensely competitive, where both established pioneers and new entrants are progressing with innovative and user-centric solutions. Exemplifying the same, Vivoo launched its at-home smart UTI test kit and mobile application at the CES 2024, which marked a notable step toward advances in digital, consumer-friendly diagnostics in this category. The tool utilizes a deep learning-assisted image processing algorithm to scan and review test results with the Vivoo app. Such a strategy underscores the potential of this sector in greater revenue generation from AI and IoT integration in the existing pipeline.

Here is a list of key players operating in the global market:

Recent Developments

- In September 2024, Mankind launched its new range of diagnostic products, RAPID NEWS self-test kits, which are designed to address prevalent health issues, including urinary tract infections (UTIs). This signifies the company’s remarkable progress towards accessible and affordable healthcare.

- In June 2024, PathogenDx introduced a fast multiplexed testing solution, D3 Array-UTI, for urinary pathogen detection run simultaneously with antibiotic resistance gene markers. This UTI assay provides a scalable, low-cost solution in a single test with results in under 6.5 hours.

- Report ID: 8040

- Published Date: Aug 29, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.