Swarm Robotics Market Outlook:

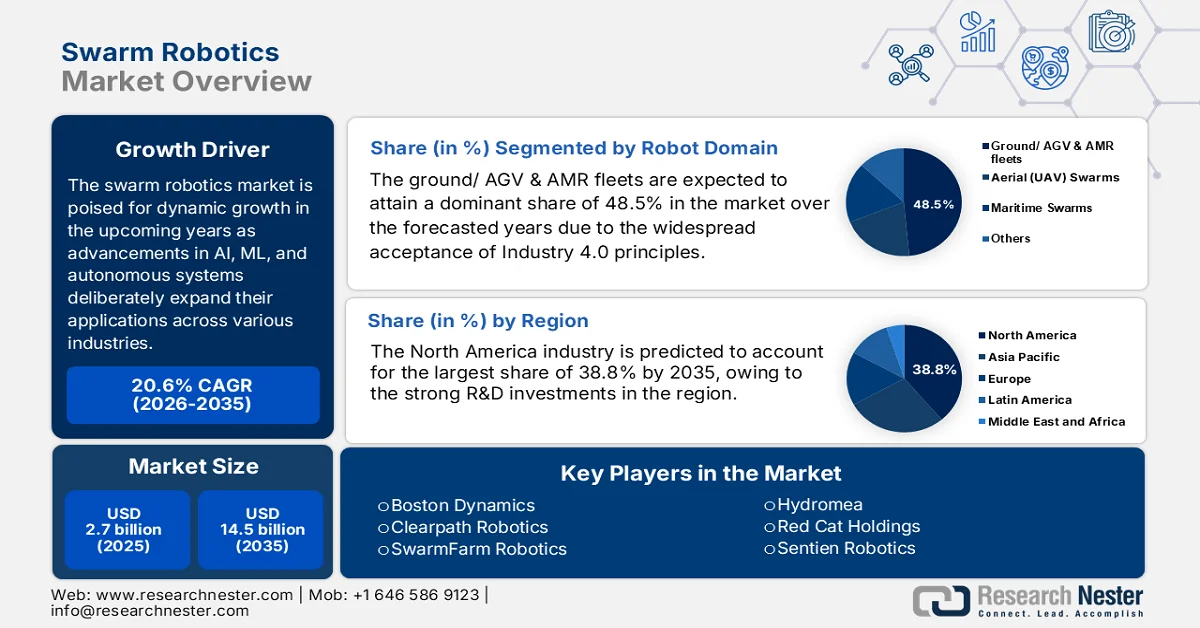

Swarm Robotics Market size was valued at USD 2.7 billion in 2025 and is projected to reach USD 14.5 billion by the end of 2035, rising at a CAGR of 20.6% during the forecast period, i.e., 2026-2035. In 2026, the industry size of swarm robotics is evaluated at USD 3.2 billion.

The market is poised for dynamic growth in the upcoming years as advancements in AI, ML, and autonomous systems deliberately expand their applications across various industries. Based on the officially reported data from NASA Technical Reports Server, the Starling swarm, which was launched in July 2023 under NASA’s Small Spacecraft Technology program, successfully showcased swarm robotics technologies using four 6U CubeSats. The mission tested decentralized Mobile Ad-Hoc Networking, autonomous onboard decision-making, optical-based navigation, and autonomous maneuver planning, thereby enabling coordinated operations without any direct ground control. In this context, results showed successful network establishment, consensus-based observation planning, multi-spacecraft optical navigation, and autonomous formation maintenance, improving the capabilities for future large-scale satellite swarms.

Furthermore, ongoing research & development accelerate and commercialization progresses, wherein the market is expected to redefine operational processes, optimize, and drive innovation across both industrial and service-oriented sectors. USDA officially reported that the CASS project, which is being led by West Texas A&M University and funded by the USDA National Institute of Food and Agriculture with a total of USD 1,000,000, 2021 to 2026, is developing a configurable, adaptive, and scalable swarm of 25 robots, i.e., 15 ground, 10 aerials, for collaborative smart agriculture. Besides, the system integrates a mobile ad-hoc network (MANET), swarm decision-making, and a digital twin to enable autonomous field scouting, weed management, and livestock monitoring. Moreover, in this project, two real-world case studies were focused on cotton and peanut field management and beef cattle behavior detection, hence increasing the growth potential of the market.

Key Swarm Robotics Market Insights Summary:

Regional Highlights:

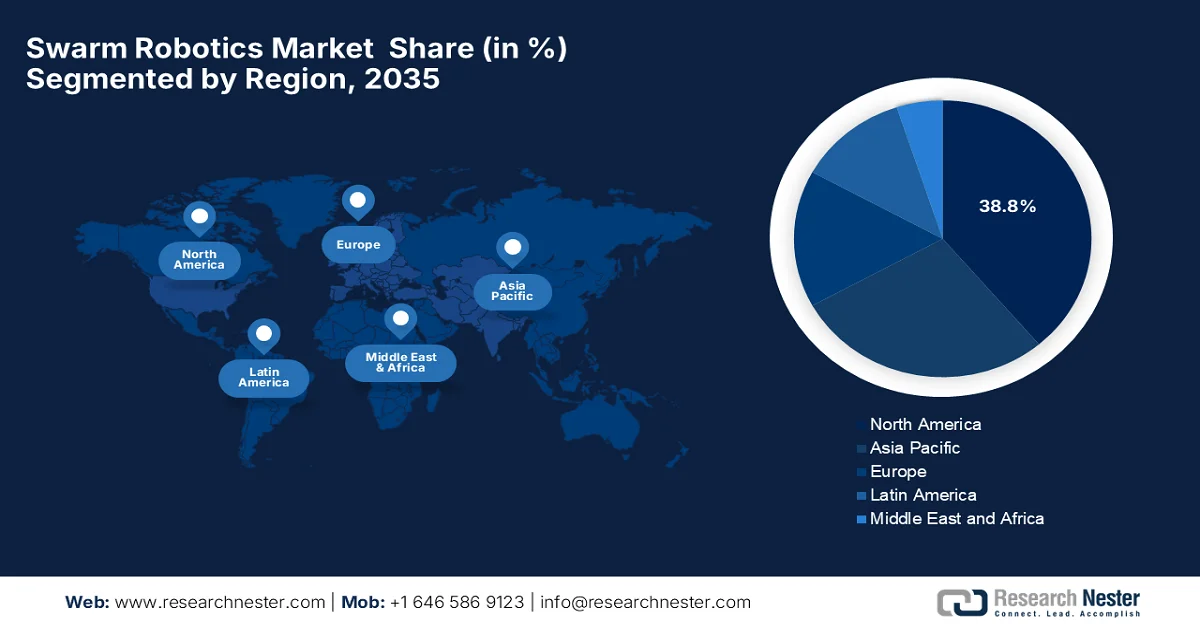

- By 2035, North America is projected to command 38.8% of revenue in the swarm robotics market, attributed to advanced defense applications, logistics automation, and robust R&D investments in autonomous and swarm robotics.

- Asia Pacific is poised to witness the fastest expansion in the swarm robotics market through 2035, fueled by rapid industrial automation, smart city initiatives, and large-scale manufacturing ecosystems.

Segment Insights:

- The ground/ AGV & AMR fleets segment is forecasted to secure a leading 48.5% share by 2035 in the swarm robotics market, propelled by widespread adoption of Industry 4.0 and heightened emphasis on smart manufacturing and logistics environments.

- The logistics & warehousing application segment is anticipated to expand at a considerable pace by 2035, stimulated by rising demand for efficient supply chain management and increasing complexity of large-scale inventory handling.

Key Growth Trends:

- Rising demand for automation across industries

- Smart manufacturing & industry 4.0 initiatives in parallel

Major Challenges:

- Technical complexity and coordination

- Communication and network reliability

Key Players: Boston Dynamics (U.S.), Clearpath Robotics (Canada), SwarmFarm Robotics (Australia), DJI Innovations (China), Hydromea (Switzerland), Red Cat Holdings (U.S.), Sentien Robotics (U.S.), Blue River Technology (U.S.), GreyOrange (India), ABB Ltd. (Switzerland), KUKA AG (Germany), Siemens AG (Germany), Omron Corporation (Japan), iRobot Corporation (U.S.), Locus Robotics (U.S.), Exyn Technologies (U.S.), Swarm Systems Limited (UK), Icarus Drone (U.S.), K-Team Corporation (Switzerland).

Global Swarm Robotics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.7 billion

- 2026 Market Size: USD 3.2 billion

- Projected Market Size: USD 14.5 billion by 2035

- Growth Forecasts: 20.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Canada, United Kingdom, France, Australia

Last updated on : 16 February, 2026

Swarm Robotics Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand for automation across industries: The adoption of automation in sectors such as manufacturing, logistics, agriculture, healthcare, and defense is progressing to boost productivity and operational efficiency. In this context, swarm robotics, which is enabling coordinated work by multiple robots, fits very well into this trend, enhancing the uptake of the swarm robotics market. In November 2024, the U.S. Defense Innovation Unit reported that it awarded contracts under the replicator initiative to develop software for collaborative autonomy and resilient command-and-control of large fleets of autonomous systems. It also notes that the autonomous collaborative teaming program enables coordinated operation of swarms of many uncrewed assets across different domains, enhancing lethality and system-of-systems interoperability. These efforts, which have the involvement of multiple government components, reflect the accelerated heterogeneous swarm robotics capabilities and scalable autonomous collaboration across the joint force.

- Smart manufacturing & industry 4.0 initiatives in parallel: The move toward smart factories with the capabilities of IoT, data analytics, and edge computing is deliberately boosting demand in the market. These systems help streamline production and real-time adaptability in complex manufacturing environments. As of November 2025, based on the government data from China, the country has established more than 7,000 advanced smart factories, becoming the world’s largest intelligent manufacturing base. Besides, the government has implemented a tiered cultivation system, identifying more than 500 excellence-level factories and 15 pioneer-level enterprises to drive technological maturity and integration. In addition, these smart factories leverage IoT, industrial software, and automation, with a prime focus to enhance efficiency and adaptability, denoting a strong potential for the market to grow in the upcoming years.

- Adoption in defense and surveillance: The drone swarms have gained enhanced exposure in various defense applications, from surveillance to reconnaissance, accelerating the growth of the swarm robotics market. In April 2025, the UK Ministry of Defense announced a successful trial where British soldiers made use of a radiofrequency directed energy weapon (RF DEW) to defeat swarms of drones in West Wales. It is a £40 million (USD 51 million) government-backed project, which was led by Defense Equipment & Support and the Defense Science and Technology Laboratory with Thales UK, marking the largest counter-drone swarm exercise conducted by the British Army. Furthermore, it is capable of neutralizing multiple drones instantly at low cost, hence strengthening the layered air defense and making it suitable for market growth and development.

Challenges

- Technical complexity and coordination: The swarm robotics are dependent on multiple operating agents that operate collectively, posing considerable technical challenges. Also, each robot needs to sense, communicate, and make decisions in real time by efficiently maintaining synchronization with the swarm. Therefore, ensuring proper coordination between heterogeneous platforms is very challenging since there are differences in hardware, software, and communication protocols. Any type of signal interference or sensor errors, latency can result in collisions or failure in the mission undertaken. In addition, scaling from small experimental swarms to large operational deployments multiplies these challenges, making system validation and robustness critical hurdles for both commercial and defense applications in the swarm robotics market.

- Communication and network reliability: This aspect also causes a hindrance to market expansion since proper operation depends on continuous and secure communication between robots and the ground station. The wireless networks in the battlefield, underwater, or urban environments are prone to jamming, interference, and signal loss, which can lead to disruptions in proper coordination. Also, designing a robust mesh or network to allow the swarm continue operations in such conditions is technically demanding, which most manufacturers can’t adopt for. Heterogeneous swarms combining aerial, ground, and marine robots exacerbate these communication challenges. Furthermore, ensuring high reliability while maintaining low energy consumption is highly essential, since excessive data transmission can drain battery-operated units even more rapidly, thereby limiting operational endurance in this field.

Swarm Robotics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

20.6% |

|

Base Year Market Size (2025) |

USD 2.7 billion |

|

Forecast Year Market Size (2035) |

USD 14.5 billion |

|

Regional Scope |

|

Swarm Robotics Market Segmentation:

Robot Domain Segment Analysis

The ground/ AGV & AMR fleets are expected to attain a dominant share of 48.5% in the swarm robotics market over the forecasted years. The widespread acceptance of Industry 4.0 principles and the strong focus on smart manufacturing and logistics environments drive the subtypes' dominance. AMRs and AGVs are effective in terms of repetitive, labor-intensive tasks such as material handling, inventory management, and just-in-time delivery across sectors, i.e., automotive, consumer goods, and electronics manufacturing. In January 2024, ABB notified that it had acquired Sevensense to enhance its position in AI-enabled autonomous mobile robots by integrating advanced 3D vision and visual SLAM navigation technology. Therefore, this innovation allows AMRs to operate autonomously and collaboratively in dynamic industrial environments, thereby boosting efficiency in sectors such as automotive and logistics, hence denoting a wider segment scope.

Application Segment Analysis

In the application segment, logistics & warehousing is anticipated to grow at a considerable rate in the market by 2035. The growth of the segment is mainly driven by increasing demand for efficient supply chain management and the growing complexity of handling large inventories in constrained spaces. The adoption of swarm robotics results in more flexible operations and real-time adaptability, making it a highly suitable solution for modern logistics and warehousing challenges. For instance, in June 2024, DHL Supply Chain stated that it had achieved 500 million picks by utilizing Locus Robotics’ autonomous mobile robots (AMRs) across 35 warehouse sites worldwide. This particular situation highlights the transformative impact of collaborative robotics on productivity and operational efficiency, whereas the LocusBots work seamlessly alongwith human workers, enabling faster, more accurate order fulfillment, hence positively impacting market growth.

End use Segment Analysis

Military & defense is likely to grow with a significant share in the swarm robotics market, mainly due to ongoing investment in autonomous multi-agent systems for reconnaissance, surveillance, and distributed battlefield operations. In these cases, swarm robotics offers enhanced situational awareness and redundancy, which is highly essential for modern defense robotics programs. The sector opts for the heterogeneous swarms that combine aerial, ground, and maritime robots to operate collaboratively across multiple domains. In addition, the improvements in terms of AI-based coordination algorithms allow these swarms to autonomously distribute tasks, adapt to dynamic environments, and maintain mission continuity even if some units fail. Governments are funding rapid prototyping and field trials to test swarm capabilities in real-world military scenarios, accelerating technology maturation.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Robot Domain |

|

|

Application |

|

|

End use |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Swarm Robotics Market - Regional Analysis

North America Market Insights

North America swarm robotics market is expected to be the dominating landscape, capturing 38.8% of revenue share by 2035. The region’s leadership is mainly ascribable to advanced defense usage, logistics automation, and strong R&D investments in autonomous and swarm robotics. This region’s ecosystem also benefits from large government and private sector funding. In January 2026, NASA reported that its autonomous robot swarms for lunar orbit servicing and space asset assembly project, which is led by MIT under the Space Technology Mission Directorate, demonstrated swarming and inchworm robots to perform inspection, assembly, and maintenance tasks in microgravity through parabolic flight tests. In addition, this particular project showed how cooperative robot swarms can reduce astronaut workload and reliance on Earth-supplied parts, enabling a very low-cost, automated in-orbit servicing and in-space manufacturing, hence making it suitable for standard market growth.

The mission-oriented adoption is particularly witnessed in defense, space exploration, and large-scale automation, driving growth in the U.S. market. Federal programs and national laboratories play a central role in advancing swarm autonomy, whereas the startups and established robotics firms translate research outcomes into scalable systems for different applications. In May 2024, Lawrence Livermore National Laboratory (LLNL) reported that in 2023, the FAA granted it the first-ever authorization allowing autonomous drone swarm testing, enabling one operator to control up to 100 drones for real-time national security missions. Besides, it was led by LLNL’s autonomous sensors team, the effort advances swarm autonomy using laboratory-developed AI and machine-learning software for applications such as explosive hazard detection, methane leak identification, and nonproliferation. Hence, such instances in the country translate swarm robotics research into scalable, mission-ready systems.

The continued innovations through public-sector experimentation and academic-led development are responsible for the progress of the swarm robotics market in Canada. A strong focus on collaborative autonomous systems for aerospace safety, environmental monitoring, and defense preparedness, supported by government-backed testing environments, encourages the adoption of the swarm’s robotics in the country. In November 2025, the country’s government reported that its Counter Uncrewed Aerial Systems (CUAS) Sandbox (Urban) brought together innovators, the armed forces of the country, the RCMP, and U.S. government end-users to test advanced technologies for detecting micro and mini drones in dense urban environments. Besides the sandbox enabled real-world demonstrations across rooftops, balconies, and ground-level sites by utilizing live red team drone swarms to make evaluations regarding autonomous detection, tracking, and response capabilities, hence enhancing the utilization of autonomous swarm drone detection and response capabilities.

APAC Market Insights

The Asia Pacific swarm robotics market is expected to record the fastest growth due to rapid industrial automation, smart city development, and large-scale manufacturing ecosystems. The region mainly prioritizes coordinated robotic systems to improve efficiency in warehouses, transportation networks, and urban infrastructure. In August 2025, METI and NEDO announced that they had launched two coordinated government R&D initiatives to build an open, scalable software development platform for robotics with a prime focus on productivity gains in manufacturing, logistics, and services. The projects are focused on modularizing robot system functions and developing shared software tools and verification technologies, enabling diverse robot systems to work together efficiently at scale. The initiative will be running from FY2025 to FY2029, and support coordinated and interoperable robotic deployments positively impacting swarm robotics adoption in the region.

The national strategies for smart manufacturing and autonomous systems are responsibly positioning China market at the forefront of growth in the region. The country emphasizes large-scale deployment of coordinated robots in industrial production, logistics, and unmanned systems, leveraging strong hardware supply chains and aggressive technology localization. In January 2023, the country’s Ministry of Industry and Information Technology, along with 17 other departments, issued the implementation plan for the application of robot+ with a key goal of aiming to double robot density in manufacturing by 2025, when compared to 2020. The plan promotes coordinated deployment of industrial, service, and specialized robots by targeting breakthroughs in more than 100 innovative applications and establishing model enterprises, testing centers, and collaborative innovation systems. It reflects China’s government-led strategy for robotics-based economic development across key industries.

The academic research, defense innovation programs, and startup-led experimentation are certain drivers boosting the swarm robotics market in India. The focus spans around cost-efficient autonomous swarms for surveillance, disaster response, agriculture, and infrastructure inspection. For instance, in July 2025, Kepler Aerospace successfully secured a USD 4 million iDEX Prime contract from the country’s government to develop a 6-satellite ISR swarm constellation for the Defense Space Agency, HQ IDS, and Ministry of Defense. These satellites will operate collaboratively by utilizing swarm technology to autonomously track signals, heat signatures, and any suspicious activity, providing real-time situational awareness and enhancing national security. Hence, with such instances, there is a strong growth opportunity for the market in India.

Europe Market Insights

Europe swarm robotics market is forecasted to be a prominent player in the global landscape, propelled by its research-intensive ecosystem, focus on collaborative autonomy, safety, and human-robot interaction. Cross-border research programs and industrial partnerships support the development of swarm systems for different purposes. In May 2023, the European Defence Agency (EDA) stated that it had completed the ARTUS project by developing a demonstrator for a swarm of intelligent, autonomous unmanned ground vehicles to support infantry in transport and observation missions. It also notes that the system allows a single operator to manage the swarm through a battle management system in which the robots are autonomously navigating, avoiding obstacles, and continuing missions even if some units fail. It was led by Fraunhofer Gesellschaft, and including partners from France, Germany, and Austria, ARTUS showcases a collaborative industry and regional defence innovation in autonomous swarm robotics.

The industrial sector growth, coupled with improved manufacturing and Industry 4.0 initiatives are the key factor behind the increased exposure of Germany market. The country is exploring coordinated robot systems for flexible production lines, factory automation, and intelligent material handling, building on the country’s strong engineering base and automation expertise. As per the June 2024 announcement from Quantum Systems, it has successfully tested seven vector and scorpion drones flying in coordinated swarm formation under the KITU2 study, which is a feasibility project commissioned by the country’s armed forces. The drones were controlled by a mission AI, performed joint reconnaissance and target acquisition, including operations under GNSS-denied conditions, demonstrating autonomous, multi-mission swarm capabilitie hence, highlighting progress in military swarm robotics.

The UK swarm robotics market is readily blistering growth, mainly driven by university-led research, defense experimentation, and applications in environmental monitoring and infrastructure management. The country’s market also benefits from adaptive, decentralized control systems and real-world field trials by supporting innovation in both civil and security-focused use cases. In October 2025, the country’s Transport Research Innovation Grants (TRIG) programme, which was run by Connected Places Catapult for the Department for Transport, awarded an amount of £1.8 million (approximately USD 2.2 million) to 40 innovators, including projects developing swarm robotics for transport and freight efficiency. The funding supports research, prototyping, and real-world testing, with access to industry experts, mentoring, and networking within the TRIG ecosystem, hence suitable for bolstering the market’s growth.

Key Swarm Robotics Market Players:

- Boston Dynamics (U.S.)

- Clearpath Robotics (Canada)

- SwarmFarm Robotics (Australia)

- DJI Innovations (China)

- Hydromea (Switzerland)

- Red Cat Holdings (U.S.)

- Sentien Robotics (U.S.)

- Blue River Technology (U.S.)

- GreyOrange (India)

- ABB Ltd. (Switzerland)

- KUKA AG (Germany)

- Siemens AG (Germany)

- Omron Corporation (Japan)

- iRobot Corporation (U.S.)

- Locus Robotics (U.S.)

- Exyn Technologies (U.S.)

- Swarm Systems Limited (UK)

- Icarus Drone (U.S.)

- K-Team Corporation (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Boston Dynamics is a major pioneer in advanced mobile robotics, which is well known for dynamic, highly agile platforms. The company is also recognized for its individual robots, such as Spot. It is mainly focused on multi-agent coordination and collective autonomy for logistics, inspection, and defense use cases.

- Clearpath Robotics is a frontrunner in this field that specializes in autonomous ground vehicles and fleet systems that are suitable for industrial automation and research. Besides, the firm’s platforms are widely used in warehouses and manufacturing, with emphasis on multi-robot coordination and autonomous navigation.

- SwarmFarm Robotics is based in Australia and leads in terms of agricultural swarm robotics by developing distributed autonomous tractors and field robots that work collaboratively for diverse sorts of agricultural tasks. In addition, the company’s technology enhances precision agriculture by increasing productivity and reducing chemical usage through a very well-coordinated and decentralized system.

- DJI Innovations is yet another prominent player in this field, which is integrating swarm intelligence into UAV fleets for applications spanning agriculture, environmental monitoring, logistics, and security. DJI’s drones leverage advanced flight control and AI for coordinated multi-unit operations at scale.

- Hydromea is a predominant leader in underwater swarm robotics and is developing autonomous submersible systems that are capable of collaborative sensing, inspection, and marine research. Furthermore, the company’s solutions emphasize communication and coordination underwater, which is considered to be a technically challenging domain.

Below is the list of some prominent players operating in the global market:

The swarm robotics market is extremely dynamic and competitive, consisting of established automation leaders along with specialized innovators in terms of aerial, ground, and underwater autonomous systems. Major entities in this field are making investments in AI, decentralized control, and scalable multi-agent coordination with a primary focus on improving resilience, communication, and decision-making in complex environments. Partnerships, acquisitions to enhance technology portfolios, and international R&D expansion into logistics, agriculture, and military domains are a few prominent strategies adopted by the leading pioneers to secure their market positions. In September 2025, Auterion notified the launch of Nemyx, which is a cross-platform drone swarm system that enables multiple drones from different manufacturers to operate as a coordinated unit by properly executing AI-guided missions with precision and scale.

Corporate Landscape of the Market:

Recent Developments

- In November 2025, Apium Swarm Robotics reported that it had signed an MOA with Red Cat Holdings to join the Red Cat Futures Initiative, which was followed by a successful U.S. Army testing of Apium’s Swarm Autopilot integrated into Red Cat’s Teal 2 tactical drone. Through this, an operator can launch and adapt missions in real time, without centralized control or complex pre-planning.

- In October 2025, Palladyne AI Corp. reported that it entered into a collaboration with Draganfly Inc. with a key goal to enhance the capabilities of Draganfly’s unmanned aerial vehicle platforms with Palladyne Pilot AI software.

- Report ID: 3099

- Published Date: Feb 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.