Suture Needle Market Outlook:

Suture Needle Market size was valued at USD 614.5 million in 2025 and is anticipated to reach USD 1.04 billion by the end of 2035, expanding at around 5.5% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of suture needle is estimated at USD 648.3 million.

The suture needle market is supported by sustained surgical procedure volumes, rising demand for wound closure in chronic disease management, and continued expansion of healthcare infrastructure globally. According to the NLM December 2025 study, noncommunicable diseases account for approximately 43 million deaths annually, representing around 75% of all non-pandemic deaths worldwide, creating a significant burden of cardiovascular, oncological, and gastrointestinal conditions that frequently require surgical intervention. The WHO February 2024 data estimated 20 million new cancer cases and 9.7 million cancer-related deaths globally in 2022, with the number of new cases projected to increase in coming decades. Cancer surgeries remain a major contributor to demand for surgical consumables, including suture needles.

In parallel, the U.S. Centers for Disease Control and Prevention (CDC) reports that adults in the United States live chronic disease, increasing the likelihood of operative procedures over a patient’s lifetime. Healthcare expenditure growth also supports procurement activity. According to the AMA April 2025 data, U.S. healthcare spending reached USD 4.9 trillion in 2023, accounting for 17.5% of GDP, reflecting continued investment in hospitals, ambulatory surgical centers, and procedural care environments where suture needles are routinely utilized. These demographic, disease-burden, and healthcare-investment trends collectively support stable procurement and utilization of suture needles across hospital, specialty clinic, and ambulatory care networks worldwide.

Key Suture Needle Market Insights Summary:

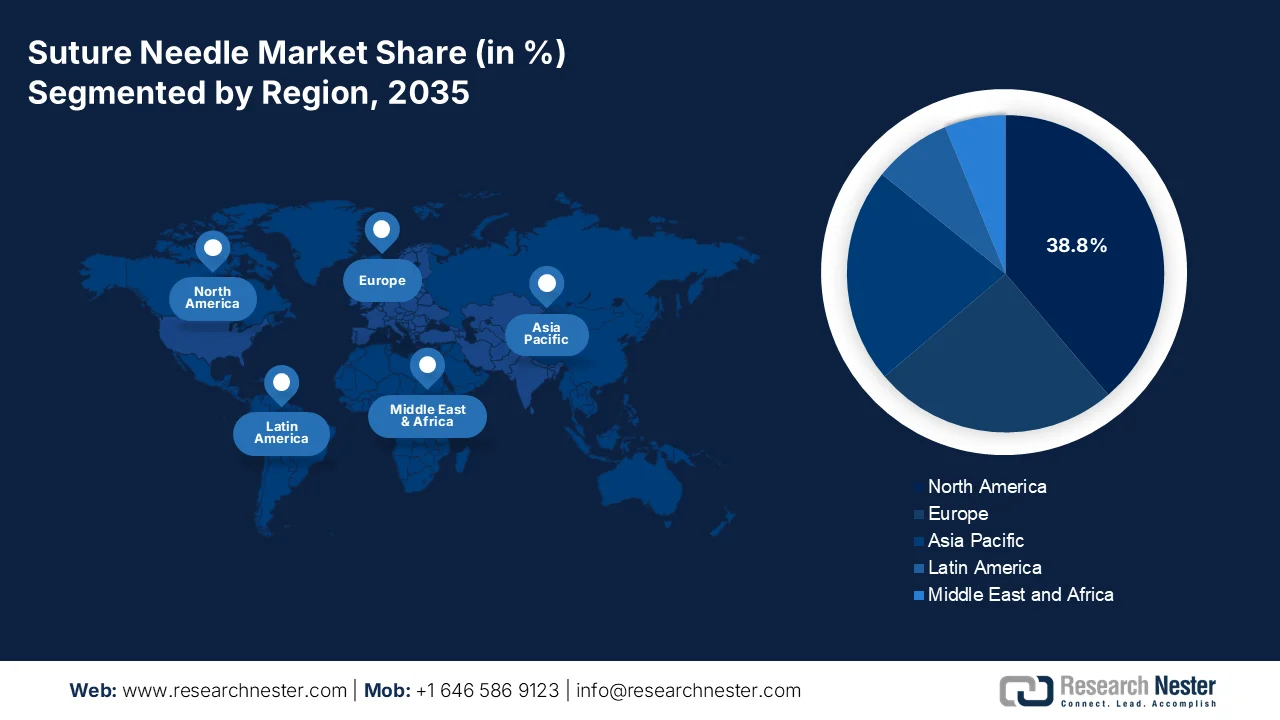

Regional Highlights:

- Suture needle market North America is anticipated to capture 38.8% of the regional revenue share by 2035, bolstered by advanced surgical infrastructure, high procedure volumes, and strong clinician preference for innovative wound closure technologies

- Asia Pacific is projected to witness the fastest expansion throughout 2026-2035, fueled by expanding healthcare access, rising surgical volumes, and increasing medical tourism across developing economies

Segment Insights:

- Suture needle market the straight shaped needles segment is projected to account for 42.3% of the market share by 2035, supported by the growing prevalence of microsurgical and super-microsurgical procedures

- The Reverse Cutting Needles segment is expected to retain its leading position in the market by 2035, attributed to its superior design for skin and fascial closures

Key Growth Trends:

- Expansion of universal surgical access programs

- Growing cancer surgery volumes worldwide

Major Challenges:

- Stringent regulatory approvals

- High capital investment for precision manufacturing

Key Players: Medtronic (U.S.), B. Braun (Germany), Smith & Nephew (UK), MMI (Italy), Arthrex (U.S.), Corza (U.S.).

Global Suture Needle Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 614.5 million

- 2026 Market Size: USD 648.3 million

- Projected Market Size: USD 1.04 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, South Korea, Malaysia, Indonesia, Vietnam

Last updated on : 8 July, 2026

Suture Needle Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of universal surgical access programs: Governments and international health organizations are increasing investments to improve access to essential surgery. The NLM June 2025 study estimates that 143 million additional surgical procedures are needed annually in low- and middle-income countries to address unmet healthcare needs. India's public healthcare infrastructure expansion under Ayushman Bharat continues increasing access to surgical care for hundreds of millions of beneficiaries. These investments generate recurring demand for surgical consumables, including suture needles. Procurement agencies are prioritizing cost-effective, high-volume products capable of supporting expanding public health systems. Manufacturers that establish local distribution networks and government tender participation strategies can gain access to growing procedure volumes.

- Growing cancer surgery volumes worldwide: Cancer incidence is increasing globally, creating sustained demand for surgical procedures and associated consumables. Many solid tumors require surgical resection as a primary or complementary treatment approach, directly increasing utilization of suture needles across oncology departments. Governments are allocating larger budgets toward cancer diagnosis and treatment infrastructure. For example, the U.S. National Cancer Institute May 2026 data depicts that it has received funding exceeding USD 7 billion in recent federal budgets to support cancer-related healthcare and research programs. Suppliers capable of serving oncology-focused hospitals and specialty surgical centers can benefit from this expanding patient pool. The continued rise in cancer burden remains one of the strongest long-term demand drivers across the surgical consumables sector.

Challenges

- Stringent regulatory approvals: Navigating FDA 510(k) and EU MDR requirements demands extensive clinical evidence and quality documentation, creating high entry barriers. Smaller manufacturers struggle with costly, time-consuming submission processes. Companies like Ethicon leverage decades of pre-market approvals, while new entrants must invest heavily in regulatory affairs teams to achieve market access.

- High capital investment for precision manufacturing: Producing surgical needles requires advanced CNC grinding, laser-drilled swaging, and electropolishing equipment, with millions in upfront costs. Maintaining micron-level tolerances demands cleanroom facilities and skilled technicians. Arthrex has vertically integrated its forging facilities to control quality, whereas startups often outsource production, compromising margin control.

Suture Needle Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 614.5 million |

|

Forecast Year Market Size (2035) |

USD 1.04 billion |

|

Regional Scope |

|

Suture Needle Market Segmentation:

Shape Segment Analysis

Under the shape segment, the straight shaped needles dominate the suture needle market and is poised to hold the share value of 42.3% by the end of 2035. The segment is driven due to the prevalence of microsurgical and super-microsurgical procedures. Their linear design allows for direct, axial placement of sutures without the need for wrist rotation, making them ideal for superficial wound approximation, tendon repair, and microvascular anastomosis. Straight needles are particularly valued in ophthalmic and neurological surgeries, where precision and minimal tissue dissection are paramount. Their simplicity also facilitates easier handling in confined surgical fields, offering surgeons a reliable alternative to curved counterparts for specialized procedures.

Type Segment Analysis

Reverse cutting needles dominate the suture needle market by type, holding the largest share value by the end of 2035, due to their superior design for skin and fascial closures. As per the NLM August 2023 study, these needles feature 3 sharp edges with the cutting surface located on the outer curvature, which lifts tissue fibers rather than cutting downward, minimizing the risk of suture pull-through and reducing tissue trauma. This geometry makes them ideal for penetrating tough tissues like skin, sternum, and scarred fascia, where precision and hemostasis are critical. Unlike conventional cutting needles, the reverse design provides greater tensile strength and lower dehiscence rates, making them the preferred choice for emergency and trauma surgeries. Their predictable penetration force and reduced needle-stick injury risk further cement their clinical superiority in high-tension wound closures.

Material Segment Analysis

Stainless steel remains a dominant material in the suture needle market. The segment is driven due to its exceptional hardness, corrosion resistance, and ability to maintain sharpness through multiple tissue passes. The NLM study in August 2024 data depicts that Shouldice Hospital—a world-renowned hernia center—demonstrates stainless steel's enduring reliability. In a prospective study of 1,120 patients undergoing primary inguinal hernia repair, stainless-steel wire sutures achieved a 1.96% recurrence rate at a median follow-up of 16 months, which was statistically non-inferior to polypropylene (p > 0.05). The study also reported only a 1.96% surgical site infection rate, affirming stainless steel's safety profile. These findings reinforce stainless steel's value in high-tension fascial closures, particularly in centers where alternative materials are unavailable.

Our in-depth analysis of the suture needle market includes the following segments:

|

Segment |

Subsegments |

|

Shape |

|

|

Type |

|

|

Material |

|

|

Suture Attachment |

|

|

Coating |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Suture Needle Market - Regional Analysis

North America Market Insights

North America is dominating the suture needle market and is projected to hold the regional revenue share of 38.8% by the end of 2035. The segment is driven by the advanced surgical infrastructure, high procedure volumes, and strong clinician preference for innovative wound closure technologies. The United States drives regional growth through concentrated hospital networks, group purchasing organizations, and value-based reimbursement models favoring quality outcomes. Canada's publicly funded system prioritizes cost-effective procurement while maintaining stringent regulatory standards through Health Canada. Key trends include rising adoption of barbed knotless sutures, silicone-coated needles for reduced tissue drag, and swaged eyeless designs minimizing needlestick injuries.

The high surgical volumes supported by oncology, obstetric, cardiovascular, and general surgery procedures is shaping the suture needle market in the U.S. According to the NLM February 2025 study, the U.S. is expected to record approximately 2,041,910 new cancer cases, sustaining demand for tumor resection and reconstructive surgeries that require wound-closure products. In addition, the Centers for Disease Control and Prevention (CDC) June 2026 data reported approximately 3.63 million births, supporting continued utilization of suture needles in cesarean sections and other obstetric procedures. Ongoing investments in hospital infrastructure, ambulatory surgery centers, and surgical workforce capacity further strengthen procurement demand across public and private healthcare systems.

The growing surgical demand and sustained public healthcare investment is shaping the suture needle market in Canada. According to the Elite Providers Hub for Progressive Play 2026 data, total health spending in Canada is projected to reach approximately CAD 372 billion, equivalent to about CAD 9,054 per person, reflecting continued funding for hospitals and surgical services. In addition, Federal Retirees March 2025 data reported that the population aged 65 years and older reached approximately 7.8 million, accounting for nearly one-fifth of the national population. This demographic trend is increasing the volume of orthopedic, cardiovascular, and other age-related surgical procedures, thereby supporting demand for suture needles across acute care hospitals, specialty surgical centers, and outpatient treatment facilities.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035. The region is driven by the expanding healthcare access, rising surgical volumes, and increasing medical tourism across developing economies. Japan and South Korea lead in technological innovation with precision micro-needles, while China and India drive volume growth through large-scale public hospital networks and cost-effective manufacturing capabilities. Southeast Asian nations like Malaysia and Indonesia are emerging as production hubs for export-oriented suture needle manufacturing. Key trends include growing adoption of disposable, pre-sterilized needles, increasing preference for swaged eyeless designs, and rising demand for absorbable suture-compatible needles.

The rising healthcare utilization and government-led healthcare infrastructure development is driving the suture needle market in India. According to the PIB December 2023 data, more than 6.11 crore hospital admissions had been authorized under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY), reflecting substantial growth in access to surgical and inpatient care. Additionally, the PIB July 2025 data reported that the number of medical colleges in India increased to 780 in 2025, up from 706 in 2023, supporting expansion of healthcare facilities and surgical capacity nationwide. These developments are increasing procedural volumes across public and private hospitals, thereby strengthening demand for suture needles used in general, obstetric, orthopedic, and specialty surgeries.

The expanding healthcare services, rising surgical volumes, and continued public investment in medical infrastructure is driving the suture needle market in China. According to the ILO 2025 data, the country recorded approximately 9.55 billion medical and health institution visits in 2024, reflecting strong utilization of hospital and clinical services that drive demand for surgical consumables. Additionally, data from the People’s Republic of China November 2023 data show that the number of hospitals increased to more than 38,000, supported by ongoing healthcare capacity expansion and modernization initiatives. The combination of a large patient base, growing access to surgical care, and government-backed healthcare development programs continues to strengthen procurement demand for suture needles across tertiary hospitals, specialty centers, and regional healthcare facilities.

Europe Market Insights

The suture needle market in Europe is mature and innovation-driven, characterized by stringent regulatory oversight under the Medical Device Regulation (MDR) and strong emphasis on surgical safety and infection control. Key trends include growing preference for eco-friendly, reduced-packaging needle systems, rising adoption of barbed knotless sutures in minimally invasive surgeries, and increasing demand for premium silicone-coated needles that minimize tissue trauma. Price sensitivity varies across Southern and Eastern Europe, where cost-effective alternatives gain traction, while Western Europe prioritizes clinical performance and regulatory compliance.

The large hospital network, advanced surgical capabilities, and sustained healthcare expenditure is driving the suture needle market in Germany. According to the NLM March 2025 study, hospitals in Germany treated approximately 16.8 million inpatient cases, highlighting the substantial volume of medical procedures performed across the healthcare system. This high level of patient activity supports consistent demand for surgical consumables, including suture needles used in general surgery, orthopedics, cardiovascular procedures, and oncology interventions. Ongoing investments in hospital modernization, an aging population requiring more surgical care, and continued emphasis on maintaining high clinical standards further contribute to procurement demand across public and private healthcare facilities throughout Germany.

The substantial surgical activity within the National Health Service and ongoing investment in healthcare delivery is driving the suture needle market in the UK. According to NHS England 2024 data, hospitals and community health services delivered approximately 1.51 million consultant-led referral-to-treatment (RTT) pathways, reflecting the significant volume of patients progressing through diagnostic and surgical care pathways. Efforts to reduce elective care backlogs and expand surgical capacity through dedicated surgical hubs are increasing demand for wound-closure consumables across NHS facilities. Additionally, growing requirements for orthopedic, cancer, cardiovascular, and general surgical procedures continue to support procurement of suture needles, making the UK an important market within the European surgical supplies landscape.

Key Suture Needle Market Players:

- Medtronic (U.S.)

- B. Braun (Germany)

- Smith & Nephew (UK)

- MMI (Italy)

- Arthrex (U.S.)

- Corza (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic maintains a strong legacy portfolio in the suture needle market through its acquired Covidien surgical assets, which include the popular Syneture® needle line. The company focuses on precision-engineered needles with proprietary stainless-steel alloys and laser-drilled swage technology to minimize tissue drag and needle breakage.

- B. Braun is a dominant European player in the suture needle market, renowned for its Aesculap® surgical needle range, which features premium atraumatic designs and siliconized coatings for superior penetration. The company's key strategic initiative is the development of eco-friendly, sterile-packaging solutions for suture needles, reducing plastic waste without compromising sterility.

- Smith & Nephew competes aggressively in the suture needle marketthrough its orthopedic and sports medicine portfolios, particularly with needles designed for rotator cuff repairs and tendon fixations. The company's strategic focus is on developing high-tensile, corrosion-resistant needles that pair seamlessly with its ultra-high-molecular-weight polyethylene sutures.

- MMI has entered the suture needle market indirectly through its Symani® Surgical System, which uses proprietary micro-suture needles for super-microsurgery (vessels <0.8 mm). MMI's strategic initiative focuses on co-developing ultra-fine, flexible tungsten-alloy needles with specialized Italian needle manufacturers, enabling tremor-free suturing in lymphatic and reconstructive procedures.

- Arthrex is a powerhouse in the suture needle market, particularly within orthopedics and sports medicine, offering a vast array of needles for shoulder, knee, and foot/ankle repairs. The company's flagship initiative is the FiberLoop® and FiberWire® needle-suture constructs, which feature needles with proprietary PEEK or titanium tips for improved bone penetration without dulling.

Here is a list of key players operating in the global suture needle market:

The global suture needle market is highly consolidated, dominated by U.S. and Europe players that leverage deep clinical relationships and broad product portfolios. Key strategic initiatives include the development of proprietary needle geometries to reduce tissue trauma, and the integration of smart coatings for improved penetration. To counter pricing pressure from Asian manufacturers, leaders are investing in automated laser-drilled swage processes for greater consistency and expanding into absorbable and barbed suture systems. Simultaneously, regional players in India and Malaysia are scaling up exports via cost-competitive manufacturing and regulatory certifications, while Japanese firms focus on ultra-fine needles for microsurgery.

Corporate Landscape of the Market:

Recent Developments

- In April 2026, MMI (Medical Microinstruments, Inc. announced the commercial launch in the U.S. of its Robotic Suture. The first suture purpose-built for the Symani® Surgical System represents MMI’s continued innovation in microsurgery and is suitable for cases where delicate suturing is required.

- In September 2025, Arthrex announced the launch of NanoNeedle™ scope 2.0, the latest version of the company's minimally invasive imaging platform. The technology was recently used for the first time in a clinical case by Kyle Anderson, MD, at Anderson Sports Medicine in Bingham Farms, Michigan.

- In July 2025, Corza Medical announced the launch of its expanded Onatec Ophthalmic Suture Portfolio. This marks a significant extension of the product range, making it easier for surgeons worldwide to find the right Onatec suture solution for their ophthalmic procedures.

- Report ID: 8663

- Published Date: Jul 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.