Solar EPC Market - Regional Analysis

APAC Market Insights

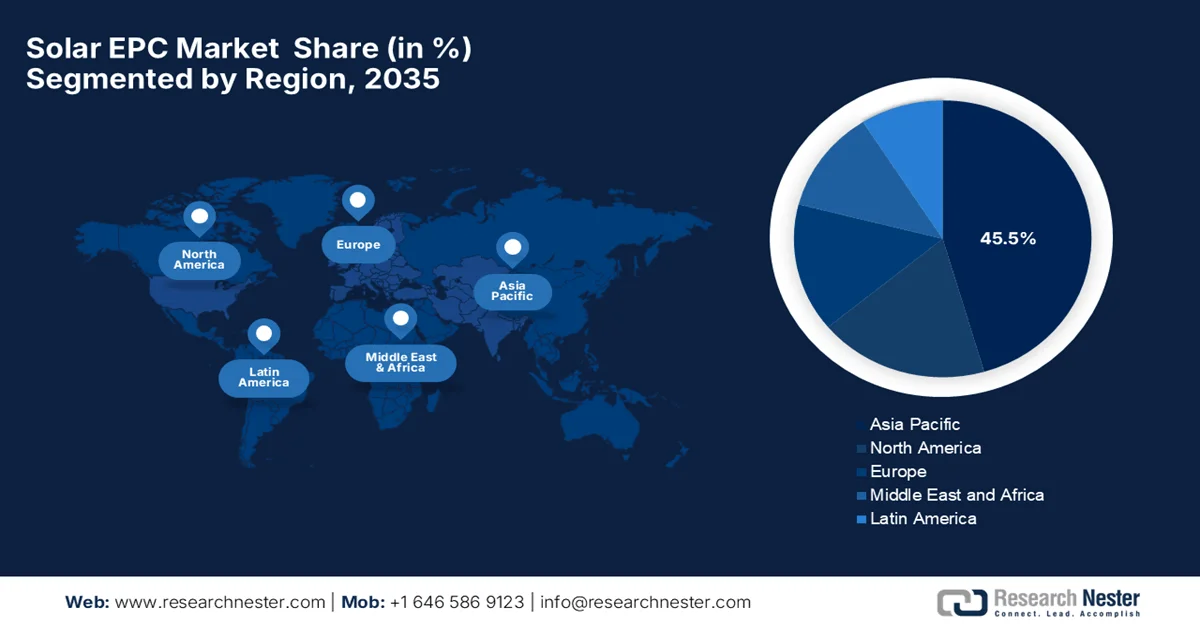

The Asia Pacific solar EPC market is expected to capture a total of 45.5% revenue share during the assessment period. The region’s prominence is highly driven by urban infrastructure development, where solar installations are embedded into industrial parks, smart cities, and new commercial developments. This integration creates large-scale EPC opportunities that are suitable for urban expansion, and the region is exploring alternatives to address land efficiencies. Based on the government data from Japan, which was published in August 2023, the country is emerging with two major solar technologies, such as space-based solar power and perovskite solar cells, with the main goal to overcome land and efficiency limitations of traditional PV. SBSP satellites are equipped with giant solar panels and will transmit microwaves to Earth, enabling a 90% utilization rate and power output comparable to nuclear plants. Kyoto University has led decades of microwave transmission experiments wherein the country’s basic plan on space policy targets a space-to-ground transmission test by FY2025, expanding solar deployment across urban environments.

The large-scale renewable base development in industrial regions, which is designed to supply power to distant demand centers are responsible for uplifting China solar EPC market. These mega-projects necessitate complex engineering, transmission coordination, and high-capacity EPC execution, providing encouraging opportunities for both foreign and domestic players. CPA in February 2024 revealed that the country controls more than 80% of the worldwide solar PV supply chain, spanning polysilicon, wafers, cells, and modules. There is a financial strain on the country’s players, whereas companies such as JinkoSolar, Trina Solar, and Canadian Solar sustain operations through substantial subsidies and investments from the country’s government, which allocated USD 130 billion into solar in 2023. This state-backed support propels solar EPC market growth by supporting project development, lowering financial risks for EPC contractors.

The constant government backing and the deployment of hybrid and renewable energy projects are the main fueling factors for the solar EPC market in India. Support also includes financial incentives, policy frameworks, and streamlined approval processes that make large-scale solar projects even more feasible. The country is also identified as a major trade hub, attracting more investments in this field. In this context, Energy & Environment in August 2025 stated that the country has emerged as the world’s third-largest solar energy producer, which has generated around 1,08,494 GWh in 2025. Besides, the country’s cumulative solar capacity reached 119.02 GW, which includes 90.99 GW from ground-mounted plants and 19.88 GW from rooftop systems. Government initiatives such as PM Surya Ghar Yojana, PM-KUSUM, and Solar Parks Scheme are driving adoption, whereas the domestic manufacturing of solar modules expanded from 38 GW to 74 GW in FY 2024-25, making it suitable for standard solar EPC market growth.

India Solar Energy Statistics 2025: Installed Capacity, Generation, and Government Initiatives

|

Metric |

Value (2025) |

Notes |

|

Solar Power Generation |

1,08,494 GWh |

Surpassed Japan’s 96,459 GWh |

|

Cumulative Solar Capacity |

119.02 GW |

90.99 GW ground-mounted, 19.88 GW rooftop, 3.06 GW hybrid, 5.09 GW off-grid |

|

Solar Module Manufacturing Capacity |

74 GW |

Up from 38 GW in FY 2024-25 |

|

Renewable Share of Total Installed Capacity |

50.07% |

Out of 484.82 GW total capacity |

|

Solar Parks Approved |

53 Parks |

Total capacity 39,323 MW; 18 fully developed |

Source: Energy & Environment

India’s Country-wise Imports of Solar PV Cells and Modules in 2021-22 and 2022-23 (USD Millions)

|

Country |

2021-22 Solar PV Cells (HS 85414011) |

2021-22 Solar PV Modules (HS 85414012) |

2022-23 Solar PV Cells (HS 85414200) |

2022-23 Solar PV Modules (HS 85414300) |

|

Australia |

0.01 |

- |

0.22 |

- |

|

Cambodia |

1.72 |

- |

52.72 |

- |

|

Canada |

1.32 |

- |

0.01 |

- |

|

Chile |

0.63 |

- |

- |

- |

|

Taiwan |

5.48 |

- |

0.13 |

1.92 |

|

China PRP |

1069.88 |

3075.32 |

581.45 |

874.89 |

|

France |

- |

- |

- |

- |

|

Germany |

0.19 |

- |

0.21 |

0.13 |

|

Hong Kong |

0.55 |

- |

229.12 |

3.04 |

|

Indonesia |

0.78 |

- |

1.56 |

- |

|

Italy |

- |

- |

0.01 |

- |

|

Japan |

- |

- |

0.61 |

- |

Source: Ministry of New and Renewable Energy

North America Market Insights

The solar EPC market in North America is primarily reshaped by suitable project financing incentives and long-term power contracting mechanisms, which readily enable large, bankable solar developments. The risk management, standardized EPC contracts, and strong institutional participation support constant project execution across the region’s vast geography. In January 2025, the U.S. Department of Energy reported that its loan programs office approved a total of USD 289.7 million loan guarantee to Sunwealth for Project Polo, which will deploy up to 1,000 solar PV and battery storage systems across 27 states. It has an aggregate capacity of 168 MW PV and 16.8 MW BESS, and it will function as a wide-scale virtual power plant by enhancing grid resilience and cutting 4.07 million metric tons of carbon emissions. Hence, from a strategic perspective, such government-backed financing is boosting investor confidence and accelerating large-scale solar-plus-storage projects in the region.

The expansion of community solar and shared solar ownership models creates EPC demand more than traditional utility and rooftop installations, driving business in the U.S. solar EPC market. These models broaden solar EPC market participation and diversify EPC project portfolios across different sectors. NREL in September 2024 revealed that between 2023 and 2024, community solar in the U.S. had expanded, with several states updating or enacting policies to enhance accessibility and benefits. Alaska established enabling legislation under Senate Bill 152, whereas Maryland made its 583 MW pilot program permanent. Colorado and Minnesota revised their programs to reserve 51% and 30% of new projects for income-qualified subscribers, and New Jersey converted its 243 MW pilot into a permanent program. These policy updates are creating new EPC opportunities across multiple states in the U.S., hence denoting a positive solar EPC market outlook.

Provincial-level clean electricity planning and public-sector procurement frameworks, which create structured and predictable project pipelines, are the main factors driving the growth of the solar EPC market in Canada. Long-term energy planning and utility-led initiatives deliberately support steady EPC demand in the country. In October 2024, the country’s government reported that under its greening government strategy, it has awarded more than USD 73 million in renewable energy certificate contracts to Hep Solar and South Head Switch Power to supply 100,600 RECs on a yearly basis from new solar facilities. This particular initiative supports 100% clean electricity for federal buildings, reduces up to 32,600 tons of eCO₂, and efficiently strengthens partnerships with Indigenous-owned businesses, thereby driving sustained solar EPC demand in the country.

Europe Market Insights

Europe solar EPC market has acquired a prominent position in the global landscape mainly due to cross-border energy integration and regional grid harmonization efforts, which support multi-country solar developments and interconnected renewable systems. EPC players in the region benefit from projects that are aligned with continental energy coordination. In April 2024, as stated by the European Commission, along with energy ministers from 23 Europe based countries, it launched the European Solar Charter to strengthen the region’s photovoltaic sector. This Charter promotes the region-specific solar panels, supports sustainable products, and encourages the use of non-price criteria in renewable energy auctions and public procurement. Furthermore, the initiative aims to help the region to reach at least 42.5% renewable energy by 2030, with solar PV as a key driver of the energy transition, hence denoting there is a huge opportunity for solar EPC in the upcoming years.

EU Solar Panel Trade 2024: Imports and Exports in USD

|

Trade Flow |

Value (€ billion) |

Largest Partners |

Share |

|

Imports |

11.1 (USD 12.1 billion) |

China |

98% of imports from China |

|

Exports |

0.7 (USD 0.76 billion) |

Switzerland, UK |

26% to Switzerland, 22% to the UK |

Source: Eurostat

The growth of citizen and cooperative solar ownership models, which are focused on decentralized generation and community participation, and increasing PV expansions, is rearranging the growth dynamics in the Germany solar EPC market. These projects generate constant EPC demand across distributed and mid-scale installations, encouraging more players to make investments in this field. In April 2024, the Federal Ministry of Economic Affairs & Energy reported that Germany’s Bundestag and Bundesrat adopted Solar Package I, which is designed to accelerate PV expansion toward 2030 climate targets. It was followed by a record 14 GW of new PV capacity in 2023, and the package simplifies deployment rules, reduces bureaucracy, and supports installations from balcony systems to large-scale ground-mounted projects. Furthermore, it also strengthens provisions for wind, bioenergy, and grid connections, forming a key part of the country’s solar strategy to ensure competitive prices in a climate-neutral electricity system.

The UK solar EPC market has gained enhanced traction, effectively driven by the rise of corporate-led renewable procurements in which businesses directly contract solar installations to meet long-term sustainability and energy sourcing objectives. Such trends support EPC activity across commercial and utility-scale projects in the country. For instance, in April 2024, RWE notified that it had signed its first UK solar power purchase agreement with Kerry Group, by committing a clean electricity supply from its Cotmoor and Copse Lodge solar projects for more than 10 years starting in 2025. It also mentioned that each project has a potential capacity of 49.9 MWac, wherein Cotmoor is already under construction, and Copse Lodge is set to follow in 2025. Hence, the presence of such corporate-led PPAs effectively drives consistent demand for EPC services in the country.