Smart Transformers Market Outlook:

Smart Transformers Market size was valued at USD 3.8 billion in 2025 and is expected to surpass a significant USD 14.2 billion by the end of 2035, rising at a CAGR of 15.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of smart transformers is assessed at USD 4.4 billion.

The global smart transformers market is all set to witness extensive growth in the next decade, mainly due to the urgent need for grid modernization, the integration of renewable energy sources, and the rapid expansion of electric vehicle charging infrastructure. In this context, the article published by the International Energy Agency (IEA) in July 2023 reported that global investment in smart grids is accelerating, wherein Europe is planning USD 633 billion by 2030, including USD 184 billion for digitalization. Meanwhile, China has invested almost USD 442 billion between 2021 and 2025, whereas Japan has announced USD 155 billion and India USD 38 billion for grid modernization. In addition, the U.S. generously invested almost USD 10.5 billion through its GRIP program, and Canada is supporting deployment with USD 100 million, hence indicating a sustained demand for smart transformers in the years ahead.

Furthermore, the key trends reshaping the future dynamics of the market are increasing demand for distribution transformers and the adoption of energy-efficient designs to meet sustainability goals. The future outlook for the market is solid, with substantial investments that are directed toward creating intelligent grid systems that can manage complex energy flows. For instance, in December 2024, as stated by the U.S. Department of Energy, it is supporting grid modernization through generous funding for advanced transformer and semiconductor technologies. Besides, the DOE Office of Electricity selected nine projects under the Flexible Innovative Transformer Technologies program, allocating about USD 18 million and USD 2 million with a main goal to develop hybrid and solid-state transformer systems for improved voltage control, fault management, and grid responsiveness. These initiatives reflect a federal effort to deal with aging grid infrastructure, rising electrification demand, and instability from renewable integration through transformer and power electronics deployment.

U.S. DOE Grid Modernization & Silicon Carbide (SiC) Smart Transformer Funding Breakdown: FITT Program and Prize Investment Statistics (2024)

|

Category |

Program |

Allocation |

Participants |

|

Grid modernization |

FITT FOA |

USD 20 million (USD 18 million OE + USD 2 million CESER) |

9 projects |

|

Project funding |

SHAPE (Clemson Univ.) |

USD 2.47 million |

Clemson University |

|

Project funding |

GE Vernova FASST |

USD 1.99 million |

GE Vernova |

|

Project funding |

Eaton hybrid transformer |

USD 2.94 million |

Eaton |

|

Project funding |

Univ. of Pittsburgh testbed |

USD 2.5 million |

University of Pittsburgh |

|

Semiconductor program |

SiC Packaging Prize Phase 1 |

USD 400K total |

8 teams |

|

Program scale |

DOE SiC multi-phase |

Up to USD 2.25 million total |

Selected teams |

|

Phase 2 support |

SiC Phase 2 |

Up to USD 250K/team |

Up to 4 teams |

Source: U.S. DOE

Key Smart Transformers Market Insights Summary:

Regional Highlights:

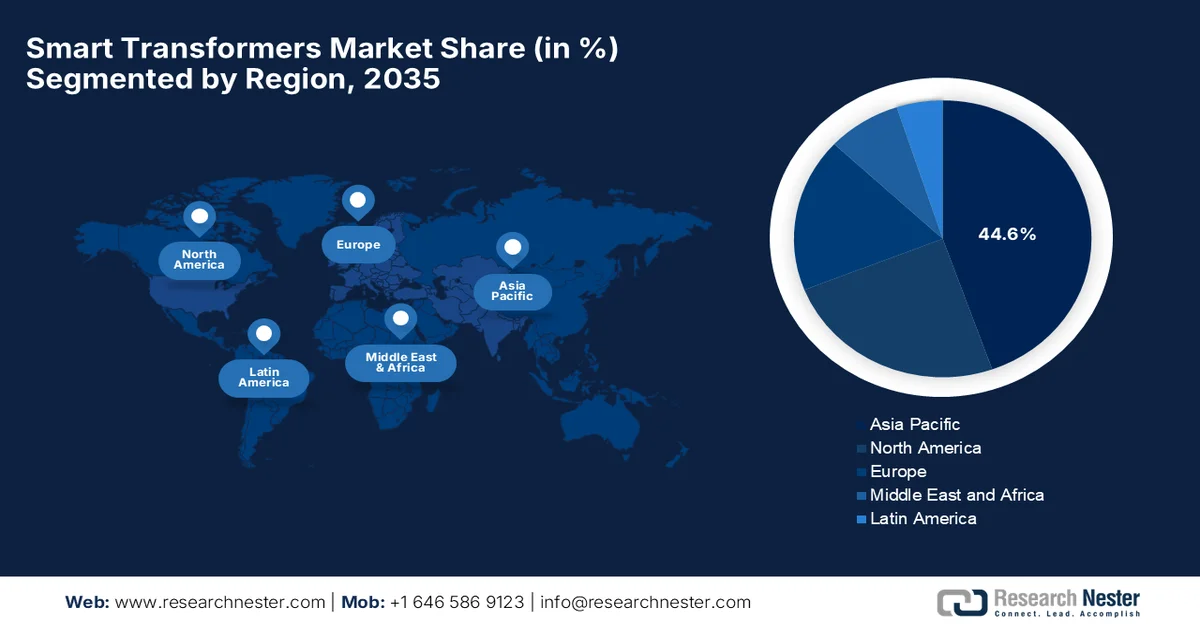

- Asia Pacific smart transformers market is anticipated to dominate with a 44.6% share by 2035, impelled by massive investments in urban electrification, renewable energy integration, and smart city infrastructure

- North America region is projected to hold a significant share over the forecast period 2026-2035, stimulated by intensive grid modernization efforts and rising demand for reliable and efficient power systems

Segment Insights:

- Smart Transformers Market’s smart grid segment is projected to account for 75.7% share by 2035, bolstered by its extensive integration in modern power system operations

- Distribution transformer segment is expected to secure a notable share over the forecast period 2026-2035, fueled by massive deployment in urban and rural electrification projects

Key Growth Trends:

- Rising integration of renewable energy

- Increasing demand for energy efficiency

Major Challenges:

- Complex integration with legacy grid systems

- Cybersecurity risks and data vulnerability

Key Players: ABB Ltd, Hitachi Energy Ltd, Schneider Electric SE, Siemens Energy AG, SGB-SMIT Group, GE Vernova, Eaton Corporation plc, SPX Transformer Solutions Inc., Howard Industries Inc., Emerson Electric Co., Mitsubishi Electric Corporation, Toshiba Energy Systems & Solutions Corporation, Fuji Electric Co., Ltd., Nissin Electric Co., Ltd., Hammond Power Solutions, Hyundai Electric & Energy Systems Co., Ltd., Hyosung Heavy Industries Corporation, Bharat Heavy Electricals Limited (BHEL), CG Power & Industrial Solutions Ltd., Transformers and Rectifiers (India) Ltd., TBEA Co., Ltd.

Global Smart Transformers Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.8 billion

- 2026 Market Size: USD 4.4 billion

- Projected Market Size: USD 14.2 billion by 2035

- Growth Forecasts: 15.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (44.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Brazil, South Korea, Mexico, Saudi Arabia, Indonesia

Last updated on : 17 April, 2026

Smart Transformers Market - Growth Drivers and Challenges

Growth Drivers

- Rising integration of renewable energy: Growth of solar and wind energy requires flexible grid systems. In this context, smart transformers handle fluctuating power supply, support bidirectional energy flow, and maintain grid stability, thus driving extensive growth in the smart transformers market. As per an article published by IEA in December 2025, global renewable energy is projected for a sharp rise, wherein the share of renewables in power generation is increasing from 32% in 2024 to 43% by 2030, whereas variable renewable energy grows from 15% to 28%. It also mentioned that the yearly renewable capacity additions are anticipated to expand from 683 GW in 2024 to nearly 890 GW in 2030. Between 2025 and 2030, cumulative renewable capacity is expected to grow by almost 4,600 GW, hence driving huge growth in the smart transformers industry globally.

- Increasing demand for energy efficiency: The traditional grids that have been used in earlier years face high transmission losses and inefficient load management. Therefore, utilizing smart transformers reduces energy wastage, operational costs, and carbon emissions. As per the November 2023 article published by the U.S. Energy Information Administration, electricity transmission and distribution losses in the U.S. are a major inefficiency in traditional power grids. It also stated that these losses averaged about 5% of total electricity transmitted and distributed in a span of five years. This means a notable portion of generated electricity is lost before reaching end users due to resistance, heat dissipation, and grid limitations. Therefore, the concern regarding such consistent losses highlights the need for advanced technologies to improve efficiency, reduce wastage, and optimize grid performance, thus benefiting the overall market.

- Growth in electricity demand & electrification: The aspects such as rising urbanization, industrialization, and population growth are efficiently boosting electricity demand. On the other hand, in data centers, electric vehicles, and industrial automation, there is an extensive electricity need, which is creating an urgent requirement for efficient power distribution systems. In 2025, the article published by the IEA stated that global electricity demand had grown at a noteworthy pace, increasing by 3.3% in 2025 and 3.7% in 2026. This growth is largely propelled by rising industrial activity, expanding data centers, air conditioning demand, and ongoing electrification across sectors. It also underscored that overall, global electricity consumption is expected to exceed 29,000 TWh by the end of 2026, growing more than twice as fast as total energy demand, thus benefiting the overall market.

Global Electricity Demand Growth Forecast (2024-2026): Regional Trends, Key Drivers, and Consumption Insights

|

Region |

2024 |

2025 |

2026 |

Key Drivers |

|

Global |

4.4% |

3.3% |

3.7% |

Electrification, data centers, and AC demand |

|

China |

7.0% |

5.0% |

5.7% |

EVs, manufacturing, and services growth |

|

India |

- |

4.0% |

6.6% |

Industrial recovery, rising AC usage |

|

U.S. |

2.1% |

2.3% |

2.2% |

Data centres, AI, manufacturing |

|

Europe |

1.6% |

1.1% |

1.5% |

Slow industrial recovery |

Source: IEA

Challenges

- Complex integration with legacy grid systems: One of the biggest challenges in the smart transformers market is integrating them into aging and heterogeneous power grid infrastructure. Most of the utilities operate very old systems, which are not designed for digital communication or real-time monitoring. At the same time, retrofitting these systems necessitates some additional equipment, software compatibility layers, and grid modernization investments, making it challenging for small-scale players in this sector. Interoperability between different vendors’ systems is also a concern, as standards are not fully uniform in the global dynamics. Therefore, this creates technical complexity and increases deployment timelines, wherein utilities need to plan phased integration to avoid grid instability. As a result, modernization projects often take years, ultimately slowing down the widespread adoption.

- Cybersecurity risks and data vulnerability: Smart transformers are mostly dependent on digital communication networks, IoT sensors, and cloud-based analytics, which makes them extremely susceptible to cybersecurity threats. Any type of unauthorized access, data breaches, or cyberattacks on grid infrastructure can cause severe disruptions, including power outages. As transformers become more connected, the attack surface also increases significantly. In this context, utilities need to make heavy investments in encryption, secure communication protocols, and intrusion detection systems. But still, cybersecurity standards in the power sector are evolving and vary across regions. Therefore, making sure of real-time protection without affecting system performance is considered to be challenging. This risk perception slows down adoption in the market, especially in critical infrastructure sectors such as defense, healthcare, and national grids.

Smart Transformers Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15.8% |

|

Base Year Market Size (2025) |

USD 3.8 billion |

|

Forecast Year Market Size (2035) |

USD 14.2 billion |

|

Regional Scope |

|

Smart Transformers Market Segmentation:

Application Segment Analysis

The smart grid, which is under the application segment, is expected to garner the largest share of 75.7% in the smart transformers market by the end of 2035. The segment’s leadership is mainly propelled by its extensive integration in modern power system operations. This dominance is also supported by the increasing deployment of digitalized grid infrastructure to manage electricity flow, voltage regulation, and real-time load balancing. In August 2024, Siemens expanded its Gridscale X portfolio with two new software products, Protection Data Manager and dynamic line rating, which were launched at CIGRE Paris 2024. These tools help Transmission System Operators manage rising grid complexities by improving data accuracy, preventing outages, and unlocking 10% to 15% extra line capacity. Hence, with such consistent efforts from leading players, the segment will sustain huge dominance in the upcoming years.

Type Segment Analysis

In terms of the type segment, the distribution transformer is anticipated to capture a significant revenue share in the smart transformers market over the forecasted years. The growth of the segment is largely attributable to massive deployment in urban and rural electrification projects. Its extensive usage in voltage regulation and efficient power distribution across residential, commercial, and industrial networks also positions the subtype for solid growth. In this context, Schneider Electric in February 2024 announced the launch of EcoStruxure transformer expert in the UK & Ireland, which is a subscription-based IoT monitoring solution that extends the lifespan of oil transformers and reduces downtime. The company mentioned that this particular system provides real-time health insights, predictive analytics, and risk assessments, thereby enabling data-driven decisions on maintenance and replacements.

Component Segment Analysis

By the conclusion of the forecast period, hardware is anticipated to grow with a considerable share in the smart transformers market. Transformers are capital-intensive physical assets with long replacement cycles. Even as digital monitoring grows, the core transformer unit accounts for most of the system cost, thus allowing the hardware segment to maintain a prominent position. In September 2025, Siemens Energy reported that it is investing USD 259 million with the main goal of expanding its transformer factory in Germany, adding 350 new jobs and boosting production capacity by 50 percent. Besides, it is supported by up to USD 23.5 million in Bavarian funding. The expansion strengthens Nuremberg’s role as a hub for innovation and the energy transition. Hence, such expansion projects by the leading pioneers will help meet rising global demand for large transformers that are highly essential to modern power grids and renewable energy projects.

Our in-depth analysis of the smart transformers market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Type |

|

|

Component |

|

|

Connectivity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Smart Transformers Market - Regional Analysis

APAC Market Insights

The Asia Pacific smart transformers market is forecasted to be the largest region, capturing the highest share of 44.6% during the discussed time frame. The region’s dominance is largely propelled by massive investments in urban electrification, renewable energy integration, smart cities, EV infrastructure, and industrial expansion, which drive demand. At the same time, rapid grid expansion and new transmission infrastructure make smart transformers highly essential for load balancing and automation. As per an article published by IEA, the electricity production reached 15,489,513 GWh in 2023, thereby accounting for almost 51% of global generation, reflecting the rapid growth of 266% since past two decades. Besides, the electricity consumption in the region averaged 3.556 MWh per capita, wherein 26% of final energy use comes from electricity, primarily driven by the industrial sector, which accounts for 53% of total consumption, thus driving huge demand for smart transformers.

The national mandates to modernize power grids, integrate renewable energy sources, and enhance energy efficiency are the crucial factors behind the exponential growth of the market in China. At the same time, the urgent need to manage fluctuating power loads in high-growth industrial and urban centers, ensuring grid stability, is also propelling continued market demand. As per an article published by IEA, the country’s solar PV sector saw booming expansion in 2024, with 277.57 GWAC of new capacity added, bringing total installed capacity to 886 GWAC. It mentioned that PV power generation reached 834.1 TWh, marking a 44% year-on-year increase and supplying about 8% of China’s total electricity consumption, with a utilization rate of 96.8%. In addition, policy reforms in 2024-2025 accelerated market-based renewable integration, with over 50% of new renewable electricity traded through market mechanisms and 4.7 billion green electricity certificates issued in 2024, thus making it suitable for standard market growth.

There is a huge opportunity for the market in India owing to the presence of government initiatives for digital infrastructure and smart cities. The sector is seeing increased adoption of IoT-enabled, real-time monitoring solutions across distribution networks as well as industrial applications. Based on government data published in June 2024, India’s smart grid modernization under the National Smart Grid Mission shows strong progress through ongoing smart grid deployments. In Rajasthan JVVNL, 6 urban towns, the project installed 145,343 smart meters, with operations and maintenance started in November 2023, supported by a government-approved project cost of almost USD 10.5 million. In Chandigarh Sub-Division 5, 24,214 smart meters and feeder automation systems under AMI, SCADA, and DTMU were deployed, with a total project cost of USD 3.4 million. Such initiatives with government support will readily bolster the market’s growth and exposure in the years ahead.

North America Market Insights

The smart transformers market in North America has acquired a prominent position in the global dynamics, strongly propelled by intensive grid modernization efforts, the integration of renewable energy sources, and the necessity for increased power system reliability and efficiency. The market is witnessing a very high technological adoption to improve operational efficiency and reduce energy losses. In March 2024, the National Renewable Energy Laboratory, which is funded by the U.S. Department of Energy, reports that demand for distribution transformers in the U.S. could increase by 160% to 260% by 2050 when compared to 2021 levels due to electrification, aging infrastructure, and rising extreme weather risks. These transformers are highly essential for stepping down and regulating electricity across the grid, and their demand is expected to rise sharply with the growth in electric vehicles, buildings, and renewable energy integration.

The continued federal investments and increasing electric vehicle adoption have led the utilities to shift toward digital substations for enhanced efficiency, thus uplifting the smart transformers market in the U.S. Key factors that are propelling this growth include the necessity to handle and provide dynamic load management, thereby aligning with national goals for cleaner, more reliable power distribution. In November 2025, the U.S. DOE reported that it is modernizing the grid by enhancing technologies such as the dynamic line rating, which uses real-time weather data to safely boost transmission capacity. It states that data centers consumed 4.4% of U.S. electricity in 2023, a share expected to rise to 12% by 2028, adding 130 GW of demand. Therefore, rising deployment of grid-enhancing technologies and increasing transmission congestion effectively drive demand for smart transformers by enabling proper load management.

The urgent need to support widespread electrification in transportation and industry is the main factor driving the market in Canada. At the same time, strong investments in high-voltage direct current systems, along with federal support for manufacturing and clean technology adoption, are fueling demand for both smart power transformers and distribution units. In September 2025, the government of Canada, through the Federal Economic Development Agency for Southern Ontario, announced a generous USD 6 million investment with a prime focus to support Northern Transformer’s new large power transformer manufacturing facility in Innisfil, Ontario. It will be a 183,000-square-foot facility, expected to open in 2028, and is especially designed to significantly increase domestic transformer production capacity to meet rising demand from utilities driven by grid modernization and electrification.

Europe Market Insights

Europe smart transformers market is maintaining a strong position in the global dynamics, highly attributable to stringent environmental regulations. As the regional nations are making a shift away from fossil fuels and expanding charging infrastructure for electric vehicles, utilities are deploying these advanced devices to manage, monitor, and control power flows to enhance grid flexibility and reliability. In April 2026, the article published by the European Commission revealed that out of the 235 cross-border energy projects announced, 113 focus on electricity, offshore, and smart electricity grids, directly supporting the integration of renewables. These smart grid projects are especially designed to modernize infrastructure, enhance interconnectivity, and improve efficiency across Europe’s energy system. Therefore, by streamlining permits and enabling financing, they will accelerate the deployment of smart transformers and grid technologies, effectively tackling bottlenecks and boosting resilience for the clean energy transition.

The shift towards digital substations equipped with IoT-enabled sensors and the adoption of improved power electronics, such as solid-state transformers, are responsible for uplifting the smart transformers market in Germany. Demand is continuously expanding across industrial automation, electric vehicle charging networks, and smart city projects, in which these intelligent units efficiently optimize energy efficiency and facilitate two-way power flows. In September 2023, Siemens Smart Infrastructure announced projects in Hamburg and Saarlouis to expand electric bus charging infrastructure, integrating systems directly into the medium-voltage grid. This particular solution includes transformer station deployment, planning, and installation of high-power charging points for large-scale e-bus fleets. These systems are connected to digital charging and depot management platforms to optimize energy use and grid stability, thus suitable for bolstering the market’s growth in the overall country.

The smart transformers market in the UK has achieved strong momentum as the nation intensifies its efforts to achieve net-zero targets and modernize its aging electrical grid. Some of the catalyzing factors in the country’s market include the transition toward digital substations and the deployment of IoT-enabled sensors that facilitate predictive maintenance as well as enhance grid resilience. In November 2025, National Grid began upgrading its Didcot substation in Oxfordshire, with Linxon appointed as principal contractor to support new connections for data centres and battery storage, thereby strengthening the country’s digital and energy infrastructure. The project includes extending the 400kV substation with additional bays and installing supergrid transformers, along with a new 132kV GIS facility using SF6-free technology from Hitachi Energy, hence making it suitable for standard market growth.

Key Smart Transformers Market Players:

- ABB Ltd (Switzerland)

- Hitachi Energy Ltd (Switzerland)

- Schneider Electric SE (France)

- Siemens Energy AG (Germany)

- SGB-SMIT Group (Germany)

- GE Vernova (U.S.)

- Eaton Corporation plc (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- Howard Industries Inc. (U.S.)

- Emerson Electric Co. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Toshiba Energy Systems & Solutions Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Nissin Electric Co., Ltd. (Japan)

- Hammond Power Solutions (Canada)

- Hyundai Electric & Energy Systems Co., Ltd. (South Korea)

- Hyosung Heavy Industries Corporation (South Korea)

- Bharat Heavy Electricals Limited (BHEL) (India)

- CG Power & Industrial Solutions Ltd. (India)

- Transformers and Rectifiers (India) Ltd. (India)

- TBEA Co., Ltd. (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ABB Ltd has registered itself as a predominant player in this sector, and it benefits from a strong position in electrification and grid automation. The firm is extensively focused on digitally enabled transformer systems, which are incorporated with smart sensors, IoT-based monitoring, and predictive analytics platforms.

- Siemens Energy AG is leading in the global market through its advanced grid technologies and digital energy solutions. The company is highly focused on high-voltage transformer systems, which are integrated with grid stabilization, automation, and digital twin technology.

- Hitachi Energy Ltd is identified as a major global player that specializes in terms of high-voltage transformers and smart grid solutions. Besides, the company has been expanding manufacturing capacity, especially in North America and Europe, with the main goal of meeting the rising demand for grid infrastructure.

- GE Vernova is yet another prominent player in this field and is the energy division of General Electric Company, a key competitor in the market with a strong focus on grid modernization and electrification. The firm provides advanced transformer solutions integrated with digital monitoring, analytics, and grid optimization systems.

- Schneider Electric SE is a leading player in the smart transformer ecosystem, which is especially known for its expertise in energy management and digital automation. The company is highly concentrated on EcoStruxure-enabled solutions that provide real-time visibility and energy optimization for transformers as well as substations.

Below is the list of some prominent players operating in the global market:

The market is being dominated by global giants such as ABB, Siemens Energy, Hitachi Energy, Schneider Electric, and GE Vernova, which lead through strong R&D and digital grid integration capabilities. The leading pioneers in the market are highly focused on smart monitoring, predictive maintenance, and eco-efficient transformer designs with the main goal to support renewable-heavy grids. Meanwhile, players such as Mitsubishi Electric, Toshiba, Hyundai Electric, and Hyosung efficiently strengthen competition in high-voltage and industrial applications. Some of the strategic initiatives adopted by the leading players in this field are digitalization, factory expansion, and grid modernization partnerships. In September 2023, Hitachi Energy inaugurated a transformer factory in China that encompasses advanced digital manufacturing and sustainability measures to meet rising grid electrification needs. The modern facility supports major HVDC projects, thus positively impacting the market’s growth.

Corporate Landscape of the Smart Transformers Market:

Recent Developments

- In March 2026, GE Vernova announced almost USD 200 million to build a new Hai Phong facility in Vietnam, expanding its manufacturing capacity for HVDC transformers to meet rising global electrification demand.

- In October 2024, Hammond Power Solutions introduced HPS smart transformers by integrating IIoT-enabled monitoring for medium and low voltage systems to deliver predictive maintenance and real-time analytics. This innovation enhances operational efficiency, prevents costly downtime, and supports applications from renewable energy to data centers.

- Report ID: 3466

- Published Date: Apr 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.