Smart Grid Network Market Outlook:

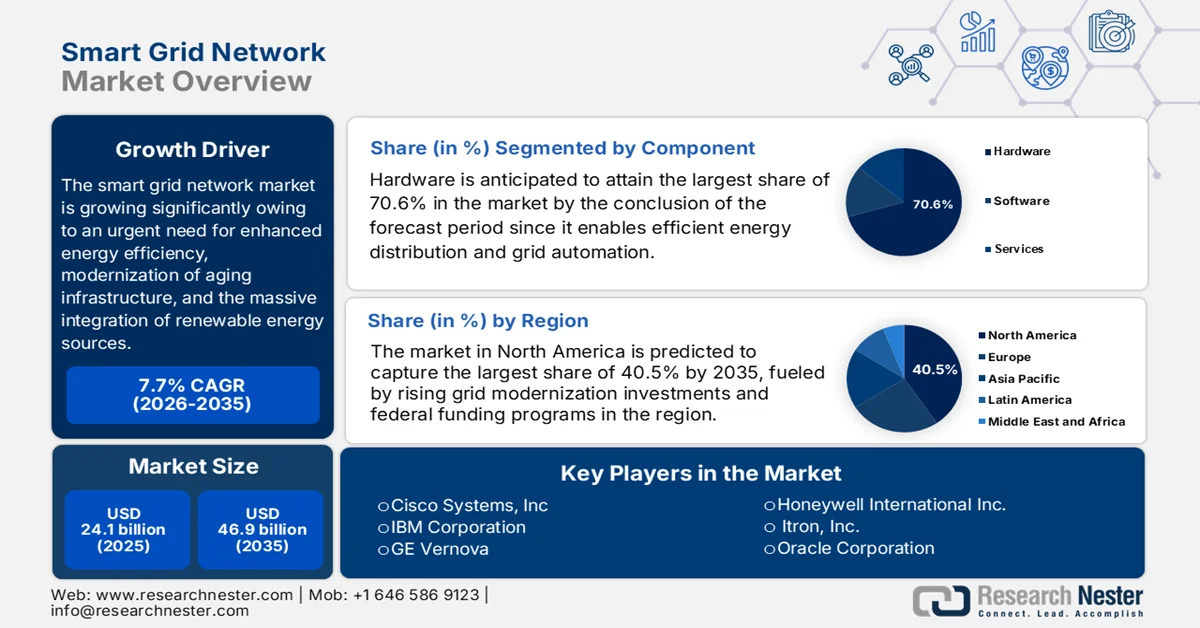

Smart Grid Network Market size was valued at USD 24.1 billion in 2025 and is anticipated to grow to USD 46.9 billion by 2035, registering a CAGR of 7.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of smart grid network is assessed at USD 25.9 billion.

The global smart grid network market is poised for extensive growth in the years ahead, owing to an urgent need for enhanced energy efficiency, modernization of aging infrastructure, and the massive integration of renewable energy sources. In this context, the International Energy Agency reported that a smart grid uses advanced digital technologies to manage electricity efficiently, but global investment needs to be more than double by 2030 to align with Net Zero by 2050. It also mentioned that Europe in 2022 announced an action plan with almost USD 633 billion by 2030, including USD 184 billion for digitalization. Meanwhile, China has invested almost USD 442 billion during 2021‑2025, whereas Japan launched a USD 155 billion programme in 2022. India introduced a USD 38 billion scheme in 2022, and the U.S. announced USD 10.5 billion under GRIP in 2022; Canada is contributing USD 100 million to smart grid deployment; thus, all of these investments contribute to wider smart grid network market expansion.

Furthermore, the continuously expanding electric vehicle charging infrastructure effectively fuels smart grid network market expansion across both developed and emerging economies. In addition, utilities across the globe are focused on reducing outages and improving operational flexibility. Hence, with this focus, the industry is making a shift toward software solutions and real-time monitoring, positioning smart grid technology as a highly essential component of global sustainability and carbon emission reduction strategies. As per the official statistics published by IEA in 2025, global EV charging infrastructure has grown rapidly, with public chargers doubling since 2022 to surpass 5 million worldwide. Besides, it is mentioned that in 2024 alone, 1.3 million chargers were added, wherein China accounted for 65% of global chargers and 60% of EVs, thus all of these factors together position the market for strong upliftment.

Global Electric Vehicle Charging Infrastructure Statistics 2024: Regional Deployment, Growth Trends, and Charging Capacity Breakdown

|

Parameter |

2024 Value |

Growth / Share |

Key Observation |

|

Global public chargers |

>5 million |

+30% YoY |

Doubled since 2022 |

|

New chargers added (2024) |

1.3 million |

Highest annual addition |

Equivalent to the 2020 global stock |

|

China share |

65% stock |

60% EV LDV stock |

Dominant global market |

|

Europe's total chargers |

>1 million |

+35% YoY |

Strong Europe-wide expansion |

|

Netherlands |

180,000+ |

Largest in Europe |

Dense urban rollout |

|

Germany |

160,000 |

High maturity market |

Strong policy support |

|

France |

155,000 |

Rapid expansion |

Corridor-focused growth |

|

U.S. |

200,000 |

+20% YoY |

USD 5 billion federal funding program |

|

Fast chargers (global) |

2 million |

Strong growth |

China = 80% growth contribution |

|

Ultra-fast chargers |

>50% YoY growth |

10% share of fast chargers |

Falling cost (-20% since 2022) |

|

India |

40,000 added (2024) |

Policy-driven growth |

USD 240 million allocation |

|

Brazil |

12,000+ |

Rapid expansion |

Emerging market scaling |

|

SE Asia (ID, TH, MY, VN) |

24,000+ |

9x since 2022 |

Strong policy + private investment |

Source: IEA

Key Smart Grid Network Market Insights Summary:

Regional Highlights:

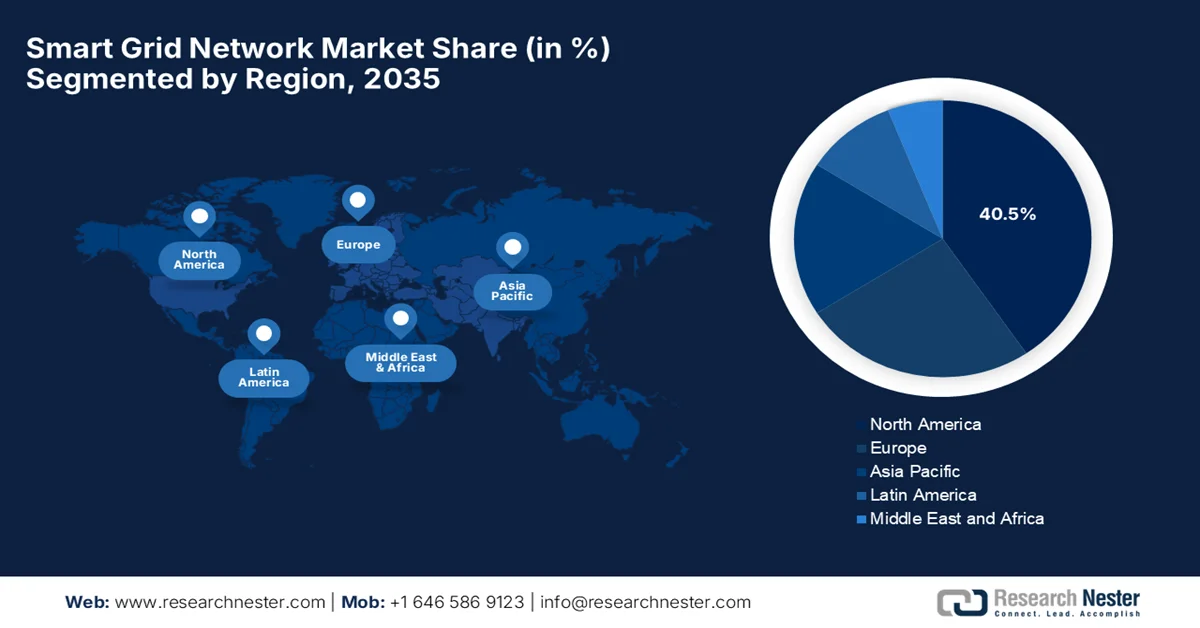

- North America in the smart grid network market is projected to hold a dominant 40.5% share by 2035, reinforced by robust grid modernization investments and federal funding initiatives accelerating advanced metering and infrastructure upgrades

- Asia Pacific is expected to witness substantial growth during 2026–2035, fueled by rapid urbanization and escalating electricity demand necessitating advanced grid infrastructure expansion

Segment Insights:

- The hardware segment in the smart grid network market is projected to capture a 70.6% share by 2035, underpinned by its critical role as the backbone of grid modernization enabling efficient energy distribution and automation

- The new installation segment is expected to secure a significant revenue share over 2026-2035, propelled by expanding electrification projects and the growing need for advanced grid architectures

Key Growth Trends:

- Rising electricity demand & load complexity

- Integration of renewable energy sources

Major Challenges:

- High initial investment costs

- Cybersecurity risks

Key Players: Cisco Systems, Inc. (U.S.), International Business Machines Corporation (IBM) (U.S.), GE Vernova (U.S.), Honeywell International Inc. (U.S.), Itron, Inc. (U.S.), Oracle Corporation (U.S.), S&C Electric Company (U.S.), Siemens AG (Germany), Schneider Electric SE (France), ABB Ltd. (Switzerland), DNV (Norway), Eaton Corporation plc (Ireland), Landis+Gyr Group AG (Switzerland).

Global Smart Grid Network Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 24.1 billion

- 2026 Market Size: USD 25.9 billion

- Projected Market Size: USD 46.9 billion by 2035

- Growth Forecasts: 7.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Saudi Arabia

Last updated on : 15 April, 2026

Smart Grid Network Market - Growth Drivers and Challenges

Growth Drivers

- Rising electricity demand & load complexity: The aspect of rapid urbanization, industrialization, and population growth remarkably increases the global electricity consumption. In this context, the traditional grids find it difficult to manage fluctuating and peak loads, which drives the adoption of smart grid systems that enable efficient load balancing. In February 2026, IEA stated that the global electricity demand is projected to grow by 3.5% annually through 2030, rising 2.5 times faster when compared to overall energy demand. Besides, renewables and nuclear are set to provide 50% of global power by the end of 2030, which is up from 42% currently. More than 2,500 GW of projects are stalled in grid connection queues, but reforms could unlock 1,600 GW of capacity. Also, meeting this demand will require grid investments to rise by 50% by 2030, prompting a favorable ecosystem for the smart grid network market.

- Integration of renewable energy sources: The worldwide shift towards solar, wind, and other intermittent renewables is the major growth driver for the smart grid network market. These smart grids help manage variability by deliberately enabling two-way power flow, grid stability support, better forecasting, and dispatching, hence this makes renewable integration more reliable and scalable. As per the December 2025 article published by IEA, global renewable energy is experiencing rapid expansion, driven mainly by solar PV and wind, with renewables expected to supply 43% of global power generation by 2030, which is up from 32% in 2024. At the same time, the total global renewable capacity additions are projected to reach about 4,605 GW between 2025 and 2030, reflecting accelerated energy transition momentum worldwide, thus benefiting the overall smart grid network market growth.

Global Renewable Energy Growth Forecast (2024-2030): Capacity, Generation Share & Expansion Trends

|

Indicator |

2024 |

2030 (Forecast) |

|

Share of renewables in power generation |

32% |

43% |

|

Share of VRE in power generation |

15% |

28% |

|

Total renewable capacity additions (2025–2030) |

- |

4,605 GW |

|

Annual renewable capacity additions |

683 GW |

890 GW |

|

Share of solar PV & wind in new additions |

- |

96% |

|

Utility-scale renewable drivers (Auctions & tenders) |

- |

57% |

|

Distributed solar PV share of PV expansion |

- |

42% |

Source: IEA

- Demand for real-time data, automation & analytics: Utilities across the globe are mostly dependent on IoT sensors, AI, ML analytics, smart meters, i.e., AMI systems. These technologies efficiently improve fault detection, outage management, and predictive maintenance, thereby reducing the overall operational costs and improving reliability. In this context, Argonne National Laboratory in May 2024 reported that artificial intelligence is revolutionizing grid maintenance by enabling predictive models that forecast equipment failures before they occur. Its researchers have shown AI can cut maintenance costs by 43% to 56%, reduce unnecessary crew visits by 60% to 66%, and boost profits by almost 3% to 4%. With over 240,000 transmission lines and 50 million transformers, many nearing the end of life, AI-driven asset health monitoring is highly essential, thus positively impacting smart grid network market growth and exposure.

Challenges

- High initial investment costs: One of the major barriers to the smart grid network market is the extensive upfront capital for deployment. Utilities need to make heavy investments in advanced metering infrastructure, communication networks, sensors, and grid automation technologies. In addition, revamping the aged transmission networks and distribution systems adds an extra financial burden for pioneers in this sector. In the case of developing economies, budget constraints and limited access to funding ultimately lead to slower adoption. Even in developed markets, utilities can face regulatory hurdles when attempting to pass costs on to consumers. Despite the existence of long-term efficiency gains, the initial cost factor hampers the widespread smart grid network implementation, thus negatively impacting the smart grid network market’s growth.

- Cybersecurity risks: The smart grids are mostly reliant on digital communication networks; as a result, they become susceptible to cyberattacks. At the same time, threats, i.e., data breaches, ransomware, and infrastructure sabotage, pose severe risks to grid stability as well as national security. Besides, the cyber-attack can cause disruptions to the electricity supply across large regions, in turn causing economic and social consequences. Therefore, to address these concerns, utilities need to make investments in cybersecurity frameworks, which include encryption, intrusion detection, and secure communication protocols. However, the evolving nature of cyber threats makes it difficult to maintain robust defenses. Furthermore, the incorporation of IoT devices increases the attack surface, intensely complicating security management in the smart grid network market.

Smart Grid Network Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.7% |

|

Base Year Market Size (2025) |

USD 24.1 billion |

|

Forecast Year Market Size (2035) |

USD 46.9 billion |

|

Regional Scope |

|

Smart Grid Network Market Segmentation:

Component Segment Analysis

In the component segment, hardware is anticipated to attain the largest share of 70.6% in the smart grid network market by the conclusion of the forecast period. The segment consists of critical infrastructure such as smart meters, sensors, communication devices, and automated control equipment, which collectively enable efficient energy distribution and grid automation. In the upcoming years, the hardware segment is expected to continue attracting remarkable investment and innovation as the backbone of smart grid modernization efforts. As per the article published by Press Information Bureau (PIB) in March 2022, the National Smart Grid Mission empowers consumers through smart grids and smart meters, thereby helping them to manage electricity usage more efficiently and reduce bills. Besides, the large-scale prepaid smart meter deployment in Bihar has improved revenue collection by up to 20% for distribution companies, thus indicating a wider segment scope.

Installation Type Segment Analysis

Based on installation type, the new installation is predicted to grow with a significant revenue share in the smart grid network market during the stipulated timeframe. The growth of the segment is largely propelled by rapid electrification projects in emerging economies, along with large-scale grid expansion to support industrialization and urban development. The increasing deployment of distributed energy resources is also creating an extensive need for entirely new, grid architectures rather than retrofitted systems. As stated by the PIB article in February 2026, under the revamped distribution sector scheme, smart metering works have been sanctioned for 45 distribution utilities across 28 States, UTs by covering 197.9 million consumers along with 5.253 million distribution transformers and 205,000 feeders, with 52.8 million smart meters installed across India as of December 2025, thus reflecting the subtype’s continued growth.

End user Segment Analysis

The utilities sub-segment, which is a part of the end user, is expected to grow at a noteworthy pace over the forecasted years. Utilities are primary end users since they are directly responsible for generation, transmission, and distribution system efficiency and stability. Their investment decisions are highly driven by the need to manage rising peak demand, integrate variable renewable energy sources, and ensure an uninterrupted power supply under more complex grid conditions. As a result, utilities are prioritizing the deployment of intelligent grid infrastructure. In March 2024, Itron announced that Xcel Energy deployed 2 million Gen 5 Riva distributed intelligence-enabled smart meters as part of its advanced metering infrastructure and industrial IoT network. The deployment efficiently enhances outage detection, reduces field operations, and thus contributes to wider smart grid network market expansion.

Our in-depth analysis of the smart grid network market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Installation Type |

|

|

End user |

|

|

Technology |

|

|

Communication Network Type |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Smart Grid Network Market - Regional Analysis

North America Market Insights

The North America smart grid network market is anticipated to garner the largest share of 40.5% by the end of the forecast period. The region’s dominance is mainly propelled by strong grid modernization investments and federal funding programs. The important growth drivers for the regional market include significant investments in advanced metering infrastructure, demand response programs, and enhanced cybersecurity measures. In November 2024, the U.S. Energy Information Administration reported that the total utility spending on electricity infrastructure rose to USD 320 billion in 2023, wherein the capital investment was the primary driver of this growth. Distribution infrastructure recorded the strongest increase, as utilities expanded and upgraded networks to improve resilience against extreme weather and integrate renewable energy sources. Also, the investments in terms of new technologies such as smart meters, sensors, automated controls, and energy storage have become a key part of modern grid development.

U.S. Electric Utility Infrastructure Spending Trends 2023: Grid Modernization, Distribution Growth & Smart Technology Investments

|

Segment |

2023 |

Growth Trend |

|

Total utility electricity infrastructure spending |

USD 320 billion |

+12% |

|

Distribution system capital spending |

USD 50.9 billion |

+160% since 2003 |

|

Transmission spending |

USD 27.7 billion |

Nearly 3x increase |

|

Production spending |

Declined 24% |

Shift due to fuel cost changes |

|

Overhead infrastructure spending |

USD 17.4 billion |

+220% since 2003 |

|

Underground line investment |

USD 11.8 billion |

More than doubled |

|

Smart meters, sensors & customer-side infrastructure |

Part of USD 5.1 billion (2023) |

+84% since 2003 |

|

Energy storage (distribution level) |

USD 723 million (2023) |

Sharp increase |

Source: U.S. EIA

The growing renewable energy integration and high demand for advanced, resilient utility infrastructure are the main factors responsible for the growth of the smart grid network market in the U.S. Major investment is focused on deploying smart metering, AI-driven management, and electric vehicle charging infrastructure to enhance both distribution efficiency and reliability. In this context, the International Council on Clean Transportation in April 2025 reported that by the end of 2024, the U.S. had deployed about 204,000 public and workplace chargers for light-duty EVs, growing at an average annual rate of 25%. Besides, in 2024 alone, more than 40,000 chargers were added, with Level 2 chargers rising to 153,000 and DC fast chargers to 51,000, which is considered to be a 56% increase from 2023. EV sales also surged 1.5 million in 2024, accounting for 10% of new vehicles, bringing total EV stock to 6.3 million, thus suitable for standard smart grid network market growth.

Influenced by the presence of federal support and provincial initiatives, utilities are making a shift from traditional one-way distribution to two-way, data-driven systems, thus responsibly uplifting the smart grid network market in Canada. In addition, the industry is witnessing a major shift towards virtual power plants and distributed energy resource management, allowing for better balancing of supply and demand. Based on the government data published in December 2024, Canada’s National Smart Grid initiative focuses on modernizing electricity networks by improving technology-grid interfaces and enabling interoperability. Besides, this particular project emphasizes inverter-grid connections, distributed energy resource control and aggregation, and advancing grid integration standards. By testing advanced inverter functions and behind-the-meter technologies, it supports renewable integration and flexibility, thus denoting a positive smart grid network market outlook.

APAC Market Insights

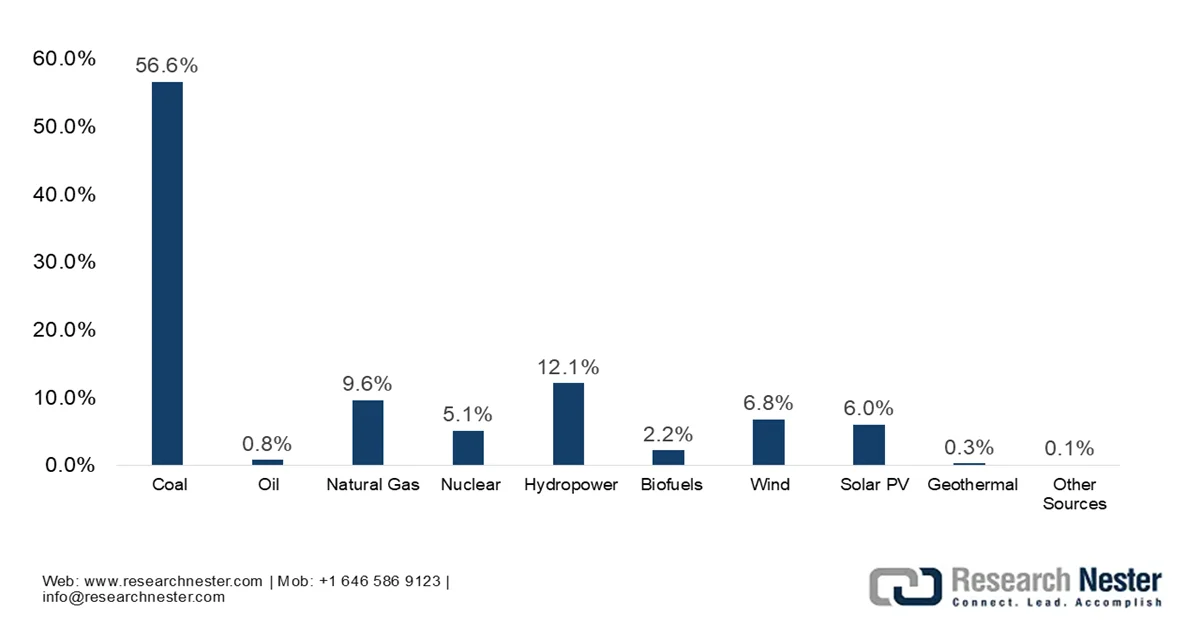

The Asia Pacific smart grid network market is projected for exponential growth in the next decade, mainly attributable to urbanization, rising electricity demand, and strong governmental focus on grid modernization and decarbonization. At the same time, major investments in renewable energy integration, particularly in solar and wind, along with the necessity for robust, secure communication infrastructure, are accelerating the adoption of advanced digital solutions. In this context, electricity generation in the Asia Pacific is still heavily dominated by fossil fuels, with coal alone accounting for 56.6% of total generation in 2023, followed by natural gas at 9.6%. The region produced around 15.49 million GWh of electricity in 2023, representing 51% of global electricity output, driven largely by rapid growth in countries such as China and India, thus positively impacting the market’s growth and exposure in the overall region.

Asia Pacific Electricity Generation Mix (2023): Fuel-wise Share of Coal, Gas, Oil, and Renewable Energy Sources

Source: IEA

In China, the smart grid network market is evidently supported by the urgent need for improved energy efficiency. The country’s market is also supported by government policies, with key initiatives focusing on ultra-high voltage, transmission, intelligent distribution systems, and widespread digital upgrading of the power grid. In February 2026, the country’s State Grid Corporation of China (SGCC) introduced a five-year investment plan with a total worth of USD 574 billion for 2026 to 2030, which is a 40% jump from the previous cycle. This particular plan has its main priority towards west-to-east power transmission, boosting cross-provincial capacity by 30%, and advancing microgrid solutions to support carbon peaking goals. This comes as China’s electricity consumption hit a historic 10 trillion kilowatt-hours in 2025, reflecting a 5% annual rise. Hence, this, coupled with the presence of key smart grid network market players, is leading to a transformation to support cleaner energy and increased demand.

In India, the smart grid network market is gaining momentum, facilitated by suitable government initiatives such as the National Smart Grid Mission and the Revamped Distribution Sector Scheme. These schemes are highly focused on modernizing infrastructure and deploying advanced metering infrastructure with the main goal of reducing high transmission losses and improving grid reliability. In this context, Maharashtra State Electricity Distribution Co. Ltd and the Global Energy Alliance in October 2025 signed a Statement of Intent to modernize the state’s power grid through digitalization and AI-based solutions. This particular collaboration will deliberately strengthen grid reliability, integrate renewables, and reduce transmission losses by leveraging advanced analytics and the Alliance’s DUET program. Furthermore, major metropolitan areas lead in terms of adoption, utilizing technologies such as distribution automation, energy storage, and AI-enabled analytics to boost efficiency.

Europe Market Insights

Europe smart grid network market is maintaining a strong position in the global dynamics, largely driven by regional decarbonization targets, increasing adoption of electric vehicles, and the need for integration of decentralized renewable energy sources. The market is strongly supported by significant European Union initiatives and regulatory mandates, which are aimed at grid modernization. In this context, the revised energy efficiency directive that came into force in October 2023 makes energy efficiency a binding principle, requiring it to be considered in all major policy and investment decisions. It sets a collective target of reducing energy consumption by 11.7% by 2030, with stricter annual savings obligations rising to 1.9% by 2028-2030. In addition, this particular directive also prioritizes alleviating energy poverty, improving consumer protections, and enhancing efficiency in data centres, heating, cooling, and industrial audits to support the region’s climate neutrality goals, thus denoting a positive outlook for the market’s exposure.

The smart grid network market in Germany is growing, mainly propelled by a prime focus to support the nation's energy transition, focusing on integrating volatile renewable energy sources. At the same time, due to the need for decarbonization, the market emphasizes digital infrastructure, including intelligent meters, enhanced storage, and automated management systems to handle localized energy production. From 2025, Germany has rolled out dynamic electricity tariffs and smart meters under the Digitization of the Energy Transition Law, with the main goal to modernize consumption and integrate renewables. The article published by Smart Meter Europe in January 2025 mentioned that households that are consuming over 6,000 kWh annually have been prioritized, with targets of 50% adoption by 2028 and 95% by 2030. These measures promise efficiency and flexibility, thus making them suitable for bolstering the country’s smart grid network market.

The government initiatives to decarbonize, modernize electricity infrastructure, and facilitate renewable energy integration are responsible for uplifting the smart grid network market in the UK. Growth is also propelled by increased investment in automation, software, and hardware to increase energy efficiency. Based on the government data published in March 2026, the Department for Energy Security and Net Zero consultation proposed a post-2025 smart metering framework to improve consumer experience, ensure meters operate reliably, and support the Clean Power 2030 mission. In this context, it sets a new obligation for energy suppliers to complete the domestic smart meter rollout by 2030, fix non-smart traditional mode meters within 90 days, and transition systems to 4G before 2G/3G shutdown by 2033. The framework enables a flexible, modern, and fully digital smart grid system, hence positively influencing the market’s growth.

Key Smart Grid Network Market Players:

- Cisco Systems, Inc. (U.S.)

- International Business Machines Corporation (IBM) (U.S.)

- GE Vernova (U.S.)

- Honeywell International Inc. (U.S.)

- Itron, Inc. (U.S.)

- Oracle Corporation (U.S.)

- S&C Electric Company (U.S.)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- ABB Ltd. (Switzerland)

- DNV (Norway)

- Eaton Corporation plc (Ireland)

- Landis+Gyr Group AG (Switzerland)

- Gridspertise S.r.l. (Italy)

- Hitachi Energy Ltd. (Japan)

- Fujitsu Limited (Japan)

- Wipro Limited (India)

- Power Grid Corporation of India Limited (India)

- Trilliant Holdings, Inc. (U.S.)

- EDMI Limited (Malaysia)

- LS Electric Co., Ltd. (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Siemens AG has registered itself as a predominant leader in smart grid networks, which is offering advanced grid automation, digital twin technology, and IoT-enabled communication platforms. The company is highly focused on building autonomous grid ecosystems with real-time monitoring and analytics.

- Schneider Electric SE is yet another dominant force in this field, which specializes in energy management and automation, with a strong focus on smart grid communication infrastructure and digital energy platforms. Besides, the firm is focused mainly on sustainability and electrification, thereby making it suitable for its smart grid solutions with global decarbonization goals.

- ABB Ltd. is a major player in grid automation and network control systems, which is providing solutions such as SCADA, distribution management systems, and communication infrastructure. The company is highly focused on enabling real-time grid visibility and reliability through advanced digital technologies.

- Cisco Systems, Inc. plays a pivotal role in the market by providing secure communication infrastructure, networking hardware, and IoT connectivity solutions. In addition, the company proactively collaborates with utilities and technology partners to deploy IP-based grid networks and edge computing solutions.

- GE Vernova delivers smart grid solutions that include grid software, advanced analytics, and network management systems. The firm is highly focused on integrating renewable energy sources into the grid while maintaining stability and efficiency.

Below is the list of some prominent players operating in the global smart grid network market:

The smart grid network market is a moderately consolidated landscape, which is being led by global giants such as Siemens, Schneider Electric, ABB, and GE Vernova, along with strong technology players such as Cisco and IBM. Competition in this field is largely driven by digitalization, wherein firms are proactively making investments in AI, IoT, and cloud-based grid management platforms. At the same time, strategic initiatives adopted by the players are mergers & acquisitions, partnerships with utilities, and expansion into emerging markets. Companies are also focusing on cybersecurity and real-time data analytics to strengthen network reliability. For instance, in February 2026, DNV announced the acquisition of Smarter Power Solutions Pty Ltd with the main goal of establishing a global center of excellence for grid‑connection engineering in Australia. This move deliberately strengthens DNV’s technical leadership in advanced grid integration and accelerates renewable adoption.

Corporate Landscape of the Smart Grid Network Market:

Recent Developments

- In January 2026, ABB announced the acquisition of Netcontrol, one of the prominent providers of advanced grid automation solutions, to strengthen its portfolio and support utilities in digitalizing power grids. This particular deal will integrate Netcontrol’s offerings into ABB’s global distribution solutions.

- In November 2025, Schneider Electric unveiled its one digital grid platform, which is an AI-enabled solution that unifies planning, operations, and asset management to help utilities modernize without costly infrastructure overhauls.

- Report ID: 3465

- Published Date: Apr 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.