Global Silicone Market

1. An Outline of the Global Silicone Market

1.1. Market Definition and Segmentation

1.2. Study Assumptions and Abbreviations

2. Research Methodology & Approach

2.1. Primary Research

2.2. Secondary Research

2.3. Data Triangulation

2.4. SPSS Methodology

3. Executive Summary

4. Growth Drivers

5. Major Roadblocks

6. Opportunities

7. Prevalent Trends

8. Government Regulation

9. Growth Outlook

10. Competitive White Space Analysis – Identifying Untapped Market Gaps

11. Risk Overview

12. SWOT

13. Technological Advancement

14. Technology Maturity Matrix for the Silicone Market: Recent News

15. Regional Demand

16. Global Silicone by Geography – Strategic Comparative Analysis

17. Strategic Segment Analysis: Silicone Demand Landscape

18. Silicone Demand Trends Driven by Expanding Electronics, Healthcare, Personal Care, and Advanced Manufacturing Industries (2026-2036)

19. Root Cause Analysis (RCA) for discovering problems of the Silicone Market

20. Porter Five Forces

21. PESTLE

22. Comparative Positioning

23. Global Silicone – Key Player Analysis (2036)

24. Competitive Landscape: Key Suppliers/Players

25. Competitive Model: A Detailed Inside View for Investors

26. Company Market Share, 2036 (%)

26.1. Dow

26.2. DuPont

26.3. Wacker Chemie AG

26.4. Momentive Performance Materials

26.5. Shin-Etsu Chemical Co., Ltd.

26.6. Mitsubishi Chemical Group Corporation

26.7. Evonik Industries AG

26.8. Elkem ASA

26.9. KCC Corporation

26.10. Gelest Inc.

27. Global Silicone Market Outlook

27.1. Market Overview

27.1.1. Market Revenue by Value (USD Billion), by Volume (Thousand Tons), and Compound Annual Growth Rate (CAGR)

27.2. Silicone Market Segmentation Analysis (2026-2036)

27.2.1. By Product Type

27.2.1.1. Fluids, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.2. Gels, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.3. Resins, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.4. Elastomers, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.4.1. High-Temperature Vulcanized (HTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.4.2. Liquid Silicone Rubber (LSR), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.4.3. Room Temperature Vulcanized (RTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.5. Adhesives and Sealants, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.6. Emulsions, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1. By End use Industry

27.2.1.1. Electronics, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.2. Construction, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.3. Healthcare, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.4. Personal Care and Consumer Goods, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.5. Energy and Utilities, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.6. Industrial Processes, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2. Regional Synopsis, Value (USD Billion), 2026-2036

27.2.2.1. North America Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.2.2. Europe Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.2.3. Asia Pacific Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.2.4. Latin America Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.2.5. Middle East and Africa Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

28. North America Market

28.2. Overview

28.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

28.2.2. Increment $ Opportunity Assessment, 2026-2036

28.3. Segmentation (USD Billion), 2026-2036, By

27.2.2. By Product Type

27.2.2.1. Fluids, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.2. Gels, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.3. Resins, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.4. Elastomers, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.4.1. High-Temperature Vulcanized (HTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.4.2. Liquid Silicone Rubber (LSR), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.4.3. Room Temperature Vulcanized (RTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.5. Adhesives and Sealants, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.6. Emulsions, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1. By End use Industry

28.3.1.1. Electronics, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.2. Construction, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.3. Healthcare, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.4. Personal Care and Consumer Goods, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.5. Energy and Utilities, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.6. Industrial Processes, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2. Country Level Analysis, Value (USD Billion)

28.3.2.1. U.S. Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

28.3.2.2. Canada Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29. Europe Market

29.2. Overview

29.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

29.2.2. Increment $ Opportunity Assessment, 2026-2036

29.3. Segmentation (USD Billion), 2026-2036, By

27.2.3. By Product Type

27.2.3.1. Fluids, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.2. Gels, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.3. Resins, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.4. Elastomers, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.4.1. High-Temperature Vulcanized (HTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.4.2. Liquid Silicone Rubber (LSR), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.4.3. Room Temperature Vulcanized (RTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.5. Adhesives and Sealants, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.6. Emulsions, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1. By End use Industry

29.3.1.1. Electronics, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.2. Construction, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.3. Healthcare, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.4. Personal Care and Consumer Goods, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.5. Energy and Utilities, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.6. Industrial Processes, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2. Country Level Analysis, Value (USD Billion)

29.3.2.1. UK Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.2. Germany Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.3. France Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.4. Italy Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.5. Spain Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.6. Netherlands Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.7. Russia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.8. Switzerland Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.9. Poland Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.10. Belgium Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.2.11. Rest of Europe Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30. Asia Pacific Market

30.2. Overview

30.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

30.2.2. Increment $ Opportunity Assessment, 2026-2036

30.3. Segmentation (USD Billion), 2026-2036, By

27.2.4. By Product Type

27.2.4.1. Fluids, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.2. Gels, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.3. Resins, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.4. Elastomers, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.4.1. High-Temperature Vulcanized (HTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.4.2. Liquid Silicone Rubber (LSR), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.4.3. Room Temperature Vulcanized (RTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.5. Adhesives and Sealants, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.6. Emulsions, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1. By End use Industry

30.3.1.1. Electronics, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.2. Construction, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.3. Healthcare, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.4. Personal Care and Consumer Goods, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.5. Energy and Utilities, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.6. Industrial Processes, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2. Country Level Analysis, Value (USD Billion)

30.3.2.1. China Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.2. India Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.3. South Korea Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.4. Australia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.5. Indonesia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.6. Malaysia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.7. Vietnam Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.8. Thailand Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.9. Singapore Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.10. New Zealand Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.2.11. Rest of Asia Pacific Excluding Japan Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31. Latin America Market

31.2. Overview

31.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

31.2.2. Increment $ Opportunity Assessment, 2026-2036

31.2.3. Year-on-Year Growth Forecast (%)

31.3. Segmentation (USD Billion), 2026-2036, By

27.2.5. By Product Type

27.2.5.1. Fluids, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.2. Gels, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.3. Resins, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.4. Elastomers, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.4.1. High-Temperature Vulcanized (HTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.4.2. Liquid Silicone Rubber (LSR), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.4.3. Room Temperature Vulcanized (RTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.5. Adhesives and Sealants, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.6. Emulsions, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1. By End use Industry

31.3.1.1. Electronics, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.2. Construction, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.3. Healthcare, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.4. Personal Care and Consumer Goods, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.5. Energy and Utilities, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.6. Industrial Processes, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2. Country Level Analysis, Value (USD Billion)

31.3.2.1. Brazil Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31.3.2.2. Argentina Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31.3.2.3. Mexico Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31.3.2.4. Rest of Latin America Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32. Middle East & Africa Market

32.2. Overview

32.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

32.2.2. Increment $ Opportunity Assessment, 2026-2036

32.2.3. Year-on-Year Growth Forecast (%)

32.3. Segmentation (USD Billion), 2026-2036, By

27.2.6. By Product Type

27.2.6.1. Fluids, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.2. Gels, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.3. Resins, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.4. Elastomers, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.4.1. High-Temperature Vulcanized (HTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.4.2. Liquid Silicone Rubber (LSR), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.4.3. Room Temperature Vulcanized (RTV), Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.5. Adhesives and Sealants, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.6. Emulsions, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1. By End use Industry

32.3.1.1. Electronics, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.2. Construction, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.3. Healthcare, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.4. Personal Care and Consumer Goods, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.5. Energy and Utilities, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.6. Industrial Processes, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.7. Others, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2. Country Level Analysis, Value (USD Billion)

32.3.2.1. Saudi Arabia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.2. UAE Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.3. Israel Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.4. Qatar Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.5. Kuwait Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.6. Oman Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.7. South Africa Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.2.8. Rest of Middle East & Africa Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

33. Global Economic Scenario

33.2. World Economic Outlook

34. About Research Nester

34.2. Our Global Clientele

34.3. We Serve Clients Across World

Silicone Market Outlook:

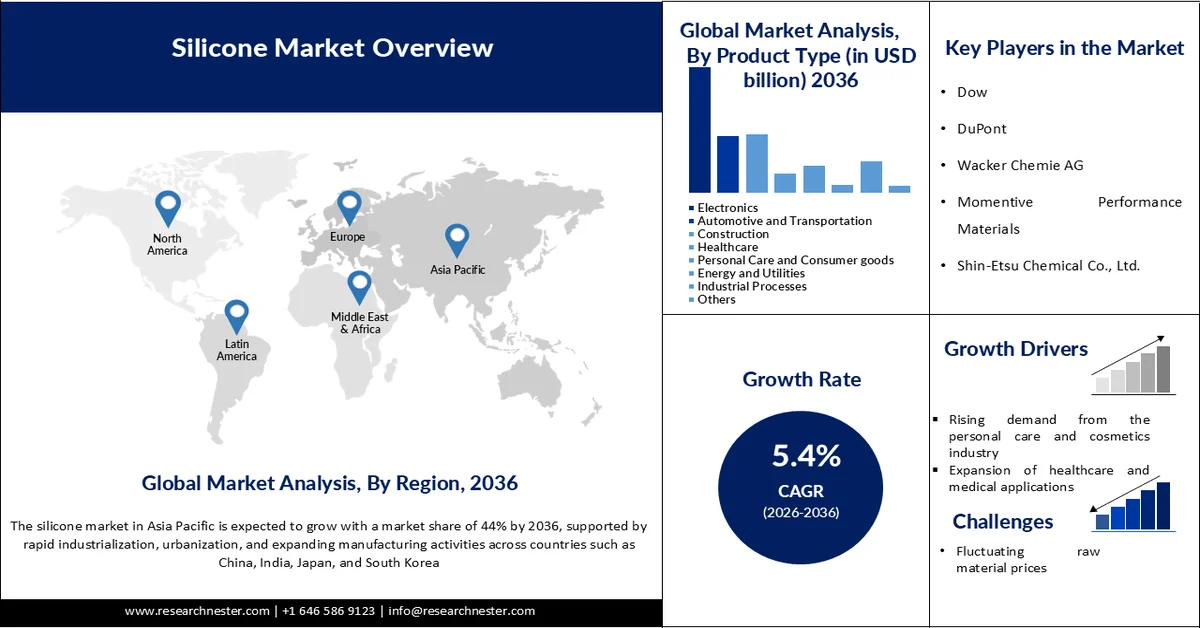

Silicone Market is valued at USD 24.26 billion in 2025 and is projected to reach USD 43.27 billion by 2036, growing at a CAGR of 5.4% during the forecast period, i.e., 2026-2036. In 2026, the industry size of silicone is assessed at USD 25.57 billion.

One of the primary growth drivers of the global silicone market is the rapid expansion of the electric vehicle (EV) and electronics industries. Silicones are extensively used in EV battery insulation, thermal management systems, semiconductors, sensors, and charging infrastructure because of their superior heat resistance and electrical insulation properties. According to the International Energy Agency (IEA), global electric car sales exceeded 17 million units in 2024, accounting for more than 20% of total global car sales. The IEA further projects that EV sales will continue growing strongly in the coming years due to supportive government policies and increasing investments in clean transportation infrastructure. Rising EV production directly increases demand for silicone materials used in battery safety systems, electronic components, and lightweight automotive applications.

Another major growth driver for the silicone market is the increasing investment in sustainable construction and energy-efficient infrastructure worldwide. Silicone sealants, adhesives, coatings, and elastomers are widely used in commercial and residential buildings because of their durability, UV resistance, waterproofing capability, and thermal insulation performance. According to the United Nations Environment Programme (UNEP), buildings and construction accounted for approximately 37% of global energy-related CO₂ emissions in 2023, driving governments and developers to adopt more energy-efficient construction materials. Additionally, the U.S. Department of Energy states that improving building insulation and sealing can reduce heating and cooling energy use by up to 20%, increasing the adoption of high-performance silicone-based materials in modern infrastructure projects.

Key Silicone Market Insights Summary:

Regional Highlights:

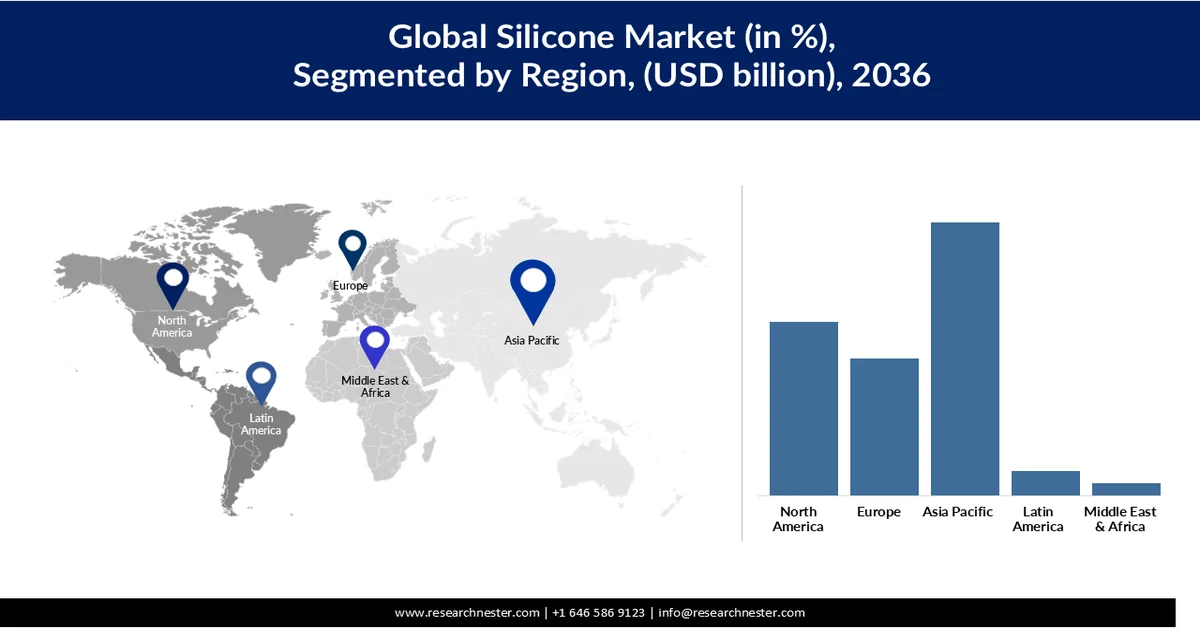

- Asia Pacific silicone market is projected to capture 44% share by 2036, propelled by rapid industrialization, urbanization, and expanding manufacturing activities across key economies

- North America is anticipated to witness notable growth throughout 2026-2036, stimulated by rising demand for high-performance materials in healthcare, electronics, and aerospace applications

Segment Insights:

- The silicone elastomers segment is expected to account for 43.24% share by 2036 in the silicone market, fueled by superior flexibility, durability, and resistance to extreme temperatures and chemicals

- The electronics segment is projected to hold 36.58% share during 2026-2036, accelerated by increasing demand for high-performance and miniaturized electronic devices

Key Growth Trends:

- Rising demand from the personal care and cosmetics industry

- Expansion of healthcare and medical applications

Major Challenges:

- Fluctuating raw material prices

- Stringent environmental and regulatory challenges

Key Players: Dow (U.S.), DuPont (U.S.), Wacker Chemie AG (Germany), Momentive Performance Materials (U.S.), Shin-Etsu Chemical Co., Ltd. (Japan), Mitsubishi Chemical Group Corporation (Japan), Evonik Industries AG (Germany), Elkem ASA (Norway), KCC Corporation (South Korea), Gelest Inc. (U.S.).

Global Silicone Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 24.26 billion

- 2026 Market Size: USD 25.57 billion

- Projected Market Size: USD 43.27 billion by 2036

- Growth Forecasts: 5.4% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Asia Pacific (44% Share by 2036)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: India, Brazil, Vietnam, Indonesia, Mexico

Last updated on : 29 May, 2026

Silicone Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand from the personal care and cosmetics industry: The increasing demand for high-performance personal care and cosmetic products is a major growth driver of the global silicone market. Silicones are widely used in skincare, haircare, and beauty formulations because they provide smooth texture, water resistance, and long-lasting effects. Consumers are increasingly preferring premium cosmetic products with enhanced sensory properties, which has boosted the use of silicone-based ingredients. In addition, the growth of the global beauty and wellness industry, especially in emerging economies, is supporting higher silicone consumption. Manufacturers are also developing specialty silicones for multifunctional cosmetic applications, further accelerating market growth.

- Expansion of healthcare and medical applications: Rapid advancements in the healthcare and medical industry are significantly driving the global silicone market. Silicones are extensively used in medical devices, implants, tubing, wound care products, and pharmaceutical applications due to their biocompatibility, flexibility, and resistance to extreme temperatures. The rising aging population and increasing prevalence of chronic diseases have increased demand for advanced healthcare products, thereby boosting silicone usage. Furthermore, growth in minimally invasive surgeries and wearable medical devices is creating additional opportunities for medical-grade silicones. Their durability and non-reactive nature make them highly suitable for long-term medical applications.

- Growing use in electronics and semiconductor industry: The growing adoption of silicones in the electronics and semiconductor industry is another important driver of market expansion. Silicones are used as insulating, sealing, and thermal management materials in smartphones, laptops, semiconductors, and consumer electronics. With the rapid digitalization across industries and rising demand for compact, high-performance electronic devices, the need for reliable silicone materials has increased substantially. Silicones help improve device durability, heat resistance, and protection against moisture and environmental stress. Moreover, the expansion of 5G technology and advanced electronic manufacturing is further supporting the demand for specialty silicone products worldwide.

Challenges

- Fluctuating raw material prices: One of the major restraints in the global silicone market is the fluctuation in raw material prices, particularly silicon metal and other petrochemical derivatives. Variations in energy costs, supply chain disruptions, and geopolitical uncertainties often impact production expenses for silicone manufacturers. These price fluctuations reduce profit margins and create challenges in maintaining stable product pricing. As a result, manufacturers may face difficulties in long-term planning and cost management.

- Stringent environmental and regulatory challenges: The silicone industry faces strict environmental and regulatory requirements related to manufacturing processes and chemical emissions. Governments and environmental agencies in several countries have imposed regulations regarding the use and disposal of certain silicone compounds due to environmental and health concerns. Compliance with these standards increases operational and research costs for manufacturers. In addition, lengthy approval procedures for specialized silicone products can slow down market expansion and product innovation.

Silicone Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2036 |

|

CAGR |

5.4% |

|

Base Year Market Size (2025) |

USD 24.26 billion |

|

Forecast Year Market Size (2036) |

USD 43.27 billion |

|

Regional Scope |

|

Silicone Market Segmentation:

Product Type Segment Analysis

The silicone elastomers segment is significantly driving the growth of the product type segment and is expected to grow at a market share of 43.24% by 2036 due to their superior flexibility, durability, and resistance to extreme temperatures and chemicals. These materials are widely used across industries such as electronics, automotive, healthcare, and consumer goods for applications requiring high performance and long service life. The increasing demand for lightweight and reliable materials in industrial manufacturing has further boosted the adoption of silicone elastomers. In addition, products such as High-Temperature Vulcanized (HTV), Liquid Silicone Rubber (LSR), and Room Temperature Vulcanized (RTV) silicones are gaining popularity because of their excellent molding and sealing properties. Their broad application range and strong performance advantages continue to support substantial market expansion within the silicone product segment.

End use Industry Segment Analysis

The electronics segment is expected to grow at a market share of 36.58% between 2026 and 2036 due to the increasing demand for high-performance and miniaturized electronic devices. Silicones are widely used in electronic components as insulating, encapsulating, sealing, and thermal management materials because they offer excellent heat resistance, electrical insulation, and durability. The rapid expansion of smartphones, semiconductors, wearable devices, and advanced communication systems has significantly increased silicone consumption. In addition, the growing adoption of 5G infrastructure and smart electronics is further accelerating demand for specialty silicone materials. Their ability to enhance device reliability and protect sensitive components makes silicones essential in modern electronic manufacturing.

Our in-depth analysis of the silicone market includes the following segments:

|

Segments |

Subsegments |

|

Product Type |

|

|

End use Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Silicone Market - Regional Analysis

Asia Pacific Market Insights

Asia Pacific is driving the growth of the global silicone market and is expected to hold a share of 44% by 2036 due to rapid industrialization, urbanization, and expanding manufacturing activities across countries such as China, India, Japan, and South Korea. The region has a strong presence of electronics, automotive, healthcare, and personal care industries, all of which extensively use silicone-based products. Rising consumer demand for advanced electronic devices and high-quality consumer goods is further increasing silicone consumption. In addition, the availability of low-cost labor and raw materials supports large-scale silicone production in the region. Government initiatives promoting industrial and technological development are also contributing to market expansion.

The Japan silicone market is anticipated to grow from USD 2.07 billion in 2026 to USD 3.50 billion by 2036, registering a CAGR of 5.4% during the forecast period due to the country’s strong semiconductor, electronics, and advanced manufacturing industries. Silicones are widely used in semiconductor packaging, thermal management, and electronic insulation materials, which have increased demand alongside Japan’s expanding chip sector. According to the U.S. International Trade Administration, Japan’s semiconductor market is expected to exceed USD 51 billion by 2025, supported by government investments and AI-driven chip demand. These developments are creating substantial opportunities for silicone materials used in electronics, healthcare, and industrial applications.

India is emerging as a fast-growing silicone market due to rapid expansion in electronics manufacturing, specialty chemicals, and consumer industries. Silicones are increasingly used in electronic components, adhesives, sealants, personal care products, and industrial applications across the country. According to the Press Information Bureau (PIB), India’s electronics production increased nearly six-fold from USD 1.9 trillion in 2014–15 to USD 11.3 trillion in 2024–25, while the country became the world’s second-largest mobile phone manufacturer. The rapid industrial and manufacturing expansion is significantly boosting the demand for silicone products across multiple end-use sectors.

North America Market Insights

North America is a significant contributor to the silicone market due to strong demand from advanced healthcare, electronics, and aerospace industries. The region is characterized by high adoption of innovative silicone technologies and increasing use of specialty silicone materials in industrial applications. The presence of major silicone manufacturers and continuous investments in research and development are supporting product innovation and market growth. In addition, growing demand for high-performance materials in medical devices and electronic systems is boosting silicone consumption. The region’s focus on technological advancement and premium-quality products continues to strengthen the market.

The silicone market in the U.S. is witnessing steady growth driven by strong demand from advanced end-use industries such as healthcare, electronics, aerospace, and personal care. The country’s well-established medical device sector extensively uses silicone in implants, tubing, and diagnostic equipment due to its biocompatibility and durability. In addition, increasing demand for high-performance electronics and thermal management materials is supporting market expansion. The presence of major silicone manufacturers and continuous innovation in specialty silicone formulations further strengthen growth. Rising focus on advanced materials in industrial applications is also contributing to sustained market development.

Canada silicone market is growing gradually, supported by rising demand from healthcare, construction-related applications, and industrial manufacturing sectors. The healthcare industry is a key driver, with increasing use of silicone in medical devices, prosthetics, and wound care products due to its safety and flexibility. Growth in electronics and consumer goods manufacturing is also contributing to higher silicone consumption. Additionally, expanding industrial activities and the adoption of advanced sealing and insulation materials are supporting market uptake. The country’s emphasis on high-quality and durable materials is further encouraging the use of silicone-based products across various applications.

Europe Market Insights

Europe is driving the silicone market through its well-established automotive, healthcare, industrial, and consumer goods sectors. The region has a strong emphasis on sustainable and high-performance materials, which has increased the adoption of advanced silicone products across various applications. Growing demand for energy-efficient electronic devices and innovative healthcare solutions is also supporting market growth. In addition, stringent quality standards and continuous technological developments encourage manufacturers to produce specialty silicones with enhanced performance characteristics. Countries such as Germany, France, and the UK remain major contributors due to their strong industrial and manufacturing bases.

Germany silicone market is growing steadily, driven by its strong automotive, industrial manufacturing, and electronics sectors. The country’s leadership in advanced engineering and high-performance materials has increased the use of silicones in sealing, bonding, and thermal management applications. In the automotive sector, silicones are widely used in gaskets, coatings, and electronic components due to their durability and heat resistance. Growth in industrial automation and smart manufacturing is also supporting demand for silicone-based materials. Additionally, Germany’s focus on sustainability and energy-efficient technologies is encouraging the adoption of advanced silicone solutions.

The silicone market in the UK is expanding due to rising demand from the healthcare, construction, and personal care industries. The healthcare sector is a major driver, with increased use of silicones in medical devices, implants, and pharmaceutical applications because of their biocompatibility. Growth in the cosmetics and personal care industry is also boosting demand for silicone-based ingredients. In addition, ongoing industrial and infrastructure modernization is supporting the use of silicones in sealing and protective applications. The UK’s emphasis on innovation and high-value manufacturing is further strengthening market growth.

Key Silicone Market Players:

- Dow (U.S.)

- DuPont (U.S.)

- Wacker Chemie AG (Germany)

- Momentive Performance Materials (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- Evonik Industries AG (Germany)

- Elkem ASA (Norway)

- KCC Corporation (South Korea)

- Gelest Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Dow is one of the leading global players in the silicone market, with a strong focus on innovation and diversified applications. The company offers a wide range of silicone products used in healthcare, electronics, personal care, and industrial sectors. It invests heavily in R&D to develop advanced specialty silicones with improved performance and sustainability. Dow’s global manufacturing and distribution network strengthens its supply chain and market reach.

- Wacker Chemie AG is a major silicone producer known for its extensive portfolio of silicone fluids, elastomers, and resins. The company plays a key role in supplying high-performance materials for construction, automotive, and electronics industries. It focuses on expanding production capacity and enhancing product innovation to meet rising global demand. Its strong presence in Europe and Asia supports its competitive position in the global market.

- Shin-Etsu Chemical Co., Ltd. is a dominant player in the silicone industry, particularly strong in high-quality silicone products for electronics and semiconductor applications. The company benefits from advanced manufacturing technologies and strong R&D capabilities. It supplies silicone materials widely used in automotive, healthcare, and industrial applications. Its global expansion strategy strengthens its leadership in specialty silicones.

- Momentive Performance Materials is a key global supplier of advanced silicone solutions serving industries such as aerospace, healthcare, electronics, and energy. The company emphasizes product innovation and customized silicone solutions to meet specific customer needs. It has a strong focus on high-performance and specialty silicones for demanding applications. Its global operational footprint enables it to serve a diverse industrial base efficiently.

Below is the list of the key players operating in the global silicone market:

Key players in the global silicone market are driving growth through continuous investment in research and development to create advanced, high-performance silicone materials. Companies are expanding their production capacities to meet rising global demand across electronics, healthcare, and industrial applications. They are also focusing on developing sustainable and specialty silicone products with improved efficiency and environmental compatibility. In addition, strategic collaborations, mergers, and global expansion initiatives are strengthening their market presence and enhancing supply chain capabilities.

Corporate Landscape of the Global Silicone Market:

Recent Developments

- In September 2025, Dow announced the launch of DOWSIL™ EG-4175 Silicone Gel, designed for next-generation high-voltage power electronics used in applications such as electric vehicle inverters and renewable energy systems. The silicone gel is engineered to withstand temperatures up to 180°C, improving reliability, thermal stability, and efficiency in insulated gate bipolar transistor (IGBT) modules. This innovation supports the growing demand for advanced materials in high-performance electronic systems and energy-efficient technologies.

- In June 2025, Wacker Chemie AG presented new silicone elastomer innovations focused on energy, digitalization, and mobility applications at its industry preview for K 2025. The company highlighted developments such as ceramifying silicone rubber for improved fire safety in mobility applications and electroactive silicone laminates for sensors and smart systems. These products are designed to support key megatrends like electrification, automation, and sustainable materials development.

- Report ID: 8445

- Published Date: May 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.