Silicon Carbide Market Outlook:

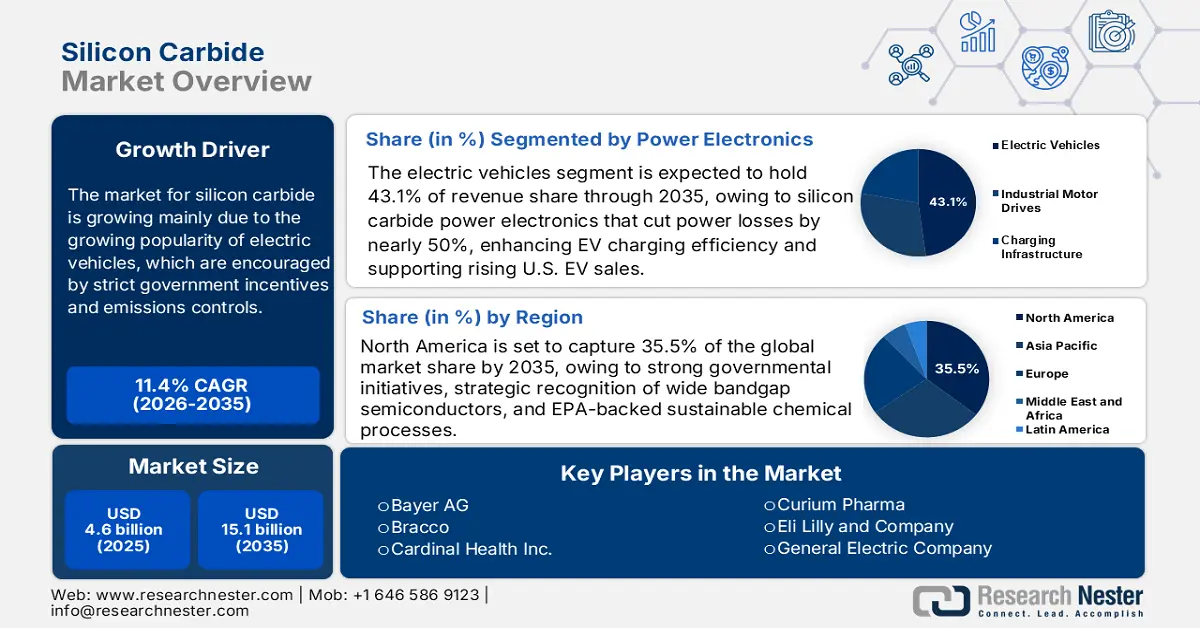

Silicon Carbide Market size was valued at USD 4.6 billion in 2025 and is projected to reach USD 15.1 billion by the end of 2035, rising at a CAGR of 11.4% during the forecast period from 2026 to 2035. In 2026, the industry size of silicon carbide is estimated at USD 5.2 billion.

The global silicon carbide market is projected to witness an upward trend over the forecast years, primarily driven by the growing popularity of electric vehicles, which are encouraged by strict government incentives and emissions controls. The Bipartisan Infrastructure Law has allocated 7.5 billion dollars by the Biden Administration to construct an EV charging network nationwide, with 500,000 public chargers set to be installed by 2030, which is a significant obstacle to EV adoption because of its effect on the use of EVs based on the availability of chargers. This large investment in infrastructure is creating a rise in demand for silicon carbide (SiC) power electronics that are essential in efficient inverters and onboard chargers in EVs. Additionally, the EU mandates that all new automobiles and vans sold by 2035 have zero CO2 emissions to achieve the 2050 climate neutrality target, and by 2030, cars and vans are expected to emit 55% and 50% less than in 2021, respectively. This act enhances the uptake of battery-electric vehicles, which demand power electronics of high efficiency. Subsequent electric vehicle manufacturing boosts the market of silicon carbide needed in efficient inverters and onboard chargers in EVs.

Additionally, the IEA Global EV Outlook 2023 says that China is the dominant player in the electric vehicle market, with over 60% of the total worldwide EV sales, and that by 2022, more than 20% of all vehicle sales in China had been electric vehicles. This rush to EV is vastly sustained by robust policy provisions concerning New Energy Vehicles (NEVs), which are triggering a huge demand for high-efficiency power electronics. The rise of the EV market in China creates a large demand for silicon carbide, in that the SiC components are needed to improve the efficiency of the EV inverter and onboard charger to enable the nation to adopt electric mobility.

On the supply side, the silicon carbide supply chain relies majorly on the source of the high-purity raw materials, such as silicon and carbon, sophisticated crystal growth and wafer processing technology, and vertically integrated manufacturing to manage quality and production. In 2023, the US manufactured some 40,000 metric tons of silicon carbide worth about 28 million US dollars, and imports were 120,000 metric tons, predominantly of Chinese origin. The capacity of silicon carbide manufacturing across the world is approximately one million metric tons, with China manufacturing 450,000 metric tons and controlling the supply chain. This manufacturing extends the silicon carbide market, which is rapidly increasing with the increasing demand for electric vehicles and power electronics, highlighting the necessity for increased manufacturing and secure supply chains.

Furthermore, according to the U.S. Bureau of Labor Statistics, August 2025 records that the Producer Price Index of Nonmetallic Abrasive Products (WPU113603) was 292.339 (1982 = 100) and the industry PPI index of Abrasive Product Manufacturing (PCU3279103279104) was 339.408 in the same month. These values show broad-based cost pressures in materials associated with silicon carbide, which show increasing costs of inputs to support market growth. The SiC is listed as a priority material to invest further in the manufacturing, processing, and device deployment in the U.S. federal R&D and deployment programs, such as the DOE Critical Materials Assessment. These trends signal a supply chain that is in active growth, where imports are strongly dependent but supported by state funding of R&D and manufacturing.