Silicon Carbide Market Outlook:

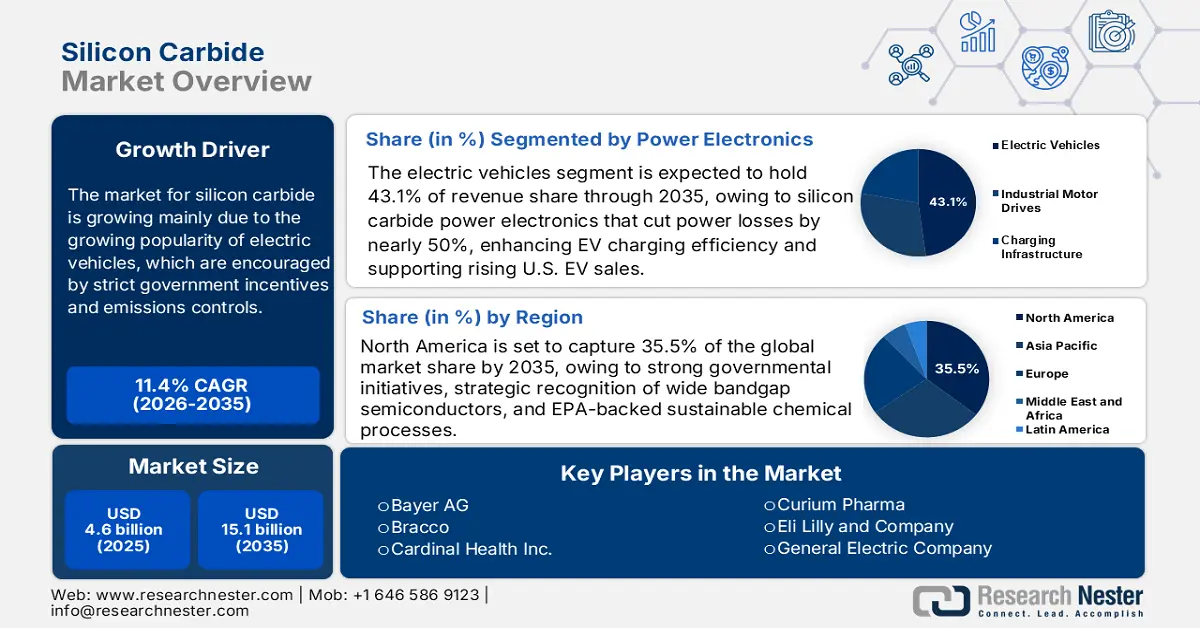

Silicon Carbide Market size was valued at USD 4.6 billion in 2025 and is projected to reach USD 15.1 billion by the end of 2035, rising at a CAGR of 11.4% during the forecast period from 2026 to 2035. In 2026, the industry size of silicon carbide is estimated at USD 5.2 billion.

The global silicon carbide market is projected to witness an upward trend over the forecast years, primarily driven by the growing popularity of electric vehicles, which are encouraged by strict government incentives and emissions controls. The Bipartisan Infrastructure Law has allocated 7.5 billion dollars by the Biden Administration to construct an EV charging network nationwide, with 500,000 public chargers set to be installed by 2030, which is a significant obstacle to EV adoption because of its effect on the use of EVs based on the availability of chargers. This large investment in infrastructure is creating a rise in demand for silicon carbide (SiC) power electronics that are essential in efficient inverters and onboard chargers in EVs. Additionally, the EU mandates that all new automobiles and vans sold by 2035 have zero CO2 emissions to achieve the 2050 climate neutrality target, and by 2030, cars and vans are expected to emit 55% and 50% less than in 2021, respectively. This act enhances the uptake of battery-electric vehicles, which demand power electronics of high efficiency. Subsequent electric vehicle manufacturing boosts the market of silicon carbide needed in efficient inverters and onboard chargers in EVs.

Additionally, the IEA Global EV Outlook 2023 says that China is the dominant player in the electric vehicle market, with over 60% of the total worldwide EV sales, and that by 2022, more than 20% of all vehicle sales in China had been electric vehicles. This rush to EV is vastly sustained by robust policy provisions concerning New Energy Vehicles (NEVs), which are triggering a huge demand for high-efficiency power electronics. The rise of the EV market in China creates a large demand for silicon carbide, in that the SiC components are needed to improve the efficiency of the EV inverter and onboard charger to enable the nation to adopt electric mobility.

On the supply side, the silicon carbide supply chain relies majorly on the source of the high-purity raw materials, such as silicon and carbon, sophisticated crystal growth and wafer processing technology, and vertically integrated manufacturing to manage quality and production. In 2023, the US manufactured some 40,000 metric tons of silicon carbide worth about 28 million US dollars, and imports were 120,000 metric tons, predominantly of Chinese origin. The capacity of silicon carbide manufacturing across the world is approximately one million metric tons, with China manufacturing 450,000 metric tons and controlling the supply chain. This manufacturing extends the silicon carbide market, which is rapidly increasing with the increasing demand for electric vehicles and power electronics, highlighting the necessity for increased manufacturing and secure supply chains.

Furthermore, according to the U.S. Bureau of Labor Statistics, August 2025 records that the Producer Price Index of Nonmetallic Abrasive Products (WPU113603) was 292.339 (1982 = 100) and the industry PPI index of Abrasive Product Manufacturing (PCU3279103279104) was 339.408 in the same month. These values show broad-based cost pressures in materials associated with silicon carbide, which show increasing costs of inputs to support market growth. The SiC is listed as a priority material to invest further in the manufacturing, processing, and device deployment in the U.S. federal R&D and deployment programs, such as the DOE Critical Materials Assessment. These trends signal a supply chain that is in active growth, where imports are strongly dependent but supported by state funding of R&D and manufacturing.

Key Silicon Carbide Market Insights Summary:

Regional Highlights:

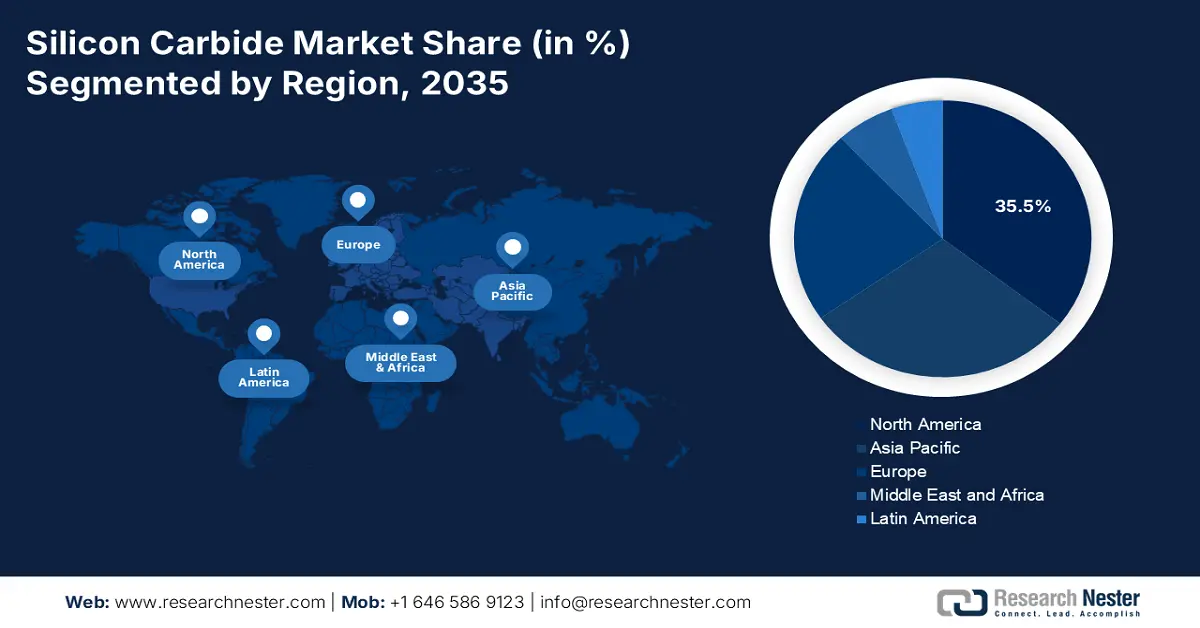

- North America is anticipated to secure a 35.5% share from 2026–2035 in the silicon carbide market, supported by expanding federal funding for strategic semiconductor technologies.

- The Asia Pacific region is expected to account for a 29.8% share during 2026–2035, reinforced by strong semiconductor manufacturing capacity and growing emphasis on SiC-based electrification technologies.

Segment Insights:

- The electric vehicles segment is set to capture a 43.1% share by 2035 in the silicon carbide market, bolstered by rising dependence on high-efficiency SiC power electronics that enhance EV charging and grid performance.

- The power devices segment is expected to attain a 28.9% share over 2026–2035, supported by increasing deployment of SiC MOSFETs and diodes across industrial and renewable energy systems.

Key Growth Trends:

- Regulatory risk assessment and compliance with chemical safety

- Integration of electric vehicle (EV) & renewable energy system

Major Challenges:

- High environmental compliance costs

- Trade barriers and tariffs

Key Players: Coherent Corp. (formerly II-VI), STMicroelectronics NV, Infineon Technologies AG, ROHM Semiconductor, ON Semiconductor, SK Siltron Co. Ltd., Toshiba Materials Co. Ltd., Cree Inc. (Wolfspeed), SICC Materials Co. Ltd., ESD-SIC bv, AGS Technologies, Norstel AB (STMicro), Everspin Technologies Inc., Malaysian Advanced Materials (MAM).

Global Silicon Carbide Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.6 billion

- 2026 Market Size: USD 5.2 billion

- Projected Market Size: USD 15.1 billion by 2035

- Growth Forecasts: 11.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Taiwan, Vietnam, Mexico, United Kingdom

Last updated on : 24 October, 2025

Silicon Carbide Market - Growth Drivers and Challenges

Growth Drivers

- Regulatory risk assessment and compliance with chemical safety: The existing overhaul of the chemical risk evaluation in the Toxic Substances Control Act (TSCA) of the U.S. is influencing the market. In 2024, the EPA revised TSCA processes to include elaborate risk evaluations on each use condition, exposure pathway, and lifecycle phase of the existing chemicals, making compliance complicated among manufacturers. The fees paid by the silicon carbide manufacturers in order to comply are going to intensify significantly, whereas the pre-manufacture notices (PMNs) fees have also escalated to USD 37,000 compared to USD 19,020, and the risk assessment fees can go up to USD 4.287 million per substance. These laws compel demand for safer and purer SiC products and upgrades to the processes, which strengthen the growth of markets in the chemical industry.

- Integration of electric vehicle (EV) & renewable energy system: The electrification and adoption of renewable energy is a strong demand driver of silicon carbide. In EVs and renewable systems, SiC power devices are increasing inverter efficiency significantly to lower energy loss, and are needed to meet EU eco-design and U.S. Department of Energy efficiency targets. According to the U.S. Department of Energy, Alternative Fuels Data Center, the electric vehicle (EV) charging systems are growing at a high rate. During the second quarter of 2024, the count of EV charging ports grew by 6.3% and the DC fast charging ports grew by 7.4%. The Northeast area has recorded a significant growth in the number of public charging ports by 13.2%. These efficiency-based regulatory standards form an effective B2B demand pipeline, propelling the production of SiC and expansion of the international market.

- Innovation in the Production efficiency and purity of the material: The technological breakthroughs in the production of SiC refine the production efficiency and purity of the material. Better energy use has also been achieved through the adoption of better plasma-based synthesis and catalytic processes, which resulted in 20% less energy usage per ton of SiC synthesized. Moreover, a thermal treatment process with 2000-2600°C in an inert atmosphere recovers up to 80% reusable silicon carbide in the form of powder material in waste, improving the supply of silicon carbide with an increasing demand. These inventions conform to the sustainability requirements set by agencies like the EPA and DOE that enable manufacturers to comply with the tightened emissions and waste standards, as well as control production costs. Consequently, the increased efficiency of the SiC manufacturing, and thus, environmental compliance, as well as scalable market expansion in high-need markets such as power electronics and renewable energy.

Challenges

- High environmental compliance costs: Silicon carbide production entails energy-consuming processes that generate greenhouse gases and particulate matter, for which environmental compliance is a significant issue. In the U.S., the manufacturers are obliged to comply with the laws of the Clean Air Act and the Clean Water Act, which require the installation of pollution control devices, continuous monitoring, and reporting of emissions. In the case of small and medium-sized enterprises (SMEs), the cost of covering these environmental conditions is prohibitive, and thus, the production capacity and entry into the market may be restricted. Such compliance costs affect the pricing models and retard the adoption of SiC-based products in the near term, especially in the areas where stricter standards are imposed, and encourage bigger players to invest in the cleaner and more effective production technologies to stay competitive.

- Trade barriers and tariffs: The distribution of silicon carbide products to the market throughout the world is limited by trade barriers and tariffs that raise the prices of raw materials and influence access to markets. For example, the U.S. has imposed anti-dumping levies on the SiC imports of some countries in order to support the local manufacturers. These policies increase the price of imported SiC raw materials and components, compel suppliers to revise pricing models, and may constrain supply chain flexibility. Smaller producers can hardly bear these expenses, and large ones have to deal with complicated compliance and reporting. These trade barriers affect market penetration in the world, as the time taken to introduce the product is long, and the competitiveness is diminished in the major regions.

Silicon Carbide Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.4% |

|

Base Year Market Size (2025) |

USD 4.6 billion |

|

Forecast Year Market Size (2035) |

USD 15.1 billion |

|

Regional Scope |

|

Silicon Carbide Market Segmentation:

Power Electronics Segment Analysis

The electric vehicles segment is expected to grow with the largest revenue share of 43.1% by 2035, driven in large part by the electric vehicle (EV) revolution. Silicon carbide power electronics and DC power networks achieve power losses by almost 50%, improving the efficiency of EV charging and battery health. This leads to reduced cooling needs and more efficient and economical fast charging solutions. As per the report by the U.S. Department of Energy, EV sales in the U.S. are expected to reach as high as 6.8 million units annually in the high scenario, and boost the electric power demand up to 26 TWh. This surge drives the power electronics business growth in silicon carbide, which supports efficient EV inverters and charging infrastructures to support higher grid loads and rapid charge requirements.

Traction inverters take DC battery power and convert it to AC to optimally drive the electric motors, and inverters based on SiC have a better power density, lower energy loss, and better thermal operation, resulting in a longer driving range and higher acceleration. The battery management system guarantees the maximum performance and life of lithium-ion batteries by monitoring, controlling, and balancing the battery cells; the SiC components enhance the efficiency of the system and decrease the amount of heat generation, which justifies increased charge rates. Together, these subsegments are essential to improving EV performance and increasing the pace at which the silicon carbide market grows.

Semiconductors Segment Analysis

The power devices segment is expected to grow with a market share of 28.9% over the projected years from 2026 to 2035, owing to its adoption in industrial and renewable energy applications, accelerated by SiC-based MOSFETs and diodes. For instance, Toshiba's latest SiC trench MOSFETs and super-junction Schottky barrier diodes reduce on-resistance by up to 35% compared to conventional devices, enhancing efficiency and reliability. These advancements significantly boost the power devices segment growth, particularly for electric vehicles and renewable energy systems requiring high-efficiency power conversion. Furthermore. SiC-based MOSFETs and diodes are significantly less energy-consuming and more efficient than silicon, which allows higher efficiency, lower cooling requirements, and greater reliability in conversion to power.

High-voltage MOSFETs, particularly 600-1200V and medium-voltage support greater switching frequencies and power density, and can support 800V EV architectures and switch frequencies as high as 20 kHz. And device developments have reduced 1,200V MOSFET switching losses up to 28%, accelerating the switch to inverters in EVs and industrial drives. Meanwhile, Schottky diodes are low-loss rectifiers/freewheeling devices since their per-wafer cost is lower than that of MOSFETs, and they reduce system cost at scale. NREL modelling indicates that MOSFET processing produces higher wafer costs, whereas SBDs are economic.

RF Devices Segment Analysis

The 5G infrastructure segment is expected to grow steadily during the projected years by 2035, since next-generation 5G (including mmWave) requires amplifiers and high-frequency transceivers to be able to operate beyond 100 GHz. RF devices made with SiC have better power density, thermal conductivity, and frequency response compared to silicon. According to the U.S. Department of Energy, wide-bandgap semiconductors, including SiC, have been well-characterized as RF-use devices, and further wireless communications beyond 100 GHz will demand amplification capabilities otherwise unavailable in the conventional Si technology. This establishes base station front ends and small cell systems with the ability to provide superior throughput and efficiency, which will drive expansion in the RF silicon carbide market due to volume applications in 5G networks.

Our in-depth analysis of the silicon carbide market includes the following segments:

|

Segment |

Subsegments |

|

Power Electronics |

|

|

Semiconductors |

|

|

Industrial |

|

|

RF Devices |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Silicon Carbide Market - Regional Analysis

North America Market Insights

North America’s market is anticipated to grow with the largest revenue share of 35.5% during the forecast years from 2026 to 2035, attributed to governmental initiatives on high-technology materials, energy security, and sustainability of chemicals. Wide bandgap semiconductors, such as SiC, are formally identified as strategic technologies by the U.S. Department of Energy (DOE), and it emphasizes the capability of such materials to enable increased power density, shorter switching, and efficiency improvements in grid and transportation systems. Additionally, one of the largest drivers is federal funding, where in August 2022, DOE declared it would fund university and national laboratory activities in clean energy technology and low-carbon manufacturing at a sum of USD 540 million, with SiC research being one of the areas of emphasis in semiconductor innovation. There are also environmental regulations that push the regional SiC market by promoting sustainable chemical processes. The EPA Green Chemistry Challenge Program has documented various innovative technologies adopted in 2021, which have resulted in quantifiable reductions in hazardous waste and are in line with the safer chemical manufacturing practices in support of SiC wafer processing requirements.

Furthermore, the NIST report states that advanced metrology systems that have been developed to serve high-voltage, high-speed, SiC power devices, such as 10-kV MOSFETs with a continuous current of 2A (50A/cm 2) and 10-kV PiN diodes in operation with 40 A (80 A/cm 2), are selected to provide accurate performance and reliability test results. These criteria minimise the risk of commercialization and help to promote the increasing use of SiC in the energy transition of North America, electric vehicles, and industrial markets by facilitating powerful, efficient electronics of power. Together, these factors, including an increase in government spending on R&D, sustainability requirements, and adoption of SiC in new manufacturing and chemical development, are making North America a major growth centre in the global SiC market.

The U.S. market is projected to lead the North American region with the largest share by 2035, mainly driven by the federal laws and the technical standards promoting the growth of advanced power electronics. The CHIPS and Science Act of 2022 permitted the allocation of USD 52.7 billion to broaden domestic semiconductor capacity, where wide-bandgap semiconductor materials like SiC are also included in the research and manufacturing priorities. In addition, in direct response to decreasing the risk of commercialization by removing a barrier to manufacturers, the National Institute of Standards and Technology (NIST) is making progress in metrology programs to enhance the reliability and measurement standards of SiC devices. Moreover, crystalline silica, which is a major component in semiconductor processing, has imposed limiting exposure levels on the Occupational Safety and Health Administration (OSHA) of chemicals, so that safer manufacturing habits are adhered to. For instance, OSHA has imposed permissible exposure limits (PEL) of respirable crystalline silica, which stipulates a limit of 50 micrograms per cubic meter (µg/m³) of silica concentration in the air, which is to be allowed during an 8-hour work shift to make the manufacturing process in semiconductor processing and other industries safer. All these combines to have a robust federal funding, technical infrastructure, and workplace safety regulations as the U.S. pathway to leading the world in the adoption of SiC in industrial, automotive, and grid implementation.

The market in Canada is likely to expand steadily over the forecast years by 2035, owing to the robust clean technology innovation and advanced materials research by the federal government. In 2022-23, Natural Resources Canada has given out more than 350 energy innovation projects, some of which are advanced semiconductor and chemical process projects, which indirectly support SiC adoption with a budget of CAD 115 million. Sustainable manufacturing is also becoming a priority in Canada, as the 2030 Emissions Reduction Plan developed by the government is aimed at a 40% reduction of greenhouse gases by 2030, which will necessitate the usage of power electronics based on SiC in renewable energy and electrified transport. Additionally, the involvement of Canadians in international semiconductor alliances will guarantee access to important materials and technologies, thereby facilitating the adoption of the same domestically. With the added focus on clean-energy ambitions alongside strategic investment in research and development, Canada is establishing a solid base in SiC integration of the chemical and energy industries.

Asia Pacific Market Insights

The Asia Pacific market is expected to grow rapidly, with a revenue share of 29.8% during the projected years from 2026 to 2035, driven by the high demand for electric cars, renewable energy systems, and industrial power electronics. The wide-bandgap semiconductors, such as SiC, are being emphasized in regional energy and manufacturing strategies to enhance energy efficiency and greenhouse gas emissions reduction. For instance, according to the Congressional Research Service report, the Asia Pacific is at the forefront of the world semiconductor manufacturing scene with strong government-based investments in engineering materials such as silicon carbide (SiC) to improve power electronics to promote energy efficiency and electrification. The region comprises more than 70% of the worldwide capacity for semiconductor wafer fabrication, and semiconductor fabrication is used to propel the adoption of SiC in electric vehicles and the renewable energy industry. This is the leading role in production and long-term policy support, making the Asia Pacific play a significant role in developing the global SiC market.

Similarly, there has been a large growth in investment into the production of advanced materials and sustainable chemical processes, and, at the regional level, there are programs of investment in clean-energy adoption, practices in low-carbon industries, and high-efficiency power electronics. For example, the Asian Development Bank (ADB) has funded clean energy projects in Asia with a loan of USD 65 million to Nepal to support the energy access and efficiency improvement project, which installed 1000 solar-powered streetlights and distributed 1 million compact fluorescent lamps. The measures are expected to cut carbon dioxide emissions by 15,000-20,000 tons/year, indicating the regional investments in energy-efficient technologies and sustainable practices, which indirectly facilitate the adoption of silicon carbide in power electronics. Meanwhile, the metrology and device reliability standards are being developed in research institutions and standards bodies in the region, and the commercialization of high-performance SiC modules is accelerating.

By 2035, China’s market is likely to dominate the Asia Pacific region with a substantial revenue share, owing to significant investment in silicon carbide (SiC) technologies to boost its semiconductor and chemical sectors. In 2023, China made breakthroughs in 50 technologies dubbed as 50 foundations under the leadership of the State Council Information Office, such as the production of SiC. In addition, in the State Council of China National 13th Five-Year Plan, strategic emerging industries, such as new materials, such as silicon carbide (SiC), have priorities, and the scale of their industries will grow to more than 15% of GDP by the year 2020. The strategy aims to enhance the ability to innovate and create industrial clusters at the global scale in favor of the faster development of SiC as an important material in the Chinese semiconductor and clean energy industries. Additionally, the Ministry of Ecology and Environment is encouraging the use of green chemistry to cut the number of harmful wastes in the production of chemicals. This has been backed by heavy investment in research and development, making China a major player regarding the use of SiC in chemical processes.

The market in India is expected to grow with the fastest CAGR from 2026 to 2035, attributed to the growing introduction of silicon carbide (SiC) technology to the chemical industry via government policies. The India Semiconductor Mission (ISM) provides fiscal subsidies to project expenses of setting up SiC-related facilities, such as compound semiconductor fabrication plants and packaging units. For example, the government under ISM has approved 10 semiconductor projects in six states, with a total cost of about 1.60 lakh crore. Such projects include different semiconductor manufacturing processes such as fabrication, packaging, and testing. It is also worth noting that the ISM has contributed to the development of the first commercial-scale semiconductor plant in the country in Odisha, and it specializes in Silicon Carbide (SiC) technologies. Additionally, the government has spent 234 crores on chip design projects in 2025 that facilitated innovation in SiC applications. Moreover, the production of specialty chemicals has been growing steadily in the Department of Chemicals and Petrochemicals, and there has been a dramatic expansion of exports between the FY 2018-19 and FY 2022-23. These efforts indicate that India is increasingly concerned with the application of SiC technologies in order to make its chemical sector efficient and sustainable.

Europe Market Insights

The European market is projected to grow with a substantial revenue share of 22.7% over the forecast years, owing to the demand for electric cars (EVs), renewable energy systems, and the growth of power electronics. The research and innovation devoted to climate change and sustainable development, as well as sustainable chemical technologies, is funded by Horizon Europe, with an indicative budget of €93.5 billion in 2021-2027. This is a significant investment that supports the development of silicon carbide (SiC) technologies in the European power electronics and clean energy industries, which also strengthens the leadership of the continent in advanced semiconductor materials. Additionally, the European Chemicals Agency (ECHA) and the European Chemical Industry Council (CEFIC) have played a key role in establishing regulatory frameworks that promote the use of SiC in other industrial uses. Furthermore, the National Semiconductor Strategy by the UK government promises up to 2023-25 and up to £200 billion, and by 2030, a decade later, 1 billion to expand domestic semiconductor manufacturing, including in compound semiconductors such as silicon carbide (SiC). The investment helps the UK in its advantages in the field of R&D, design, and manufacturing in order to speed up the development of SiC in the fields of power electronics and advanced technology.

Moreover, German chemical industries are determined to ensure that by 2050, they will have attained a climate-neutral scenario by investing more in sustainable and green chemical technologies. The nation focuses on the increased market need for environmentally friendly chemical solutions that are advanced by the innovation and regulatory measures to mitigate carbon emissions and promote the use of the circular economy. These eco-friendly innovations form the foundation of sophisticated technology for the development of such materials as silicon carbide (SiC), which makes Germany a pioneer in clean technologies and energy-saving devices with semiconductors.

Key Silicon Carbide Market Players:

- Wolfspeed, Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Coherent Corp. (formerly II-VI)

- STMicroelectronics NV

- Infineon Technologies AG

- ROHM Semiconductor

- ON Semiconductor

- SK Siltron Co., Ltd.

- Toshiba Materials Co., Ltd.

- Cree, Inc. (part of Wolfspeed)

- SICC Materials Co., Ltd.

- ESD-SIC bv

- AGS Technologies

- Norstel AB (acquired by STMicro)

- Everspin Technologies Inc.

- Malaysian Advanced Materials (MAM)

U.S. companies Wolfspeed, Coherent, and ON Semi lead the global market for SiC chemicals, using the CHIPS Act and DOE contracts to increase production. While Japan (ROHM, Toshiba) is the leader in high-purity SiC wafers, European companies (STMicro, Infineon) concentrate on automotive and industrial SiC solutions. China's SICC Materials and South Korea's SK Siltron are expanding through government-supported semiconductor regulations. With their green chemistry projects, Malaysia's MAM and India's AGS Tech are rising to prominence. Important tactics include partnerships (Infineon-Resonac), vertical integration (Wolfspeed's $5.5 billion fab expansion), and research and development in SiC recycling (STMicro's $101 million EU initiative).

Here is a list of key players operating in the global market:

Recent Developments

- In September 2025, Wolfspeed detailed commercial availability of its 200mm silicon carbide (SiC) materials portfolio, and the event was a major milestone in the journey of Wolfspeed to accelerate the transition of the industry to silicon with SiC. This launch is expected to satisfy the increasing demand for high-performance power devices in several industries, such as automobiles and renewable energy. These 200mm SiC wafers will increase power electronics efficiencies and scalability, and be a part of electric vehicles and the green energy solution.

- In May 2025, Himadri Speciality Chemicals signed a technology licensing agreement with Australian-based battery materials company Sicona to build the first silicon-carbon factory in India. This partnership gives Himadri the right to access, localize, and commercialize the innovative SiCx silicon-carbon anode technology developed by Sicona, which can be viewed as one of the significant technological advancements in the field of lithium-ion batteries. Himadri has already put in 139 crores in Sicona, comprising a 12.5% stake with an initial investment of 58 crores in Elixir Carbo Private Limited and a later investment of 81 crores in convertible notes.

- In February 2024, SK Siltron CSS was committed to a loan of up to 544 million dollars by the U.S Department of Energy. The loan helped to enhance American manufacturing of high-quality silicon carbide (SiC) wafers, which are important components of electric vehicle (EV) power electronics. The growth is expected to involve the creation of up to 200 construction jobs, as well as 200 skilled manufacturing jobs. Technology that has been developed in the SK Siltron unit in Auburn, Michigan, will be deployed to the Bay City plant to deal with the current depleted supply of these wafers.

- Report ID: 5213

- Published Date: Oct 24, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.