Semiconductor Manufacturing Equipment Market Outlook:

Semiconductor Manufacturing Equipment Market size was over USD 123.13 billion in 2025 and is anticipated to cross USD 280.97 billion by 2035, growing at more than 8.6% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of semiconductor manufacturing equipment is assessed at USD 132.66 billion.

Manufacturers are significantly developing advanced semiconductor fabrication plants to address the rising global demand for semiconductors in industries such as consumer electronics, automotive, and data center infrastructures. In November 2023, Texas Instruments (TI) began construction of a new 300-mm wafer fabrication facility, LFAB2, in Lehi, Utah. The plant is expected to produce tens of millions of analog and embedded processing chips per day and generate approximately 800 direct jobs, along with thousands of indirect employment opportunities. Such developments demonstrate the need for enhanced chip production capacity to support the digital transformation across sectors.

Key Semiconductor Manufacturing Equipment Market Insights Summary:

Regional Highlights:

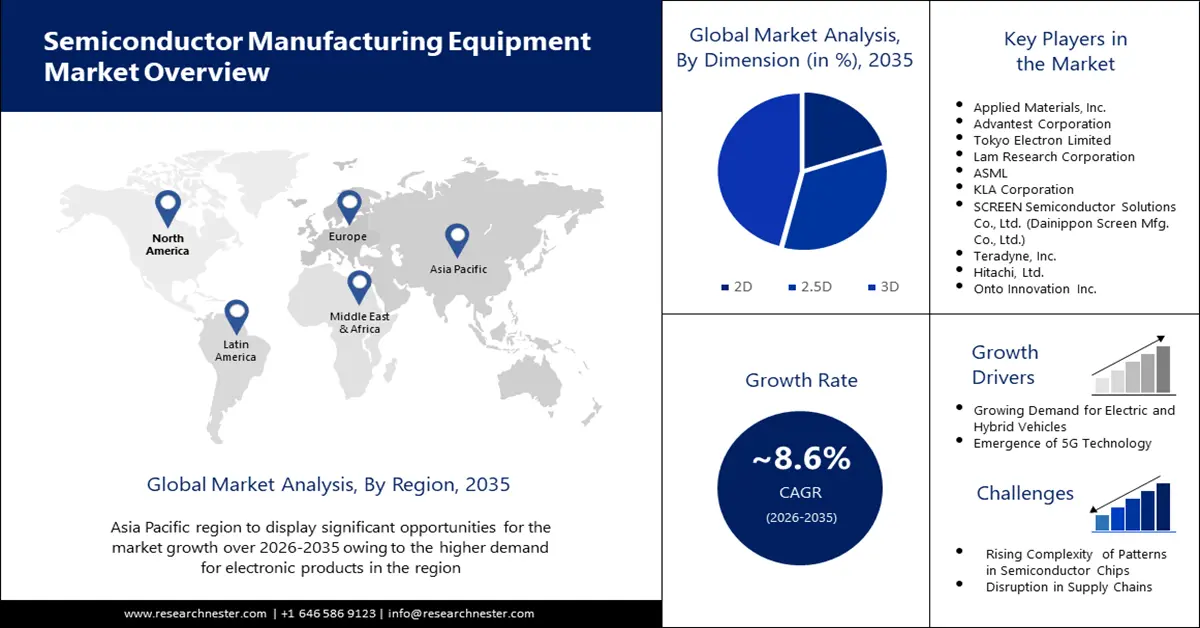

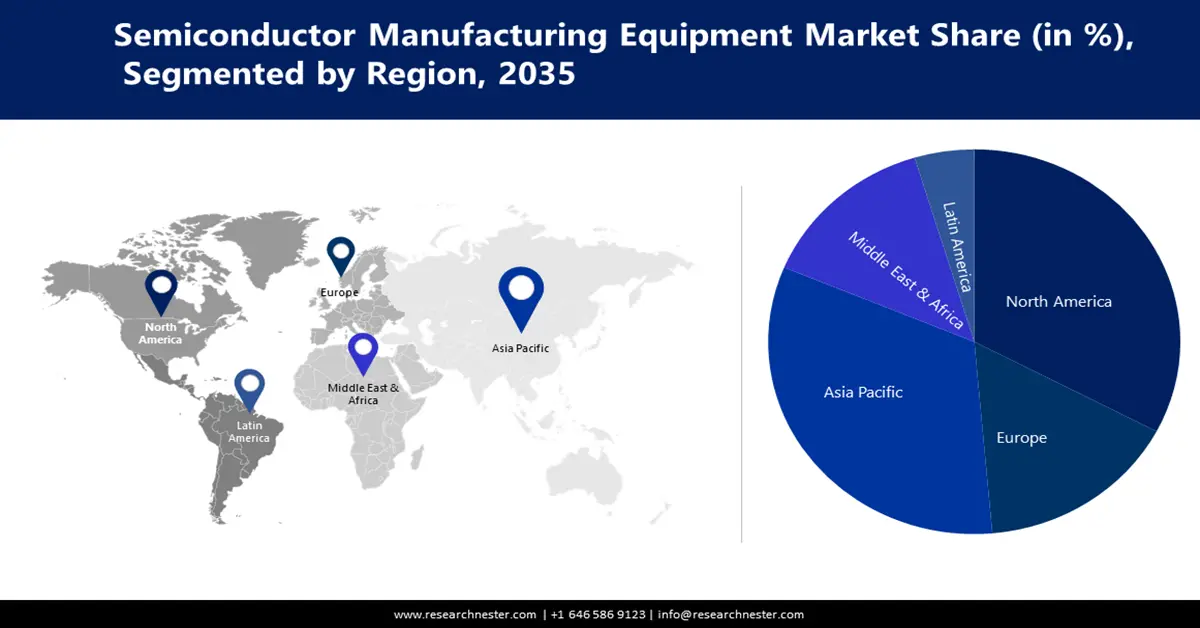

- The Asia Pacific semiconductor manufacturing equipment market is projected to capture a 35% share by 2035, fueled by rising development efforts in advanced semiconductor packaging technologies.

- The North America market is expected to secure a 24% share by 2035, attributed to the strong presence of chip manufacturers and equipment suppliers.

Segment Insights:

- The 3d segment in the semiconductor manufacturing equipment market is projected to secure a 46% share by 2035, driven by AI-driven tools for better yield and inspection accuracy.

- The front-end equipment segment in the semiconductor manufacturing equipment market is projected to hold a 41% share by 2035, influenced by the demand for advanced 3D IC manufacturing equipment.

Key Growth Trends:

- Shift towards electric and autonomous vehicles

- Demand for smaller node technologies

Major Challenges:

- Lengthy lead times and equipment delivery

Key Players: Applied Materials, Inc., Advantest Corporation, Tokyo Electron Limited, Lam Research Corporation, ASML, KLA Corporation, SCREEN Semiconductor Solutions Co., Ltd. (Dainippon Screen Mfg. Co., Ltd.), Teradyne, Inc., Hitachi, Ltd., Onto Innovation Inc.

Global Semiconductor Manufacturing Equipment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 123.13 billion

- 2026 Market Size: USD 132.66 billion

- Projected Market Size: USD 280.97 billion by 2035

- Growth Forecasts: 8.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Japan, South Korea, China, Germany

- Emerging Countries: China, Japan, South Korea, Taiwan, Singapore

Last updated on : 11 September, 2025

Semiconductor Manufacturing Equipment Market Growth Drivers and Challenges:

Growth Drivers

- Shift towards electric and autonomous vehicles: The automotive industry's shift toward electric and autonomous vehicles requires more semiconductors, as these vehicles need numerous electronic components for operation. Various governments are rolling out initiatives to strengthen the semiconductor supply chain, primarily through emerging technology sectors, including electric vehicles. In December 2024, the U.S. Department of Commerce reached a preliminary agreement with Bosch to provide up to USD 225 million in subsidies for the production of silicon carbide power semiconductors at its Roseville, California facility. This funding supports Bosch's USD 1.9 billion investment to transform its manufacturing facility, aiming to start producing SiC chips by 2026. The initiative demonstrates that the electric vehicle transition produces substantial capital inflows to create specialized chip production capacities for rising automotive markets.

- Demand for smaller node technologies: The semiconductor industry requires advanced manufacturing tools to perform production of 5nm and 3nm process nodes as smaller technology demands are advancing. Organizations are accelerating the development of next-generation lithography solutions that satisfy the scaling requirements of modern-day semiconductor nodes. In December 2023, ASML shipped its first High-NA (Numerical Aperture) EUV lithography system to Intel. This next-generation tool, priced at around USD 300 million, enhances resolution and precision, enabling the production of more complex and efficient chips. The deployment of such systems enables industry progress toward developing enhanced, miniaturized, powerful devices.

Challenges

- Lengthy lead times and equipment delivery: The semiconductor equipment production requires long delivery periods, especially among highly complex tools like EUV lithography machines, creating a significant challenge for chipmakers. The delayed capacity from semiconductor fabrication plants is becoming a problem due to prolonged wait times. Different parts of the manufacturing process cannot adapt quickly enough to handle market requirements, including AI technology, electric vehicles, and consumer electronics. Rapid scaling is also hampering the market, affecting the industry’s agility.

Semiconductor Manufacturing Equipment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

8.6% |

|

Base Year Market Size (2025) |

USD 123.13 billion |

|

Forecast Year Market Size (2035) |

USD 280.97 billion |

|

Regional Scope |

|

Semiconductor Manufacturing Equipment Market Segmentation:

Equipment

The front-end equipment segment is anticipated to generate the largest revenue share of 41% by the end of 2035. Advancing front-end equipment is essential with the rising industry focus on implementing 3D ICs to boost performance while minimizing size. Companies are constantly reinventing their equipment products to adapt to the changing, advanced semiconductor manufacturing needs. In December 2024, Tokyo Electron introduced the LEXIA-EX sputtering system, designed for next-generation memory devices. This system offers improved film uniformity, higher throughput, and a reduced footprint, aligning with the demands of 3D IC manufacturing. The semiconductor industry is increasingly implementing technological developments, due to heightened demand for advanced equipment.

Dimension

The 3D segment is set to hold 46% share of the semiconductor manufacturing equipment market through the forecasted timeframe. AI-driven tools detect anomalies with increased speed and enhanced precision, thus reducing the manual inspection hours for better yield results. These capabilities remain especially essential when dealing with complex 3D chip architectures, as standard metrology systems do not possess sufficient capability. AI integration enables manufacturers to use predictive maintenance for faster process control while learning from production data, they obtain higher production speeds and shorter downtime instances. The demand for semiconductors is driving next-generation 3D metrology equipment throughout its complete value chain.

Our in-depth analysis of the global market includes the following segments:

|

Equipment |

Front-End Equipment

Back-End Equipment

Fab Facility Equipment

|

|

Product |

|

|

Dimension |

|

|

Supply Chain Participant |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Semiconductor Manufacturing Equipment Market Regional Analysis:

Asia Pacific Market Insights

The Asia Pacific semiconductor manufacturing equipment market is expected to account for a share of 35% in 2035, due to the rising development efforts in advanced semiconductor packaging technologies. Countries including South Korea and Taiwan are significantly investing in 2.5D and 3D integrated circuit technologies as these methods help run high-performance computing systems and AI. The market is expanding as the equipment revolution necessitates next-generation front-end and back-end solutions.

The China semiconductor equipment market is rapidly expanding as its domestic chip design industry is increasing. Local companies that develop their own processors, memory, and AI chips are creating a rising demand for customized fabrication tools that deliver precise operation. The local manufacturers are making significant investments to strengthen both production facilities and local supply chains.

North America Market Analysis

The semiconductor manufacturing equipment market in North America is expected to account for a market share of 24% during 2026-2035. The market is experiencing massive growth due to the strong presence of chip manufacturers and equipment suppliers. Various companies are investing heavily in EUV lithography technology and advanced packaging owing to the rising requirement of highly specialized fabrication equipment. This expertise is generating innovation and increased demand for the cutting-edge industry equipment.

Supply chain resilience efforts and semiconductor production reshoring are standing as crucial determinants for the market growth. Public and private sectors are collaborating to maintain chip fabrication plant expansion, as part of plans to reduce foreign dependency on semiconductor products. The drive toward domestic production is fueling demand for front-end and back-end manufacturing equipment throughout the semiconductor industry.

The growth of the U.S. market is accelerating owing to rising partnerships between private and public entities that promote technological self-sufficiency. Such partnerships encourage innovation for chip design and fabrication while driving higher investments into advanced semiconductor equipment. Next-generation materials and tools are emerging from research collaborations between institutional groups and businesses, boosting the market growth.

Semiconductor Manufacturing Equipment Market Players:

- Applied Materials, Inc.

- Company Overview

- Business Strategy

- Key Technology Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Advantest Corporation

- Tokyo Electron Limited

- Lam Research Corporation

- ASML

- KLA Corporation

- SCREEN Semiconductor Solutions Co., Ltd. (Dainippon Screen Mfg. Co., Ltd.)

- Teradyne, Inc.

- Hitachi, Ltd.

- Onto Innovation Inc.

The semiconductor manufacturing equipment market is highly competitive, dominated by key global players such as ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA Corporation. These companies consistently invest in R&D to develop cutting-edge technologies like EUV lithography, atomic layer deposition, and advanced metrology tools. Strategic collaborations, mergers, and geographic expansions are common as players aim to strengthen their market positions. The market also sees growing competition from emerging Asian manufacturers, particularly in China and South Korea, driving innovation and pricing dynamics. With increasing global demand for semiconductors, competition continues to intensify across front-end and back-end equipment segments. Here are some key players operating in the global market:

Recent Developments

- In September 2023, Camtek Ltd. announced the acquisition of FormFactor Inc.’s FRT Metrology business for USD 100 million. FRT, based in Germany, specializes in precision metrology for Advanced Packaging and Silicon Carbide markets. The deal strengthens Camtek’s 3D metrology capabilities with FRT’s SurfaceSens technology, enhancing inspection solutions for next-gen semiconductor manufacturing.

- In June 2023, Lam Research launched the Coronus DX, the industry's first bevel deposition solution. This innovative system applies a protective film to both sides of a wafer's edge in a single operation, addressing critical manufacturing challenges in next-generation logic, 3D NAND, and advanced packaging applications.

- Report ID: 5058

- Published Date: Sep 11, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Semiconductor Manufacturing Equipment Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.