Robotic Radiotherapy Market Outlook:

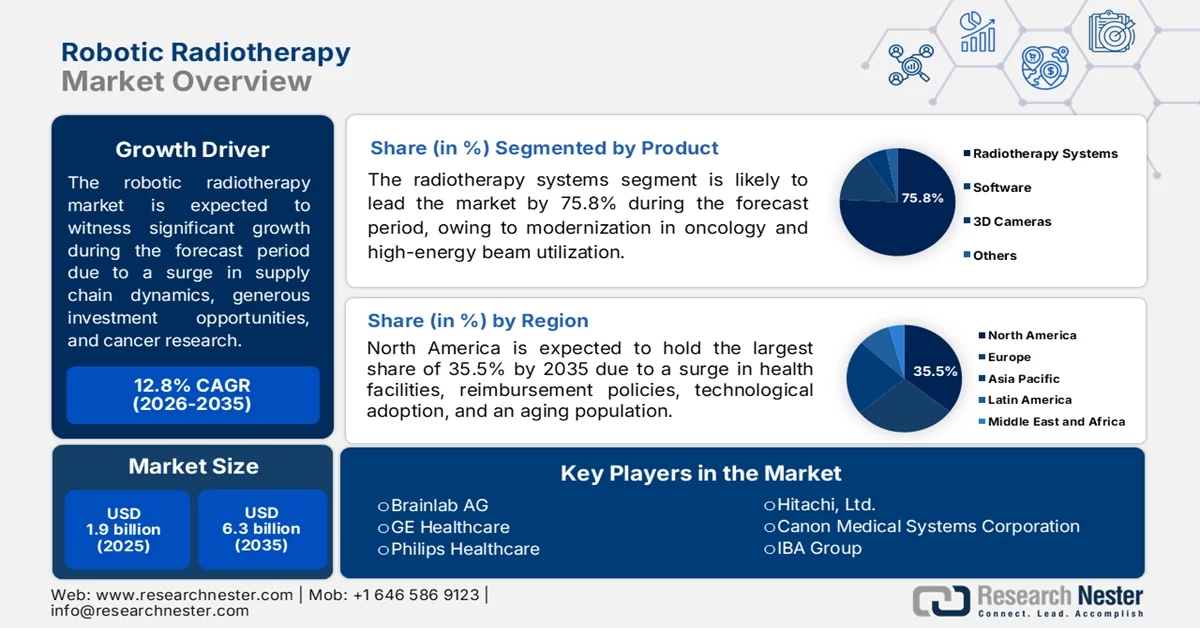

Robotic Radiotherapy Market size was valued at USD 1.9 billion in 2025 and is expected to reach USD 6.3 billion by the end of 2035, growing at around 12.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of robotic radiotherapy is evaluated at USD 2.1 billion.

The worldwide robotic radiotherapy market is effectively shaped by tariff adjustments, especially in China and the U.S., an increase in semiconductor chips, imaging sensors, and robotic arms, diversification in hospitals and supply chains, and an increase in funding opportunities for conducting in-depth cancer research. According to official statistics published by the Lung Cancer Research Foundation in 2026, 24,990 deaths took place from lung cancer, for which USD 3,936 funding has been provided per cancer death. Likewise, there were 36,320 deaths from prostate cancer for which USD 8,562 has been provided for research, along with USD 17,343 for 42,670 deaths from breast cancer, and USD 5,536 for 52,740 deaths from pancreatic cancer. Apart from this, the volume of radiotherapy equipment readily varies from country to country, based on which, there is a huge growth opportunity for the market globally.

Radiotherapy Equipment Volume Analysis (Per 1,000,000 Inhabitants) by Country, 2024

Source: OECD

Furthermore, the stereotactic and hypofractionated treatment protocols, geographic expansion of particle and proton therapy facilities, along with compact and vault-free system configurations, are a few trends that are responsible for driving the market globally. As stated in an article published by NLM in June 2025, artificial intelligence (AI)-based robotic surgeries indicated a 25% reduction in medical operation duration, along with 30% decrease in intraoperative complications, in comparison to manual technologies. In addition, there has been an improvement in surgical precision by 40%, which has been effectively reflected in enhanced accuracy during implant placements and tumor resections. Simultaneously, there has also been an average 20% increase in surgeon-based workflow efficacy as well as a 10% lower in healthcare expenses over traditional procedures, thus boosting the market exposure.

Key Robotic Radiotherapy Market Insights Summary:

Regional Highlights:

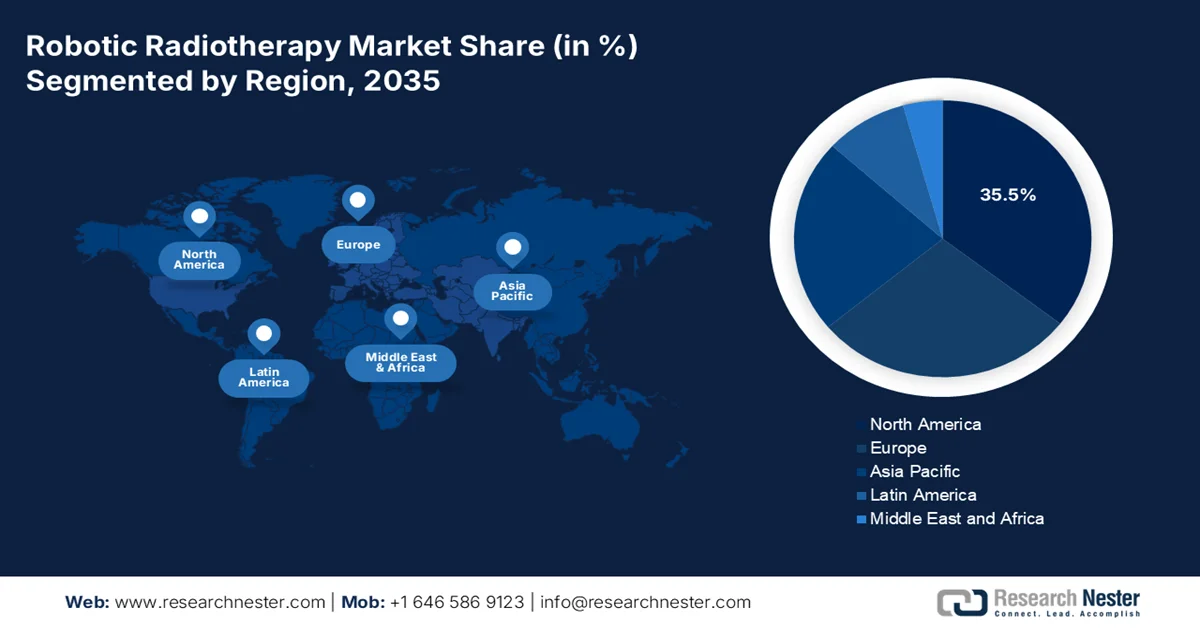

- The North America region is anticipated to capture 35.5% share of the robotic radiotherapy market by 2035, impelled by advanced healthcare infrastructure, favorable reimbursement policies, rising cancer prevalence, and accelerated adoption of non-invasive precision treatments

- Asia Pacific is projected to emerge as the fastest-growing region in the market throughout 2026-2035, propelled by rapid population aging, increasing tumor incidence, government-backed healthcare modernization, and expanding AI-integrated treatment planning

- The robotic radiotherapy market in the U.S. accounts for 31.9% share in North America, which is fueled by a surge in cancer treatment facilities, the integration of high-precision technologies, and aggressive reimbursement pathways for accessing radiotherapy services.

- The robotic radiotherapy market in Japan has grabbed 4.1% share in the Asia Pacific, owing to an increase in MRI equipment exports, the strong commercialization and production processes, and an upsurge in cancer patients.

Segment Insights:

- The radiotherapy systems segment is expected to dominate the robotic radiotherapy market with a 75.8% share by 2035, owing to the rising utilization of targeted high-energy beam technologies for precise cancer cell destruction and expanding availability of radioactive chemicals across global trade networks

- The linear accelerators segment is projected to secure the second-highest share during the forecast period, catalyzed by increasing global demand for high-precision radiotherapy devices amid persistent shortages in radiotherapy infrastructure across multiple income-level nations

Key Growth Trends:

- Increase in AI-based adaptive radiotherapy

- Surge in government infrastructure modernization

Major Challenges:

- Regulatory fragmentation and approval delays

- Integration with existing hospital workflows and IT systems

Key Players: Accuray Incorporated, Varian Medical Systems, Siemens Healthineers, Elekta AB, Brainlab AG, GE Healthcare, Philips Healthcare, Hitachi, Ltd., Canon Medical Systems Corporation, IBA Group, ViewRay, Inc., Mevion Medical Systems, C-RAD AB, RaySearch Laboratories AB, Best Theratronics Ltd., Nordion, Inc., Neusoft Medical Systems Co., Ltd., Huiheng Medical, Inc., MASEP Medical Science & Technology Development Co., Ltd., Zhuhai Hokai Medical Instruments Co., Ltd., Precision NeuroMed.

Global Robotic Radiotherapy Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.9 billion

- 2026 Market Size: USD 2.1 billion

- Projected Market Size: USD 6.3 billion by 2035

- Growth Forecasts: 12.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, Singapore, South Korea, Brazil, United Arab Emirates

Last updated on : 27 May, 2026

Robotic Radiotherapy Market - Growth Drivers and Challenges

Growth Drivers

- Increase in AI-based adaptive radiotherapy: The aspect of AI adoption is specifically fueling the robotic radiotherapy market and ensuring the ability to modify treatment approaches in real-time anatomical changes. According to official statistics published by NLM in September 2025, AI-driven contouring tools in radiotherapies tend to diminish time spent contouring by almost 92%, thus making them suitable for maintaining increased levels of clinician satisfaction. Simultaneously, AI-based auto-segmentation has the ability to diminish contouring duration from nearly 60 minutes to only 2 minutes per case. This, in turn, significantly translates to yearly savings of an estimated 1,000 clinician hours that tend to redirect patient care, thus positively impacting the market growth.

- Surge in government infrastructure modernization: The presence of suitable government-based radiotherapy equipment replacement programs is escalating the adoption across both emerging and developed countries. For instance, as per the May 2025 UK Government article, radiotherapy machines in the UK reduce waiting times and assist more than 4,500 patients with rapid treatment facilities. This particular upgraded technology has been successfully rolled out in 28 hospitals, and this rollout is significantly backed by USD 94.2 million, which has been offered by the government as part of the approach to optimize cancer care through the Plan for Change strategy. Moreover, based on this, different patients tend to benefit from safe and rapid cancer treatment, thereby denoting an optimistic outlook for the market’s growth and expansion.

Challenges

- Regulatory fragmentation and approval delays: Global manufacturers seeking industry accessibility need to navigate a complex web of divergent regulatory frameworks across jurisdictions, each with unique documentation requirements, clinical evidence standards, and review timelines. Besides, a system approved by the FDA may require substantial modifications or additional clinical trials before gaining clearance from China's NMPA or India's CDSCO. Besides, Europe's transition under the new Medical Device Regulation (MDR) has introduced stricter scrutiny for legacy devices, forcing some manufacturers to re-certify existing products at significant expense. These regulatory disparities create supply chain inefficiencies and delay patient access to innovative technologies by months or even years, thus restricting the market.

- Integration with existing hospital workflows and IT systems: The implementation of robotic radiotherapy systems into established clinical workflows presents substantial operational challenges that extend beyond simple hardware installation. For instance, hospital radiation oncology departments typically operate with legacy record-and-verify systems, treatment planning platforms, and electronic medical records that were not designed to interface with modern robotic interfaces. Moreover, data exchange between the robotic system and hospital information systems often requires custom middleware or manual data entry, introducing potential points of error and administrative burden. Therefore, all these challenges have caused a hindrance in the market.

Robotic Radiotherapy Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.8% |

|

Base Year Market Size (2025) |

USD 1.9 billion |

|

Forecast Year Market Size (2035) |

USD 6.3 billion |

|

Regional Scope |

|

Robotic Radiotherapy Market Segmentation:

Product Segment Analysis

The radiotherapy systems segment, part of the product, is anticipated to register at the highest share of 75.8% in the robotic radiotherapy market by the end of 2035. The segment’s upliftment is primarily attributed to its crucial role in modernized oncology, which is increasingly utilized for targeting high-energy and targeted beams for damaging the DMA of cancer cells. According to official statistics published by NLM in May 2023, the World Health Organization (WHO) has successfully set the global approach for eliminating cervical cancer, which includes the objective of 90% of women with invasive cancer. Besides, the increased availability of the human papillomavirus vaccine is poised to decrease mortality by the end of 2030. Moreover, an upsurge in the availability of radioactive chemicals and their continuous shipment in massive volumes through export and import dynamics is also boosting the segment’s demand and growth.

2024 Radioactive Chemicals Global Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Kazakhstan |

4.7 billion |

- |

|

Canada |

4.3 billion |

- |

|

Russia |

2.9 billion |

1.8 billion |

|

U.S. |

- |

7.1 billion |

|

China |

- |

3.6 billion |

|

Global Trade Valuation |

25.0 billion |

|

|

Global Trade Share |

0.1% |

|

|

Export Growth |

29.4% |

|

Source: OEM

Technology Segment Analysis

Based on technology, the linear accelerators segment is projected to account for the second-highest share in the market during the forecast period. The segment’s growth is effectively fueled by their utilization as critical devices in modernized physics and oncology for generating targeted and high-energy electrons or X-rays precisely and eradicate tumors, while protecting healthy tissues. As stated in an article published by NCBI in February 2025, a clinical study was conducted on cancer incidence data, the number of radiotherapy facilities, and the distribution of linear accelerators across 181 countries. This study demonstrated that the global median linear accelerator shortage index (LSI) was 130, which suggested a 30% limitation in radiotherapy capacity. Besides, the LSI across low-income nations was 1,523, 399 in middle-income countries, 133 in upper-middle-income regions, and 96 across high-income nations. Therefore, this ensures a huge demand for linear accelerators across different nations, which in turn, is escalating the market demand.

Application Segment Analysis

By the end of the stipulated timeline, the lung cancer sub-segment, which is part of the application segment, is expected to grab the third-highest share in the market. The sub-segment’s development is highly propelled by its recognition as the most commonly diagnosed cancer worldwide, along with the notable cause of cancer-based deaths. As per an article published by the WHO in April 2026, there were approximately 2.5 million new lung cancer cases, as well as 1.8 million deaths, as of 2022. In addition, over 1.3 million cases among the male population and almost 500,000 cases among the female population are preventable, with the majority constituting to tobacco smoking, significantly accounting for 60% to 70%, which is followed by occupational exposure and air pollution, thereby denoting a huge growth opportunity for the market globally.

Our in-depth analysis of the robotic radiotherapy includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Technology |

|

|

Application |

|

|

End user |

|

|

Software |

|

|

Particle Therapy |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Robotic Radiotherapy Market - Regional Analysis

North America Market Insights

North America in the robotic radiotherapy market is anticipated to account for the largest share of 35.5% by the end of 2035. The market’s upliftment in the region is primarily attributed to the presence of healthcare infrastructure, favorable reimbursement policies, early technological integration, a rise in cancer incidences, an aging population, and the sudden shift to non-invasive precision treatments. According to official statistics published by the American Hospital Association in 2026, the U.S. comprises 6,100 hospital facilities, which makes it suitable for conducting radiotherapies. In this regard, freestanding and single hospitals in the country are categorized as a suitable system by ensuring more than 3 memberships, along with 25% of leased or owned non-hospital post-acute or pre-acute healthcare organizations, thereby positively impacting the market growth in the region.

Total Number of Hospitals in the U.S., 2026

|

Hospital Type |

Number |

|

Community Hospitals |

5,121 |

|

Non-Government Not-for-Profit Community Hospitals |

2,984 |

|

Investor-Based Community Hospitals |

1,224 |

|

Local and State Government Community Hospitals |

913 |

|

Federal Government Hospitals |

210 |

|

Non-Federal Psychiatric Hospitals |

656 |

|

Other Hospitals |

113 |

|

Total Staff Beds in Hospitals |

907,216 |

|

Staffed Beds in Community Hospitals |

775,297 |

|

Overall Admissions in Hospitals |

35,658,583 |

|

Admissions in Community Hospitals |

22,553,725 |

|

Rural Community Hospitals |

1,797 |

|

Urban Community Hospitals |

3,324 |

|

Community Hospitals in a System |

3,567 |

Source: American Hospital Association

The robotic radiotherapy market is growing significantly in the U.S., owing to generous federal budget allocations for conducting cancer-based research, along with suitable Medicaid support, Medicare investments, and primary reimbursement services for the patient population. As stated in an article published by the NIH in September 2025, the Childhood Cancer Data Initiative (CCDI), since its establishment, has continued to collect, generate, and analyze cancer data for children, with a rise in its budget from USD 50 million to USD 100 million. This particular funding opportunity is suitable for escalating the development of optimized diagnostics, treatments, and prevention strategies. Through this ongoing research ability, it has been identified that pediatric cancer is one of the leading causes of disease-specific death for children in the country, and its incidence has surged by more than 40%, thus driving the market upliftment.

The provision of a generous federal budget, an increase in provincial spending for expanding radiotherapy services and the launch of the newest radiation oncology equipment, along with suitable national coverage, are certain factors that are proliferating the market in Canada. As per an article published by the Government of Canada in February 2026, cancer is estimated to cost families, patients, and healthcare systems in the country almost USD 37.7 billion annually, from medications and hospital care to out-of-pocket expenses, reduced productivity, and lost wages. However, almost 40% of domestic cancer cases can be prevented through modifications in environmental and lifestyle factors. Besides, the government and its partners readily invested more than USD 41 million in ground-breaking cancer prevention research, thereby enhancing the market growth.

APAC Market Insights

The Asia Pacific in the robotic radiotherapy market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the rapid aging population, a rise in tumor incidence, strong government-based infrastructure modernization, technological adoption, reduction in construction expenses, and the incorporation of AI-based treatment plans. According to official statistics published by NLM in September 2025, the Association of Southeast Asian Nations (ASEAN) significantly accounted for 9.3% of the worldwide cancer incidence, with Singapore constituting the highest age-standardized incidence rate (ASIR) of 231.1 and Myanmar at the lowest with 135.5. Meanwhile, the Philippines constituted the highest age-standardized mortality rate (ASMR) at 112.9, with lung cancer accounting for the highest 26.0 ASIR among the male population, thus enhancing the market development in the overall region.

The robotic radiotherapy market is gaining increased traction in China, owing to an escalation in approvals for radiotherapy systems, the government’s Healthy China 2030 plan, an increase in health and medical expenditure, growth in the oncology field, dependency on international vendors, and the latest installations by domestic manufacturers. As stated in an article published by Frontiers Organization in February 2022, nearly 4.5 million new cancer incidences and 3 million cancer-based deaths have been recorded in the country. Besides, to combat the disorder, almost 8,000 patients in the country are treated with carbon ion, proton, or a combined carbon ion and proton therapy. Moreover, chemotherapy, radiotherapy, and surgery are the standard methods for treating cancer in the country, thereby denoting a huge growth opportunity for the market.

The aspects of generous funding allocation for ensuring advanced cancer medical research, an increase in accessing carbon-ion therapy, an upsurge in operational facilities, an expansion in the patient population, and a focus on high-cost particle therapy are a few trends that are responsible for enhancing the robotic radiotherapy market demand in Japan. Besides, the Japan robotic radiotherapy market was valued at USD 72.1 million as of 2025, which is projected to reach USD 80.5 million by the end of 2026, and further reach USD 218 million, along with a recording a 12.5% growth rate by 2035. As per an article published by the Commonwealth Fund Organization in May 2026, the total health and medical expenditure in the form of gross domestic product (GDP) caters to 11%, along with 84.1 years of total life expectancy at birth, and the provision of 100% public insurance coverage, thereby positively impacting the market’s development in the country.

Europe Market Insights

Europe in the market is projected to witness considerable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by a transition from conventional surgery to adopting non-invasive techniques, a rise in the incidence of prostate cancer among the elderly population, and suitable strategies for diminishing waiting lists. According to official statistics published by NLM in September 2024, the variation of prostate cancer differed from 6 cases in Ukraine to 336 cases in France per 100,000 male population. Moreover, the differentiation between the highest and lowest prevalence rates across regional nations ranged from 89.6 per 100,000 men to 385.8 per 100,000 men. Meanwhile, the mortality rates across countries also ranged from 23.7 per 100,000 men to 5.6 per 100,000 men, thereby denoting an optimistic outlook for the market expansion.

The market is gaining increased exposure in Germany, owing to the presence of private insurance models, federal funding parity, strong DRG-based reimbursement codes, organizational contributions, and the existence of hospital systems. As stated in an article published by the Commonwealth Fund Organization in 2026, the overall healthcare expenditure in the form of GDP significantly accounted for 12.3%, along with 80.9 years as life expectancy at birth and 100% public insurance coverage services. Besides, the statutory health insurance (SHI) covered almost 89% of the population in the country as of December 2023. Additionally, this SHI was compulsory for all employed citizens with a gross yearly income lower than USD 65,174, thereby making it suitable for driving the market exposure in the nation.

Insurance Coverage in Germany Based on Population, 2023

Source: Commonwealth Fund Organization

The existence of centralized mandates, suitable health policy requirements, an increase in pancreatic and central lung cancers, the government’s Health Innovation 2030 approach, and an effective procurement pipeline for vendors are certain trends that are driving the market in France. As per a data report published by the Department of Health and Social Care in January 2026, the Health Innovation 2030 plan is focused on developing neighborhood health services, which are predicted to cover almost 50,000 people, with solutions and strategies that require operating on a massive landscape, which is effectively organized across a huge population of more than 250,000. Besides, the transition of services from hospitals to the community demonstrated an increase in investments by an average 15% in the case of lower non-elective admission rates and 10% for low ambulance conveyance rates, thereby boosting the market expansion in the country.

Key Robotic Radiotherapy Market Players:

- Accuray Incorporated (U.S.)

- Varian Medical Systems (U.S.)

- Siemens Healthineers (Germany)

- Elekta AB (Sweden)

- Brainlab AG (Germany)

- GE Healthcare (U.S.)

- Philips Healthcare (Netherlands)

- Hitachi, Ltd. (Japan)

- Canon Medical Systems Corporation (Japan)

- IBA Group (Belgium)

- ViewRay, Inc. (U.S.)

- Mevion Medical Systems (U.S.)

- C-RAD AB (Sweden)

- RaySearch Laboratories AB (Sweden)

- Best Theratronics Ltd. (Canada)

- Nordion, Inc. (Canada)

- Neusoft Medical Systems Co., Ltd. (China)

- Huiheng Medical, Inc. (China)

- MASEP Medical Science & Technology Development Co., Ltd. (China)

- Zhuhai Hokai Medical Instruments Co., Ltd. (China)

- Precision NeuroMed (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Accuray Incorporated is recognized for its CyberKnife platform, which remains a dedicated robotic radiosurgery system designed to treat tumors anywhere in the body with sub-millimeter precision. The company focuses on expanding its Synchrony motion tracking technology to address complex oncological cases that move with patient respiration.

- Varian Medical Systems established a strong presence by integrating robotic precision into its versatile linear accelerator platforms for mainstream radiotherapy departments. The company emphasizes adaptive intelligence and workflow automation to enhance the efficiency of robotic treatments across multiple cancer sites.

- Siemens Healthineers leveraged its expertise in diagnostic imaging to advance MRI-guided robotic radiotherapy systems that enable real-time soft tissue visualization during treatment. The company focuses on developing integrated solutions that combine high-field magnetic resonance with precise radiation delivery.

- Elekta AB developed a robust portfolio of linear accelerator-based systems that incorporate advanced motion management and stereotactic capabilities. The company prioritizes software-driven solutions that enable clinics to perform robotic-quality treatments on conventional hardware platforms.

- Brainlab AG readily specializes in precision software and navigation solutions that enhance the targeting accuracy of robotic radiotherapy systems. The company focuses on developing integrated platforms that bridge surgical navigation and radiation oncology workflows.

Here is a list of key players operating in the global market:

The robotic radiotherapy market features a consolidated competitive landscape dominated by U.S.-headquartered leaders Accuray and Varian, followed closely by Europe-based players, such as Elekta in Sweden and Brainlab in Germany. Key strategic initiatives include Accuray's focus on expanding its CyberKnife platform's Synchrony respiratory tracking capabilities, while Varian (Siemens Healthineers) integrates AI-driven adaptive workflows into its systems. Besides, in February 2026, Brainlab and Precision NeuroMed formed a strategic partnership, with the intention of standardizing and upscaling the delivery of targeted therapies into brain tissue directly. This collaboration assisted in combating the restrictions of the blood-brain barrier by effectively combining Brainlab’s expertise in medical imaging digitalization, along with NeuroMed’s proprietary molecular flow simulation software, thus driving the robotic radiotherapy industry’s growth globally.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, Mevion Medical Systems signed a definitive purchase-based agreement to introduce the MEVION S250-FIT Proton Therapy System™, which is the first-ever proton therapy system, at Tam Anh General Hospital in Vietnam, reflecting a wide-ranging shift in cancer care.

- In April 2026, Siemens Healthineers has been awarded almost USD 60 million for more than 5 years by the U.S. Advanced Research Projects Agency for Health (ARPA-H) for accelerating the development of photon flash therapy, which is an ultra-high dose rate strategy to radiotherapy.

- In September 2025, Accuray Incorporated signed a memorandum of understanding with the University of Wisconsin School of Medicine and Public Health (UW SMPH) for advancing online adaptive radiotherapy on the company’s helical radiation treatment delivery platform.

- Report ID: 8584

- Published Date: May 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.