Pulmonary Embolism Drugs Market Outlook:

Pulmonary Embolism Drugs Market size was over USD 1.85 billion in 2025 and is anticipated to cross USD 3.34 billion by 2035, growing at more than 6.1% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of pulmonary embolism drugs is estimated at USD 1.95 billion.

The market growth is driven by increasing prevalence of cardiovascular diseases owing to the malfunction of arteries. Cardiovascular diseases are associated with blood vessels or the heart. It is a medical condition in which the circulation of blood to the brain, heart, and body is reduced owing to blood clots. Based on the data provided by the World Health Organization (WHO), in 2019, around 17.9 million people were observed to be suffering from cardiovascular disease.

In addition, rising awareness of healthy lifestyles promoting the importance of early diagnosis and a surge in the cases of cancer are estimated to expand the market size. Pulmonary embolism is observed to cause a significant number of cancers in the global population. For instance, around 5% of cancer-related deaths are accounted by pulmonary emboli which is a type of blood clot in the lungs. Furthermore, people suffering from cancer associated with the brain, lungs, stomach, and people who are noticed to be undergoing chemotherapy are at higher risk of getting pulmonary embolism. For instance, it was projected that there is estimated to be around 22 million cancer survivors owing to chemotherapy by the year 2032.

Key Pulmonary Embolism Drugs Market Insights Summary:

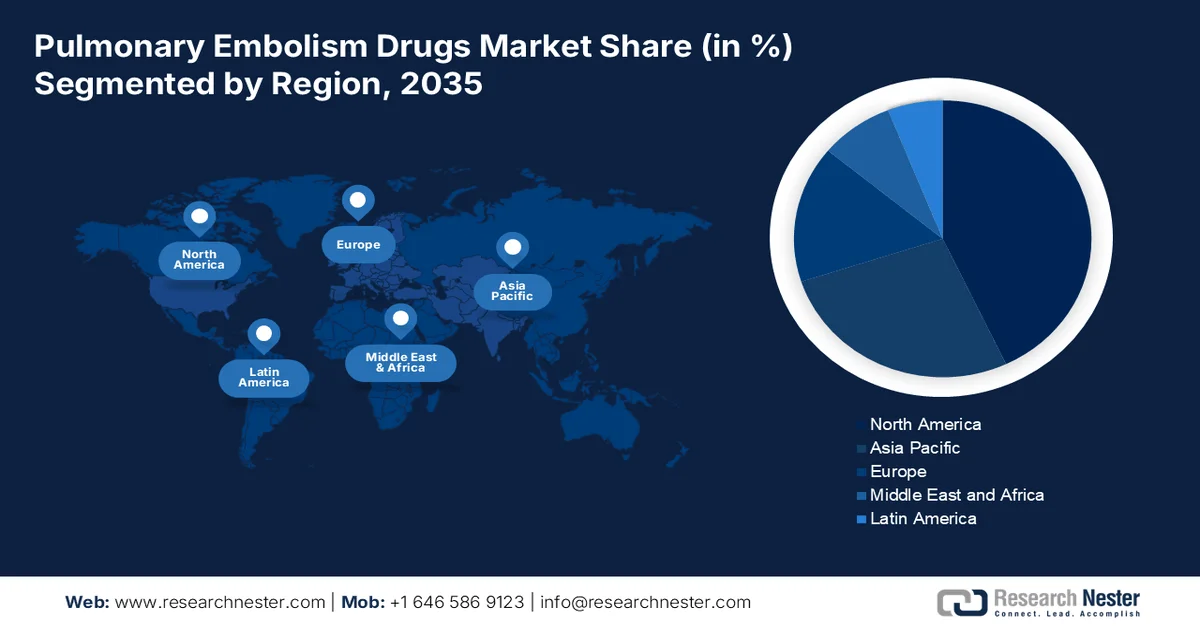

Regional Highlights:

- The North America pulmonary embolism drugs market is anticipated to command the majority share by 2035, driven by rising healthcare expenditure supported by escalating government spending to strengthen healthcare services.

- Asia Pacific is projected to witness substantial growth in the pulmonary embolism drugs market through 2026–2035, attributed to the high prevalence of cancer alongside expanding government initiatives to enhance medical support programs.

Segment Insights:

- The thrombosis segment in the pulmonary embolism drugs market is projected to gain the largest share by 2035, fueled by the rising global prevalence of venous thrombosis and increasing incidence among individuals aged above 45.

- The hospital pharmacies segment is anticipated to account for a significant share by 2035, propelled by expanding hospital infrastructure investments and the growing number of hospitals worldwide.

Key Growth Trends:

- Growing Prevalence of Bone Fractures

- Rising Awareness of Pulmonary Embolism Across the Globe

Major Challenges:

- Side Effects of Pulmonary Embolism Drugs

- Higher Possibility of Blood Clotting

Key Players: Water Office, ACCIONA, Harbin ROPV Industrial Co LTD, TotalEnergies SE, SUEZ, LG Nano H2O Inc, ACWA Power, Vontron Membrane Technology, Solar Water Solutions Ltd., Sinovoltaics Group.

Global Pulmonary Embolism Drugs Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.85 billion

- 2026 Market Size: USD 1.95 billion

- Projected Market Size: USD 3.34 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, Japan, France

- Emerging Countries: China, India, Japan, South Korea, Brazil

Last updated on : 25 February, 2026

Pulmonary Embolism Drugs Market - Growth Drivers and Challenges

Growth Drivers

-

Growing Prevalence of Bone Fractures - Bone fracture is one of the major reasons to cause of pulmonary embolism since during bone injury, fat around the muscle turns into broken blood vessels. When these symptoms are developed owing to a lack of medical attention, they turn into embolism syndrome. For instance, it was anticipated that nearly 1 million individuals suffer from bone fractures annually.

-

Rising Awareness of Pulmonary Embolism Across the Globe - In modern times, owing to the developing medical technology and the launch of new innovative diagnostic devices has spurred awareness of the early diagnosis of pulmonary embolism which is anticipated to hike the market growth over the forecast period. It was estimated that around 35% of people lose their lives before getting any sort of diagnosis and treatment.

-

Increasing Prevalence of Pulmonary Embolism (PE) - The prevalence of pulmonary embolism is so high that it is third behind heart attack and stroke. For instance, approximately 300,000 people lose their lives every year in the United States.

-

Growing Incidences of Heart Failure to Boost Market Growth - Heart failure is also considered to be one of the major causes of pulmonary embolism. For instance, it was estimated that approximately 6 million Americans aged above 20 have heart failure while 900,000 new cases of heart failure are diagnosed every year in the American region.

Challenges

-

Side Effects of Pulmonary Embolism Drugs - The possibility of side effects can be quite higher owing to the consumption of pulmonary embolism drugs such as chest pain, shortness of breath, anxiety, dizziness, fainting, and others. Hence, such a higher number of side effects owing to the consumption of these drugs was projected to hamper the growth of the market over the forecast period.

-

Higher Possibility of Blood Clotting

-

Lack of Awareness regarding Pulmonary Embolism Drugs

Pulmonary Embolism Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 1.85 billion |

|

Forecast Year Market Size (2035) |

USD 3.34 billion |

|

Regional Scope |

|

Pulmonary Embolism Drugs Market Segmentation:

Drug Class (Thrombolytics, Thrombosis, Heparins, Thrombin Inhibitors)

The thrombosis segment is estimated to gain largest market share by 2035. Thrombosis is a medical condition that is mainly caused by a lump of thick blood clots that forms in a blood vessel in the heart. Venous thrombosis is observed to be quite prevalent across the globe which is estimated to hike the market revenue. For instance, it was expected that every year, in every 1000, 1 of them suffer from venous thrombosis. The occurrence rate of thrombosis rises after the age of 45 and is quite higher in men than women. The risk factors of thrombosis include immobility, hospitalization, trauma, pregnancy, and others.

Distribution Channel (Hospital Pharmacy, Drug Store, Online Pharmacy)

The hospital pharmacies segment is predicted to account for significant market share by 2035. Hospitals are noticed to have luxury medical services in a single place. A huge staff of medical professionals is available to provide healthcare services 24/7. Furthermore, every nation is observed to spend a significant amount of money to develop hospital infrastructures to provide better medical services. The growth in the number of hospitals across the globe is anticipated to be backed by increasing income, population demographics, growing health awareness, and others.

Our in-depth analysis of the global market includes the following segments:

|

By Drug Class |

|

|

By Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Pulmonary Embolism Drugs Market - Regional Analysis

North American Market Forecast

The North American pulmonary embolism drugs market is anticipated to account for majority share by the end of 2035. The market growth is propelled by rising healthcare expenditure backed by escalating government spending to develop healthcare services. According to a report by the World Health Organization (WHO), as of 2018, the per capita healthcare expenditure of North America is valued at USD 10,050.279. Moreover, the presence of major pharmaceutical companies in the region will boost the market growth.

APAC Market Statistics

The Asia Pacific pulmonary embolism drugs market is predicted to observe massive growth during the forecast period, impelled by high prevalence of cancer in the region backed by growing government initiatives to launch and support programs to provide medical services for people living with cancer. For instance, in 2020, approximately 150 thousand people were estimated to be living with cancer in the Asia Pacific along with the high geriatric population, both of which are major causes of pulmonary embolism.

Europe Market Forecast

The Europe pulmonary embolism drugs market is set to hold a notable share by 2035. Factors such as, a higher prevalence of cancer in the region and higher demand for healthcare solution backed by increasing geriatric population will propel the market revenue. Moreover, the surge in research & development of pulmonary embolism drugs in the region will drive the market growth.

Pulmonary Embolism Drugs Market Players:

- Janssen Global Services, LLC

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Novartis AG

- Pfizer Inc.

- Sanofi S.A.

- Abbott Laboratories

- Merck & Co., Inc.

- Boehringer Ingelheim International GmbH

- Daiichi Sankyo Company, Limited

- Siemens Healthcare GmbH

- Baxter International Inc.

Recent Developments

-

Janssen Pharmaceuticals, Inc. revealed the results from Phase 3 A DUE study. This Phase 3 study is to represent investigational single-tablet combination therapy.

-

Novartis AG got approval for Tafinlar (dabrafenib) + Mekinist (trametinib) from U.S. Food and Drug Administration (FDA). These medications are used to treat pediatric patients or people with brain cancer.

- Report ID: 3400

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.