Preimplantation Genetics Diagnosis Market Outlook:

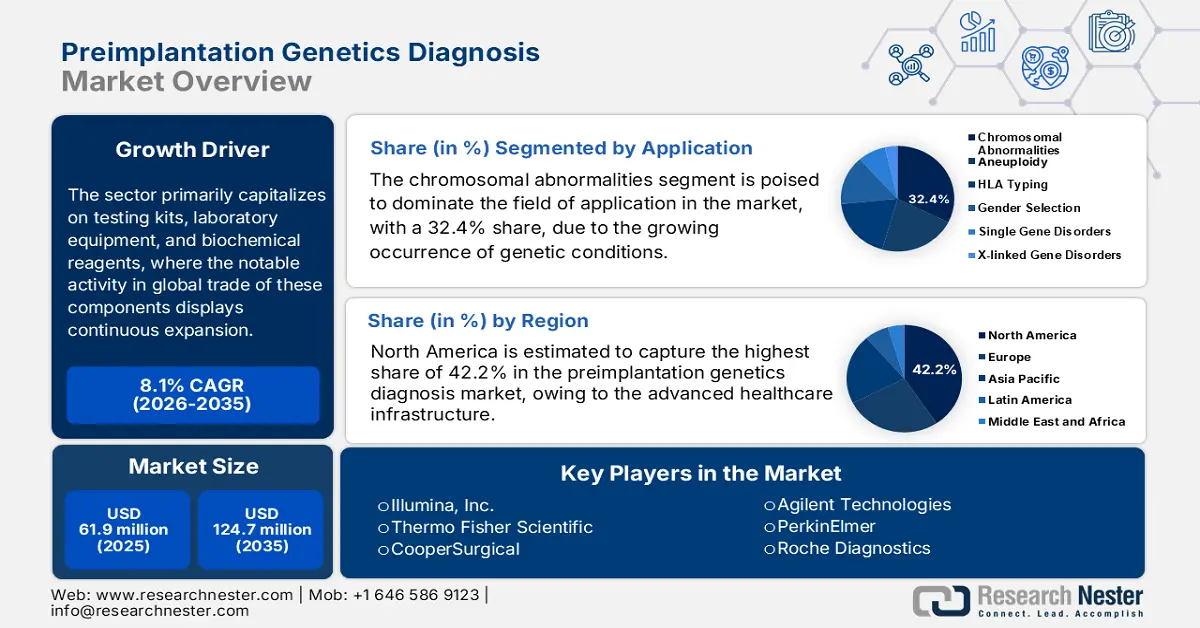

Preimplantation Genetics Diagnosis Market size was over USD 61.9 million in 2025 and is estimated to reach USD 124.7 million by the end of 2035, expanding at a CAGR of 8.1% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of preimplantation genetics diagnosis is estimated at USD 66.9 million.

The preimplantation genetics diagnosis market serves a substantial patient pool of infertility worldwide. This can be testified by the 2023 report from the World Health Organization (WHO), predicting 17.5% of the adult population around the globe to have this condition. It also mentioned the lifetime occurrence rate of infertility to be 17.8% in high-income countries and 16.5% in low- and middle-income countries (LMICs). This is subsequently creating a surge in assisted reproductive technologies (ART) such as preimplantation genetics diagnosis (PGD). The sector primarily capitalizes on testing kits, laboratory equipment, and biochemical reagents, where the notable activity in global trade of these components displays continuous expansion.

Portraying such dynamics in the market, the OEC reported that the value of globally traded enzymes totals $6.99 billion in 2023. However, regulatory and tariff controls over these critical products often create disparity in both accessibility and availability in the supply chain of this sector. This further translates to a remarkable increase in the payers’ pricing, making end-user services hard to afford and limiting the adoption of PGD assessments. Currently, both suppliers and research institutions are opting for next-generation sequencing (NGS) technologies to minimize this barrier. In this regard, a study published in March 2023 gave recognition to the NGS approach for comprehensive aneuploidy screening as a low-cost yet high-specificity option.

Key Preimplantation Genetics Diagnosis Market Insights Summary:

Regional Insights:

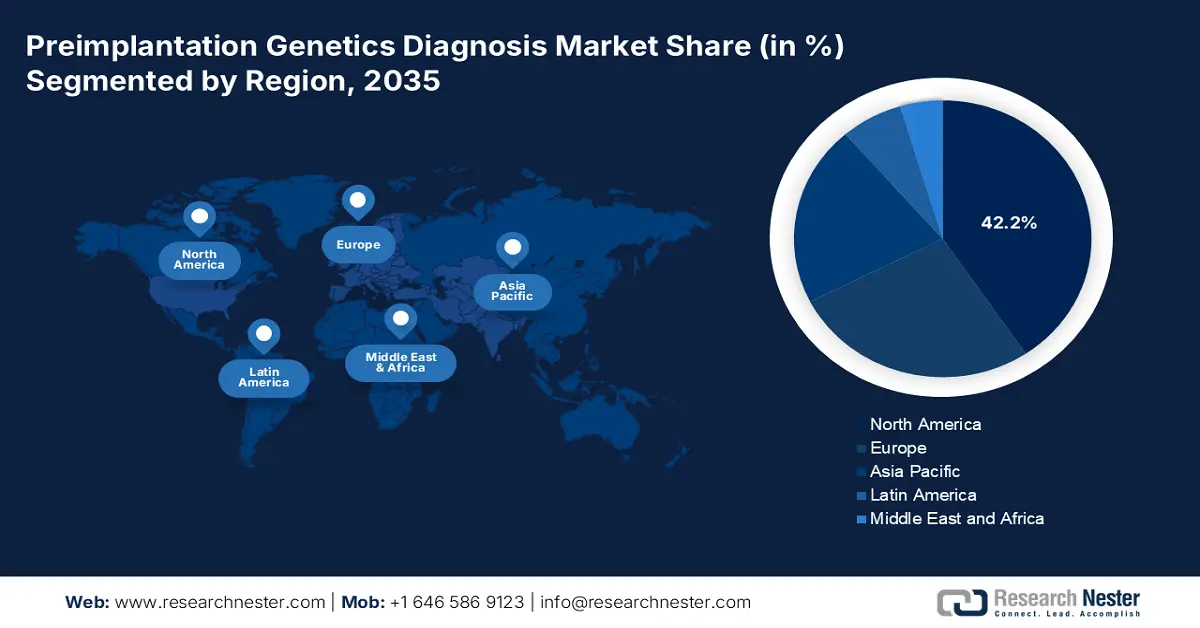

- North America is projected to command a 42.2% share in the preimplantation genetics diagnosis market by 2035, bolstered by advanced healthcare infrastructure, high ART adoption rates, and strong genetic-testing capabilities.

- Asia Pacific is anticipated to emerge as the fastest-expanding region through 2026–2035 in the sector, supported by rising reproductive health issues, growing awareness of genetic disorders, and improved access to PGD services.

Segment Insights:

- The chromosomal abnormalities segment is expected to secure a 32.4% share by 2035 in the preimplantation genetics diagnosis market, propelled by the escalating prevalence of genetic conditions among newborns.

- Next-generation sequencing (NGS) is set to hold a dominant 42.6% market share by 2035, owing to its high accuracy, scalability, and ability to detect multiple genetic conditions simultaneously.

Key Growth Trends:

- Wide application in detecting genetic disorders

- Innovations in genomic technologies

Major Challenges:

- Restrictions in profitability from price controls

- nconsistent financial backing

Key Players: Thermo Fisher Scientific (U.S.), CooperSurgical (U.S.), Agilent Technologies (U.S.), PerkinElmer (U.S.), Roche Diagnostics (Switzerland), Qiagen (Germany), Natera, Inc. (U.S.), Oxford Gene Technology (UK), Abbott Laboratories (U.S.), Genea Biomedx (Australia), Progyny, Inc. (U.S.), Invitae Corporation (U.S.), Igenomix (Spain), MedGenome Labs (India), BGI Genomics (China), Yikon Genomics (China), LG Chem (South Korea), TMC Fertility (Malaysia), Reprogenetics (U.S.).

Global Preimplantation Genetics Diagnosis Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 61.9 million

- 2026 Market Size: USD 66.9 million

- Projected Market Size: USD 124.7 million by 2035

- Growth Forecasts: 8.1%

Key Regional Dynamics:

- Largest Region: North America (42.2% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Australia, Brazil, United Arab Emirates, United Kingdom

Last updated on : 27 August, 2025

Preimplantation Genetics Diagnosis Market - Growth Drivers and Challenges

Growth Drivers

-

Wide application in detecting genetic disorders: Heightened public and medical awareness about the inheritance of genetic deformities is pushing more couples to invest in the market to prevent passing on serious conditions. Testifying to the risk factor, in May 2024, the Centers for Disease Control and Prevention (CDC) unveiled that if any one of the parents contains an autosomal dominant disease or condition, then each child carries a 50% chance of developing a similar genetic mutation causing the ailment. On the other hand, the probability of inheriting two of such afflicted genes becomes 25% in the case of both parents being carriers.

-

Innovations in genomic technologies: Innovations that improved the accuracy and efficiency of PGD consolidate future expansion of the market. As advanced products introduced or cultivated by this sector offer greater convenience and cost-effectiveness, more eligible individuals and dedicated research facilities tend to amplify their expenditure and engagement in this category. Such a positive response further prompts companies to invest larger capital in extensive R&D, expanding the pipeline. Following the same pathway, in June 2023, Kindbody launched its in-house genetic testing division, Kindlabs, to deliver an optimized success rate of pregnancy.

-

Rising acceptance of IVF and ART: Broadened social acceptance and access to artificial conception procedures propel global-scale utilization of PGD services and components, thereby benefiting the market. This is also portrayed through the explosive augmentation of the global IVF industry, which is estimated to achieve a value of USD 45.74 billion by the end of 2037. Moreover, the importance of assisted reproductive technology (ART) in conducting these procedures successfully is fueling demand in this sector. Besides, the governing bodies are also supporting the increase in IVF adoption by enacting favorable policies and subsidies.

Current and Historic Trends in IVF and ART Utilization in Different Circumstances

Comparative Volume of Infertility Treatment Utilization in the U.S.

(2018-2022)

|

Metric |

States with Comprehensive IVF Insurance Mandates |

States without Comprehensive IVF Insurance Mandates |

|

Fertility Clinics per 100,000 women (ages 25–44) |

1.31 |

1 |

|

Cycle Volume per Clinic per Year |

478 |

267 |

|

Cycle Volume per Clinic (% difference) |

Not Specified |

80% lower than states with mandates |

|

IVF Utilization Increases by 1% Cost Drop |

3.2% increase in utilization |

Not Specified |

Source: NLM

Variation in Pricing and Spending in Different Regions Across the World

Cost Comparison of PGD Utilization

|

Year |

Cost/Expenditure |

Context/Description |

Notes |

Calculated Region |

|

2023 |

AED 40,000 (USD 11,000) |

Total cost range for PGD/PGT as a disease prevention approach |

Includes various treatment setups |

Global |

|

2023 |

¥39,230.71 (avg per live birth) |

Average direct medical cost per live birth with PGT-A |

Around 16.8% higher vs. conventional IVF |

China |

|

2022 |

(350 RMB per screening, ART+PGT included in total costs) |

Direct medical cost for genetic deafness screening with PGT |

Includes ART+PGT+Other |

China |

Source: PGDIS, NLM, and Frontiers

Challenges

-

Restrictions in profitability from price controls: As governing bodies concentrate their focus on enabling accessibility, the scope of securing lucrative profit margins from the market shrinks. Moreover, the implementation of strict pricing regulations makes it harder for manufacturers to gain profit while maintaining optimum quality. To address such issues, global leaders are now forming strategic alliances with insurance authorities to attain compliance with the cost-effectiveness threshold, even for their premium-priced commodities.

-

Inconsistent financial backing: The absence of adequate reimbursement policies that provide coverage for both producers and consumers imposes access-related disparity in the market. As the backing is rarely availed to patients for PGD except for high-risk chronic and hereditary ailments, a majority of the potential consumer base remains unattended. Thus, improvement and expansion in insurance policy and coverage are required to bridge this gap and gain maximum revenue from this sector.

Preimplantation Genetics Diagnosis Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.1% |

|

Base Year Market Size (2025) |

USD 61.9 million |

|

Forecast Year Market Size (2035) |

USD 124.7 million |

|

Regional Scope |

|

Preimplantation Genetics Diagnosis Market Segmentation:

Application Segment Analysis

The chromosomal abnormalities segment is poised to dominate the field of application in the preimplantation genetics diagnosis market with a 32.4% share over the assessed period. This is primarily attributable to the growing occurrence of genetic conditions, such as Down syndrome, Turner syndrome, and other aneuploidies, among newborns. The demography can be testified by the report presented at the 2024 PGDIS Conference in Malaysia, unveiling that more than 7 million people around the world are born with genetic disorders every year. Thus, the ability to detect these chromosomal issues in embryos during IVF at an early stage makes PGD a necessity for a successful and healthy pregnancy.

Technology Segment Analysis

Next-generation sequencing (NGS) is expected to hold the largest share of 42.6% in the market by the end of 2035. This leadership originates from the high accuracy, scalability, and wide applicability of this technology in comparison to traditional methods. NGS offers deeper genomic insights, faster turnaround times, and cost-effectiveness, which is escalating along with ongoing MedTech innovations. Besides, the capacity to identify multiple genetic conditions at a time makes it the preferred choice for large-scale fertility clinics and laboratories with higher workloads, which solidifies the segment's forefront position in this sector.

End user Segment Analysis

Diagnostic laboratories are anticipated to augment as the largest end-user segment in the preimplantation genetics diagnosis market throughout the discussed timeline. The large volume of genetic material from embryos that require processing and analysis is the major growth driver behind this proprietorship. As these labs are equipped with advanced technologies and skilled personnel, they are highly suitable for conducting complex tests with high precision. Moreover, their ability to deliver accurate and timely services, irrespective of sample volumes, is becoming an essential part of IVF procedures, which supports the continuous increase in demand for reliable genetic screening services.

Our in-depth analysis of the global preimplantation genetics diagnosis market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Test Type |

|

|

End user |

|

|

Application |

|

|

Product |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Preimplantation Genetics Diagnosis Market - Regional Analysis

North America Market Insights

North America is estimated to capture the highest share of 42.2% in the preimplantation genetics diagnosis market during the analyzed tenure. The advanced healthcare infrastructure, high ART adoption rates, and a strong presence of genetic testing pioneers are the foundational pillars of the region's dominance in this sector. The landscape also benefits from greater awareness about genetic disorders, increasing maternal age, and favorable reimbursement policies in selected regions. These factors are collectively fueling the widespread use of PGD in North America, which is stimulated further by NGS innovations and robust investment in fertility research.

The U.S. leads the regional market with a majority share in revenue generation. The country's augmentation in this sector is backed by a well-established network of fertility clinics and a strong emphasis on advanced reproductive technologies. This cohort of innovation can be exemplified by the commencement of Ovation Fertility's progress toward enhancing and expanding the genetic testing options, in collaboration with Genomic Prediction in October 2022. Such commercial success, coupled with the rising awareness of hereditary conditions, increased demand for PGD as part of IVF procedures across the nation.

Canada is establishing propagating as an emerging landscape of the regional preimplantation genetics diagnosis market. The increasing acceptance of ART and rising awareness of genetic health are cumulatively fueling the country's significance in this sector. The demand for PGD in Canada is also pledged to delayed family planning and a heightened focus on preventing hereditary disorders. Besides, government efforts to enhance the reproductive capacity of the country through reinforcement in public healthcare infrastructure and investment in medical research are also backing the gradual expansion of PGD services in Canada.

APAC Market Insights

Asia Pacific is poised to augment the global market as the fastest-growing region by the end of 2035. The massive population, increasing reproduction-related health issues, and growing awareness of genetic disorders are creating a surge in PGD services across the region. The remarkable improvement in healthcare systems, policies, and access is also benefiting the sector. Besides, the rapidly expanding medical tourism and a growing middle-class population are contributing to a greater cash inflow in this category. Moreover, as cultural attitudes shift and healthcare infrastructure continues to develop, APAC is expected to play an increasingly significant role in the global PGD market.

China is a hub of both the global producers of raw materials and a massive consumer base in the preimplantation genetics diagnosis market. The nation's amplifying citizen count, increasing infertility rates, and growing emphasis on the MedTech industry are contributing to its regional proprietorship. The rising average maternal age, coupled with a greater focus on preventing genetic disorders, has also increased interest in PGD among prospective parents. Further, as public awareness and regulatory clarity enhances, China is positioned to become a major contributor to the region's largest asset for PGD market expansion.

India is an influential landscape, filled with opportunities for the Asia Pacific market. It is primarily backed by the substantially expanding IVF industry and government initiatives to promote healthy pregnancy. The country's expanding healthcare and diagnostic infrastructure, coupled with the availability of cost-effective fertility treatments, has made ART-related assessments more accessible. Public efforts in support of this cohort can further be exemplified by the collaboration between AIIMS Jammu and 4baseCare in January 2025 to launch the Centre for Advanced Genomics and Precision Medicine in India.

Country-wise IVF & ART Adoption Trends

|

Country |

Indicator/Metric |

Latest Available Values |

Year |

|

Australia |

Number of IVF (ART) patients |

16,952 patients; 30,152 treatment cycles |

2022-2023 |

|

China |

Annual count of new IVF cycles |

3.7 million cycles performed |

2024 |

|

Japan |

ART cycles were performed nationwide |

543,630 cycles; 77,206 neonates born |

2022 |

Source: VARTA and NLM

Europe Market Insights

Europe is estimated to hold a steady position in the global preimplantation genetics diagnosis market between 2026 and 2035. The well-established medical systems, increasing infertility rates, and strong awareness of genetic disorders are the major growth drivers in this landscape. The region also benefits from advanced clinical innovations, widespread availability of ART, and standardized regulatory frameworks that ensure the safe and ethical use of PGD. Besides, continuous tech-based integration in healthcare and increasing government allocations to extensive fertility research are expected to expand the territory of Europe in this field.

Germany is a key landscape of the Europe market, which is highly attributable to high standards of medical care and the presence of global MedTech pioneers. Increasing occurrence and severity of genetic disorders, along with the rising average maternal age, also contribute to the rise in demand for PGD. Moreover, the country’s well-regulated IVF industry ensures the ethical use of reproductive technologies, where ongoing R&D and innovations in genetic testing technology secure large-scale utilization in this sector.

The UK is a prominent growth engine of the regional market, which is achieved through its advanced healthcare system and progressive regulatory framework for ARTs. Further, testifying to the high utilization and large consumer base, the Human Fertilisation and Embryology Authority (HFEA) unveiled that more than 77,500 IVF cycles were performed for approximately 52,400 patients in the UK in 2023 alone. This caused over 20,700 childbirths, which constitutes 3.1% of all births in the country during the same timeline. Such an evolving dynamics of the IVF industry underscores the country's potential to avail new opportunities for this sector.

Key Preimplantation Genetics Diagnosis Market Players:

- Illumina, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Thermo Fisher Scientific (U.S.)

- CooperSurgical (U.S.)

- Agilent Technologies (U.S.)

- PerkinElmer (U.S.)

- Roche Diagnostics (Switzerland)

- Qiagen (Germany)

- Natera, Inc. (U.S.)

- Oxford Gene Technology (UK)

- Abbott Laboratories (U.S.)

- Genea Biomedx (Australia)

- Progyny, Inc. (U.S.)

- Invitae Corporation (U.S.)

- Igenomix (Spain)

- MedGenome Labs (India)

- BGI Genomics (China)

- Yikon Genomics (China)

- LG Chem (South Korea)

- TMC Fertility (Malaysia)

- Reprogenetics (U.S.)

The commercial dynamics of the preimplantation genetics diagnosis market are primarily controlled by the presence of several key players focusing on innovation, technological advancements, and strategic partnerships. These moves to strengthen their position create a roadmap for both new entrants and investors willing to participate in this sector. Moreover, heavy investments in research and development are also being made to enhance the accuracy, speed, and cost-effectiveness of the sector's existing pipeline, securing the future with remarkable progress of the merchandise.

Here is a list of key players operating in the global market:

Recent Developments

- In May 2025, Roche collaborated with Broad Clinical Labs to develop and pilot groundbreaking applications using its recently unveiled next-generation sequencing (NGS) Sequencing By Expansion (SBX) technology. The alliance was intended to transform clinical genomics and biomedical discovery.

- In July 2023, Thermo Fisher Scientific launched two new next-generation sequencing-based options to support preimplantation genetic testing-aneuploidy. The Ion ReproSeq PGT-A Kit and the Ion AmpliSeq Polyploidy Kit are designed to be used for in vitro fertilization (IVF) and intracytoplasmic sperm injection (ICSI) research.

- Report ID: 8019

- Published Date: Aug 27, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Preimplantation Genetics Diagnosis Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.