Glioma Diagnosis and Treatment Market Outlook:

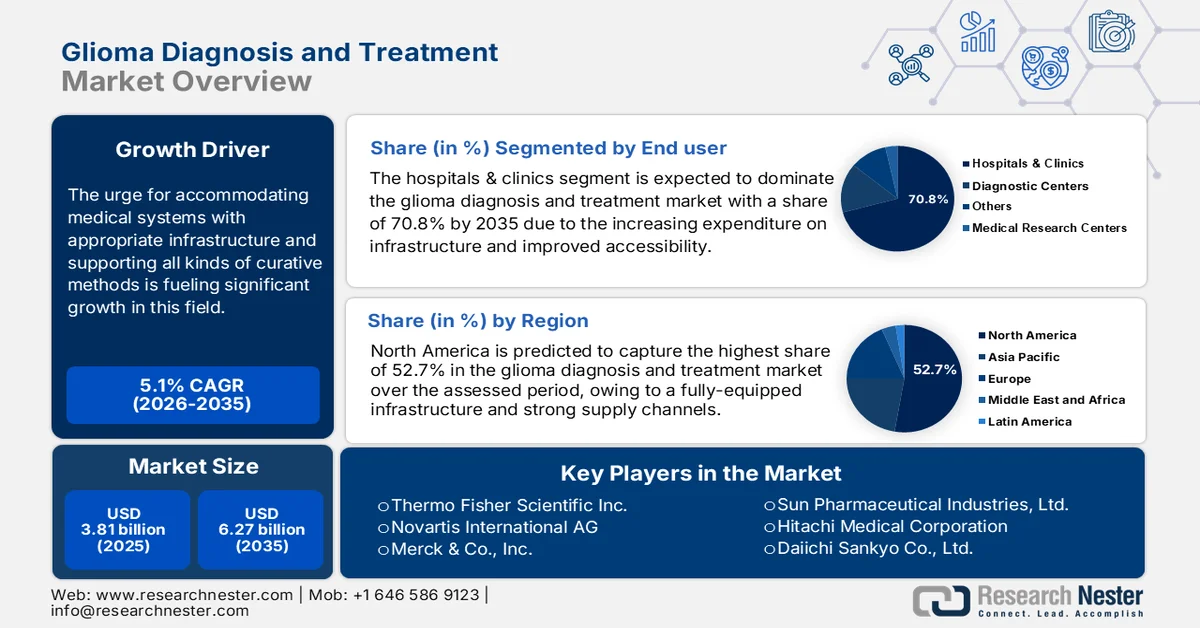

Glioma Diagnosis and Treatment Market size was valued at USD 3.81 billion in 2025 and is set to exceed USD 6.27 billion by 2035, registering over 5.1% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of glioma diagnosis and treatment is estimated at USD 3.98 billion.

As per the 2023 Journal of Brain and Spine, glioblastomas, a high-grade aggressive form of glioma, is one of the most common types of malignant central nervous system (CNS) tumors. This registered a worldwide prevalence rate of 3.19 per 100,000 habitats. Another NLM study from January 2023 disclosed that the world witnessed a 42.8% prevalence of glioma tumors. Subsequently, the urge to accommodate medical systems with appropriate infrastructure and support all kinds of curative methods is fueling significant growth in this field. Thus, the gradual rise in these deadly brain malignancy incidences concerns both public and private health organizations, pushing them to invest in the glioma diagnosis and treatment market.

However, a greater initial cost for advanced forms of this condition, such as glioblastomas (GBMs), has been observed in past years. As per the estimations from a Neuro-Oncology and Neurosurgical Oncology article, published in March 2024, the spending on new GBM cases was USD 95,377.0 for each patient. This was followed by a monthly cost of USD 18,053.0, over a survival tenure of 5.9 months, making it one of the most expensive conditions. Thus, the glioma diagnosis and treatment market is meticulously improvising its product line to offer better payers’ pricing, reducing the economic disparity and increasing adoption.

On this note, the 2021 publication of JCO Global Oncology introduced a comparatively affordable option for India, temozolamide + radiation, presenting a 90.0% and 80.0% decrease and increase in cost reduction and effectiveness, respectively. This promotes a new genre of pipelines with hybrid and accessible solutions, diversifying this sector and creating greater scopes for investment. In addition, it is encouraging global pioneers to engage in extensive R&D to find the most suitable solutions, increasing availability in the glioma diagnosis and treatment market.

Cost for GBM management in Europe, North America, and China (Except the U.S.) (2024)

|

Type of Therapy |

Mean Cost per Patient (USD) |

|

Surgical Resection |

10,042.0 |

|

Radiotherapy |

6,777.0 |

|

Combined Therapy (Surgery, Radiation, and Chemotherapy) |

62,602.0 |

Source: NLM Study

Key Glioma Diagnosis and Treatment Market Insights Summary:

Regional Highlights:

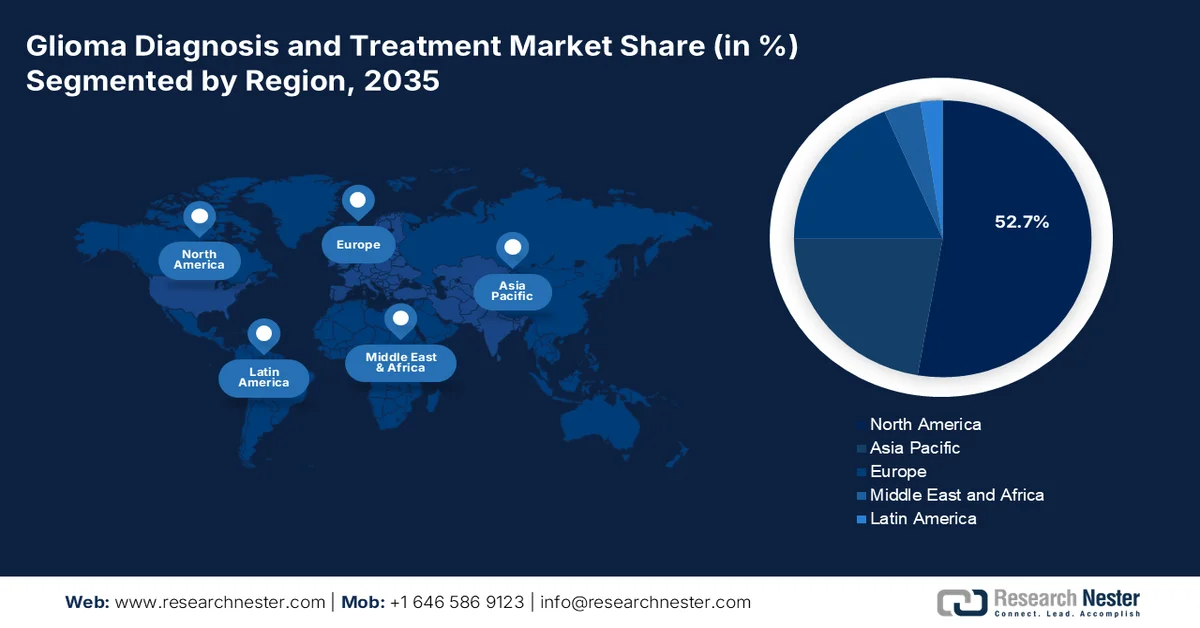

- North America is projected to dominate the glioma diagnosis and treatment market with over 52.7% revenue share by 2035, driven by well-established healthcare infrastructure and strong distribution networks supported by regulatory advancements.

- Asia Pacific is anticipated to witness notable growth through 2035, fueled by rapid advancements in precision medicine and increasing investments to address rising glioma mortality rates.

Segment Insights:

- Hospitals & clinics segment is set to account for over 70.8% share of the glioma diagnosis and treatment market by 2035, owing to expanding healthcare infrastructure, improved accessibility, and strong institutional funding support.

- Primary tumors segment is expected to hold the largest share throughout the forecast period, impelled by higher prevalence rates and the aggressive progression associated with astrocytomas, ependymomas, and oligodendrogliomas.

Key Growth Trends:

- Growing focus and investments in brain tumors

- Innovations in detection and curative methods

Major Challenges:

- Variability in types and market needs

- Hesitation along higher recurrence rates

Key Players: Agilent Technologies Inc., Waters Corporation, Shimadzu Corporation, PerkinElmer Inc., Bruker Corporation, ACD/Labs, SepSolve Analytical.

Global Glioma Diagnosis and Treatment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.81 billion

- 2026 Market Size: USD 3.98 billion

- Projected Market Size: USD 6.27 billion by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (52.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, United Kingdom, France

- Emerging Countries: China, India, Japan, South Korea, Germany

Last updated on : 25 February, 2026

Glioma Diagnosis and Treatment Market - Growth Drivers and Challenges

Growth Drivers

-

Growing focus and investments in brain tumors: The close association with brain carcinomas is forcing governing bodies across the globe to prioritize the widespread glioma diagnosis and treatment market. The efforts from several public associations are securing a continuously enlarging capital influx, fueling progress in this field. For instance, in March 2022, the Omnibus Spending Bill allocated increased funding for dedicated U.S.-based agencies for brain tumors. This enabled USD 1.0 billion, USD 45.0 billion, and USD 7 billion grants for the Advanced Research Projects Agency for Health (ARPA-H), National Institutes of Health (NIH), and National Cancer Institute (NCI). Such initiatives are also encouraging private firms to engage their resources.

- Innovations in detection and curative methods: The spreading awareness about the benefits of early and advanced detection and intervention is inflating demand in the glioma diagnosis and treatment market. Ongoing developments and discoveries are propelling exponential growth in this sector with improved patient outcomes and response. According to a WHO report, published in October 2023, the glioma sub-types encompassed the highest number of drug developments (156), in terms of childhood brain tumors, where 40.0% were undergoing phase-II trials. The disease type occupied 35.0% of the total 187 new therapeutics, including 70 drugs being orally consumables and 24 of them being child-friendly.

Challenges

-

Variability in types and market needs: This condition consists of a wide spectrum of mutational complexities and characteristics, which may not respond to the available solutions from the glioma diagnosis and treatment market. In addition, many of them are asymptomatic and heterogenetic, making it hard to detect and intervene at an earlier stage and hindering the effectiveness of existing treatments. To mitigate these issues, more intensive research is required, introducing tailored and developmental therapies and strategies.

- Hesitation along higher recurrence rates: The blood-brain barrier often eliminates the implementation of oral administration, pushing professionals to perform other aggressive therapeutics. Particularly for pediatric patients, applying these methods results in harsh health impacts. Additionally, the incidences of resistant tumors make it difficult for them to endure and respond to a long-term session. These may conjugatively discourage parents or families from adopting these therapeutics, limiting exposure in the glioma diagnosis and treatment market.

Glioma Diagnosis and Treatment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.1% |

|

Base Year Market Size (2025) |

USD 3.81 billion |

|

Forecast Year Market Size (2035) |

USD 6.27 billion |

|

Regional Scope |

|

Glioma Diagnosis and Treatment Market Segmentation:

End user Segment Analysis

In glioma diagnosis and treatment market, hospitals & clinics segment is set to dominate revenue share of over 70.8% by 2035. The increasing expenditure on infrastructure, coupled with improved accessibility, particularly in developed countries, is driving progress in this segment. On this note, the American Hospital Association reported in August 2022 that the annual financial contribution of hospitals to community benefits accounts for USD 110.0 billion. Many clinical studies display better outcomes due to early admissions to these institutions for treatment, making them a reliable destination for residents. In addition, the easy availability of essentials and government subsidies are influencing them to invest in this setting, inspiring companies to incorporate this network as a primary distribution channel.

Type Segment Analysis

In terms of type, the primary tumors segment is poised to hold the largest share of the glioma diagnosis and treatment market throughout the forecasted timeframe. The higher prevalence of this sub-type is the major growth factor in this segment. The majority of the primary class encompasses astrocytomas, ependymomas, and oligodendrogliomas with global prevalences of 20.3%, 3.2%, and 3.9% till 2023: as per NLM. Another report from the same source concluded that the average survival of GBM (a form of astrocytomas) is 9 months. This testifies to this segment’s growth with frequent occurrence and high mortality rates. Moreover, the aggressiveness and rapid progression of these disorders make them the top priority of medical systems.

Our in-depth analysis of the global glioma diagnosis and treatment market includes the following segments:

|

End user |

|

|

Type |

|

|

Diagnosis |

|

|

Treatment |

|

|

Grade |

|

|

Location |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Glioma Diagnosis and Treatment Market - Regional Analysis

North America Market Insights

North America in glioma diagnosis and treatment market is predicted to dominate over 52.7% revenue share by 2035. The region’s healthcare industry is pledged with a fully-equipped infrastructure and strong supply channels. This increases the accessibility and availability of this sector, securing a stable business flow. It also attracts foreign pharmacology giants to participate in this landscape. For instance, in April 2024, Telix Pharmaceuticals attained Fast Track designation for its investigational glioma imaging commodity, TLX101-CDx, from the U.S. FDA. The company opted for PharmaLogic Holdings Corp, a commercialization and production leader in North America, to distribute this product across the region. Thus, the presence of local support is also influencing progress in this marketplace.

Besides the supportive regulatory framework, the U.S. glioma diagnosis and treatment market is backed by rising healthcare expenditure and research-based organizations. The country has cultivated an efficient reservoir of essential tools and a network of academic excellence over the past decade to conduct fruitful and large-scale clinical trials, empowering discoveries. For instance, in June 2023, the University of California, Los Angeles (UCLA) participated in an international cohort studying the efficacy of vorasidenib. The evaluation helped this targeted therapy gain global recognition in slowing the progress of glioma with fewer adverse effects and neurological deficits. This not only assists in the authorization process but also helps pharma companies improve their product pipelines, making them more acceptable.

Canada is witnessing a sudden rise in GMB incidences among children, which is pushing it to magnify the focus on the glioma diagnosis and treatment market. The impact of this disease on the younger generation and its association with brain cancer concerns the national health authorities, fostering a stable capital influx in this sector. For instance, in May 2023, a team of scientists received a fund of USD 50 thousand for introducing tailored and less-toxic measures of treatment and identification for pediatric glioma adults with a heightened risk of brain cancer. The group of researchers believed that this initiative is capable of enabling a novel, age-stratified, and cost-effective guideline for molecular testing. These funds work as a financial cushion for future endeavors in this field.

APAC Market Insights

Asia Pacific is projected to register a notable growth in the glioma diagnosis and treatment market during the forecast period. The excellence and rapid progression in precision medicine have positively stimulated this sector. In this regard, the Research Nester estimations revealed that the APAC precision oncology industry is poised to register the highest share of 43.0% in global revenue generation by the end of 2035. Similarly, the region is also presenting a possibility to capture a remarkable share of 30.5% in the precision medicine business during the same timeline. Moreover, the growing mortality rates in low- and middle-income countries, within its territory, due to GBM are forcing authorities to implement adequate infrastructure, propelling demand in this field.

India is focusing on bringing affordability and improving availability in the glioma diagnosis and treatment market. This emerging pharmaceutical landscape is establishing a strong foundation of clinical discoveries in this sector through academic innovations and government affiliations. For instance, in December 2024, the Union Minister of State for Health and Family Welfare of India announced the commencement of research projects on CAR-T cell therapy under the supervision of the Biotechnology Industry Research Assistance Council (BIRAC). These projects are intended to produce affordable cell-based products, such as immunotherapeutic, to fight against cancers including glioblastoma.

China is also suffering from the steady incidence of GBM, pushing the government to accumulate resources from the glioma diagnosis and treatment market. According to an NLM study, published in September 2022, the overall survival of this condition was propounded to be 10.6 months and the mean age of occurrence to be 57 + 14 years. Despite the lower prevalence, the country intends to secure the older population by improving survival rates with sufficient supplies across the medical system. For instance, in May 2020, the National Medical Products Administration (NMPA) in China allowed the team of Zai Lab and Novocure to market Optune + temozolomide for treating both recurrent and new GBM cases.

Glioma Diagnosis and Treatment Market Players:

- Thermo Fisher Scientific Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Emcure Pharmaceuticals Ltd.

- Sigma-Aldrich Co.

- Pfizer Inc.

- Taj Pharmaceuticals Limited

- Novartis International AG

- Teva Pharmaceutical Industries Ltd.

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Merck & Co., Inc.

- Hoffmann-Le Roche AG

- Arbor Pharmaceuticals, LLC

- Sun Pharmaceutical Industries, Ltd.

- Amneal Pharmaceuticals. LLC

- AstraZeneca

- Carestream Health

- Foundation Medicine, Inc.

As the glioma diagnosis and treatment market has a limited product range, key players are cultivating new methodologies, such as cell-based therapy, to widen their portfolio. Many are also working on developing combination therapies to improve the efficacy and safety profile of the existing drug panel. For instance, in March 2023, Novartis gained FDA clearance for using the effect of Tafinlar (dabrafenib) and Mekinist (trametinib) to treat children aged 1 and older, suffering from low-grade glioma with a BRAF V600E mutation. The hybrid solution is indicated to be a suitable option to fulfill the need for systemic therapy in such cases. These pharmacological pioneers are:

Recent Developments

- In January 2025, Foundation Medicine attained approval from the FDA for FoundationOneCDx to be used as a companion diagnostic solution of OJEMDA (developed by Day One Biopharmaceuticals). It can enhance outcomes in treating pediatric, relapsed, or refractory low-grade glioma patients with the type II RAF inhibitor.

- In October 2024, Thermo Fisher Scientific earned FDA clearance for using companion diagnostic (CDx), Ion Torrent Oncomine Dx Target Test, before applying targeted therapy. This method is designed to identify or detect the eligibility of adults and children aged 12 and over with grade 2 IDH-mutant glioma for VORANIGO treatment.

- Report ID: 7379

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.