Nicotine Market Outlook:

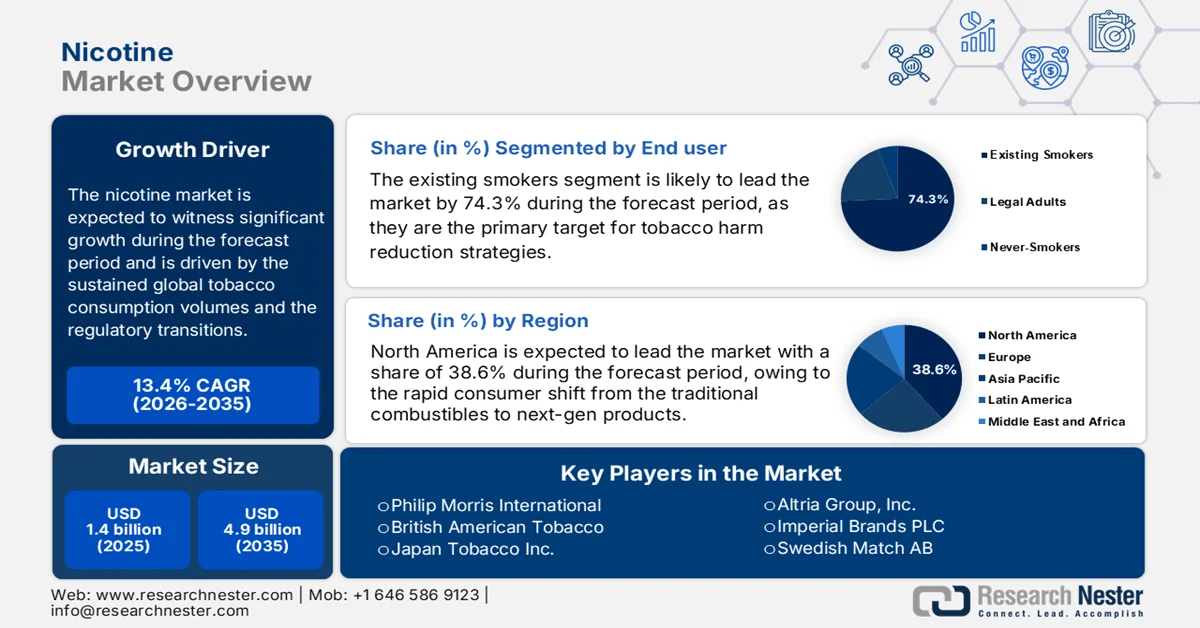

Nicotine Market size was valued at USD 1.4 billion in 2025 and is projected to reach USD 4.9 billion by the end of 2035, rising at a CAGR of 13.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of nicotine is estimated at USD 1.6 billion.

The global nicotine market continues to be shaped by the sustained global tobacco consumption volumes and the regulatory transitions toward reduced-risk nicotine delivery formats. According to the World Health Organization, in June 2025, data show that there are approximately 1.3 billion tobacco users worldwide, with tobacco responsible for 7 million deaths annually. Despite long term prevalence declines in several high-income countries, absolute user volumes remain significant due to the population growth in low and middle-income economies. The U.S. Food and Drug Administration has authorized selected nicotine products via the Premarket Tobacco Product Application pathway, signaling structured regulatory oversight that directly influences manufacturing, compliance investment, and distribution models. These regulatory mechanisms are central to the B2B supply chains, particularly for pharmaceutical-grade nicotine used in the nicotine replacement therapies and regulated disposable vape products.

Besides, the demand for nicotine replacement remains closely tied to the cessation initiatives supported by the public health agencies. As per the NLM study published in January 2023, nearly 68% of adult cigarette smokers in the U.S. reported wanting to quit, and about 55% made a quit attempt in the past year, reinforcing sustained institutional demand for regulated nicotine delivery alternatives. Moreover, the FDA-approved cessation medications, including the nicotine-based therapies, can double the likelihood of successful quitting when combined with behavioral support. Regulatory taxation frameworks also materially affect the nicotine value chain, underscoring the fiscal scale of the sector (fiscaldata.treasury.gov). Collectively, stable global user volumes, structured regulatory approvals, cessation program funding, and excise tax frameworks continue to define procurement, manufacturing compliance, and cross-border trade dynamics within the nicotine market.

Key Nicotine Market Insights Summary:

Regional Highlights:

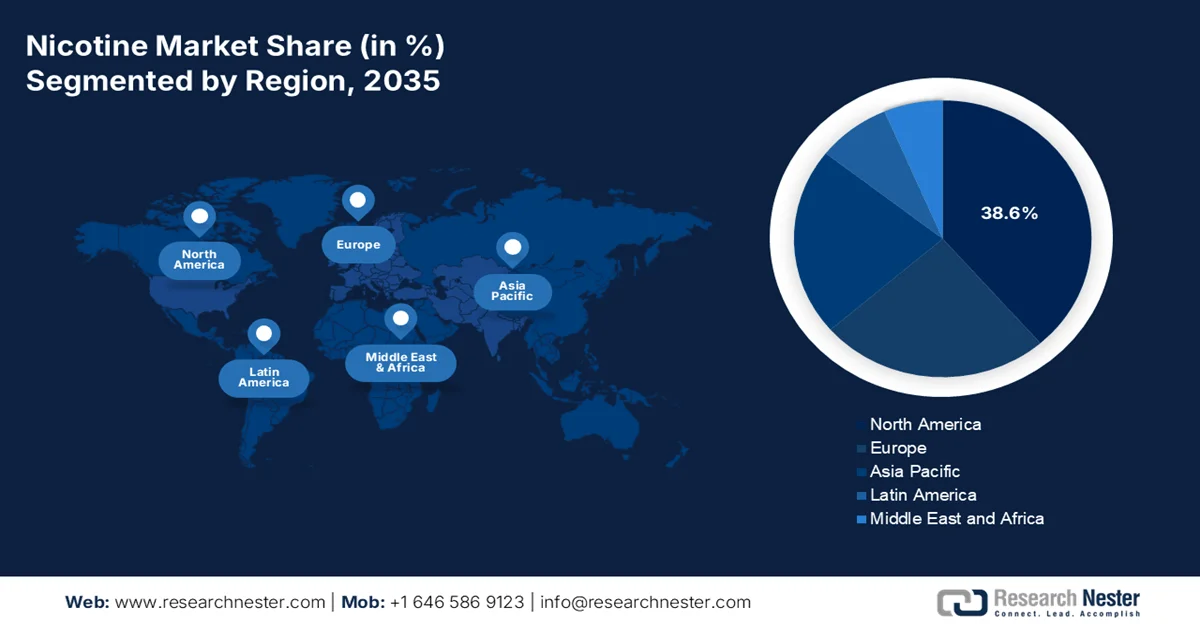

- The nicotine market in North America is anticipated to capture a 38.6% revenue share by 2035 propelled by the rapid consumer transition from traditional combustible cigarettes to next-generation nicotine products such as pouches and vapor devices.

- Asia Pacific is projected to register an 8.5% CAGR during 2026–2035 owing to the vast smoking population and accelerating adoption of heated tobacco and other next-generation nicotine products.

Segment Insights:

- Existing Smokers segment in the nicotine market is projected to hold a 74.3% share by 2035 fueled by increasing migration of established smokers from combustible cigarettes toward reduced-risk nicotine alternatives.

- Synthetic Nicotine segment is expected to maintain a dominant position by 2035 attributed to the cost efficiency of tobacco-leaf extraction and the entrenched production infrastructure of legacy tobacco companies.

Key Growth Trends:

- Public expenditure on tobacco control and cessation programs

- Federal regulatory authorization pathways

Major Challenges:

- Expensive regulatory approvals

- Raw material supply chain instability

Key Players: Philip Morris International, British American Tobacco, Japan Tobacco Inc., Altria Group, Inc., Imperial Brands PLC, Swedish Match AB, Universal Corporation, Pyxus International, Inc., Alkaloids of Australia, Broughton Nicotine Services, Fertin Pharma, Dr. Reddy's Laboratories.

Global Nicotine Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.4 billion

- 2026 Market Size: USD 1.6 billion

- Projected Market Size: USD 4.9 billion by 2035

- Growth Forecasts: 13.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Indonesia, Vietnam

Last updated on : 5 March, 2026

Nicotine Market - Growth Drivers and Challenges

Growth Drivers

- Public expenditure on tobacco control and cessation programs: Government-funded tobacco control frameworks influence the regulated nicotine market demand for approved cessation therapies. The U.S. CDC in September 2024 reported that the average state tobacco tax was USD 1.93 per pack. Moreover, the state tobacco taxes range from a high in New York of USD 5.35 per pack to a low in Missouri of 17 cents per pack. This supports quitlines counselling and pharmacotherapy access, increasing the institutional procurement of nicotine replacement therapies. At the federal level, the National Cancer Institute (NCI) confirms that combining medication with counseling significantly improves cessation success rates, reinforcing demand for approved nicotine formulations. Sustained public health appropriations create predictable B2B demand from healthcare systems, pharmacies, and public procurement agencies, particularly in North America and Europe, where reimbursement pathways are formalized.

- Federal regulatory authorization pathways: The regulatory clearance under the U.S. FDA is shaping the product in the nicotine market supply chains. The FDA has authorized specific e-cigarette products after scientific review, while denying millions of non-compliant applications. This structured approval system consolidates the demand for manufacturers able to meet the compliance, toxicology, and manufacturing standards. The FDA's September 2025 data shows that the Center for Tobacco Products is funded primarily via user fees exceeding USD 712,000,000, enabling enforcement and product review activities. Further, the regulatory filtration reduces the informal supply while increasing the institutional grade nicotine sourcing.

- Government research funding on tobacco harm and addiction: The public research funding supports scientific evaluation of nicotine addiction and cessation technologies. The NIH funds extensive tobacco-related research via the National Institute on Drug Abuse. NIH supported studies confirm that FDA approved cessation medications can significantly improve the quit success rates when combined with behavioral therapy. Moreover, the evidence-based validation strengthens the payer confidence and regulatory authorization of nicotine-based therapies. Further, the publicly funded clinical research provides data supporting procurement eligibility within public healthcare systems. Continued federal research allocations signal sustained institutional oversight and structured market evolution rather than contraction.

Challenges

- Expensive regulatory approvals: The single most significant barrier in the nicotine market in the U.S. is the premarket tobacco product application process enforced by the FDA. This requirement mandates that any new tobacco or nicotine product must receive agency authorization before legally marketing or selling it. The process is not only scientifically rigorous, demanding extensive toxicology and behavioral studies, but also financially prohibitive, often costing millions of dollars per product.

- Raw material supply chain instability: Manufacturers face significant hurdles in securing a consistent and high-quality supply of raw materials, particularly tobacco leaf, which is highly susceptible to environmental factors. Climate change has introduced greater weather variability, leading to production deficits in key agricultural regions. This instability drives up input costs and disrupts inventory management, making it difficult to meet global demand consistently.

Nicotine Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

13.4% |

|

Base Year Market Size (2025) |

USD 1.4 billion |

|

Forecast Year Market Size (2035) |

USD 4.9 billion |

|

Regional Scope |

|

Nicotine Market Segmentation:

End user Segment Analysis

The existing smokers are leading the sub-segment and are poised to hold the share value of 74.3% by the end of 2035. This demographic represents the primary target for tobacco harm reduction strategies implemented by the major manufacturers. According to the NLM study published in March 2022, the prevalence of adult smoking is 32.6% among men. Unlike the never smokers, this group possesses an established nicotine dependency but is increasingly motivated to migrate away from the combustible cigarettes due to health concerns and social pressures. Companies are customizing their marketing and product development specifically in the heated tobacco and vaping to mimic the sensory experience and ritualistic aspects of smoking, thereby lowering the psychological barrier to switching.

Source Segment Analysis

The synthetic nicotine is leading the segment in the nicotine market. This sustained leadership is driven by the cost efficiency of established agricultural supply chains and the deeply ingrained manufacturing processes of legacy tobacco companies. Extracting nicotine from the tobacco leaves remains significantly cheaper than complex chemical synthesis, allowing manufacturers to maintain higher margins on mass market products such as modern oral pouches and combustible cigarettes. Further, the taste profile of the tobacco-derived nicotine is often preferred by traditional smokers switching to reduced-risk products. Additionally, regulatory familiarity and long-standing quality control frameworks surrounding tobacco-derived nicotine further strengthen its dominance, as manufacturers can leverage existing compliance pathways and production infrastructure to scale efficiently across global markets.

Application Segment Analysis

The recreation is leading the application segment in the nicotine market and is rooted in the psychoactive and sensory pleasure that nicotine delivers, stress relief, mild euphoria, and cognitive focus, which consumers seek as part of their daily lifestyle rather than merely as a medical treatment for addiction. The rise of sleek, discreet devices and flavored modern oral pouches has rebranded nicotine consumption as a lifestyle accessory rather than a clinical habit. This recreational framing drives a higher frequency of use and brand loyalty as consumers experiment with the different flavors and nicotine strengths for enjoyment. According to the CDC October 2022 data, nearly 84.9% of youth e-cigarette users reported using flavored products concerning from a regulatory standpoint, statistically validates the massive consumer pull toward the recreational and sensory aspects of the nicotine experience.

Our in-depth analysis of the nicotine market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Source |

|

|

Distribution Channel |

|

|

Application |

|

|

Concentration |

|

|

Format |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Nicotine Market - Regional Analysis

North America Market Insights

The North America dominating and is poised to hold the regional revenue share of 38.6% by the end of 2035. The nicotine market is driven by the rapid consumer shift from the traditional combustibles to next-gen products such as nicotine pouches and vapor products. The market is defined by the dominant cigarette sector and a high-growth smokeless category. The key trends include intense regulatory activity at both the federal and state levels, focusing on product authorization, flavor restrictions, and taxation. Moreover, the FDA's increasing efficiency in reviewing premarket tobacco product applications for nicotine pouches is creating a more structured market for authorized products. This regulatory environment shows a competitive landscape for the nicotine market in North America.

Strong public health scrutiny and substantial fiscal involvement is driving the demand for the nicotine market in U.S. According to the CDC, September 2024 data, over 16 million U.S. people are living with a smoking-related disease, reinforcing sustained federal and state investment in prevention and cessation programs. Besides, youth usage remains a regulatory focal point. As per the data from the CDC in October 2022, nearly 2.55 million middle and high school students reported using e-cigarette including 14.1% of high school students, with nearly 85% of individuals using flavored products, and more than half preferring disposable devices. Further, the FDA's September 2025 data has reported that in FY2026, the estimated TTB tax revenues accounted for nearly 84% of tobacco class allocations. On the other hand, U.S. is the largest imported of nicotine products of worth USD 149 million in 2024, based on OEC 2024 report. These revenue streams show that the nicotine market in the U.S. remains a significant taxable consumption category, supporting a stable regulation-driven market.

U.S. Federal Tobacco Tax Revenue Allocation by Product Class

|

Tobacco Product Class |

FY 2026 Est. Taxes from TTB |

Allocation by Class (Percent) |

Amount Per Quarter |

|

Cigarettes |

3,217,108,951 |

83.9380% |

149,409,640 |

|

Cigars |

520,672,010 |

13.5849% |

24,181,122 |

|

Snuff |

54,379,422 |

1.4188% |

2,525,464 |

|

Chewing Tobacco |

2,482,311 |

0.0647% |

115,116 |

|

Pipe Tobacco |

36,633,065 |

0.9557% |

1,701,146 |

|

Roll-Your-Own Tobacco |

1,440,209 |

0.0375% |

66,750 |

|

Total |

3,832,715,968 |

99.9996% |

177,999,288 |

|

|

|

Total 2026 Amount |

711,997,152 |

Source: FDA September 2025

The regulatory controls on vaping devices and nicotine concentration standards are driving the nicotine market in Canada. As per the Government of Canada report published in August 2025, Canada has enforced a maximum nicotine concentration limit of 20 mg/mL under the Nicotine Concentration in Vaping Products Regulations, directly affecting formulation strategies for both freebase nicotine and nicotine salt products. Moreover, the Health Canada research detected an average of 22 chemicals and nine flavoring agents per vaping product, reinforcing ongoing federal scrutiny over ingredient disclosure and aerosol emissions. The market includes both open systems (refillable tanks/pods) and closed systems (pre-filled cartridges or disposables), with flavored, nicotine-containing liquids dominating legal retail offerings. Further, Canada’s regulatory framework supports controlled market growth, limiting high-strength imports and non-compliant disposable formats.

APAC Market Insights

The Asia Pacific is the fastest growing and is expected to register a CAGR of 8.5% during the assessed period 2026 to 2035. The nicotine market in the Asia Pacific is defined by its immense scale, cultural integration, and stark regulatory diversity, making it the most complex and critical region for the global manufacturers. Additionally, APAC presents a dual reality, where the traditional combustible products continue to dominate the volume due to deep cultural entrenchment and massive population bases, while simultaneously serving as the global epicenter for the next-gen product adoption, mainly in heated tobacco. further the absence of a harmonized regulatory framework across the region makes the companies to maintain distinct portfolios, supply chains, and compliance strategies for each country, balancing the need to cater to established smoking rituals with the imperative to invest in the innovative categories that will define the region's future growth.

The scale and persistence of tobacco dependence are promoting the growth of the nicotine market in China. According to the NLM study in May 2022, nearly 50% of current smokers in China are estimated to be tobacco-dependent, translating to a projected 183.5 million tobacco-dependent individuals, the majority of whom are men. This creates a substantial and recurring consumption base. The dynamic nature of the smoker pool is driven by cessation, mortality, and new smoker entry sustains volume stability despite public health efforts. Reducing the national smoking prevalence below 20% requires treatment access at an unprecedented scale, implying long-term demand for cessation therapies, behavioral interventions, and regulated nicotine alternatives. Further, the significant expansion potential for pharmaceutical-grade nicotine products and structured cessation programs enables a positive impact on the market growth.

The nicotine market in Japan is institutionally structured and production-driven, supported by a large adult smoker base and state-linked industry participation. The data from the Tobacco Atlas published in 2025 reports that the country has recorded 18.3 million adult smokers sustaining a domestic consumption pool. Moreover, the cigarette production reached 86.87 billion units, indicating a continued high manufacturing capacity. On the other hand, the Tobacco Tactics in December 2025 data depicts that Japan Tobacco (JT), whose parent entity is 33% owned by the Japanese government, operates under a consolidated domestic and international business model, reinforcing regulatory alignment and fiscal interdependence. Further, the combination of strong domestic production, government-linked ownership, and sustained adult consumption supports stable market value, with incremental growth increasingly tied to reduced-risk product transition rather than combustible expansion.

Europe Market Insights

The nicotine market in Europe is growing significantly and is defined by a complex interplay between progressive public health objectives and persistent consumer demand, creating a dynamic and highly regulated environment. The region is aiming to reduce the smoking population, which serves as the overarching policy framework influencing all member states. This has led to a fragmented regulatory landscape where the harmonized EU directives on taxation, advertising, and product packaging coexist with increasingly divergent national approaches to novel products such as nicotine pouches, heated tobacco, and e-liquid. Manufacturers operating in this region must navigate a patchwork of rules. Therefore, the market is mature and evolving, where compliance, scientific substantiation, and adaptability are the primary drivers of commercial success.

The nicotine market in Germany is driven by the regulated e-cigarette adoption within the structured EU-aligned framework. According to the Global State of Tobacco Harm Reduction data in November 2025, Germany recorded 1.4 million current vapers, representing 2% of the adult population, with higher prevalence seen in men, while the daily use remains limited at 0.6%. Moreover, the e-cigarettes are legal, subject to excise duty (up to 10% of cigarette tax levels), capped at 20 mg/ml nicotine concentration, and limited to 2 ml tank capacity, with mandatory product notification and child-resistant packaging requirements. However, the cessation motivation remains uneven, with 51.2% of smokers not motivated to quit, particularly among those over 65 (64.4%). These behavioral and regulatory factors suggest moderate compliance-driven growth concentrated in the adult substitution.

Structured and regulation aligned growth is propelling the demand for the nicotine market in the UK. As per the data from the Government of the UK in September 2022, the tobacco and regulated products regulations have allowed the nicotine vaping liquid strength to 20mg/mL, indicating strong compliance and limited penetration of non-compliant high-strength imports. Further, the consumer behavior trends also suggest product stabilization and gradual nicotine moderation 34% of vapers reported reducing the nicotine strength over time, while 8.1% increased the strength, supporting the demand for the mid- to lower-strength formulations. Moreover, the proportion of users uncertain about nicotine strength has slightly increased, signaling opportunities for clearer labeling and retail guidance. Flavor concentration remains commercially significant, with fruit (35.3%) leading preferences. These data support a steady expansion-driven growth in the market.

UK Vaper Flavor Preferences Distribution

|

Flavor Category |

Share of Vapers (%) |

|

Fruit |

35.3% |

|

Menthol / Mint |

22.5% |

|

Tobacco |

20.9% |

|

Other Flavors |

21.3% |

Source: Government of the UK, September 2022

Key Nicotine Market Players:

- Philip Morris International (U.S.)

- British American Tobacco (UK)

- Japan Tobacco Inc. (Japan)

- Altria Group, Inc. (U.S.)

- Imperial Brands PLC (UK)

- Swedish Match AB (Sweden)

- Universal Corporation (U.S.)

- Pyxus International, Inc. (U.S.)

- Alkaloids of Australia (Australia)

- Broughton Nicotine Services (UK)

- Fertin Pharma (Denmark)

- Dr. Reddy's Laboratories (India)

- Chemnovatic (Poland)

- Alchem International (India)

- Nicobrand Ltd (UK)

- KT&G Corporation (South Korea)

- Shanghai Tobacco Group Co. (China)

- TVS (India)

- Achieve Life Sciences (U.S.)

- Rapid Dose Therapeutics (Canada)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Philip Morris International is the dominant player and has positioned itself in the global nicotine market by pivoting away from its traditional cigarette business. The company has invested billions of dollars in the development and commercialization of its IQOS platform, a heated tobacco system that has become a cornerstone of the reduced-risk product segment. In 2024, the company made a net revenue of USD 37,878 billion.

- British American Tobacco employs a multi-category strategy to maintain its leadership in the global nicotine market, positioning itself as a total nicotine company. Its portfolio spans traditional cigarettes, modern oral nicotine pouches, vapor products, and heated tobacco. By diversifying its offering, BAT reduces the risk across regulatory changes and shifting consumer preferences. In 2024, the company made a revenue of USD 34.53 billion.

- Japan Tobacco Inc. leverages its strong domestic heritage to compete vigorously in the global nicotine market, focusing heavily on heated tobacco sticks as the future of the industry. Its Ploom TECH and Ploom X devices represent the company’s core investment in innovation, designed to capture market share in the key regions such as Europe and Asia.

- Altria Group Inc commands a formidable position in the U.S. nicotine market via its ownership of the immensely popular Marlboro brand. Recognizing the secular decline in smoking altria has pivoted toward smoke-free products via strategic investments and partnerships, most notably its stake in the e-vapor company.

- Imperial Brands PLC maintains its relevance in the competitive nicotine market by focusing on a portfolio of stable cigarette brands while actively expanding its next-gen product lineup. The company’s strategy centers on agility and targeted investment mainly in its Blu Vapor brand and its modern oral nicotine pouch offerings in key European markets.

Here is a list of key players operating in the global market:

The competitive landscape of the global nicotine market is currently defined by a seismic shift from the traditional combustible products towards the reduced-risk alternatives and pharmaceutical-grade applications. Legacy tobacco giants are actively transforming their portfolios, leveraging their massive distribution networks to pus next gen products like heated tobacco units, nicotine pouches, and e-liquids. Similarly, a new wave of specialized manufacturers, mainly from India and China, is dominating the active pharmaceutical ingredients supply chain for nicotine replacement therapies and modern oral products. Strategic initiatives are heavily focused on vertical integration to control quality and costs, mergers and acquisitions to absorb innovative startups, and heavy investment in R&D to create novel nicotine salts and synthetic nicotine, which bypass some traditional tobacco regulations and cater to evolving consumer preferences for cleaner and more discreet consumption. For example, in October 2025, Rapid Dose Therapeutics releases a nicotine business update and extends the collaboration with the International Nicotine Partner.

Corporate Landscape of the Nicotine Market:

Recent Developments

- In June 2025, Achieve Life Sciences has announced the partnership with Omnicom to execute integrated, data-driven launch of the first potential new treatment for nicotine dependence in nearly two decades

- In October 2024, British American Tobacco (BAT) launched a version of its Velo nicotine pouches using synthetic nicotine in the United States, David Waterfield, president of the company’s U.S. subsidiary Reynolds American, said on Wednesday.

- In October 2024, Dr Reddy’s Laboratories completes acquisition of Nicotinell and related brands. The acquisition expands Dr. Reddy's presence in the global nicotine replacement therapy market, with Nicotinell products now under its umbrella.

- Report ID: 8412

- Published Date: Mar 05, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.